Jul 28, 2019

Following the launch of the Derivatives Market in Kenya at the Nairobi Securities Exchange (NSE) on July 11th, 2019 (see our Topical here), investors have a new investment avenue in the Kenyan market, which is expected to diversify the existing product offering. In light of this development, it is important to examine the current investment options in the Kenyan market.

This week we focus on the investment options in the Kenyan market, where we shall discuss the following:

- Overview of Investments,

- Categories of Investment Products in the Kenyan Market, and,

- Conclusion: We give considerations an investor should take into account before choosing an investment option, highlighting the returns for the different asset classes as well as the inherent risks.

After this discussion, we shall follow up with a note on financial planning, to help investors make the appropriate decision on the most suitable investment product based on the existing options, and their individual circumstances and preferences.

Section I: Overview of Investments

An investment is the purchase of an asset with the intention to generate income or having the asset appreciate, hence selling it at a profit. Investment is mainly characterized by the three following factors;

- Return – This is compensation received for making an investment. All investments are characterized by the expectation of a return. The return may be received in the form of yield, dividend, and/or capital appreciation,

- Risk – This is the chance of a loss on the principal amount of an investment, and,

- Liquidity - This is the level of ease with which an investment can be easily converted to cash without taking a significant discount in value.

Section II: Categories of Investment Products in the Kenyan Market

Kenyan investment products are mainly categorized into two categories:

-

- Traditional Investments

- Alternative Investments

- Traditional Investment Products

Traditional investments involve putting capital into well-known assets that are sometimes referred to as public-market investments. The main categories of traditional investment products include:

- Equities – Equity represents an ownership interest in a company listed at a securities exchange, in the form of either common stock or preferred stock. With common stock, the shareholder has voting rights and is entitled to dividends depending on how much profit the company makes. On the other hand, with preferred stock, shareholders have no voting rights and are entitled to dividends at a pre-determined rate, which takes precedence over common stock shareholders. An example of an investment in equities is purchasing shares in Safaricom at the Nairobi Securities Exchange (NSE) via a licensed broker.To invest in the equities market in Kenya, one would need to open a Central Depository and Settlement (CDS) account, which is an electronic account that holds your shares and bonds, and allows for the process of transferring of shares at the Securities Exchange, through a licensed stockbroker. With an investment in equities, an investor stands to gain from capital appreciation in the event the stock trades at higher prices than the purchase price, and dividends declared by the respective companies. In Kenya, the Nairobi Securities Exchange facilitates the trading of shares of 62 public companies with a market capitalization of Kshs 2.3 trillion as at 25th July 2019.

- Fixed Income Securities – These are debt securities that provide a return in the form of fixed periodic interest payments and the repayment of the principal upon maturity. The following are the types of fixed income securities:

