Feb 16, 2025

Infrastructure development remains one of the key objectives of the Kenyan government as it seeks to achieve its vision 2030. Good infrastructure reduces costs of doing business, attracts foreign investment, opens up remote areas to investment and boosts the trade competitiveness of the country. Recognizing this, the government continues to actively support infrastructure expansion through financing strategies such as Public-Private Partnerships (PPPs), infrastructure bonds, debt financing, and substantial budgetary allocations, with a primary focus on road networks.

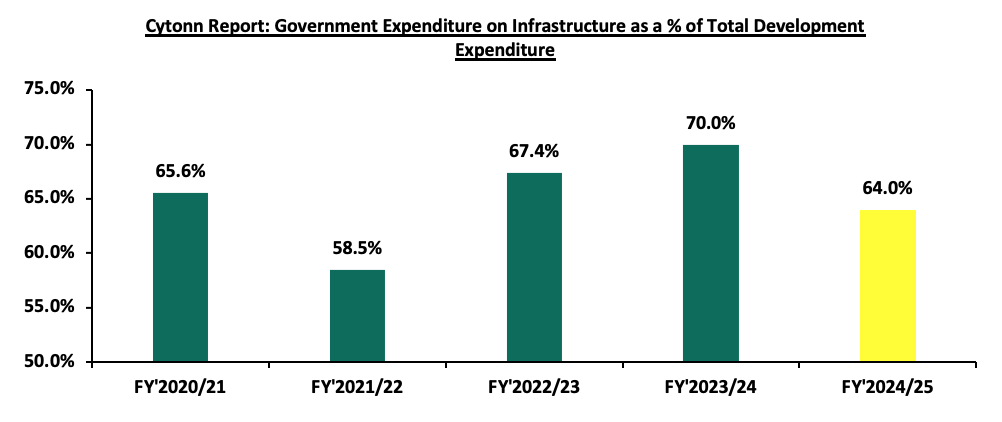

According to the Kenya National Highways Authority (KeNHA) 2023-2027 Strategic Plan, the authority aims to construct 2,349 km of roads, including 1,183 km of new roads, capacity enhancements of 674 km, and rehabilitation of 492 km. Additionally, KeNHA plans to maintain 75,891 km of national trunk roads and design 5,575 km of road networks during this period. The implementation of this strategic plan requires Ksh 708.7 bn, with Ksh 99.3 bn sourced through PPPs, Ksh 1.7 bn from climate funding, and Ksh 8.2 bn from own-source revenue. The graph below illustrates the government's infrastructure expenditure as a percentage of total development spending from FY’2020/21 to FY’ 2024/25, emphasizing the sustained priority on infrastructure, which consistently accounts for more than 50% of the total development budget.

Source: National Treasury of Kenya

Despite these efforts, infrastructure funding gaps remain a major challenge in the achievement of the Kenyan government development goals a situation also being experienced in the rest of African countries. According to the African Development Bank Group , Africa as continent has an infrastructure funding gap of USD 402.2 bn with transport infrastructure accounting for the largest share at 72.9% equivalent to USD 293.2 bn. Narrowing down to Kenya, the country is estimated to be facing a USD 2.1 bn annual infrastructure financing gap creating a need for mobilization of more resources to meet the gap.

Given this, the government has been exploring diverse infrastructure funding strategies recently partnering with a US-based infrastructure investment firm Everstrong Capital-who aim to secure funds from local financial institutions such as pensions and banks amounting to approximately Kshs 129.0bn for financing the construction of the 440.0 kilometer Nairobi-Mombasa Expressway at an estimated cost of USD 3.5 bn (Ksh 455.0 bn). In this note, we aim to analyze this initiative by specifically looking into:

- Overview of Everstrong Capital

- About Usahihi Expressway

- What is the Probability of raising USD 1 bn (Ksh 129.2bn) from Local Pension Funds?

- Conclusion and Recommendations for the Project

Section I: Overview of Everstrong Capital

Everstrong Capital is an American infrastructure fund manager founded in 2015 by Philip Dyk, with its offices in United States, South Africa and Kenya. The firm specializes in late-stage development opportunities with a primary focus on Sub- Saharan Africa, aiming to make investments that positively impact human lives, families, communities and regions. Everstrong Capital concentrates on developing and investing in sustainable infrastructure across several key sectors including energy, power, transportation, communication, healthcare and housing.

Impact and achievement:

Everstrong Capital has invested in numerous projects across Sub-Saharan Africa, particularly in the transportation, communication, social infrastructure, energy and power sectors. Some of the notable achievements include;

- The Everstrong Kenya Infrastructure Fund, in February 2022, acquired a majority stake in Seal Towers Ltd- a provider of cell towers, tower infrastructure and related services. The strategic investment aims to support a tower expansion plan, and also enhance connectivity to underserved areas in Kenya.

- In 2018, Everstrong Capital became an investor in Gulf power, a company that plays a role in meeting Kenya’s energy demand. Gulf power operates an 80-megawatt power-generation facility near Athiriver, which commenced commercial operations in 2014, generating electricity using heavy fuel oil (HFO) and Light fuel oil (LFO). Gulf Power has a 20-year power purchase agreement (PPA) with Kenya Power & Lighting Company.

- Everstrong EV Africa is a subsidiary of Everstrong capital developing and investing in electric vehicle verticals in Kenya and across Sub-Saharan Africa with specific focus is on electric motorcycle and bus manufacturing, charging, finance and operation.

- Everstrong is also sponsoring a pan-Africa energy platform Milele Energy (which rebranded to Osprey renewables ) that provides capital and development expertise in power projects within sub-Saharan Africa. Recently, Milele Energy through Gemcorp capital seeded USD 150.0 mn purchasing a significant stake at the Kenya’s Lake Turkana Wind power Project.

- Milele Energy’s Salone power project secured a 20-year power purchase agreement (PPA) with the government of Sierra Leone. The 83.5MW gas power plant received USD 217 mn in loan approval and USD 54mn in political risk insurance from the US International Development Finance Corporation (US DFC). Once operational, the project is expected to supply 24% of the country’s electricity demand, lower energy costs, and support Sierra Leone’s transition to renewables.

Section II: About Usahihi Expressway

The Usahihi Expressway is a 440-Kilometre dual carriageway connecting Nairobi to Mombasa estimated to cost approximately USD 3.5 bn (Ksh 455.0 bn), leaving developer with a balance of USD 2.5 bn to raise from external markets. Additionally, Everstrong is providing USD 100.0 mn for land acquisition along the path the road will pass. The project is expected to be developed under a Public-Private Partnership (PPP) with a Build Operate- Transfer (BOT) model with a 30-year concession period. Designed with four to six lanes, it includes modern amenities, electric vehicle charging stations powered by renewable energy, and wildlife overpasses to preserve migration routes. The expressway aims to cut travel time between Nairobi and Mombasa from 10 hours to 4.5 hours, benefiting businesses, travelers, and freight operators. In contrast, the Nairobi Expressway, which cost approximately USD 681.7 mn (Ksh 88.0 bn), was developed under a PPP model but with full private sector financing led by the China Road and Bridge Corporation (CRBC) under an Operate-Maintain-Transfer (OMT) model. Unlike the Usahihi Expressway, which is expected to involve multiple private investors, including pension funds and local banks, the Nairobi Expressway was largely financed by a single foreign entity, limiting local investment participation.

Funding structure;

Everstrong Capital, in partnership with CPF Capital Advisory Limited, is aiming to secure Ksh 129.0 bn (USD 1.0 bn) as initial funding for the project through local pension funds, investment banks, and insurance companies, leveraging Kenya’s capital markets to sustain the project’s financial needs. The project will be continuously funded and operated under a concession model, allowing investors to recoup their investment through toll revenue over 30 years.

Section III: Feasibility of Raising the Kshs 129.2 bn from Local Pension Funds in Kenya

- Growth of Retirement Benefits Schemes

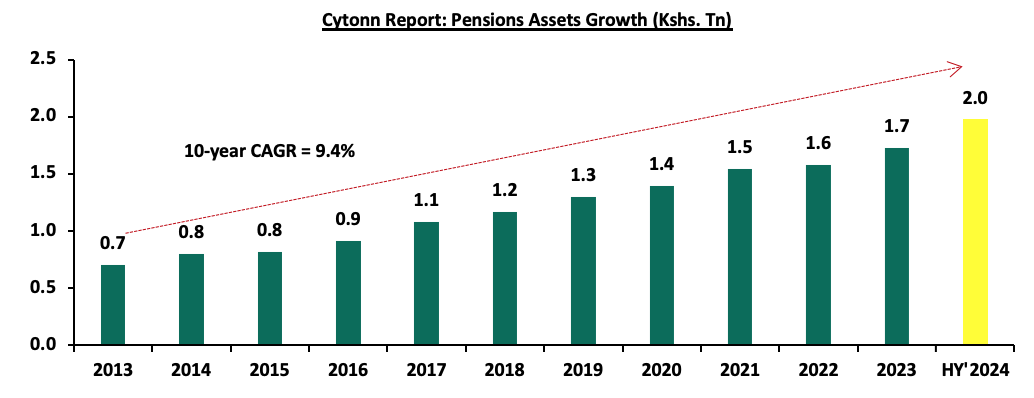

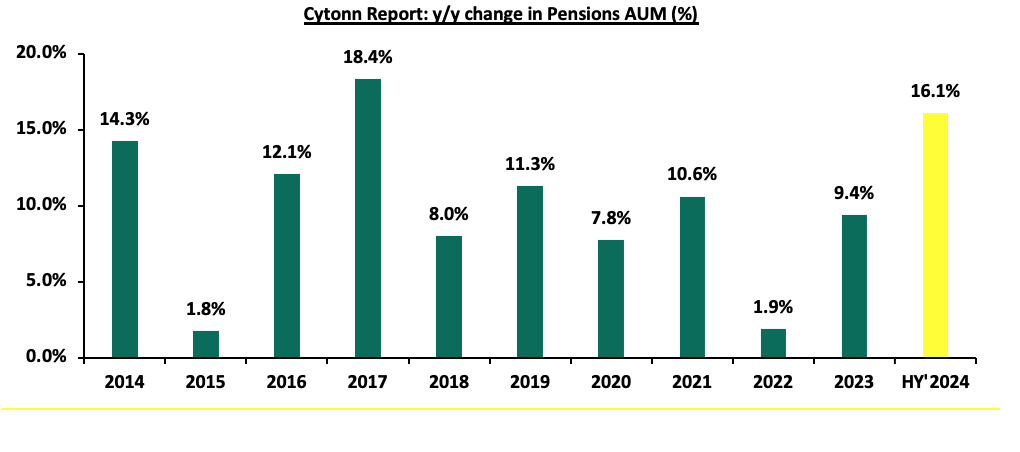

According to the latest Retirement Benefits Authority (RBA) Industry Report for June 2024, assets under management for retirement benefits schemes increased by 14.7% to Kshs 2.0 tn in June 2024 from the Kshs 1.7 tn recorded in December 2023. The growth of the assets was attributed to the improved market and economic conditions during the period as evidenced by improved business conditions, eased inflationary pressures and stability of the exchange rate. The Purchasing Manager’s Index (PMI) for HY’2024 came in at 50.0, up from 48.7 recorded in HY’2023. Additionally, the average inflation rate in HY’2024 came in at 5.6% compared to 8.5% recorded in a similar period in 2023. Notably, on a year-on -year basis, assets under management increased by 16.1% from the Kshs 1.7 tn recorded in June 2023, partly attributable to the enhanced contributions to the mandatory scheme, NSSF, which began in earnest in February 2023 following the court of appeal ruling.

The graph below shows the growth of Assets under Management of the retirement benefits schemes over the last 10 years:

The chart below shows the y/y changes in the assets under management for the schemes over the years.

- Retirement Benefits Schemes Allocations in Various Investment Opportunities

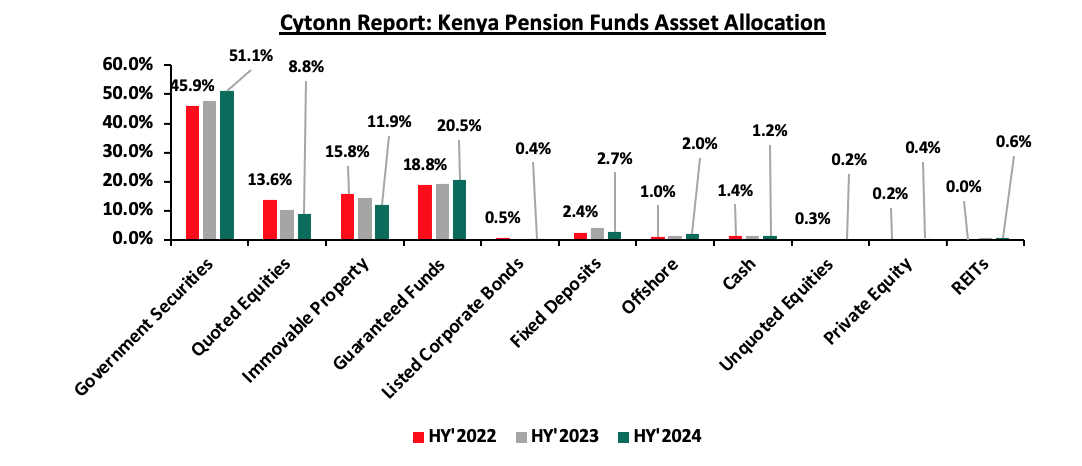

Retirement Benefits Schemes strategically allocate funds across various asset classes available in the market to safeguard members' contributions while striving to generate attractive returns. These schemes have access to a diverse range of investment opportunities, including traditional asset classes such as equities and fixed income securities. Additionally, they can explore alternative investments such as real estate, private equity, infrastructure, and other non-traditional assets, which may offer higher returns and diversification benefits. The choice of investments is guided by the scheme's Investment Policy Statement (IPS), regulatory guidelines, and the need to align with the risk tolerance and long-term goals of the members. The table below represents how the retirement benefits schemes have invested their funds in the past:

|

Cytonn Report: Kenyan Pension Funds’ Assets Allocation |

||||||||||||||

|

Asset Class |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

HY’2024 |

Average |

Limit |

|

|

Government Securities |

31.0% |

29.8% |

38.3% |

36.5% |

39.4% |

42.0% |

44.7% |

45.7% |

45.8% |

47.5% |

51.1% |

41.1% |

90.0% |

|

|

Immovable Property |

17.0% |

18.5% |

19.5% |

21.0% |

19.7% |

18.5% |

18.0% |

16.4% |

15.8% |

14.0% |

11.9% |

17.3% |

30.0% |

|

|

Quoted Equities |

26.0% |

23.0% |

17.4% |

19.5% |

17.3% |

17.6% |

15.6% |

16.5% |

13.7% |

8.4% |

8.8% |

16.7% |

70.0% |

|

|

Guaranteed Funds |

11.0% |

12.2% |

14.2% |

13.2% |

14.4% |

15.5% |

16.5% |

16.8% |

18.9% |

20.8% |

20.5% |

15.8% |

100.0% |

|

|

Fixed Deposits |

5.0% |

6.8% |

2.7% |

3.0% |

3.1% |

3.0% |

2.8% |

1.8% |

2.7% |

4.8% |

2.7% |

3.5% |

30.0% |

|

|

Listed Corporate Bonds |

6.0% |

5.9% |

5.1% |

3.9% |

3.5% |

1.4% |

0.4% |

0.4% |

0.5% |

0.4% |

0.4% |

2.5% |

20.0% |

|

|

Offshore |

2.0% |

0.9% |

0.8% |

1.2% |

1.1% |

0.5% |

0.8% |

1.3% |

0.9% |

1.6% |

2.0% |

1.2% |

15.0% |

|

|

Cash |

1.0% |

1.4% |

1.4% |

1.2% |

1.1% |

1.2% |

0.9% |

0.6% |

1.1% |

1.5% |

1.2% |

1.1% |

5.0% |

|

|

Unquoted Equities |

1.0% |

0.4% |

0.4% |

0.4% |

0.3% |

0.3% |

0.2% |

0.2% |

0.3% |

0.2% |

0.2% |

0.4% |

5.0% |

|

|

REITs |

0.0% |

0.0% |

0.1% |

0.1% |

0.1% |

0.0% |

0.0% |

0.0% |

0.0% |

0.6% |

0.6% |

0.1% |

30.0% |

|

|

Private Equity |

0.0% |

0.0% |

0.0% |

0.0% |

0.1% |

0.1% |

0.1% |

0.2% |

0.2% |

0.3% |

0.4% |

0.1% |

10.0% |

|

|

Others e.g. unlisted commercial papers |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.1% |

0.2% |

- |

0.0% |

0.0% |

10.0% |

|

|

Commercial Paper, non-listed bonds by private companies |

- |

- |

- |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.2% |

0.0% |

10.0% |

|

|

Total |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

|

Source: Retirement Benefits Authority

Retirement benefits schemes have for a long time skewed their investments towards traditional assets, mostly, government securities and the equities market, averaging 57.8% as of 30th June 2024 for the two asset classes, leaving only 42.2% for the other asset classes. However, as pension schemes seek higher returns, diversification, and inflation hedging, there has been a growing shift towards alternative investments that include immovable property, private equity as well as Real Estate Investments Trusts (REITs). It is vital to note, that in HY’2024 the second largest increase in allocation was recorded in investments in private equity by 63.3% to Kshs 8.8 bn from Kshs 5.4 bn recorded in HY’2023 and investments in Real Estate Investments Trusts increased by 4.5% to Kshs 11.1 bn in HY’2024 from Kshs 10.6 bn in HY’2023. However, allocation to immovable property decreased by 4.1% to Kshs 236.3 bn in HY’2024 from Kshs 246.3 bn in HY’2023.

The graph below shows pension funds allocation to the various asset classes, as of HY’2024;

Source: RBA Industry Report

- Funding Feasibility

The shift towards alternative investments, as shown in the analysis above, presents a strong opportunity for Everstrong Capital to secure funding from local pension schemes. According to the Retirement Benefits Authority Investment Regulations and Policies, pension schemes can invest up to 10.0% of their total assets under management in debt instruments for the financing of infrastructure or affordable housing projects approved under the Public Private Partnerships Act. Kenya's pension schemes are increasingly investing in infrastructure projects to diversify their portfolios, achieve stable long-term returns, and contribute to national development. A significant initiative in this direction is the Kenya Pension Funds Investment Consortium (KEPFIC), established in 2018. KEPFIC is a collective of prominent Kenyan retirement benefit funds that have united to make long-term investments in infrastructure and alternative assets within the region. As of the latest report, KEPFIC has mobilized over USD 113.0 mn into projects such as roads, student housing, and affordable housing, involving 88 local pension funds. The table below shows the breakdown:

|

Cytonn Report: KEPFIC Investment Mobilization |

|||

|

Opportunity |

Investment Need (USD mn) |

KEPFIC Mobilization (USD mn) |

% Achieved |

|

KMRC Affordable Housing Bond |

14.0 |

52.1 |

372.1% |

|

Lot 3 Road Annuity Project Bond |

20.0 |

50.0 |

250.0% |

|

Acorn Student Accommodation REITs |

50.0 |

11.0 |

22.0% |

|

Total |

84.0 |

113.1 |

134.7% |

Source: kepfic.co.ke

Pensions funds exceeded the total investment for the three projects, mobilizing USD 113.1 mn out the required USD 84.0 mn, translating to 134.7%. This indicates a strong appetite for infrastructure and real estate projects by pension schemes in Kenya and their growing role in infrastructure financing. Notably, the road annuity project received 250.0% of the needed funds, demonstrating a preference for projects with stable and attractive returns. Everstrong Capital intends to secure the funding through a Public -Private Partnership (PPP) model backed by local pension schemes, investment banks and insurance companies in Kenya. Based on the analysis, Everstrong Capital has a strong opportunity to raise a significant portion of the required Kshs 129.2 bn from local pension schemes, given the increasing appetite for infrastructure investments. The success of Kenya Pension Funds Investment Consortium (KEPFIC) in mobilizing USD 113.1 bn for infrastructure and real estate investments further highlights the ability of pension schemes to fund long-term projects. Additionally, the Lot 3 Road Annuity Project Bond secured 250.0% of its required funding, highlighting the strong appeal of well-structured road projects under PPP models for pension funds. This bond has an eight-year tenor and offers returns benchmarked against the government’s 8-year securities interest rate, which currently stands at 12.2%. Repayments will be made quarterly after the project is completed. However, the Kshs 129.2 bn target represents 6.5% of the total pension industry AUM; Kshs 1,978.8 bn as of June 2024, which is a substantial amount. While pension funds have the capacity under regulatory limits, mobilizing the full amount from this single source may be challenging. Given past trends, our expectation would be for pension schemes to contribute between 30.0% and 50.0% of the required funding target of Kshs 129.2 bn, which is approximately Kshs 38.8 bn to Kshs 64.6 bn.

Pension funds have an alternative investment option in infrastructure bonds issued by the Kenyan government. Infrastructure bonds (IFBs) are a preferred investment for pension funds due to their low risk, government backing, and tax-exempt status. These bonds offer fixed returns and are attractive for investors seeking stability and predictable cash flows. Currently, IFBs in Kenya provide competitive yields, with current yields to maturity of ranging between 11.2% and 15.7% and tenors of up to 25.0 years.

The Usahihi Expressway is expected to generate revenue primarily through toll collections over the 30-year concession period. Toll roads historically provide stable, inflation-hedged cash flows, making them attractive to long-term institutional investors like pension funds. Consequently, pension funds looking for higher return potential may consider the Usahihi Expressway as an alternative. Unlike IFBs, which offer fixed returns, toll roads generate cash flows that grow over time, as toll rates can be adjusted for inflation and traffic volumes are expected to increase. This allows for potentially higher long-term returns compared to the fixed yields of IFBs. Additionally, infrastructure projects like this enhance portfolio diversification and provide exposure to real assets with long-term economic value.

- Conclusion and Recommendations for the Project based on our analysis

Based on our analysis, Usahihi Expressway project, backed by Everstrong Capital, has a viable opportunity to secure partial funding from local pension funds, given the increasing appetite for infrastructure investments. However, raising the full Kshs 129.0 bn from pensions schemes alone may be challenging, our expectation would be pension schemes to contribute between 30.0% and 50.0% of the amount while the rest can be supplemented by the local banks, saccos, high net worth investors and unit trust. To bridge the funding gap, the Usahihi Expressway project can explore alternative financing options such as green financing strategies e.g. a green bond or climate finance which would attract investors focused on sustainable projects and enhance the project's environmental credibility while diversifying its funding sources.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice, or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma