Off-Plan Real Estate, & Cytonn Weekly #21/2023

By Cytonn Research, May 28, 2023

Executive Summary

Fixed Income

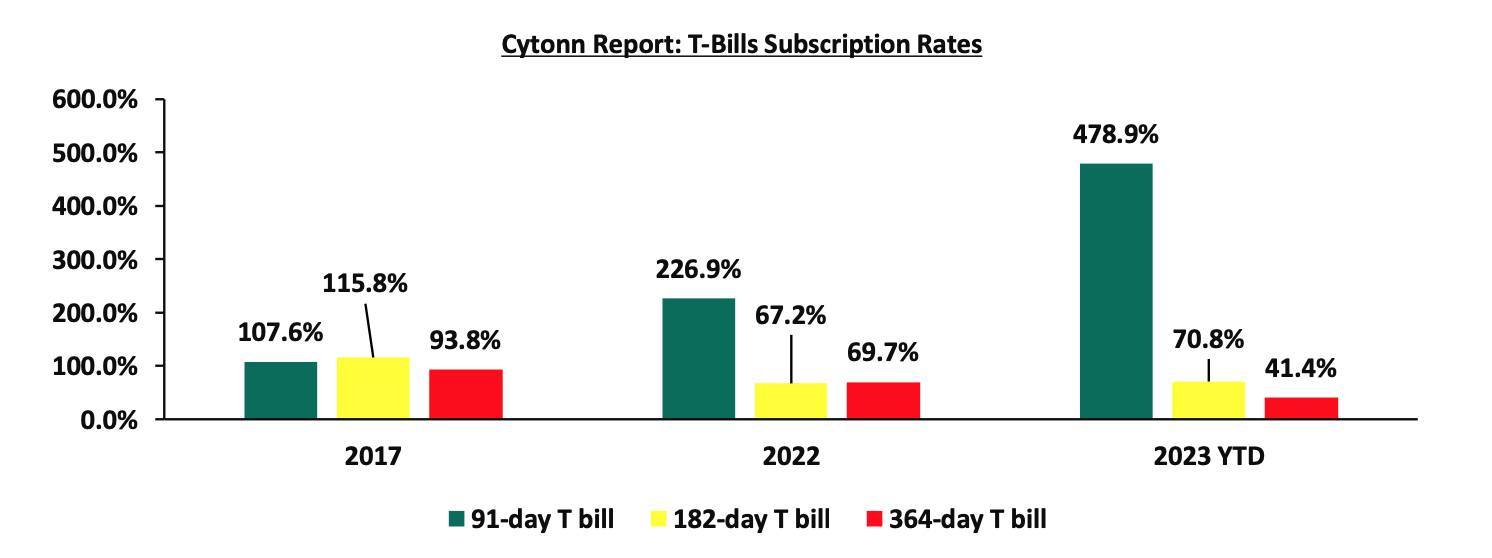

During the week, T-bills were undersubscribed for first time in four weeks, with the overall subscription rate coming in at 91.9%, down from an oversubscription rate of 150.1% recorded the previous week. Investor’s preference for the shorter 91-day paper persisted as they sought to avoid duration risk, with the paper receiving bids worth Kshs 14.2 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 356.1%, lower than the 602.3% recorded the previous week. The subscription rates for the 182-day and 364-day paper declined to 40.4% and 37.6%, from the 42.2% and 77.1% recorded the previous week, respectively. The government accepted bids worth Kshs 21.0 bn out of the Kshs 22.0 bn total bids received, translating to an acceptance rate of 95.4%. The yields on the government papers were on an upward trajectory, with the yields on the 364-day paper, 182-day and 91-day papers increasing by 6.7 bps, 13.5 bps and 31.4 bps to 11.5%, 11.1% and 10.8%, respectively;

In the primary bond market, the Central Bank of Kenya released the tap sale results for the Treasury bond FXD1/2023/003 with tenor to maturity of 3 years. In line with our expectations, the bond was oversubscribed, receiving bids worth Kshs 27.2 bn, against the offered Kshs 20.0 bn, translating to an oversubscription rate of 136.0%. This is partly attributable to investors’ preference for shorter dated bonds as they seek to avoid duration risk. The government accepted bids worth Kshs 27.2 bn, translating to an acceptance rate of 100.0%. Key to note, both the weighted average yield of accepted bids and the coupon rate came at 14.2%.;

During the week, the International Monetary Fund (IMF) announced that it had reached a staff level agreement with Kenyan authorities to conclude the fifth reviews of Kenya’s economic program under the Extended Fund Facility (EFF) and Extended Credit Facility (ECF) arrangements. This will allow Kenya to access financing of USD 410.0 mn (Kshs 56.7 bn) once the formal review is completed by July 2023;

Additionally, we are projecting the y/y inflation rate for May 2023 to come in at the range of 7.9%-8.3%, despite inflation easing to 7.9% in April 2023 from 9.2% in March 2023. Our projection is mainly on the back of increased fuel prices as well as the elevated food prices in the country;

Also, the Monetary Policy Committee (MPC) is set to meet on Monday, 29 th May 2023, to review the outcome of its previous policy decisions and recent economic developments, and to decide on the direction of the Central Bank Rate (CBR). We expect the MPC to maintain the CBR at 9.50% with their decision mainly being supported by the ease on y/y inflation in April 2023 to 7.9%, from 9.2% recorded in March 2023 and the need to support the economy by adopting an accommodative policy that will ease financing activities;

Equities

During the week, the equities market recorded mixed performance with NASI and NSE 25 declining by 0.6% and 1.2% respectively, while NSE 20 gained by 1.4%, taking the YTD performance to losses of 23.1%, 11.2% and 19.0% for NASI, NSE 20 and NSE 25, respectively. The equities market performance was mainly driven by losses recorded by large cap stocks such as Co-operative Bank, Equity Group, Diamond Trust Bank (DTB-K) and BAT of 6.9%, 3.9%, 2.2% and 1.8%, respectively. The losses were however mitigated by gains recorded by stock such as Bamburi, NCBA Group, Standard Chartered bank and ABSA bank of 9.2%, 6.1%, 4.1% and 3.8% respectively;

During the week, two listed banks released their Q1’2023 financial results with NCBA Group recoding an increase in its Core Earnings Per Share of 48.5%, while KCB Group recorded a decline of 0.1% in its Core Earnings Per Share;

Real Estate

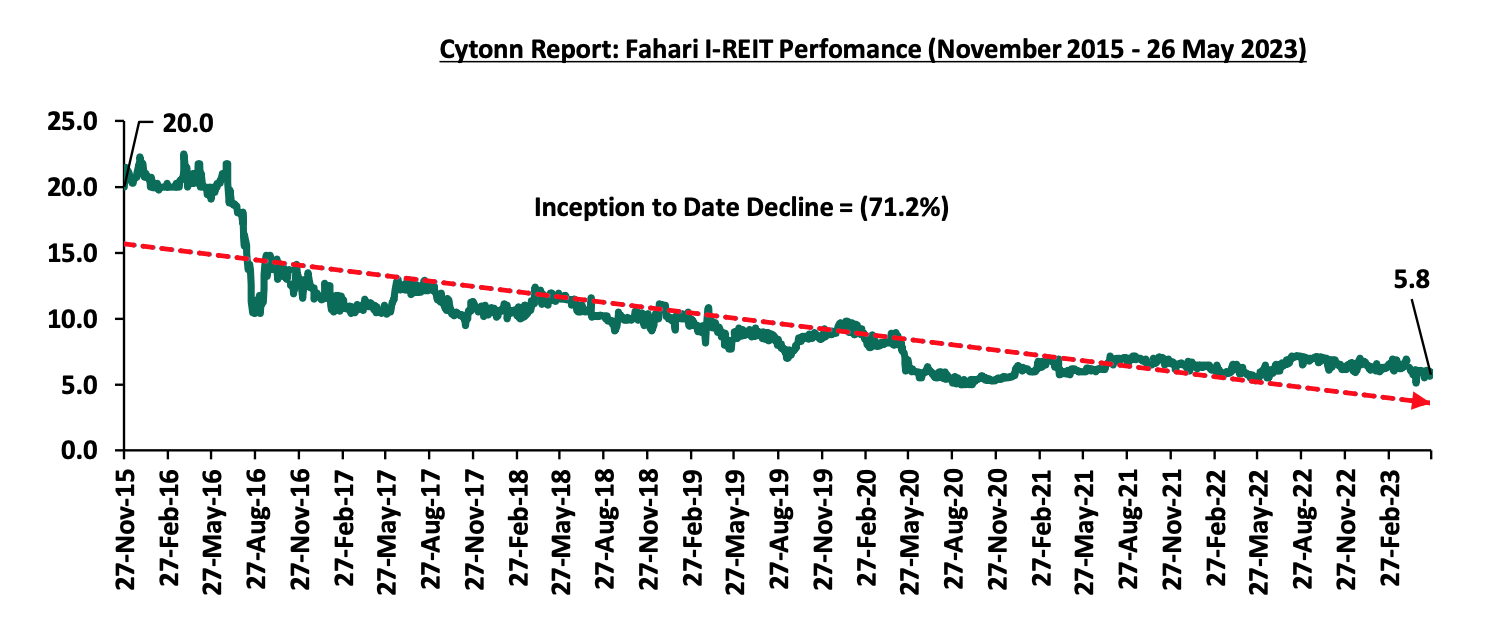

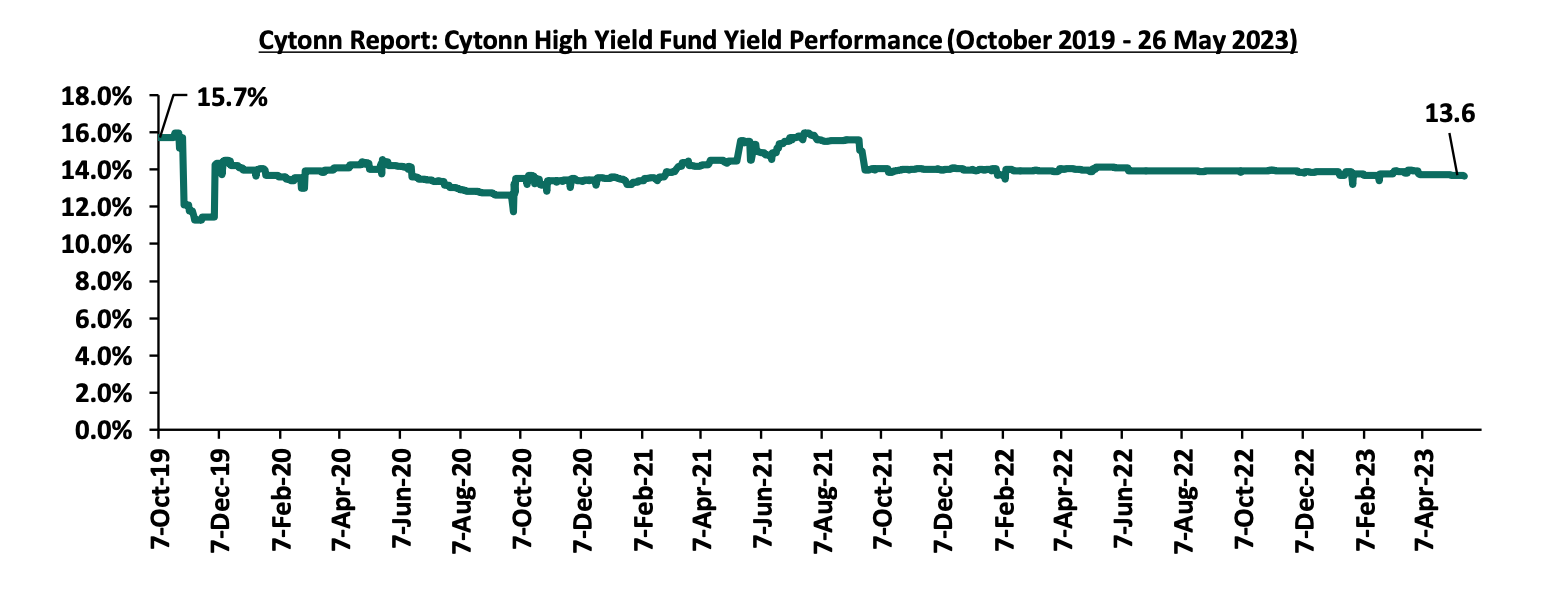

During the week, Actis Limited, a global private equity firm, announced that it had shut down two offices located in Nairobi, Kenya and Cape Town, South Africa. In the Regulated Real Estate Funds, under the Real Estate Investment Trusts (REITs) segment, Fahari I-REIT closed the week trading at an average price of Kshs 5.8 per share in the Nairobi Securities Exchange, representing a 4.0% decline from Kshs 6.0 per share recorded the previous week. On the Unquoted Securities Platform as at 26 May 2023, Acorn D-REIT and I-REIT closed the week trading at Kshs 23.9 and Kshs 21.6 per unit, respectively, a 19.4% and 7.9% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. In addition, Cytonn High Yield Fund (CHYF) closed the week with an annualized yield of 13.6%, representing a 0.1% points decline from the 13.7% yield recorded the previous week;

Focus of the Week

Off-plan investment in the Real Estate sector has emerged as an enticing opportunity, offering a mutually beneficial platform for both developers and buyers. This concept involves the sale and purchase of properties that are yet to be constructed or are still under development, with the completion and ownership transfer being governed by agreed contractual obligations. Over the years, off-plan investment has gained significant traction offering an advantageous platform for both developers and homebuyers. Through a contractual agreement, the buyer becomes the owner of a Real Estate unit with predetermined characteristics and specifications, whether it is an existing property or one under construction. The developer, in turn, is obligated to complete the construction within the agreed-upon timeframe, while the buyer is obliged to pay the price either in an expedited or deferred manner. The growing popularity of off-plan investment signifies its potential to reshape the Real Estate market by providing a promising avenue for profitable ventures and fulfilling the housing needs of prospective homeowners.

This week, we review Off-Plan program in Real Estate Development and Investing in order to identify the financial and marketing challenges being faced by such program in Kenya. Additionally, we shall undertake a case study of countries where off plan projects have been successfully implemented and the off-plan program is firmly and strictly regulated in the Real Estate sector. From the case studies, we shall give our recommendations of what can be done to improve the regulatory framework for off plan investments in Kenya;

Investment Updates:

- Weekly Rates:

- Cytonn Money Market Fund closed the week at a yield of 11.16%. To invest, dial *809# or download the Cytonn App from Google Playstore here or from the Appstore here;

- Cytonn High Yield Fund closed the week at a yield of 13.66% p.a. To invest, email us at sales@cytonn.com and to withdraw the interest, dial *809# or download the Cytonn App from Google Playstore here or from the Appstore here;

- We continue to offer Wealth Management Training every Wednesday and every third Saturday of the month, from 9:00 am to 11:00 am, through our Cytonn Foundation. The training aims to grow financial literacy among the general public. To register for any of our Wealth Management Trainings, click here;

- If interested in our Private Wealth Management Training for your employees or investment group, please get in touch with us through wmt@cytonn.com;

- Cytonn Insurance Agency acts as an intermediary for those looking to secure their assets and loved ones’ future through insurance namely; Motor, Medical, Life, Property, WIBA, Credit and Fire and Burglary insurance covers. For assistance, get in touch with us through insuranceagency@cytonn.com;

- Cytonn Asset Managers Limited (CAML) continues to offer pension products to meet the needs of both individual clients who want to save for their retirement during their working years and Institutional clients that want to contribute on behalf of their employees to help them build their retirement pot. To more about our pension schemes, kindly get in touch with us through pensions@cytonn.com;

Real Estate Updates:

- For an exclusive tour of Cytonn’s real estate developments, visit: Sharp Investor's Tour, and for more information, email us at sales@cytonn.com;

- Phase 3 of The Alma is now ready for occupation and the show house is open daily. To join the waiting list to rent, please email properties@cytonn.com;

- For Third Party Real Estate Consultancy Services, email us at rdo@cytonn.com;

- For recent news about the group, see our news section here;

Hospitality Updates:

- We currently have promotions for Staycations. Visit cysuites.com/offers for details or email us at sales@cysuites.com;

Money Markets, T-Bills Primary Auction:

During the week, T-bills were undersubscribed for first time in four weeks, with the overall subscription rate coming in at 91.9%, down from an oversubscription rate of 150.1% recorded the previous week. Investor’s preference for the shorter 91-day paper persisted as they sought to avoid duration risk, with the paper receiving bids worth Kshs 14.2 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 356.1%, lower than the 602.3% recorded the previous week. The subscription rates for the 182-day and 364-day paper declined to 40.4% and 37.6%, from the 42.2% and 77.1% recorded the previous week, respectively. The government accepted bids worth Kshs 21.0 bn out of the Kshs 22.0 bn total bids received, translating to an acceptance rate of 95.4%. The yields on the government papers were on an upward trajectory, with the yields on the 364-day paper, 182-day and 91-day papers increasing by 6.7 bps, 13.5 bps and 31.4 bps to 11.5%, 11.1% and 10.8%, respectively. The chart below compares the overall average T- bills subscription rates obtained in 2017, 2022 and 2023 Year to Date (YTD):

In the primary bond market, the Central Bank of Kenya released the tap sale results for the Treasury bond FXD1/2023/003 with tenor to maturity of 3 years. In line with our expectations, the bond recorded an oversubscription rate of 136.0%, partly attributable to investors’ preference for shorter dated bonds as they seek to avoid duration risk. The government issued the bond seeking to raise Kshs 20.0 bn for budgetary support. The tap sale of the bond received bids worth Kshs 27.2 bn, with government accepting bids worth Kshs 27.2 bn, translating to an acceptance rate of 100.0%. Key to note, both the weighted average yield of accepted bids and the coupon rate came at 14.2%.

Money Market Performance:

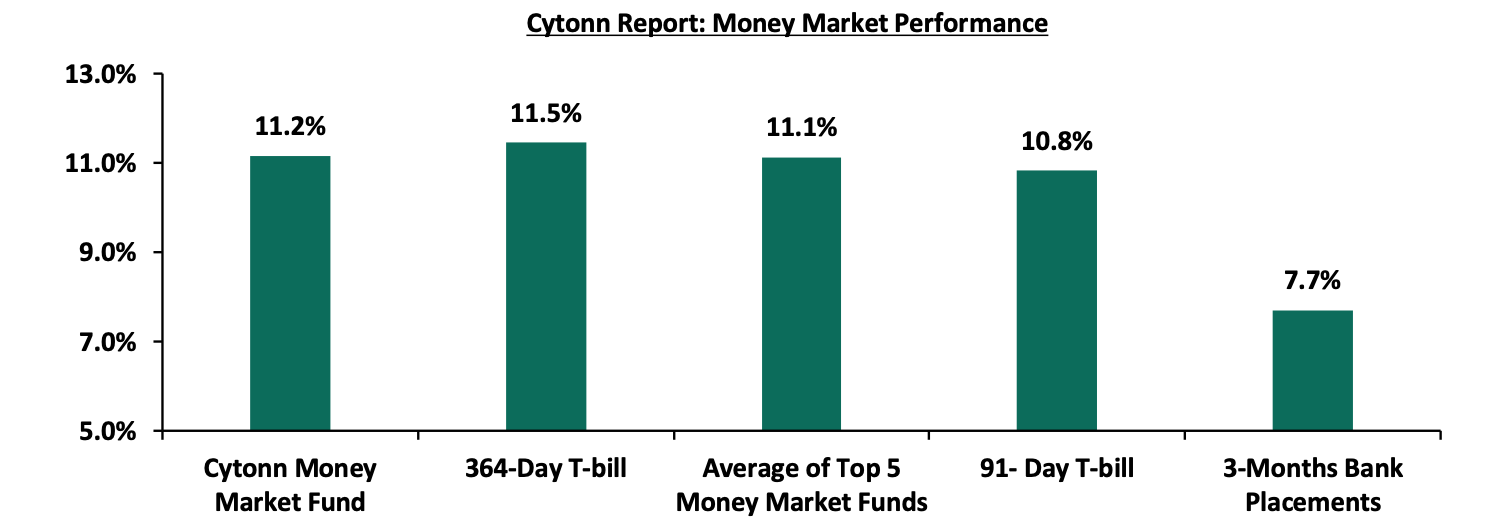

In the money markets, 3-month bank placements ended the week at 7.7% (based on what we have been offered by various banks), while the yields on the 364-day and 91-day paper increased by 6.7 bps and 31.4 bps to 11.5% and 10.8% respectively. The yield of Cytonn Money Market Fund increased by 2.0 bps to 11.2%, up from 11.1% recorded in the previous week, while the average yields of Top 5 Money Market Funds increased by 18.0 bps to 11.1%, up from 11.0% recorded the previous week.

The table below shows the Money Market Fund Yields for Kenyan Fund Managers as published on 26 May 2023:

|

Cytonn Report: Money Market Fund Yield for Fund Managers as published on 26 May 2023 |

||

|

Rank |

Fund Manager |

Effective Annual Rate |

|

1 |

Etica Money Market Fund |

11.6% |

|

2 |

Cytonn Money Market Fund (dial *809# or download the Cytonn app) |

11.2% |

|

3 |

Madison Money Market Fund |

11.0% |

|

4 |

Dry Associates Money Market Fund |

11.0% |

|

5 |

Enwealth Money Market Fund |

10.9% |

|

6 |

GenAfrica Money Market Fund |

10.9% |

|

7 |

Apollo Money Market Fund |

10.8% |

|

8 |

Jubilee Money Market Fund |

10.8% |

|

9 |

AA Kenya Shillings Fund |

10.5% |

|

10 |

Old Mutual Money Market Fund |

10.3% |

|

11 |

Co-op Money Market Fund |

10.1% |

|

12 |

NCBA Money Market Fund |

10.1% |

|

13 |

Sanlam Money Market Fund |

10.1% |

|

14 |

Kuza Money Market fund |

10.1% |

|

15 |

Nabo Africa Money Market Fund |

10.0% |

|

16 |

Zimele Money Market Fund |

9.9% |

|

17 |

GenCap Hela Imara Money Market Fund |

9.7% |

|

18 |

British-American Money Market Fund |

9.6% |

|

19 |

CIC Money Market Fund |

9.6% |

|

20 |

ICEA Lion Money Market Fund |

9.6% |

|

21 |

Orient Kasha Money Market Fund |

9.4% |

|

22 |

KCB Money Market Fund |

9.2% |

|

23 |

Absa Shilling Money Market Fund |

8.9% |

|

24 |

Mali Money Market Fund |

8.3% |

|

25 |

Equity Money Market Fund |

7.5% |

Source: Business Daily

Liquidity:

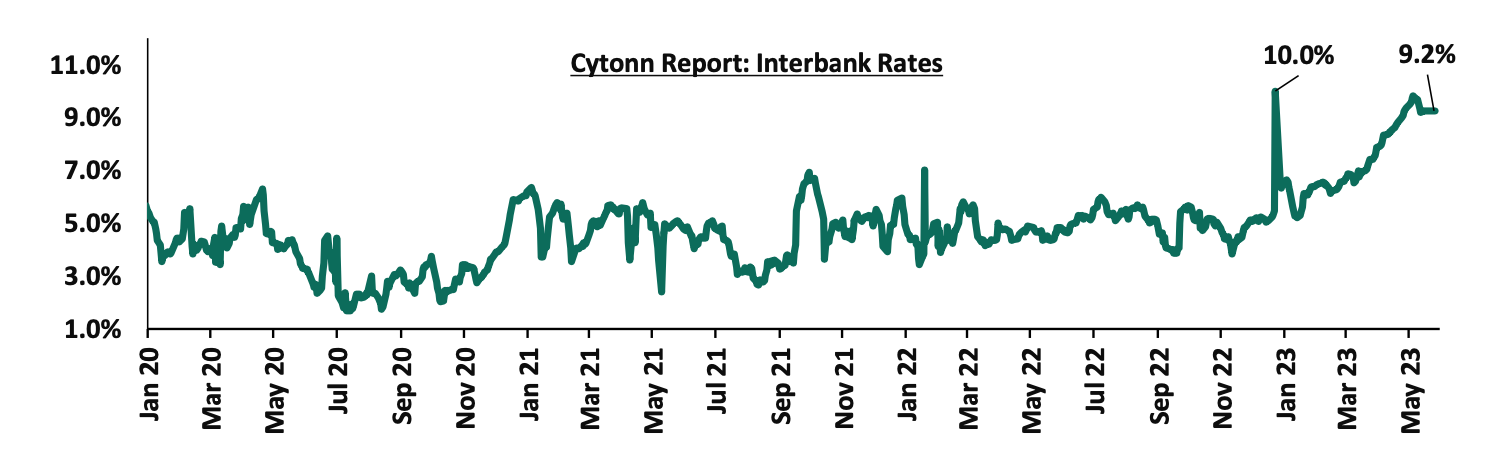

During the week, liquidity in the money markets remained tightened, with the average interbank rate remaining relatively unchanged at 9.2% similar to what was recorded the previous week, partly attributable to tax remittances that offset government payments. The average interbank volumes traded increased by 13.7% to Kshs 25.7 bn, from Kshs 22.6 bn recorded the previous week. The chart below shows the interbank rates in the market over the years:

Source: CBK

Kenya Eurobonds:

During the week, the yields on Eurobonds recorded mixed performance with the yield on the 10-year Eurobond issued in 2014 gaining by 0.3% points to 15.7%, from 15.4%, recorded the previous week, while the yield on the 7-year Eurobond issued in 2019 declining the most by 1.0% points to 13.3%, from 14.3% recorded the previous week. The table below shows the summary of the performance of the Kenyan Eurobonds as of 18 May 2023;

|

Cytonn Report: Kenya Eurobonds Performance |

||||||

|

|

2014 |

2018 |

2019 |

2021 |

||

|

Date |

10-year issue |

10-year issue |

30-year issue |

7-year issue |

12-year issue |

12-year issue |

|

Amount Issued (USD) |

2.0 bn |

1.0 bn |

1.0 bn |

0.9 bn |

1.2 bn |

1.0 bn |

|

Years to Maturity |

1.1 |

4.8 |

24.8 |

4.0 |

9.0 |

11.1 |

|

Yields at Issue |

6.6% |

7.3% |

8.3% |

7.0% |

7.9% |

6.2% |

|

02-Jan-23 |

12.9% |

10.5% |

10.9% |

10.9% |

10.8% |

9.9% |

|

1-May-23 |

20.6% |

14.1% |

12.7% |

15.5% |

13.2% |

12.4% |

|

18-May-23 |

15.4% |

12.6% |

12.0% |

14.3% |

12.4% |

11.7% |

|

19-May-23 |

14.7% |

12.3% |

11.8% |

13.5% |

12.2% |

11.4% |

|

22-May-23 |

15.3% |

12.3% |

11.8% |

13.5% |

12.2% |

11.3% |

|

23-May-23 |

15.0% |

12.1% |

11.6% |

13.2% |

12.0% |

11.2% |

|

24-May-23 |

15.5% |

12.1% |

11.7% |

13.4% |

12.1% |

11.2% |

|

25-May-23 |

15.7% |

12.1% |

11.6% |

13.3% |

12.1% |

11.2% |

|

Weekly Change |

0.3% |

(0.5%) |

(0.4%) |

(1.0%) |

(0.3%) |

(0.5%) |

|

MTD change |

(4.9%) |

(2.0%) |

(1.1%) |

(2.2%) |

(1.1%) |

(1.2%) |

|

YTD Change |

2.8% |

1.7% |

0.7% |

2.4% |

1.3% |

1.3% |

Source: Central Bank of Kenya (CBK) and National Treasury

Kenya Shilling:

During the week, the Kenya Shilling depreciated by 0.6% against the US dollar to close the week at Kshs 138.3, from Kshs 137.5 recorded the previous week, partly attributable to the persistent dollar demand from importers, especially oil and energy sectors against a slower supply of hard currency. On a year to date basis, the shilling has depreciated by 12.0% against the dollar, adding to the 9.0% depreciation recorded in 2022. We expect the shilling to remain under pressure in 2023 as a result of:

- High global crude oil prices on the back of persistent supply chain bottlenecks coupled with high demand,

- An ever-present current account deficit estimated at 4.9% of GDP in twelve months to January 2023, from 5.6% recorded in a similar period last year,

- The need for Government debt servicing which continues to put pressure on forex reserves given that 63.0% of Kenya’s External debt was US Dollar denominated as of December 2022, and,

The shilling is however expected to be supported by:

- Diaspora remittances standing at a cumulative USD 1,335.9 mn in 2023 as of April 2023, albeit 3.1% lower than the USD 1,378.9 mn recorded over the same period in 2022, and,

- The tourism inflow receipts that came in at USD 268.1 bn in 2022, a significant 82.9% increase from USD 146.5 bn inflow receipts recorded in 2021.

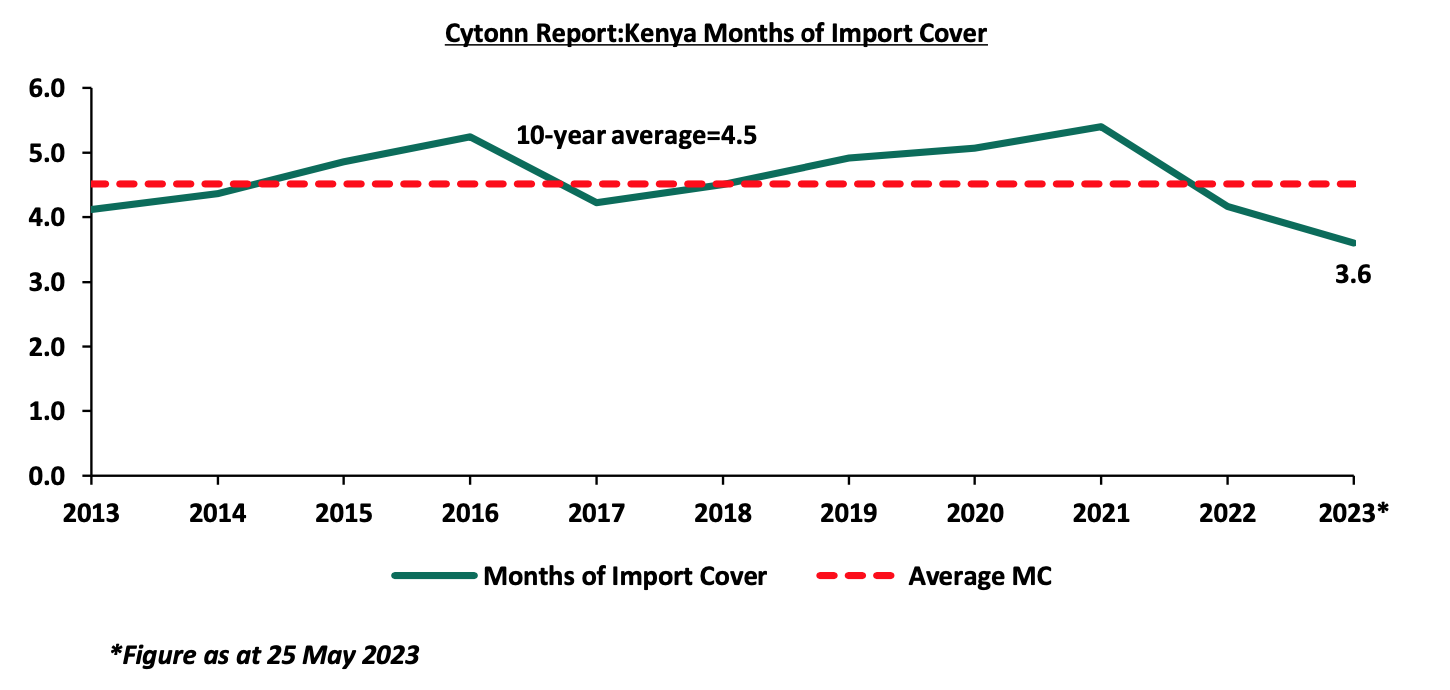

Key to note, Kenya’s forex reserves increased by 2.9% to USD 6.5 bn as of 25 May 2023, from USD 6.3 bn as of 18 May 2023. As such, it represented a 3.6 months of import cover, a notable increase from the 3.5 months of import cover recorded the previous week. However, the forex reserves remained below the statutory requirement of maintaining at least 4.0-months of import cover. Key to note, should the government receive the USD 410.0 mn from International Monetary Fund (IMF), upon completion of the fifth reviews of Kenya’s economic programme under the Extended Fund Facility (EFF) and Extended Credit Facility (ECF) arrangements, the forex reserve months of import cover is expected to increase to 3.8 months from the current 3.6 months. The chart below summarizes the evolution of Kenya months of import cover over the last 10 years:

Weekly Highlights:

- Kenya’s International Monetary Fund (IMF) Loan facility

During the week, the International Monetary Fund (IMF) announced that it had reached a staff level agreement with Kenyan authorities on the following;

- To conclude the fifth reviews of Kenya’s economic program under the Extended Fund Facility (EFF) and Extended Credit Facility (ECF) arrangements,

- An argumentation of access under the EFF/ECF totaling 75.0% of quota of USD 544.3 mn (Kshs 75.3 bn) given challenging global financing conditions,

- Extension of the duration of the EFF/ECF arrangements by 10 months to April 2025 to allow sufficient time for meeting the programme objectives, and,

- A new 20-month Resilience and Sustainability Facility (RSF) arrangement with access also of 75.0% of the quota that will run in parallel with the EFF/ECF arrangements until April 2025.

Upon the expected completion of the fifth reviews by July 2023, Kenya will have immediate access of USD 410.0 mn (Kshs 56.7 bn) of the approved loan facility totaling to USD 2.3 bn that was announced in April 2021 including from augmentation of access under the ECF/EFF. This will bring total IMF financial support disbursed under the EFF/ECF to USD 2,051.2 mn (Kshs 283.7 bn). Additionally, with the EFF/ECF augmentations and the RSF support, the total IMF commitment under these arrangements would be USD 3.5 bn (Kshs 486.7 bn)

The table below shows the funding the government has received so far out of the original amount:

|

Cytonn Report: International Monetary Fund (IMF) EFF and ECF Financing Programme |

||

|

Date |

Amount Received (USD mn) |

Amount Received (Kshs bn, 1 USD = Kshs 138.3) |

|

Apr-21 |

307.5 |

42.5 |

|

Jun-21 |

407.0 |

56.3 |

|

Dec-21 |

258.1 |

35.7 |

|

Jul-22 |

235.6 |

32.6 |

|

Nov-22 |

433.0 |

59.9 |

|

Jul-23 |

*410.0 |

56.7 |

|

Total Amount Received |

2,051.2 |

283.7 |

|

Amount Pending |

1,470.0 |

204.2 |

|

*Expected funds upon IMF management and executive board approval |

||

The government budget has been under pressure on the back of low revenue collection as well as tight financing conditions, evidenced by the total revenue collected as at the end of April 2023 amounting to Kshs 1,639.8 bn, equivalent to 78.4% of the revised estimates of Kshs 2,192.0 bn for FY’2022/2023 and was 89.8% of the prorated estimates of Kshs 1,826.7 bn. As such, the funding is expected to support the economy amid backdrop of the country’s economic growth as evidenced by the GDP of 4.8% in 2022, which was lower than the 7.6% growth recorded in 2021. Additionally, upon disbursement, the financing is expected to boost the country’s dwindling foreign exchange reserves which currently stand at USD 6.5 mn representing 3.6 months of import cover, below the minimum statutory requirement of 4.0 months of import cover. The Resilience and Sustainability Facility (RSF) is also expected to aid in addressing challenges posed by climate change, while also strengthening the macroeconomic stability.

Notably, the IMF commended the government move to bring back liquidity to the interbank market for foreign exchange which is expected to support exchange rate flexibility and backstop the external position. Going forward, the IMF noted the need for the government to fast track reforms in State Owned Enterprises (SOEs) which continues to drain on budget resources, among the SOEs include, Kenya Airways and Kenya Power and Lighting Company.

- May 2023 Inflation Projection

We are projecting the y/y inflation rate for May 2023 to come in at a range of 7.9%-8.3%, despite inflation easing to 7.9% in April 2023 from 9.2% in March 2023. Our projection is mainly on the back of:

- Increased Fuel Prices -Fuel prices increased by 1.9%, 4.0% and 10.4% to Kshs 182.7, Kshs 168.4 and Kshs 161.1 per litre of Super Petrol, Diesel and Kerosene, respectively, for the period between 15th May 2023 to 14th June 2023. The increase was attributed to the government’s decision to completely fuel subsidy which was cushioning the citizens from high fuel prices. As such, given that fuel is major input to most sectors, we expect the cost of production to increase and consequently lead to high consumer prices, and,

- Elevated food prices - Food prices have remained elevated mainly on the back of uneven weather patterns as well as supply chain bottleneck experienced globally. The elevated prices were evidenced by the 10.1% y/y increase in the prices of food and non-alcoholic beverages in April 2023. Given that the food is a major input in inflation index, we expect the resulting high prices to underpin inflationary pressures.

Notably, the high commodity prices in the country are also attributed to the sustained depreciation of the Kenya Shilling which has inflated import bill. As a result, manufactures pass on the cost to consumers through hike in commodity prices. Going forward, we expect inflationary pressures to persist in the short term, however to ease in the medium term to CBK’s target range of 2.5% to 7.5% aided by easing in global commodity prices and easing of domestic food prices on account of favorable weather conditions. We also expect the measures taken by the government to subsidize major inputs of agricultural production such as fertilizers to lower the cost of farm inputs and support the easing of inflation in the long term

- May 2023 MPC Meeting

The Monetary Policy Committee (MPC) is set to meet on Monday, 29 th May 2023, to review the outcome of its previous policy decisions and recent economic developments, and to decide on the direction of the Central Bank Rate (CBR). We expect the MPC to maintain the CBR at 9.50% with their decision mainly being supported by;

- The ease on y/y inflation in April 2023 to 7.9%, from 9.2% recorded in March 2023, despite remaining above the CBK’s target range of 2.5%-7.5%. Additionally, food inflationary pressures are expected to slow in the near term, aided by continued rains as well as importation of duty-free staples such as maize, rice, cooking oil and sugar. However, elevated inflation is expected to endure in the short to medium following the increase in fuel prices after the government completely removed the fuel subsidies which was aimed at cushioning consumers from high fuel prices. As such, we expect the MPC to maintain the CBR as the current monetary stance still transmits in the economy,

- The continued deprecation of the shilling does not provide room for any easing, hence MPC has to maintain the elevated rates to protect the shilling, and,

- The need to support the economy by adopting an accommodative policy that will ease financing activities. Additional hike in the CBR rate might slow down economic activities given the current macro and business environment fundamentals cannot accommodate further hikes.

Notably, despite the macroeconomic indicators being inclined towards an increase in the Central Bank Rate with focus on easing inflation to the CBK target range while supporting the Kenyan shilling, the committee must be cautious as the country’s economic growth has been declining. This is evidenced by Kenya’s economy recording a 4.8% growth in 2022 compared to the 7.6% expansion in 2022. Therefore, we expect the MPC to maintain the CBR at 9.50% as they monitor the impact of the policy measures, as well as developments in the global and domestic economy.

For a more detailed analysis, please see our May 2023 MPC note.

Rates in the Fixed Income market have been on upward trend given the continued government’s demand for cash as well as tight liquidity in the money market. The government is on target with its prorated borrowing target of Kshs 387.7 bn having borrowed Kshs 387.8 bn of the revised domestic borrowing target of Kshs 425.1 bn for the FY’2022/2023. We believe that the projected budget deficit of 5.7% is relatively ambitious given the downside risks and deteriorating business environment occasioned by high inflationary pressures. Further, revenue collections are lagging behind, with total revenue as at April 2023 coming in at Kshs 1.6 tn in the FY’2022/2023, equivalent to 74.8% of its revised target of Kshs 2.2 tn and 89.8% of the prorated target of Kshs 1.8 tn. Therefore, we expect a continued upward readjustment of the yield curve in the short and medium term, with the government looking to bridge the fiscal deficit through the domestic market. Owing to this, our view is that investors should be biased towards short-term fixed-income securities to reduce duration risk.

Market Performance:

During the week, the equities market recorded mixed performance with NASI and NSE 25 declining by 0.6% and 1.2% respectively, while NSE 20 gained by 1.4%, taking the YTD performance to losses of 23.1%, 11.2% and 19.0% for NASI, NSE 20 and NSE 25, respectively. The equities market performance was mainly driven by losses recorded by large cap stocks such as Co-operative bank, Equity Group, Diamond Trust Bank (DTB-K) and BAT of 6.9%, 3.9%, 2.2% and 1.8%, respectively. The losses were however mitigated by gains recorded by stock such as Bamburi, NCBA Group, Standard Chartered bank and ABSA bank of 9.2%, 6.1%, 4.1% and 3.8% respectively.

During the week, equities turnover declined by 14.8% to USD 10.2 mn, from USD 12.0 mn, recorded the previous week, taking the YTD turnover to USD 418.8 mn. Foreign investors remained net sellers with a net selling position of USD 1.7 mn, from a net selling position of USD 1.4 mn recorded the previous week, taking the YTD net selling position to USD 52.4 mn.

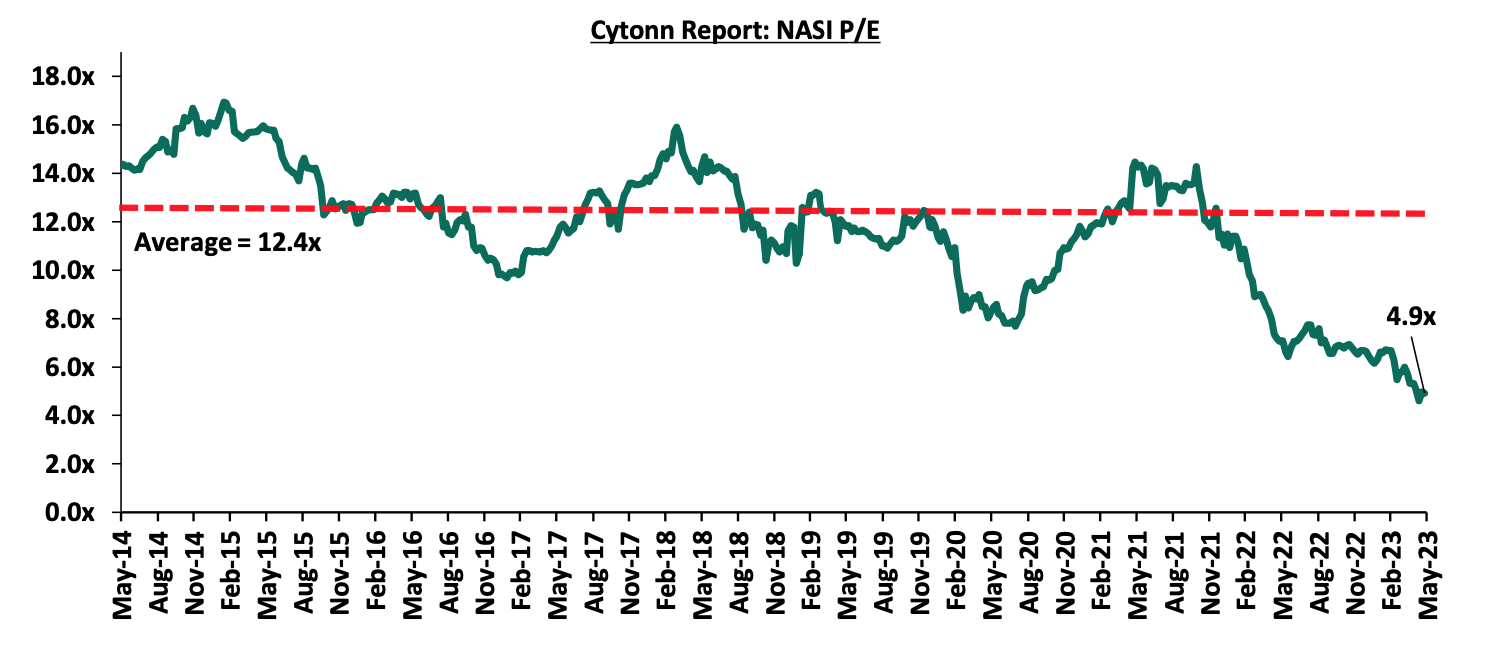

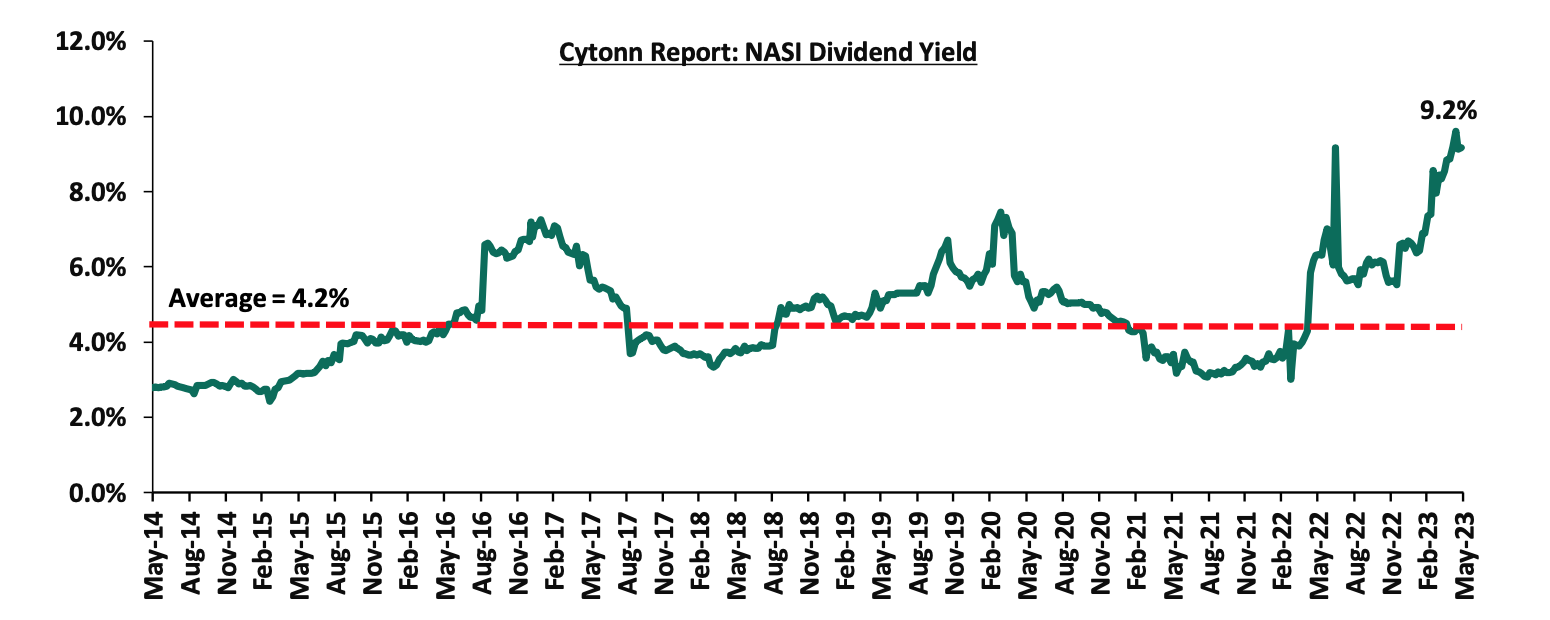

The market is currently trading at a price to earnings ratio (P/E) of 4.9x, 60.3% below the historical average of 12.4x. The dividend yield stands at 9.2%, 5.0% points above the historical average of 4.2%. Key to note, NASI’s PEG ratio currently stands at 0.6x, an indication that the market is undervalued relative to its future growth. A PEG ratio greater than 1.0x indicates the market is overvalued while a PEG ratio less than 1.0x indicates that the market is undervalued. The charts below indicate the historical P/E and dividend yields of the market;

Weekly Highlights:

- Shorecap III, LP acquires 20.0% stake in Credit Bank Plc

During the week, Central Bank of Kenya (CBK) announced the acquisition of 20.0% stake of Credit Bank Plc by Shorecap III, LP a Private Equity fund registered under the laws of Mauritius, with Equator Capital Partners LLC as the managers of the fund. The acquisition will be effective 15 June 2023 and this comes after CBK’s approval on 24 April 2023 and approval by the Cabinet Secretary for the National Treasury and Planning on 28 April 2023. Notably, the search for a potential investor by Credit Bank started in 2018 with the company having sought shareholder’s authorization to enter into discussion with potential investors interested in buying its shares. The value of the deal was not disclosed by the CBK, however, Shorecap III, LP will take over 7,289,928 ordinary shares which constitute of 20.0% of the ordinary shares of the Bank. This move comes after Oikocredit acquired 22.8% stake of the lender in August 2019, after paying a cash consideration of Kshs 1.0 bn, with the transaction trading at price to book (P/B) multiple of 1.5x.

Credit Bank Plc currently has 17 branches with its balance sheet recording expansion as its total assets grew at a 5-year CAGR of 7.6% to Kshs 25.8 bn in 2022, from Kshs 17.9 bn in 2018. In FY’2022, the Bank’s net loans came in at Kshs 17.45 bn, while Customer deposits was at Kshs 17.54 bn, translating to a loan to deposit ratio of 99.5%, reflecting the bank’s current inability to amass deposits. Additionally, the Bank’s profitability has declined significantly to a loss of Kshs 1.7 mn in 2022, from a profit of Kshs 0.1 bn in 2021, mainly due to 3.8% decline in total operating income coupled with the 14.4% increase in total operating expenses. Key capital ratios such as the Core capital to deposit liabilities ratio came in at 9.4% in FY’2022, only 1.4% points above the regulatory limit of 8.0%. The core capital to risk weighted assets came in at 7.4% in FY’2022, 3.1% points below the regulatory limit of 10.5%. Similarly, the Capital adequacy ratio came in at 14.9% in FY’2022, slightly above the regulatory requirement of 14.5%. The liquidity ratio came in 20.5%, only 0.5% points above the regulatory requirement of 20.0%. Further, other ratios have also been adverse, such as the asset quality, with the bank having Non-Performing loan (NPL) ratio of 27.4% in FY’2022, 14.1% points above the banking sector average of 13.3% during the same period. The table below summarizes Credit Bank’s Performance and Key Financial Ratios;

|

Cytonn report: Summary of Credit Bank Plc Financials |

|||||

|

|

FY’2018 |

FY’2019 |

FY’2020 |

FY’2021 |

FY'2022 |

|

Balance Sheet Summary (Kshs bn) |

|||||

|

Net Loans |

13.0 |

15.2 |

15.6 |

15.5 |

17.5 |

|

Total Assets |

17.9 |

21.7 |

23.2 |

26 |

25.8 |

|

Customer Deposits |

13.1 |

16.8 |

17.6 |

20.4 |

17.5 |

|

Total Liabilities |

15.0 |

18.6 |

20.0 |

22.6 |

22.5 |

|

Shareholders' Funds |

2.9 |

3.0 |

3.2 |

3.4 |

3.3 |

|

Income Statement Summary (Kshs mn) |

|||||

|

Total Operating income |

1,719.4 |

1,794.9 |

1,754.1 |

1,638.3 |

1,575.3 |

|

Total Operating expenses |

1,376.5 |

1,492.0 |

1,736.0 |

1,423.9 |

1,629.3 |

|

Profit After Tax (PAT) |

248.5 |

393.8 |

92.1 |

138.1 |

(1.7) |

|

Balance Sheet Ratios |

|||||

|

Loan to Deposit |

99.3% |

90.6% |

88.6% |

75.9% |

99.5% |

|

ROaE |

8.6% |

13.4% |

2.9% |

4.2% |

(0.1%) |

|

ROaA |

1.4% |

2.0% |

0.4% |

0.6% |

(0.01%) |

|

Income Statement Ratios: |

|||||

|

Yield on Interest Earning Assets |

1.8% |

2.3% |

0.5% |

0.6% |

(0.01%) |

|

Net Interest Margin |

6.6% |

5.4% |

5.6% |

4.3% |

3.6% |

|

Cost to Income Ratio |

73.0% |

75.5% |

82.6% |

84.0% |

92.9% |

|

Capital Adequacy Ratios: |

|||||

|

Core Capital liabilities ratio |

20.0% |

16.9% |

16.3% |

8.2% |

9.4% |

|

Minimum Statutory requirement |

8.0% |

8.0% |

8.0% |

8.0% |

8.0% |

|

Excess/Deficit |

12.0% |

8.9% |

8.3% |

0.2% |

1.4% |

|

Core Capital risk weighted assets ratio |

14.0% |

14.1% |

13.0% |

7.9% |

7.4% |

|

Minimum Statutory requirement |

10.5% |

10.5% |

10.5% |

10.5% |

10.5% |

|

Excess/Deficit |

3.5% |

3.6% |

2.5% |

(2.6%) |

(3.1%) |

|

Total Capital risk weighted ratio |

14.5% |

15.0% |

14.5% |

15.8% |

14.9% |

|

Minimum Statutory requirement |

14.5% |

14.5% |

14.5% |

14.5% |

14.5% |

|

Excess/Deficit |

0.0% |

0.5% |

0.0% |

1.3% |

0.4% |

|

Liquidity ratios: |

|||||

|

Liquidity ratio |

21.0% |

26.0% |

26.5% |

39.4% |

20.5% |

|

Minimum Statutory requirement |

20.0% |

20.0% |

20.0% |

20.0% |

20.0% |

|

Excess/Deficit |

1.0% |

6.0% |

6.5% |

19.4% |

0.5% |

|

Asset quality ratios: |

|||||

|

Gross Non-Performing Loan Ratio |

8.3% |

10.1% |

11.9% |

27.2% |

27.4% |

|

NPL Coverage Ratio |

36.8% |

35.8% |

65.4% |

59.7% |

63.1% |

In light of the recent Credit Bank’s performance, we expect the completed acquisition to boost the Bank’s capital adequacy and liquidity ratios to above the minimum statutory requirements and positively impact the bank’s operations. The acquisition is also a welcome move as it ensures that the bank’s customer deposits are protected and will bring stability to the bank. Additionally, the completed transaction will enhance diversification and strengthen the resilience of the Kenyan banking sector. Going forward, we expect to see more acquisition and consolidation activities in the Kenya’s banking sector as larger banks and other companies with sufficient capital base take over smaller and weaker banks.

Below is a summary of the deals in the last 9 years that have either happened, been announced or expected to be concluded:

|

Cytonn Report: Banking sector Deals and Acquisitions |

||||||

|

Acquirer |

Bank Acquired |

Book Value at Acquisition (Kshs bn) |

Transaction Stake |

Transaction Value (Kshs bn) |

P/Bv Multiple |

Date |

|

Shorecap III |

Credit Bank Plc |

3.0 |

20.0% |

Undisclosed |

N/A |

Jun-23 |

|

Premier Bank Limited |

First Community Bank |

2.8 |

62.5% |

Undisclosed |

N/A |

Mar 27 |

|

KCB Group PLC |

Trust Merchant Bank (TMB) |

12.4 |

85.0% |

15.7 |

1.5x |

Dec-22 |

|

Equity Group |

Spire Bank |

Unknown |

Undisclosed |

Undisclosed |

N/A |

Sep-22* |

|

Access Bank PLC (Nigeria) |

Sidian Bank |

4.9 |

83.4% |

4.3 |

1.1x |

June-22* |

|

KCB Group |

Banque Populaire du Rwanda |

5.3 |

100.0% |

5.6 |

1.1x |

August-21 |

|

I&M Holdings PLC |

Orient Bank Limited Uganda |

3.3 |

90.0% |

3.6 |

1.1x |

April-21 |

|

KCB Group** |

ABC Tanzania |

Unknown |

100% |

0.8 |

0.4x |

Nov-20* |

|

Co-operative Bank |

Jamii Bora Bank |

3.4 |

90.0% |

1 |

0.3x |

Aug-20 |

|

Commercial International Bank |

Mayfair Bank Limited |

1.0 |

51.0% |

Undisclosed |

N/D |

May-20* |

|

Access Bank PLC (Nigeria) |

Transnational Bank PLC. |

1.9 |

100.0% |

1.4 |

0.7x |

Feb-20* |

|

Equity Group ** |

Banque Commerciale Du Congo |

8.9 |

66.5% |

10.3 |

1.2x |

Nov-19* |

|

KCB Group |

National Bank of Kenya |

7.0 |

100.0% |

6.6 |

0.9x |

Sep-19 |

|

CBA Group |

NIC Group |

33.5 |

53%:47% |

23.0 |

0.7x |

Sep-19 |

|

Oiko Credit |

Credit Bank |

3.0 |

22.8% |

1 |

1.5x |

Aug-19 |

|

CBA Group** |

Jamii Bora Bank |

3.4 |

100.0% |

1.4 |

0.4x |

Jan-19 |

|

AfricInvest Azure |

Prime Bank |

21.2 |

24.2% |

5.1 |

1.0x |

Jan-18 |

|

KCB Group |

Imperial Bank |

Unknown |

Undisclosed |

Undisclosed |

N/A |

Dec-18 |

|

SBM Bank Kenya |

Chase Bank Ltd |

Unknown |

75.0% |

Undisclosed |

N/A |

Aug-18 |

|

DTBK |

Habib Bank Kenya |

2.4 |

100.0% |

1.8 |

0.8x |

Mar-17 |

|

SBM Holdings |

Fidelity Commercial Bank |

1.8 |

100.0% |

2.8 |

1.6x |

Nov-16 |

|

M Bank |

Oriental Commercial Bank |

1.8 |

51.0% |

1.3 |

1.4x |

Jun-16 |

|

I&M Holdings |

Giro Commercial Bank |

3.0 |

100.0% |

5.0 |

1.7x |

Jun-16 |

|

Mwalimu SACCO |

Equatorial Commercial Bank |

1.2 |

75.0% |

2.6 |

2.3x |

Mar-15 |

|

Centum |

K-Rep Bank |

2.1 |

66.0% |

2.5 |

1.8x |

Jul-14 |

|

GT Bank |

Fina Bank Group |

3.9 |

70.0% |

8.6 |

3.2x |

Nov-13 |

|

Average |

74.5% |

1.3x |

||||

|

* Announcement Date ** Deals that were dropped |

||||||

- Earnings Releases

- KCB Group Plc

During the week, KCB Group Plc released their Q1’2023 financial results. Below is a summary of the performance:

|

Balance Sheet Items (Kshs bn) |

Q1’2022 |

Q1’2023 |

y/y change |

||

|

Net Loans and Advances |

704.4 |

928.8 |

31.9% |

||

|

Government Securities |

240.6 |

252.1 |

4.8% |

||

|

Total Assets |

1,166.9 |

1,630.6 |

39.7% |

||

|

Customer Deposits |

845.8 |

1,196.6 |

41.5% |

||

|

Deposit per Branch |

1.7 |

2.0 |

15.6% |

||

|

Total Liabilities |

983.2 |

1,415.8 |

44.0% |

||

|

Shareholders’ Funds |

181.8 |

208.1 |

14.5% |

||

|

Balance Sheet Ratios |

Q1’2022 |

Q1’2023 |

% y/y change |

|

Loan to Deposit Ratio |

83.3% |

77.6% |

(5.7%) |

|

Return on average equity |

22.9% |

20.9% |

(2.0%) |

|

Return on average assets |

3.5% |

2.9% |

(0.6%) |

|

Income Statement (Kshs bn) |

Q1’2022 |

Q1’2023 |

y/y change |

|

Net Interest Income |

19.7 |

22.1 |

11.8% |

|

Net non-Interest Income |

9.3 |

14.8 |

59.2% |

|

Total Operating income |

29.0 |

36.9 |

26.9% |

|

Loan Loss provision |

(2.1) |

(4.1) |

98.4% |

|

Total Operating expenses |

(15.0) |

(23.0) |

53.3% |

|

Profit before tax |

14.0 |

13.9 |

(1.3%) |

|

Profit after tax |

9.9 |

9.8 |

(1.0%) |

|

Core EPS |

3.07 |

3.0 |

(1.0%) |

|

Income Statement Ratios |

Q1’2022 |

Q1’2023 |

y/y change |

|

Yield from interest-earning assets |

11.4% |

10.2% |

(1.2%) |

|

Cost of funding |

3.0% |

3.2% |

0.2% |

|

Net Interest Spread |

8.4% |

7.1% |

(1.3%) |

|

Net Interest Margin |

8.6% |

7.3% |

(1.3%) |

|

Cost of Risk |

7.1% |

11.2% |

4.1% |

|

Net Interest Income as % of operating income |

68.0% |

59.9% |

(8.1%) |

|

Non-Funded Income as a % of operating income |

32.0% |

40.1% |

8.1% |

|

Cost to Income Ratio |

51.7% |

62.4% |

10.7% |

|

Capital Adequacy Ratios |

Q1’2022 |

Q1’2023 |

% points change |

|

Core Capital/Total Liabilities |

19.7% |

15.0% |

(4.7%) |

|

Minimum Statutory ratio |

8.0% |

8.0% |

|

|

Excess |

11.7% |

7.0% |

(4.7%) |

|

Core Capital/Total Risk Weighted Assets |

19.2% |

13.6% |

(5.6%) |

|

Minimum Statutory ratio |

10.5% |

10.5% |

|

|

Excess |

8.7% |

3.1% |

(5.6%) |

|

Total Capital/Total Risk Weighted Assets |

22.8% |

17.0% |

(5.8%) |

|

Minimum Statutory ratio |

14.5% |

14.5% |

|

|

Excess |

8.3% |

2.5% |

(5.8%) |

|

Liquidity Ratio |

36.9% |

43.7% |

6.8% |

|

Minimum Statutory ratio |

20.0% |

20.0% |

|

|

Excess |

16.9% |

43.7% |

6.8% |

|

Adjusted core capital/ total deposit liabilities |

19.7% |

15.0% |

(4.7%) |

|

Adjusted core capital/ total risk weighted assets |

19.3% |

13.6% |

(5.7%) |

|

Adjusted total capital/ total risk weighted assets |

22.9% |

17.0% |

(5.9%) |

Key Take-Outs:

Decline in Earnings: Core earnings per share declined by 0.1% to Kshs 3.03 from Kshs 3.07 in Q1’2022, mainly as a result of the 53.3% growth in total operating expense to Kshs 23.0 bn, from Kshs 15.0 bn in Q1’2022, which outpaced the 26.9% growth in total operating Income to Kshs 36.9 bn, from Kshs 29.0 bn in Q1’2022,

Improved Lending – The Group’s loan book increased in Q1’2023 as seen by a significant 31.9% growth in loans to Kshs 928.8 bn from Kshs 704.4 bn in Q1’2022, mainly attributable to increased lending boosted by the recent acquisitions with the Group’s Congo subsidiary, Trust Merchant Bank, contributing 6.8% of the loan book during the period under review,

Revenue diversification – The Group’s Non-Funded income increased by 59.2% to Kshs 14.8 bn, from Kshs 9.3 bn in Q1’2022, which resulted to a shift in revenue mix to 60:40 from 68:32 funded to non-funded income. The increase was mainly attributable to a 38.0% increase in non-funded income from digital channels due to increased usage of internet banking, mobile banking and merchant POS terminal, coupled with 52.1% increase in Forex trading income to Kshs 2.6 bn, from Kshs 1.7 bn in Q1’2023, and,

Increased Customer Deposit – KCB customer deposit increased significantly hitting Kshs 1.2 tn mark for the first time. Customer deposits increased by 41.5% to Kshs 1,196.6 bn from Kshs 845.8 bn in Q1’2022 mainly attributable to the completion of the acquisition of TMB Bank and the organic growth in the existing business.

For a comprehensive analysis, please see our KCB Group Plc Q1’2023 Earnings Note

- NCBA Group

During the week, NCBA Group Plc released their Q1’2023 financial results. Below is a summary of the performance:

|

Balance Sheet (Kshs bn) |

Q1’2022 |

Q1’2023 |

y/y change |

|

Net Loans and Advances |

243.9 |

287.2 |

17.7% |

|

Government Securities |

194.7 |

207.1 |

6.4% |

|

Total Assets |

587.4 |

628.8 |

7.1% |

|

Customer Deposits |

465.5 |

499.7 |

7.3% |

|

Deposits Per Branch |

4.5 |

5.8 |

7.3% |

|

Total Liabilities |

507.1 |

540.9 |

6.7% |

|

Shareholders' Funds |

80.2 |

87.9 |

9.6% |

|

Key Ratios |

Q1’2022 |

Q1’2023 |

% point change |

|

Loan to Deposit Ratio |

52.4% |

57.5% |

5.1% |

|

Government Securities to Deposit ratio |

41.8% |

41.4% |

(0.4%) |

|

Return on average equity |

14.0% |

18.4% |

4.4% |

|

Return on average assets |

1.9% |

2.5% |

0.6% |

|

Income Statement (Kshs bn) |

Q1’2022 |

Q1’2023 |

y/y change |

|

Net Interest Income |

7.1 |

8.4 |

18.0% |

|

Net non-Interest Income |

6.1 |

7.2 |

18.5% |

|

Total Operating income |

13.1 |

15.5 |

18.2% |

|

Loan Loss provision |

2.5 |

2.0 |

(22.6%) |

|

Total Operating expenses |

8.1 |

9.2 |

12.8% |

|

Profit before tax |

4.8 |

6.4 |

31.9% |

|

Profit after tax |

3.4 |

5.1 |

48.5% |

|

Core EPS |

2.1 |

3.1 |

48.5% |

|

Income Statement Ratios |

Q1’2022 |

Q1’2023 |

% point change |

|

Yield from interest-earning assets |

9.8% |

10.4% |

0.6% |

|

Cost of funding |

4.3% |

4.6% |

0.3% |

|

Net Interest Spread |

5.5% |

5.7% |

0.2% |

|

Net Interest Margin |

5.7% |

6.0% |

0.3% |

|

Cost of Risk |

19.2% |

12.6% |

(6.6%) |

|

Net Interest Income as % of operating income |

53.9% |

53.8% |

(0.1%) |

|

Non-Funded Income as a % of operating income |

46.1% |

46.2% |

0.1% |

|

Cost to Income Ratio |

61.7% |

58.9% |

(2.8%) |

|

Cost to Income Ratio without LLP |

42.5% |

46.3% |

3.8% |

|

Capital Adequacy Ratios |

Q1’2022 |

Q1’2023 |

% points change |

|

Core Capital/Total Liabilities |

15.9% |

16.8% |

0.9% |

|

Minimum Statutory ratio |

8.0% |

8.0% |

|

|

Excess |

7.9% |

8.8% |

0.9% |

|

Core Capital/Total Risk Weighted Assets |

18.0% |

17.7% |

(0.3%) |

|

Minimum Statutory ratio |

10.5% |

10.5% |

|

|

Excess |

7.5% |

7.2% |

(0.3%) |

|

Total Capital/Total Risk Weighted Assets |

18.0% |

17.8% |

(0.2%) |

|

Minimum Statutory ratio |

14.5% |

14.5% |

|

|

Excess |

3.5% |

3.3% |

(0.2%) |

|

Liquidity Ratio |

63.0% |

53.1% |

(9.9%) |

|

Minimum Statutory ratio |

20.0% |

20.0% |

|

|

Excess |

43.0% |

33.1% |

(9.9%) |

|

Adjusted core capital/ total deposit liabilities |

16.0% |

16.8% |

0.8% |

|

Adjusted core capital/ total risk weighted assets |

18.6% |

17.7% |

(0.9%) |

|

Adjusted total capital/ total risk weighted assets |

18.6% |

17.8% |

(0.8%) |

Key Take-Outs:

Strong earnings growth - Core earnings per share rose by 48.5% to Kshs 3.1, from Kshs 2.1 in Q1’2022, driven by 18.2% growth in total operating income to Kshs 15.5 bn from Kshs 13.1 bn in Q1’2022. The lender’s growth in total operating income was driven by 18.0% growth in Net Interest Income to Kshs 8.4 bn, from Kshs 7.1 bn in Q1’2022, coupled with an 18.5% increase in Non-Funded Income to Kshs 7.2 bn from Kshs 6.1 bn in Q1’2022,

Improved Asset Quality – The Group’s Asset Quality improved, with Gross NPL ratio declining to 12.8% in Q1’2023, from 16.3% in Q1’2022. This was mainly attributable to 11.9% decrease in Gross non-performing loans to Kshs 39.7 bn, from Kshs 45.1 bn in Q1’2022, coupled with 12.0% increase in gross loans to Kshs 309.7 bn, from Kshs 276.7 bn recorded in Q1’2022, and,

Aggressive lending – The Group’s increased its lending in Q1’2023 with the loan book recording a 17.7% increased to Kshs 287.2 bn, from Kshs 243.9 bn in Q1’2022, highlighting the Group’s aggressive lending despite the tough operating business. Consequently, the loan to deposit ratio increased by 5.1% to 57.1% from 52.4% in Q1’2022.

For a comprehensive analysis, please see our NCBA Group Plc Q1’2023 Earnings Note

Summary performance:

Asset Quality:

The table below highlights the Asset Quality of the listed banks:

|

|

Q1'2023 NPL Ratio* |

Q1'2022 NPL Ratio** |

% point change in NPL Ratio |

Q1'2023 NPL Coverage* |

Q1'2022 NPL Coverage** |

% point change in NPL Coverage |

|

Equity Group |

10.0% |

9.0% |

1.0% |

62.0% |

66.0% |

(4.0%) |

|

Stanbic Bank |

11.7% |

11.1% |

0.6% |

66.7% |

59.1% |

7.6% |

|

NCBA Group |

12.8% |

16.3% |

(3.5%) |

56.8% |

72.6% |

(15.8%) |

|

Co-operative Bank of Kenya |

14.1% |

13.9% |

0.2% |

62.2% |

65.3% |

(3.1%) |

|

Standard Chartered Bank Kenya |

14.4% |

15.4% |

(1.0%) |

86.8% |

81.8% |

5.0% |

|

KCB Group |

17.1% |

16.9% |

0.2% |

57.3% |

52.7% |

4.6% |

|

Mkt Weighted Average |

13.2% |

12.5% |

0.7% |

63.7% |

65.1% |

(1.4%) |

|

*Market cap weighted as at 26/05/2023 |

||||||

|

**Market cap weighted as at 17/06/2022 |

||||||

Key take-outs from the table include;

- Asset quality for the listed banks that have released their Q1’2023 financial results has deteriorated with market weighted average NPL ratio increasing by 0.7% points to 13.2%, from a 12.5% in Q1’2022. The deterioration was largely driven by deterioration in Equity Group’s, Stanbic bank’s, and KCB Group’s asset quality with their NPL ratios increasing by 1.0%, 0.6% and 0.2% points to 10.0%, 11.7%, and 17.1%, from 9.0%, 11.1%, and 16.9%, respectively recorded in Q1’2022, and,

- Market weighted average NPL Coverage for the listed banks decreased by 1.4% points to 63.7% in Q1’2023, from 65.1% recorded in Q1’2022. The decrease was mainly attributable to decrease in NCBA Group’s, Equity Group’s and Co-operative Bank’s NPL coverage by 15.8%, 4.0% and 3.1% points to 56.8%, 62.0% and 62.2%, from 72.6%, 66.0% and 65.3%, respectively in Q1’2022.

The table below highlights the performance listed banks, showing the performance using several metrics:

|

Bank |

Core EPS Growth |

Interest Income Growth |

Interest Expense Growth |

Net Interest Income Growth |

Net Interest Margin |

Non-Funded Income Growth |

NFI to Total Operating Income |

Growth in Total Fees & Commissions |

Deposit Growth |

Growth in Government Securities |

Loan to Deposit Ratio |

Loan Growth |

Return on Average Equity |

||||||||||

|

Stanbic |

84.3% |

49.1% |

59.7% |

44.7% |

7.2% |

89.3% |

51.4% |

17.7% |

23.8% |

9.7% |

79.1% |

11.5% |

20.7% |

||||||||||

|

NCBA |

48.5% |

21.0% |

25.2% |

18.0% |

6.0% |

18.5% |

46.2% |

9.1% |

7.3% |

6.4% |

57.5% |

17.7% |

18.4% |

||||||||||

|

SCB-k |

47.2% |

34.1% |

(5.4%) |

40.1% |

7.3% |

55.5% |

35.9% |

13.3% |

14.2% |

(6.2%) |

45.3% |

7.0% |

23.0% |

||||||||||

|

Equity |

7.9% |

21.6% |

46.9% |

12.1% |

7.4% |

54.3% |

45.9% |

39.2% |

23.3% |

(7.7%) |

68.1% |

23.1% |

26.8% |

||||||||||

|

Co-op |

4.7% |

11.2% |

32.2% |

3.9% |

8.5% |

10.8% |

39.7% |

9.7% |

2.2% |

(2.3%) |

85.8% |

11.0% |

20.7% |

||||||||||

|

KCB |

(1.0%) |

26.0% |

67.7% |

11.8% |

7.3% |

59.2% |

40.1% |

65.5% |

41.5% |

4.8% |

77.6% |

31.9% |

20.9% |

||||||||||

|

Q1'23 Mkt Weighted Average* |

22.2% |

25.2% |

41.6% |

18.0% |

7.3% |

48.5% |

43.1% |

32.4% |

21.6% |

(0.7%) |

69.3% |

19.9% |

22.6% |

||||||||||

|

Q1'22 Mkt Weighted Average** |

37.9% |

17.8% |

17.1% |

17.7% |

7.3% |

21.4% |

35.9% |

21.7% |

9.5% |

17.6% |

73.9% |

17.2% |

21.9% |

||||||||||

|

*Market cap weighted as at 26/05/2023 **Market cap weighted as at 17/06/2022 |

|||||||||||||||||||||||

Key take-outs from the table include;

- The listed banks recorded a 22.2% growth in core Earnings per Share (EPS) in Q1’2023, compared to the weighted average growth of 37.9% in Q1’2022, an indication of sustained performance despite the tough operating environment experienced in Q1’2023,

- Non-Funded Income grew by 48.5% compared to market weighted average growth of 21.4% in Q1’2022, mainly due to growth in forex related fees occasioned by the wide spreads in the dollar exchange rate during the quarter, and,

- The Banks recorded a weighted average deposit growth of 21.6%, higher than the market weighted average deposit growth of 9.5% in Q1’2022, highlighting increased investment risk in the business environment.

Universe of coverage:

|

Company |

Price as at 19/05/2023 |

Price as at 26/05/2023 |

w/w change |

YTD Change |

Target Price* |

Dividend Yield |

Upside/ Downside** |

P/TBv Multiple |

Recommendation |

|

Jubilee Holdings |

179.8 |

178.0 |

(1.0%) |

(10.4%) |

305.9 |

6.7% |

78.6% |

0.3x |

Buy |

|

Britam |

4.2 |

4.2 |

(0.2%) |

(20.0%) |

7.1 |

0.0% |

71.2% |

0.7x |

Buy |

|

I&M Group*** |

17.0 |

15.9 |

(6.8%) |

(7.0%) |

24.5 |

14.2% |

68.7% |

0.3x |

Buy |

|

Liberty Holdings |

4.0 |

4.1 |

2.8% |

(19.2%) |

6.8 |

0.0% |

65.8% |

0.3x |

Buy |

|

Equity Group*** |

38.4 |

36.9 |

(3.9%) |

(18.1%) |

56.3 |

10.8% |

63.5% |

0.7x |

Buy |

|

Diamond Trust Bank*** |

46.0 |

45.0 |

(2.2%) |

(9.7%) |

64.6 |

11.1% |

54.7% |

0.2x |

Buy |

|

Kenya Reinsurance |

1.8 |

1.8 |

(2.2%) |

(5.9%) |

2.5 |

11.4% |

54.0% |

0.1x |

Buy |

|

NCBA*** |

32.6 |

34.6 |

6.1% |

(11.2%) |

48.7 |

12.3% |

53.2% |

0.7x |

Buy |

|

KCB Group*** |

30.9 |

31.1 |

0.6% |

(19.0%) |

45.5 |

6.4% |

53.0% |

0.5x |

Buy |

|

Sanlam |

8.0 |

7.8 |

(2.5%) |

(18.6%) |

11.9 |

0.0% |

52.7% |

0.8x |

Buy |

|

ABSA Bank*** |

10.4 |

10.8 |

3.8% |

(11.5%) |

15.1 |

12.5% |

52.7% |

0.8x |

Buy |

|

Co-op Bank*** |

12.3 |

11.4 |

(6.9%) |

(5.8%) |

15.9 |

13.2% |

52.6% |

0.5x |

Buy |

|

Standard Chartered*** |

140.0 |

145.8 |

4.1% |

0.5% |

195.4 |

15.1% |

49.1% |

0.9x |

Buy |

|

Stanbic Holdings |

110.0 |

98.3 |

(10.7%) |

(3.7%) |

131.8 |

12.8% |

46.9% |

0.7x |

Buy |

|

CIC Group |

1.7 |

1.9 |

11.2% |

(1.6%) |

2.3 |

6.9% |

30.3% |

0.7x |

Buy |

|

HF Group |

4.2 |

4.3 |

2.4% |

36.2% |

4.5 |

0.0% |

3.7% |

0.2x |

Lighten |

|

Target Price as per Cytonn Analyst estimates **Upside/ (Downside) is adjusted for Dividend Yield ***For Disclosure, these are stocks in which Cytonn and/or its affiliates are invested in |

|||||||||

We are “Neutral” on the Equities markets in the short term due to the current adverse operating environment and huge foreign investor outflows, and, “Bullish” in the long term due to current cheap valuations and expected global and local economic recovery.

With the market currently trading at a discount to its future growth (PEG Ratio at 0.6x), we believe that investors should reposition towards value stocks with strong earnings growth and that are trading at discounts to their intrinsic value. We expect the current high foreign investors sell-offs to continue weighing down the equities outlook in the short term.

- Commercial Office Sector

During the week, Actis Limited, a global private equity firm, announced that it had shut down two offices located in Nairobi, Kenya and Cape Town, South Africa. This comes at a time when Actis is actively exploring alternative working solutions, which consequently resulted in the decision to not renew the commercial leases for the two offices. However, Actis has maintained that the closure of these branches does not imply an exit from the respective markets. Following the closure Actis currently maintains a total of 17 physical offices worldwide, with four of them strategically located in Africa which include; Lagos in Nigeria, Johannesburg in South Africa, Port Louis in Mauritius, and Cairo in Egypt. Within Kenya, Actis has invested in the residential sector in Garden City Mall and Mi Vida homes, the retail sector in Junction Mall, and in the hospitality sector with an ownership of Java House.

The decision by Actis to review its office footprint in Africa aligns with the prevailing trend of hybrid and remote working strategies that have significantly influenced the commercial office market. This is as many companies have embraced these strategies to reduce costs and introduce greater flexibility in their working environments alongside their recovery from the COVID-19 pandemic. Consequently, this shift has resulted in a slowdown in occupancy rates in the commercial market, with the closure of their office located at Courtyard, along General Mathenge Road in Westlands, Nairobi prolonging the vacancy rates within the sector.

The table below shows the Nairobi Metropolitan Area (NMA) commercial office sub-market performance;

All values in Kshs unless stated otherwise

|

Cytonn Report: Nairobi Metropolitan Area Commercial Office Market Performance Q1’2022/Q1’2023 |

|||||||||||

|

Area |

Price Kshs/ SQFT Q1’2023 |

Rent Kshs/ SQFT Q1’2023 |

Occupancy Q1’ 2023 |

Rental Yields Q1 2023(%) |

Price Kshs/ SQFT Q1’2022 |

Rent Kshs/ SQFT Q1’2022 |

Occupancy Q1’2022 (%) |

Rental Yields Q1 2022(%) |

∆ in Rent |

∆ in Occupancy (% points) |

∆ in Rental Yields (% points) |

|

Gigiri |

13,500 |

118 |

81.6% |

8.7% |

13,500 |

118 |

83.3% |

8.8% |

0.4% |

(1.7%) |

(0.1%) |

|

Westlands |

12,032 |

108 |

77.2% |

8.4% |

11,846 |

105 |

74.5% |

8.1% |

2.8% |

2.7% |

0.2% |

|

Karen |

13,431 |

111 |

82.9% |

8.3% |

13,325 |

107 |

82.8% |

7.8% |

3.8% |

0.1% |

0.5% |

|

Kilimani |

12,260 |

93 |

84.1% |

7.8% |

12,440 |

91 |

80.2% |

7.1% |

2.9% |

3.9% |

0.7% |

|

Parklands |

11,662 |

91 |

82.2% |

7.8% |

11,562 |

91 |

82.8% |

7.7% |

0.0% |

(0.6%) |

0.0% |

|

Nairobi CBD |

11,971 |

83 |

85.3% |

7.2% |

11,863 |

82 |

83.8% |

6.9% |

1.4% |

1.4% |

0.3% |

|

Upperhill |

12,605 |

97 |

76.6% |

7.0% |

12,409 |

94 |

76.1% |

6.9% |

2.7% |

0.4% |

0.1% |

|

Thika Road |

12,571 |

79 |

80.3% |

6.0% |

12,571 |

78 |

77.6% |

5.7% |

1.4% |

2.7% |

0.3% |

|

Mombasa Road |

11,325 |

71 |

67.0% |

5.2% |

11,250 |

73 |

64.6% |

5.1% |

(2.5%) |

2.4% |

0.1% |

|

Average |

12,238 |

97 |

79.8% |

7.6% |

12,113 |

94 |

77.9% |

7.3% |

2.2% |

1.9% |

0.4% |

Source: Cytonn Research

Going forward, we expect the sizing down of physical operations by companies which has resulted in an oversupply of approximately 5.8 mn SQFT of space in the NMA market, to continue subduing the performance of the commercial office sector. On the other hand, the vacancy rates will further prompt investors to withhold new developments in order to allow occupation of the existing space. As a result, we expect this will in the long term boost the sector by increasing the uptake rates of commercial space.

- Regulated Real Estate Funds

- Real Estate Investment Trusts (REITs)

In the Nairobi Securities Exchange, ILAM Fahari I-REIT closed the week trading at an average price of Kshs 5.8 per share. The performance represented a 4.0% decline from Kshs 6.0 per share recorded the previous week, taking it to an 15.0% Year-to-Date (YTD) decline from Kshs 6.8 per share recorded on 3 January 2023. In addition, the performance represented a 71.2% Inception-to-Date (ITD) loss from the Kshs 20.0 price. The dividend yield currently stands at 11.3%. The graph below shows Fahari I-REIT’s performance from November 2015 to 26 May 2023;

In the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 23.9 and Kshs 21.6 per unit, respectively, as at 26 May 2023. The performance represented a 19.4% and 7.9% gain for the D-REIT and IREIT, respectively, from the Kshs 20.0 inception price. The volumes traded for the D-REIT and I-REIT came in at 12.3 mn and 30.1 mn shares, respectively, with a turnover of Kshs 257.5 mn and Kshs 620.7 mn, respectively, since inception in February 2021.

REITs provide numerous advantages, including; access to more capital pools, consistent and prolonged profits, tax exemptions, diversified portfolios, transparency, liquidity and flexibility as an asset class. Despite these benefits, the performance of the Kenyan REITs market remains limited by several factors such as; i) insufficient investor understanding of the investment instrument, ii) time-consuming approval procedures for REIT creation, iii) high minimum capital requirements of Kshs 100.0 mn for trustees, and, iv) high minimum investment amounts set at Kshs 5.0 mn discouraging investments.

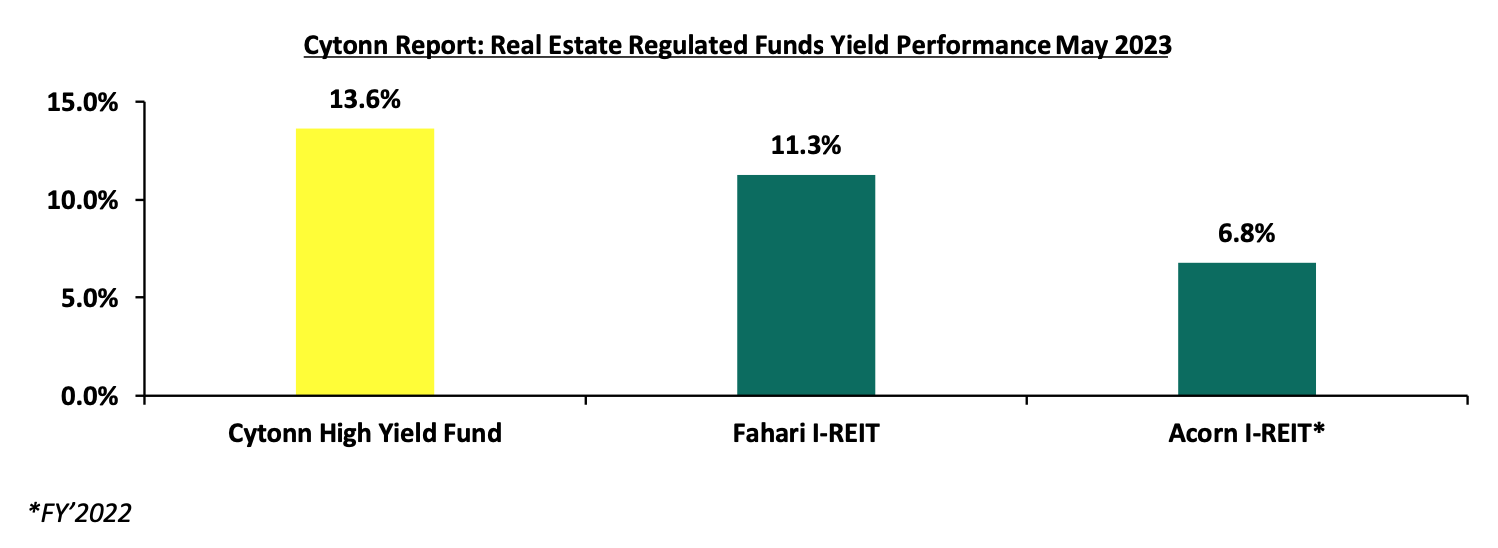

- Cytonn High Yield Fund (CHYF)

Cytonn High Yield Fund (CHYF) closed the week with an annualized yield of 13.6%, representing a 0.1% points decline from the 13.7% yield recorded the previous week. The performance also represented a 0.3% points Year-to-Date (YTD) decline from 13.9% yield recorded on 1 January 2023, and 2.1% points Inception-to-Date (ITD) loss from the 15.7% yield. The graph below shows Cytonn High Yield Fund’s performance from October 2019 to 26 May 2023;

Notably, the CHYF has outperformed other regulated Real Estate funds with an annualized yield of 13.6%, as compared to Fahari I-REIT and Acorn I-REIT with yields of 11.3%, and 6.8% respectively. As such, the higher yields offered by CHYF makes the fund one of the best alternative investment resource in the Real Estate sector. The graph below shows the yield performance of the Regulated Real Estate Funds:

Source: Cytonn Research

We expect the performance of Kenya’s Real Estate sector to remain on an upward trajectory, supported by factors such as; i) the ongoing push by both the government and private sector to focus on affordable housing, ii) improvement in infrastructure, ii) aggressive expansion drive by both local and international retailers, and, iv) the relatively positive demographics in the country that are driving demand for housing upwards. However, the shift by companies to scale down physical operations in favour of hybrid and remote work policies, existing oversupply of physical space in select sectors, rising costs of construction on the back of rising inflation, and low investor appetite for REITs are expected to continue subduing the performance of the sector.

Real Estate development relies on several elements, primarily financing and marketing. Real Estate finance involves providing the necessary financial resources for investment projects aimed at expanding building infrastructure and services. On the other hand, Real Estate marketing serves as a connection between those responsible for the production of various Real Estate properties such as residential houses and offices and those who purchase and benefit from them. Its objective is to fulfill the needs and desires of individuals by offering properties, whether it be land or housing, at the right value and with exceptional customer service.

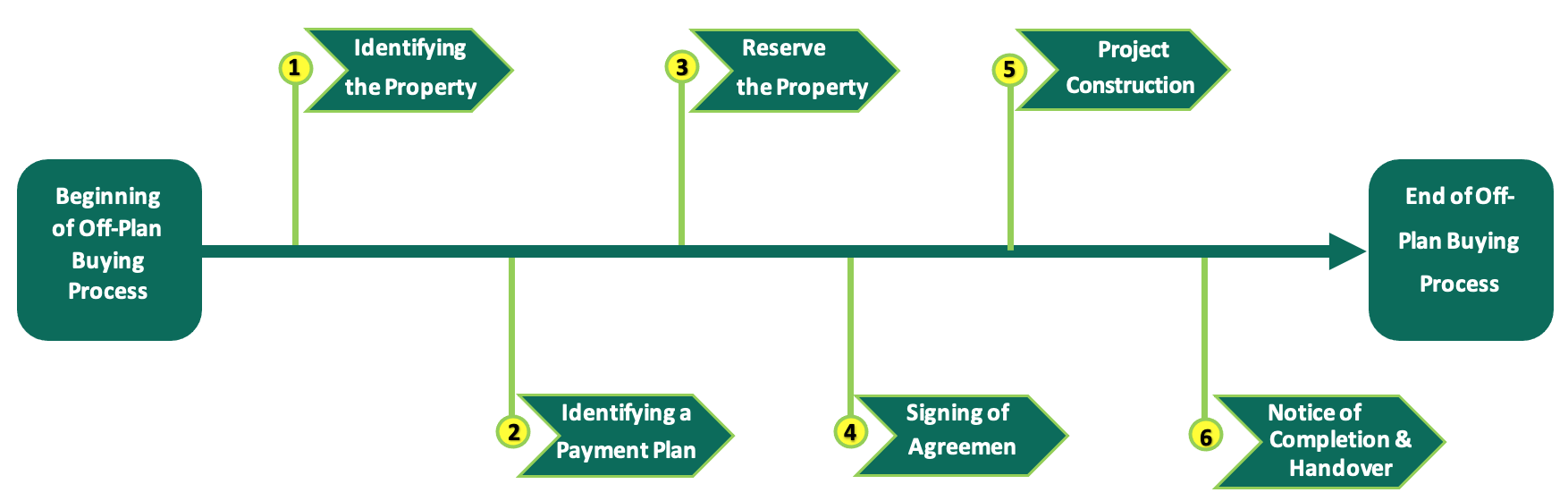

Off-plan investment in the Real Estate sector has emerged as an enticing opportunity, offering a mutually beneficial platform for both developers and buyers. This concept involves the sale and purchase of properties that are yet to be constructed or are still under development, with the completion and ownership transfer being governed by agreed contractual obligations. Over the years, off-plan investment has gained significant traction offering an advantageous platform for both developers and homebuyers. From the perspective of developers, off-plan investment refers to selling a property that has an approved design but has not been constructed or is still under development. In such cases, the developer is responsible for completing the property's construction, delivering it on time, and transferring ownership to the buyer according to the agreed contract. From the perspective of homebuyers, off-plan acquisition involves purchasing a property before its construction has commenced or been finalized. Buyers can make their decision based on blueprints, plans, and computer-generated representations of the proposed housing project. Prior to construction, buyers can secure the home by making a down payment or providing the developer with a letter of credit. Through a contractual agreement, the buyer becomes the owner of a Real Estate unit with predetermined characteristics and specifications, whether it is an existing property or one under construction. The developer, in turn, is obligated to complete the construction within the agreed-upon timeframe, while the buyer is obliged to pay the price either in an expedited or deferred manner. The growing popularity of off-plan investment signifies its potential to reshape the Real Estate market by providing a promising avenue for profitable ventures and fulfilling the housing needs of prospective homeowners.

We have previously covered the same topic on the concept of off-plan in Kenya’s Real Estate namely; Off Plan Real Estate Investing in January 2022 and Off Plan Investment in Real Estate - What a Buyer Needs to Know in 2017, where we provided an in-depth assessment of the concept of off plan investments in the Real Estate sector to provide a basis for the justification of the concept and advising buyers on what they should look out for when purchasing property off plan. This week, we turn our focus on reviewing Off Plan program in Real Estate Development and Investing in order to identify the financial and marketing challenges being faced by such program in Kenya. Additionally, we shall undertake a case study of countries where off plan projects have been successfully implemented and the off plan program is firmly and strictly regulated in the Real Estate sector. From the case studies, we shall give our recommendations of what can be done to improve the regulatory framework for off plan investments in Kenya. We shall undertake this by looking into the following;

- Background and Overview of the focus,

- Off-Plan Buying Process and Off-Plan Investing Tips,

- Benefits and Limitations of Off Plan Investments,

- Case Study of Off-Plan Development Frameworks in other countries, and,

- Recommendations and Conclusion.

Section One: Background and Overview of the topic

The Real Estate industry holds immense significance in the economy of any nation. It serves as a catalyst for growth, generating numerous employment prospects and stimulating economic activities across various sectors. It encompasses a wide range of activities, including pre-construction tasks such as engineering consultation, economic analysis, and marketing studies, as well as construction-related activities which include contracting, sourcing building materials, and actual construction work. Furthermore, the sector continues to contribute into growth of a country’s economy even after the completion of construction, with operations, property management, and maintenance of supporting infrastructures and facilities playing vital roles.

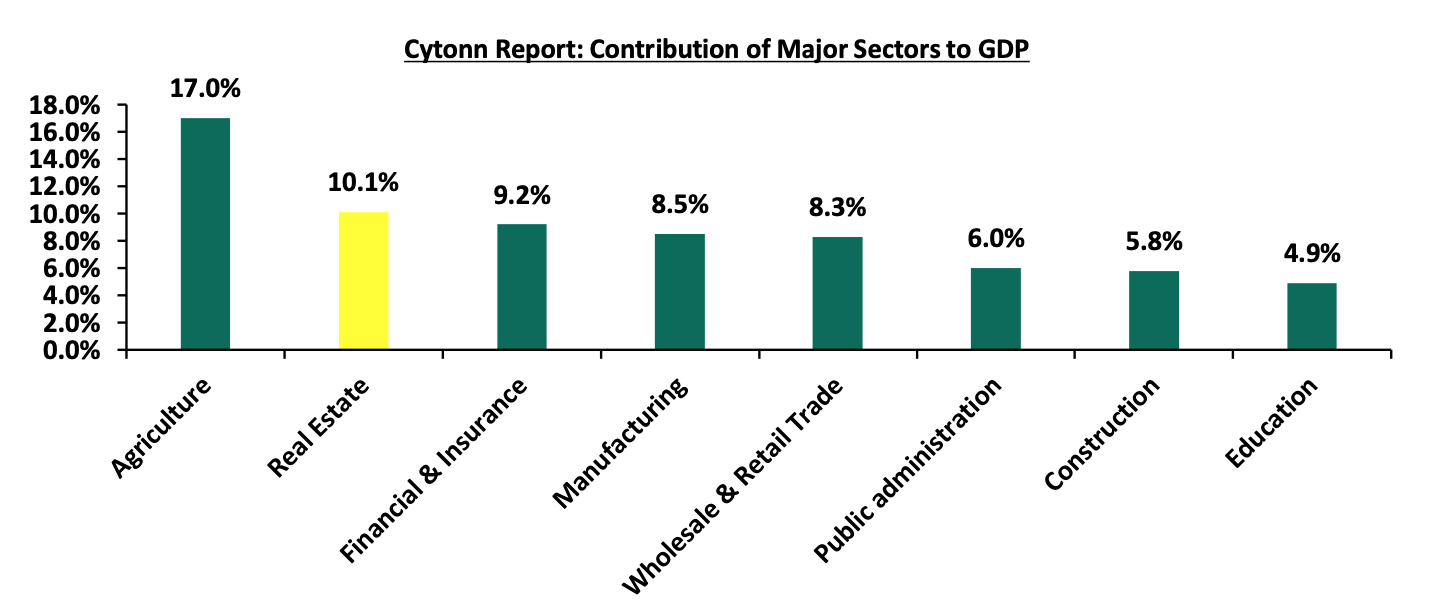

According to the Economic Survey 2023 by Kenya National Bureau of Statistics (KNBS), the Real Estate sector is the second largest contributor in Kenya’s economy as it contributed 10.1% to the country's Gross Domestic Product (GDP) in FY'2022, with a growth rate of 4.5%. With a rapid urbanization and population rates which stood at averages of 3.7% and 1.9% respectively as of 2021, against the global averages of 1.6% and 0.9, the demand for housing in Kenya is very high. This is far exceeding the available supply, as the country faces a significant housing deficit of about 2.0 mn units according to the National Housing Corporation (NHC). This is also at the back of increased infrastructural projects that have opened up new regions for development across the country. The graph below contribution of major sectors of Kenya’s economy to GDP in the year ending 2022;

Source: Kenya National Bureau of Statistics (KNBS)

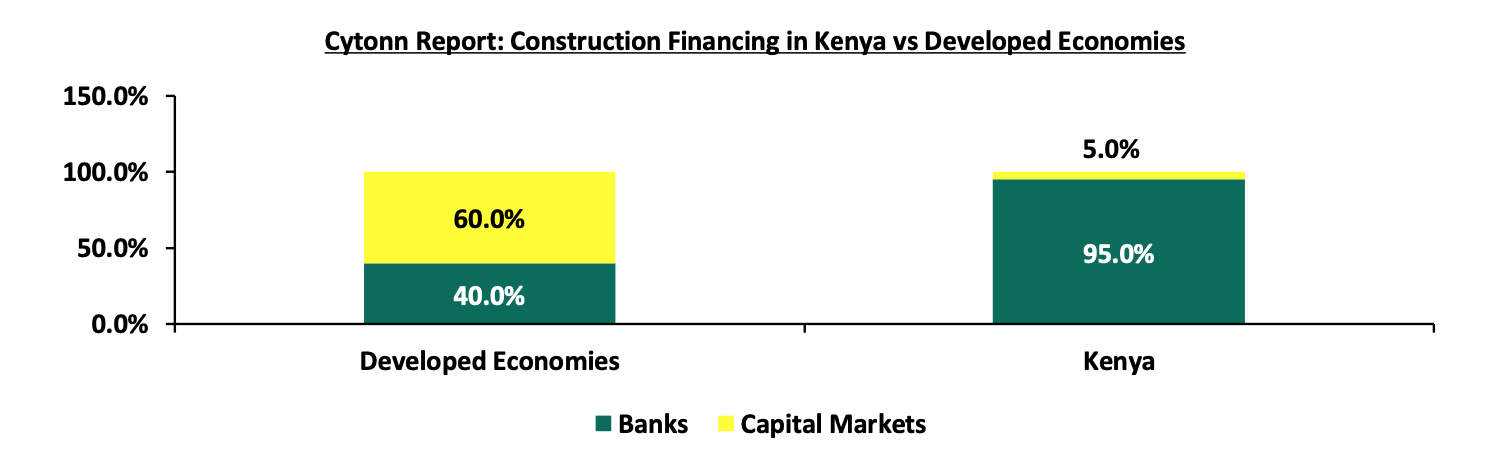

As such, there is a favorable opportunity for private developers in the residential Real Estate sector to construct additional housing units, alleviate the housing crisis, and generate significant profits from the sector. However, these developers are encountering significant financial limitations that hinder project execution. The primary issue lies in the heavy reliance on financial institutions, specifically banks, for costly financial capital required by private developers in execution of large-scale housing projects. This over-reliance and limited financial options make it challenging to secure the necessary affordable finances for construction and completion of housing projects in Kenya. In contrast, developed countries rely more on capital markets, which provide the majority of funding for such ventures. The graph below shows the comparison of construction financing in Kenya against developed economies;

Source: World Bank, Capital Markets Authority

Financial institutions, who have monopolized the access of capital for projects in the sector, continue to tighten their lending requirements and demand more collateral from developers as a result of elevated credit risk in the Real Estate sector. This is evidenced by;

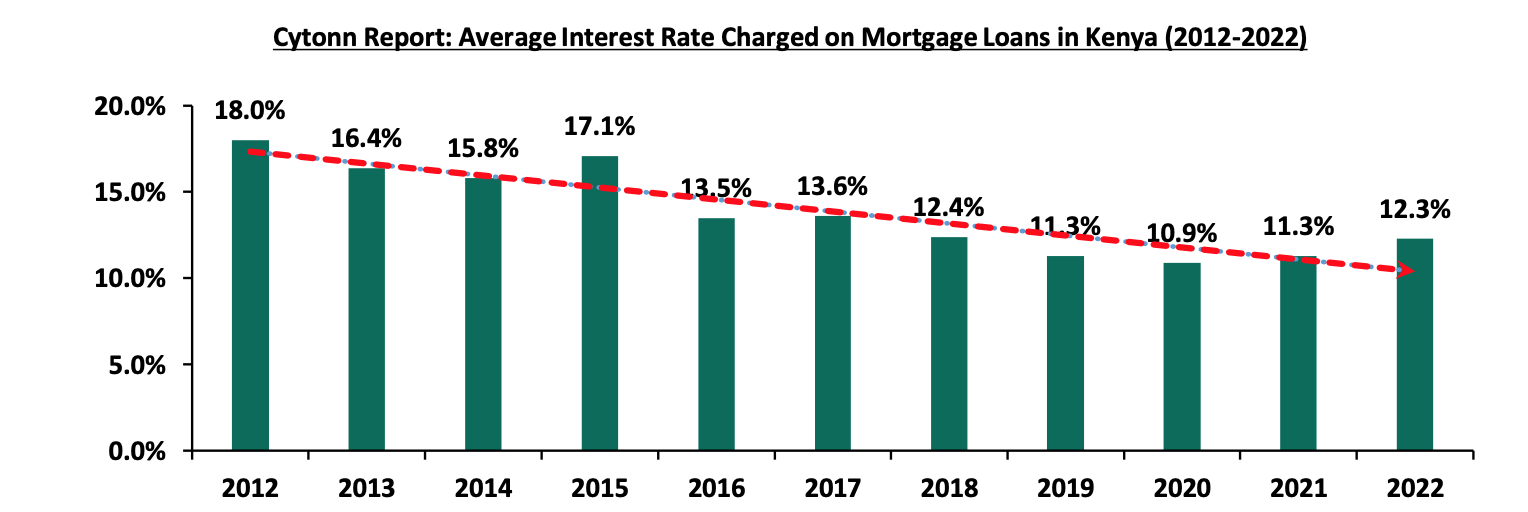

- Rising interest rates on loans: the Bank Supervision Annual Report 2022 by Central Bank of Kenya (CBK) which highlighted 1.0% points increase in interest rates charged on loans towards Real Estate developments to 12.3% in 2022, from 11.3% in 2021. The interest rates majorly ranged from 8.2% to 17.0% in 2022, compared to a range of from 7.1% to 15.0% recorded in 2021. The rise in the interest rates were in line with gradual increases in the MPC rate by CBK to 8.8% at the end of 2022, from 7.0% in 2021 aimed at curbing the elevated inflation rate. The rates are projected to even rise further illustrating return to pre-COVID-19 levels as majority of financial institutions begin to eradicate pandemic related reliefs in their new risk-based interest rate pricing formulas, making the loans more expensive. The graph below shows the trend in the average interest rate charged on mortgage loans in Kenya from 2012 to 2022:

Source: Central Bank of Kenya (CBK)

- Increasing Non-Performing Loans: the higher credit risks coincide with a 33.6% increase in the value of Non-Performing Mortgage Loans (NPMLs) to Kshs 37.8 bn in 2022, from Kshs 28.3 bn in 2021. This increase can be attributed to various factors that have made it challenging for a considerable number of housing investors and buyers to repay their loans which include; i) escalating construction costs over the years, ii) disruptions in the housing market activities caused by the COVID-19 pandemic and general elections, iii) the upward trend in prices of existing housing units, which has resulted in a slowdown in Real Estate sales, iv) rise in unemployment and income instability at the back of job losses, salary reductions and reduced business activities among borrowers, and, v) insufficient risk assessment can lead to a higher number of loans being extended to borrowers who are more likely to default,

- Decreasing the period of mortgage facilities to developers: the average maturity of the loans was 10.9 years ranging between 5 years and 18 years in 2022 as compared to loan maturity of 12 years recorded in 2021, ranging between 5 years and 20 years. As such, the financial institutions will continue to cushion themselves more against the heightened risk of default by investors in the Real Estate sector.

In light of the prevailing challenges in the industry, stakeholders are increasingly adjusting to off-plan investment which emerges as a unique alternative in progressing developments and stimulate activities in the sector majorly target to; i) lower the cost of purchasing housing units in comparison to buying ready-made units from the market, ii) protect the rights of buyers by establishing procedures and systems that ensure developers adhere to the agreed-upon project completion timelines and contractual obligations, and, iii) promoting competition among Real Estate development companies by implementing a system for qualifying and classifying developers.

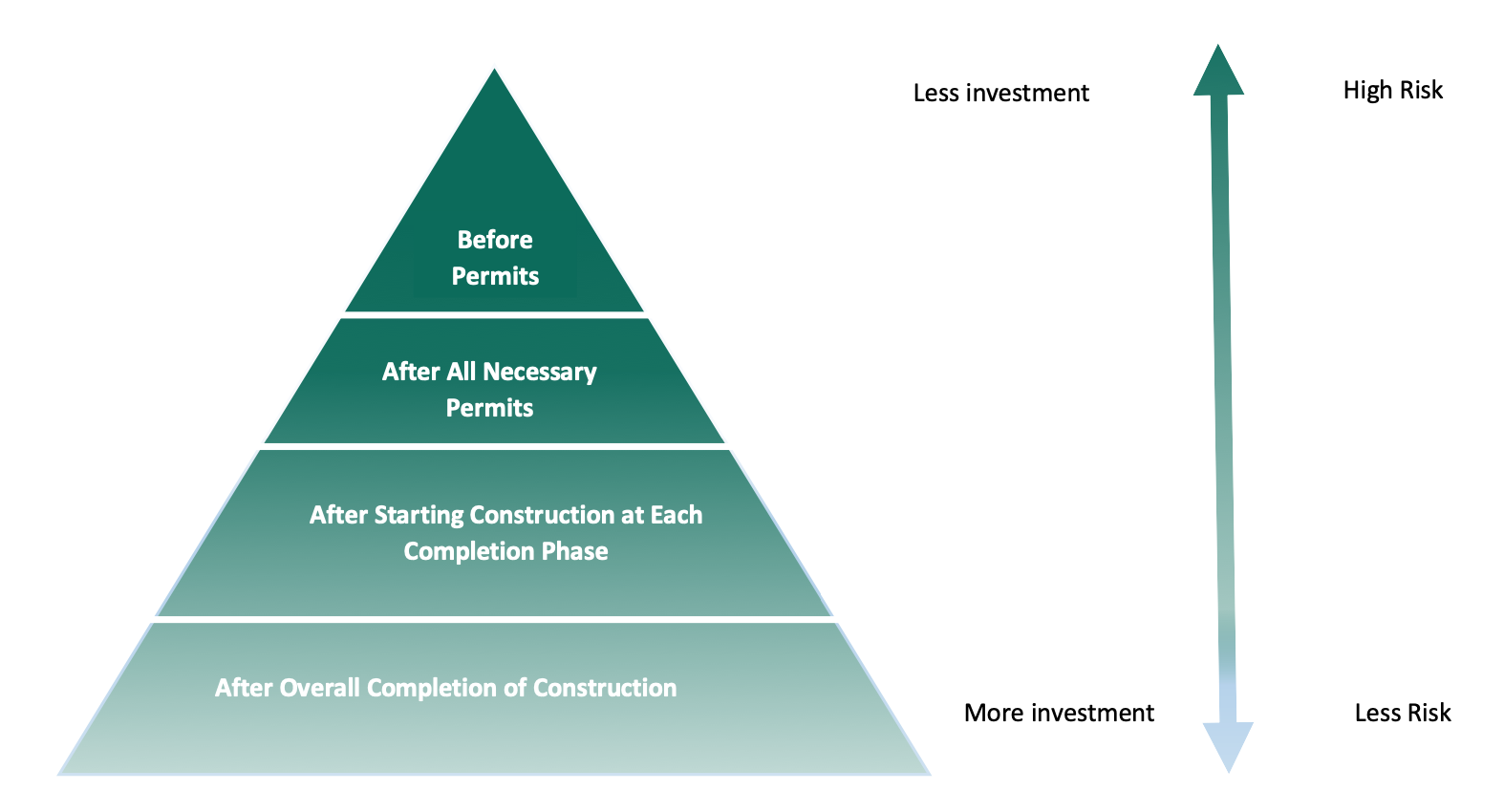

The concept of off-plan investment stands out from other sales programs due to its unique combination of financing and marketing strategies. This approach allows developers to secure funding by selling Real Estate units before construction begins, eliminating the need for costly bank fees and interest that could potentially inflate housing unit prices. Furthermore, it provides developers with valuable insights into market demand and allows them to assess buyer satisfaction and acceptance of their products. The process of off-plan sales typically involves multiple stages with varying levels of risk, which developers must carefully analyze. Initially, buyers are offered the opportunity to invest in the project at significant discount rates, even before construction starts and permits are obtained. This early stage carries a higher level of risk as the execution of the project and completion of construction is uncertain, despite thorough due diligence. However, as the project progresses and completion rates increase, the level of risk decreases, and developers adjust the discount rates offered to subsequent investors. When the project is near completion, the risk becomes very low or even non-existent as the physical nature of the project becomes evident, including the presence of amenities. However, buyers who purchase units at this stage may need to pay higher prices as developers aim to maximize profits, complete the finishing touches, initiate the handover process, and secure additional funds for property management and the operationalization of other on-site facilities. The chart below demonstrates the level of risk and amount of investments incurred by buyers during the life of an off-plan development project;

Source: Cytonn Research

Factors that have Contributed to the Concept’s Growth in Popularity Over the Years