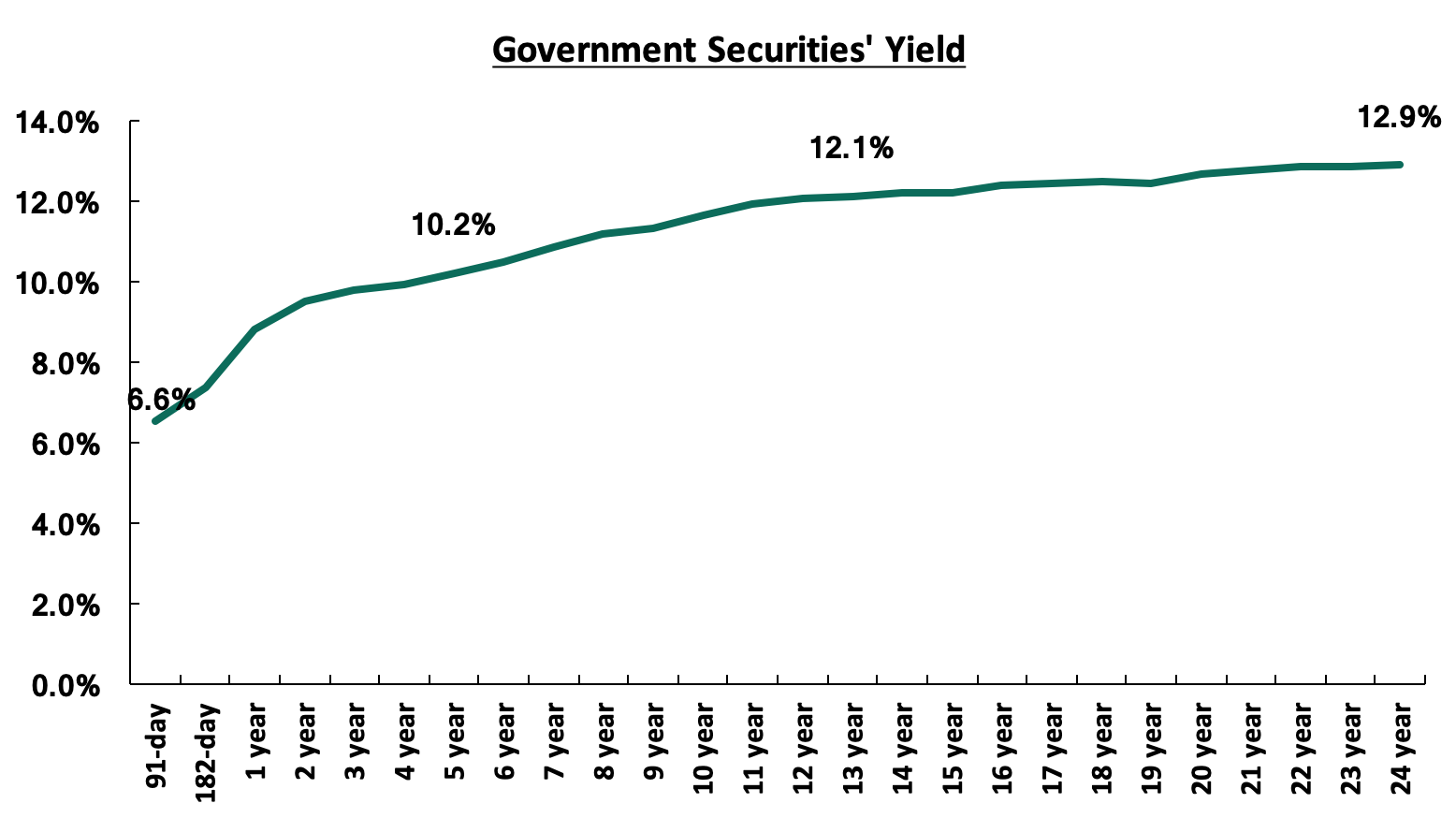

- Treasury Bills – These are promissory notes issued and fully guaranteed by the government. They are short-term investments and can have tenors of 91, 182 or 364-days. The current rates for 91-day, 182-day or 364-day are 6.6%, 7.4% and 9.0%, respectively;

- Treasury Bonds – These are long-term debt securities issued by the government with tenors of greater than 1-year. Investors stand to gain from capital gains in the event of trading at the stock exchange dependent on the performance of the bonds, and interest payments made at regular intervals over the tenor of the bond.

To invest in government securities, one can open a CDS account either through the Central Bank of Kenya, if he/she holds a bank account with a local commercial bank, or open one with a commercial bank in Kenya, who then execute transactions on behalf of their clients. Currently, the government securities’ market has a normal shaped yield curve with the market skewed towards the longer-dated government securities with the 91-day, 5-year and 24-year government securities having yields of 6.6%, 10.2%, and 12.9%, respectively. With the normal shaped yield curve, investors expect a higher return for a longer period of investment as it carries greater risk. The graph below shows the current yields of short-term to long-term government securities in the Kenyan markets.

Source: Central Bank of Kenya

- Commercial Papers – These are promissory notes issued by companies as a form of raising short-term debt. These securities can be secured or unsecured and are priced at a premium to the Treasury Bills. They are short-term securities for tenors up to one year and mainly target institutional investors. Investors stand to gain from yields which are derived from the difference between the maturity value and price when issued. Commercial papers in the market currently yield from 12% to 18% p.a.;

- Corporate Bonds – These are long-term secured debt securities issued by companies with approval from the Capital Markets Authority (CMA) and are priced at a premium to Treasury Bonds. They are normally listed on an exchange. Investors stand to gain from periodic interest payment over the life of the bond. Current corporate bonds in the market are yielding from 8.5% to 10.8% per annum;

- Bank Deposits – These are deposits placed with banks or financial institutions, which could either be term deposits, which are fixed-term investments with withdrawals after a certain period lapses, or call deposits, which have no fixed deposit period, allow for unlimited withdrawals and deposits and operate like a savings account through the accrual of interest. As per our weekly Money Markets offers, 90-day bank deposits are currently at 8.8%, (based on what we have been offered by various banks);

- Debentures – These are long-term unsecured debt securities issued by companies, which are issued through private placement, and provide periodic interest payments to investors. These securities are mainly purchased by institutional investors with the holders of the debentures having a claim over general creditors. Debentures are supposed to yield higher than corporate bonds, hence around 12.8% per annum.

- Mutual Funds / Unit Trust Funds - This is a collective investment scheme that pools money together from many investors and is managed by a professional fund manager who invests the pooled funds in a portfolio of securities to achieve objectives of the trust. The funds in the mutual fund earn income in the form of dividends, interest income and/or capital gains depending on the asset class the funds are invested in. The following are the main types of mutual funds:

- Money Market Fund – This fund mainly invests in short-term debt securities with high credit quality such as bank deposits, treasury bills, and commercial paper. An example is the Cytonn Money Market Fund (CMMF);

- Equity Fund – This fund aims to offer superior returns over the medium to longer term by maximizing capital gains and dividend income through investing in listed securities;

- Fixed Income Fund – This fund invests in interest-bearing securities which include treasury bills, treasury bonds, preference shares, corporate bonds, loan stock, approved securities, notes and liquid assets consistent with the portfolio’s investment objective;

- Balanced Fund – This fund invests in a diversified spread of equities and fixed income securities with the objective to offer investors a reasonable level of current income and long-term capital growth. For more information, please read our topical on Investing in Unit Trust Funds.

At the end of 2018, the total Assets Under Management (AUM) under Unit trusts were Kshs 58.0 bn, with the top five fund managers, who control 82.4% of the total AUM highlighted below:

|

No. |

Unit Trust Fund Manager |

AUM |

% of Market Share |

|

1 |

CIC Asset Managers |

20,270.8 |

34.9% |

|

2 |

British American Asset Managers |

8,841.6 |

15.2% |

|

3 |

Old Mutual |

6,578.8 |

11.3% |

|

4 |

ICEA Lion |

6,951.9 |

12.0% |

|

5 |

Commercial Bank of Africa |

5,189.7 |

8.9% |

|

|

Total |

47,832.9 |

82.4% |

All values in Kshs millions unless stated otherwise

The leading unit trust products by AUM are money market funds, equity funds and balanced funds with Kshs 48.9 bn, Kshs 4.8 bn and Kshs 1.9 bn, respectively, in AUM and with a market share of 84.3%, 8.3%, and 3.3%, respectively. For more information, please see our press release on the Overview of the 2018 Performance by Unit Trust Fund Managers.

- Pension Funds – This is an investment fund where individuals contribute their pensions, which are invested in various asset classes as per regulation, and from which payments are made upon retirement, which could be in a lump sum or periodic payments. Pension funds can be categorized by type of returns – guaranteed funds, which offer a guaranteed minimum rate of return, and segregated funds, which offer market-based returns. Alternatively, they can be categorized by mode of contribution, where we have individual retirement benefit schemes, where individuals can contribute directly into the fund towards saving for their retirement, and umbrella retirement benefit schemes, that pool the contributions of multiple employers and their employees.

We have classified pension as a traditional product because they largely invest in traditional products such as equities and debt, but they are also allowed to allocate to alternative investments. For more information, see our note on Retirement Benefits Schemes in Kenya.

The main advantages of traditional investment products include:

- Availability of Information - Companies offering traditional investment products in the market are required by law to publish information on a regular basis with the frequency-dependent on the asset class and thus investors have an opportunity to analyze how the market is performing and make logical investment decisions;

- Standardized, well known and easy to understand structures;

- High Liquidity – Majority of the traditional investment classes have a ready market for disposal of the assets and thus can be easily converted to cash; and,

- Regulation - Traditional investment products operate under the supervision of the regulatory bodies such as the CMA and the Retirement Benefits Authority (RBA) among others, who layout procedures to follow when making a transaction or allocation of funds for the mutual funds which presents a form of safety to any investment made.

The main disadvantages of traditional investment products include:

- Lower returns relative to alternative markets – The real returns from traditional investments, when inflation is taken into account, tend to be lower than alternative investments which are less volatile;

- High Correlation of Returns – This is the relation of movement in prices of assets in the market. Traditional investment products such as equities are known to have similar movements in the market, especially when there is a movement in the large cap stocks, this affects the performance of other equities in the market; and,

- The volatility of Returns – traditional investment products such as stocks and bonds are highly sensitive to market changes such as inflation and interest changes and thus performance is pegged on the prevailing market conditions. Furthermore, when the returns are adjusted for price changes as a result of inflation, the real return may not be as high as expected.

- Alternative Investment products

Alternative investments are those that fall outside the conventional category of investments such as publicly-traded equities and fixed income securities. The clientele of this investment category is mainly institutional investors and high-net-worth individuals.

The main types of alternative investment products in the Kenyan market include:

- Private Equity - This involves buying shares that are not listed on a public exchange or buying shares of a public company with the intent to privatize them. Private equity involves the following strategies:

- Venture Capital – This is the investment of capital into a small business or start-up which has the potential of growth in the long run. This investment takes form depending on the purposes the funds are used;

- Seed capital – This is funding provided for purposes of research, evaluation and the development of a concept before the company commences operations;

- Early-stage capital – This is funding for the establishment of new companies or the development of companies which have been in operations for a short period of time; and,

- Development capital – This is funding for purposes of growth or expansion of a company;

- Buyouts – This involves financing established companies that require money to restructure and facilitate a change of ownership;

- Growth Capital – This is funding in relatively mature companies looking for capital to expand into new markets, or finance a significant acquisition, and,

- Distressed Investing – This involves investing in companies in financial distress, where the capital is used to pay the debt and restructure the company.

- Venture Capital – This is the investment of capital into a small business or start-up which has the potential of growth in the long run. This investment takes form depending on the purposes the funds are used;

The following are the exit strategies and ways in which investors can recoup their investments:

- Initial Public Offering (IPO) – This is where private companies would offer their shares to the general public. This is a form of attracting the highest possible returns for the private equity sponsors which is fully dependent on market sentiment and conditions;

- Trade sell – This is where a private equity investor opts to sell all the shares held in a company to a third party purchaser. In most cases the third party purchaser operates in the same environment and has synergies to be brought out by acquiring the target company, for which it is willing to pay a premium;

- Secondary buyout – This is where a company held by one private equity investor is sold to another private equity sponsor which may allow for an investor to have a fast exit as compared to a trade sale;

- Leveraged recapitalization – This method allows a private equity investor to extract cash from the business without selling the company which is achieved through borrowing more money from a bank or issuance of bonds; and,

The Private Equity Market in Kenya is estimated to have USD 1.3 bn (Kshs 135.1 bn) in value of reported deals according to the African Private Equity and Venture Capital Association in 2018.These investments are mainly concentrated in the consumer and technology related sectors, information and technology, financial services and the real estate sectors, which accounted for 18.0%, 15.0%, 11.0% and 10.0%, respectively, of total deal value, respectively. The largest players in the Kenyan private equity landscape are Actis Capital, Centum Investments and Catalyst Principal Partners.

- Derivatives Market – This is the purchase of a financial contract whose value is derived/reliant on the value of an underlying asset, which may be a commodity, bond, equity, interest rate, market index, currency or real estate. The main types of derivatives contracts include:

- Forward contracts– These are private agreement contracts that can be customized to a specific commodity, specific quantity of the commodity and agreed-upon delivery date at a future point in time;

- Options contract – This type of derivative gives the holder of the option contract the right but not obligation to buy/sell the underlying asset at a specified price (strike price), at a set time in the future;

- Futures contract – This is a financial contract between two parties where both partied agree to buy/sell a particular asset at a predetermined price at a specific date;

- Swaps contract – This is a financial contract where two parties agree to exchange the cash flow from two different financial instruments; and,

- Warrants – These securities entitle the holder the right to purchase a company’s stock at a specific price at a specific date.

The derivatives market was officially launched on the 11th of July 2019 on the Nairobi Securities Exchange (NSE), and currently facilitates the trading of equities index futures contract and single stock futures contracts of large-cap stock such as Safaricom, Equity Group, KCB Group, EABL and BAT Kenya. The derivatives market is expected to provide a form of hedging against volatile stock prices, higher returns, lower transaction costs and lower credit risk with the NSE Clear in place. For more information, please read our topical on Understanding the Derivatives Market;

- Real Estate– This involves the purchase of land, buildings for the purposes of income generation. The real estate market is divided into four categories which include; the residential sector, the industrial sector, the commercial and retail sector, and mixed-use developments. An investment in real estate can also be made through a Real Estate Investment Trust (REIT), which is a regulated investment vehicle that enables a collective investment in real estate, as investors pool their funds and invest in trust with the intention of earning profits or income from real estate. There are three forms of REITs which include:

- Income REITs (I-REITs) – This is a form of REIT in which investors pool resources for the purpose of acquiring long-term income-generating real estate including housing, commercial and other real estates. They are typically listed in an exchange. An example is the Fahari I-REIT;

- Development REITs (D-REITs) – This is a type of REIT in which resources are pooled together for purposes of acquiring eligible real estate for development and construction project; and,

- Islamic REITS – This is an Islamic REIT that invests primarily in income-producing Shariah-compliant real estate. Requires a fund manager to conduct a compliance test before investing in real estate to ensure it is Shariah-compliant. For more information, please read our article on Understanding Real Estate Investment Trusts.

- Structured Products – These are products that are highly customized/tailor-made investment products that are packaged by investment professionals, to enable the investor to access returns that are not accessible in the conventional market. There are publicly placed structured products, however, the majority are privately placed. Examples of privately placed structured solutions include structured notes which are backed by high yielding assets such as real estate and commercial papers such as the Cytonn High Yielding Solution (CHYS) which offers the client a return of 18%. For more information, please read our topical on Structured High Yield Investment Products.

The main advantages of alternative investment products include:

- Potential for High Returns – Alternative investments offer a potential of higher returns in comparison to traditional investment products. This is achievable as a result of consolidation where economies of scale are achieved through aggregation of client funds which are then invested, and professional fund management by experts with market knowledge and experience;

- Low Correlation of Returns – Alternative investment products often have their own value that is not dependent on factors that affect prices of traditional asset classes like stocks and bonds and thus they are able to provide an inflation hedge; and,

- Alternative Source of Funding for Businesses – Alternative investments have provided avenues for firms to raise capital with preferable terms and conditions to both parties.

The main disadvantages of alternative investment products include:

- Operating in a Less Regulated Environment - In comparison to traditional investment products, alternative investments have less stringent regulation to abide by which heightens the risk of investments made;

- Lengthy Process to Carry out a Transaction – The majority of alternative investment products are tailor-made to the clients’ expectations and thus this process would take time from initializing the deal, proceeding to conduct due diligence on the transaction to structuring the deal and finally the actual transaction takes place;

- Limited Availability of Information - The majority of alternative investments entail private transactions and thus there is little information on the details of deals carried out subject to the information released by the parties involved; and,

- Low Liquidity - Alternative investment products mainly target long-term investors and thus before the maturity of the investment, it is difficult to dispose of the investment unless there is already a willing buyer in the market for that specific product.

Section III: Our views, Expectation, and Conclusion

With the knowledge of the current investment products in the market, there are a few considerations to be considered before making an investment, which includes:

- Returns: The various asset classes are expected to generate various returns to their investors, which come as either interest income, capital appreciation, dividends or rental income. The choice of investment depends on the returns available and the preference of the investor towards generating a stream of income or capital appreciation in their portfolio;

- Investment Horizon: This is the length of time that an investor intends to hold an investment and it is dependent on the investor’s income needs and risk exposures;

- Tax Profile of the Investors: It is critical for investors to understand their tax status for tax planning purposes to avoid losses in returns.

- Risk: This is the uncertainty that the investment may not earn its expected rate of return. There are various risks which may affect the performance of investments which include but not limited to;

- Interest rate risk – This is the risk that a change in interest rates may affect the value of the investment. This form of risk is mainly associated with government securities where an increase in interest rates will cause a decrease in a bond’s price and vice versa when interest rates decline this will cause an increase in the bond’s price;

- Currency risk – This is the risk that a fluctuation in the price of one currency may affect the value of investments. This is especially of concern to foreign investors, who may experience a loss in value on their investments on conversion should the Kenyan Shilling depreciate relative to their foreign currency;

- Re-investment risk – This is the probability that an investor may be unable to reinvest cash flows at a rate comparable to the current investment’s rate of return. This risk is mostly associated with longer-dated investments due to the uncertainty of the economic conditions and the performance of the market;

- Liquidity risk – This is the risk that an individual or firm may be unable to pay its debt obligations when due, resulting in losses made by the investor; and,

- Credit risk - This is the risk that a loss may arise from a borrower’s failure to repay a loan or meet contractual obligations.

- Liquidity: This is how quickly an investment can be converted into cash. For investors who would prefer high liquidity, they may be inclined to invest in treasury bills and equities.

In summary, the following is the comparison of the various asset classes in relation to form of returns, volatility, liquidity and the suitability to the investors:

|

Asset class |

Returns |

Volatility |

Liquidity |

Suitability |

|

Equities |

Dividends Interest income |

High Volatility |

Moderate to high liquidity |

Short-term & long-term investors |

|

Fixed Income Securities |

Interest income |

Low volatility |

Moderate to High liquidity |

Short-term & long-term investors |

|

Mutual Funds |

Capital appreciation Interest Income Dividends |

Low volatility |

Moderate to High liquidity |

Short-term & Long-term investors |

|

Private Equity |

Dividends Capital appreciation |

Relatively stable |

Low liquidity |

Long-term investors |

|

Real Estate |

Rental income Capital appreciation |

Relatively stable |

Low to moderate liquidity |

Long-term investors |

|

Derivatives |

Capital Appreciation |

Relatively stable |

Moderate liquidity |

Medium to long-term investors |

|

Structured Products |

Capital appreciation Dividends Interest Income |

Low to moderate volatility |

Moderate liquidity |

Long-term investors |

|

Pension funds |

Capital appreciation Dividends Interest Income |

Low to moderate volatility |

Moderate liquidity |

Long-term investors |

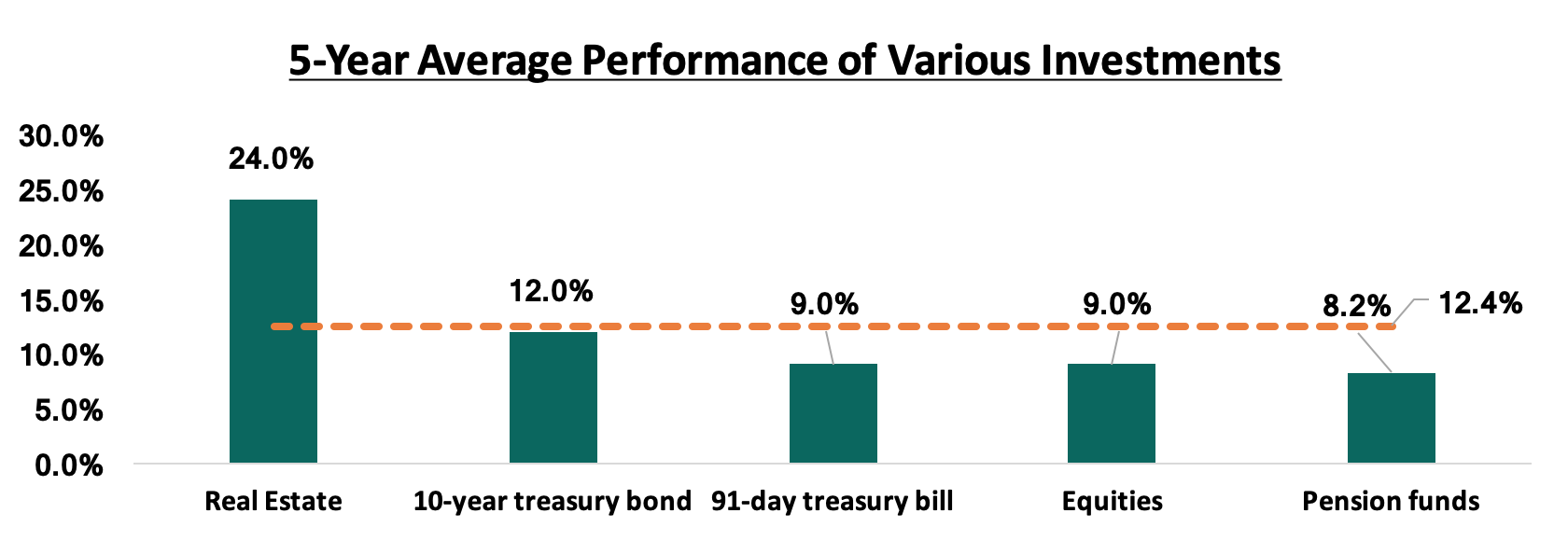

The following is a summary of the performance of the various investments:

Kenya’s diverse investment product offering echoes why the market continues to be an attractive investment destination, with a number of options that are able to suit a wide and diverse range of investors. As investors take advantage of the various investment opportunities available, we advise them to seek the advice of a registered investment advisor. We shall follow up with a note on financial planning, to help investors understand how to choose from these investment options based on their individual circumstances and need.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma