Oct 12, 2025

Following the release of the H1’2025 results by Kenyan insurance firms, the Cytonn Financial Services Research Team undertook an analysis on the financial performance of the listed insurance companies and the key factors that drove the performance of the sector. In this report, we assess the main trends in the sector, and areas that will be crucial for growth and stability going forward, seeking to give a view on which insurance firms are the most attractive and stable for investment. As a result, we shall address the following:

- Insurance Penetration in Kenya,

- Key Themes that Shaped the Insurance Sector in H1’2025,

- Interest rates

- Industry Highlights and Challenges,

- Performance of The Listed Insurance Sector in H1’2025, and,

- Conclusion & Outlook of the Insurance Sector.

Section I: Insurance Penetration in Kenya

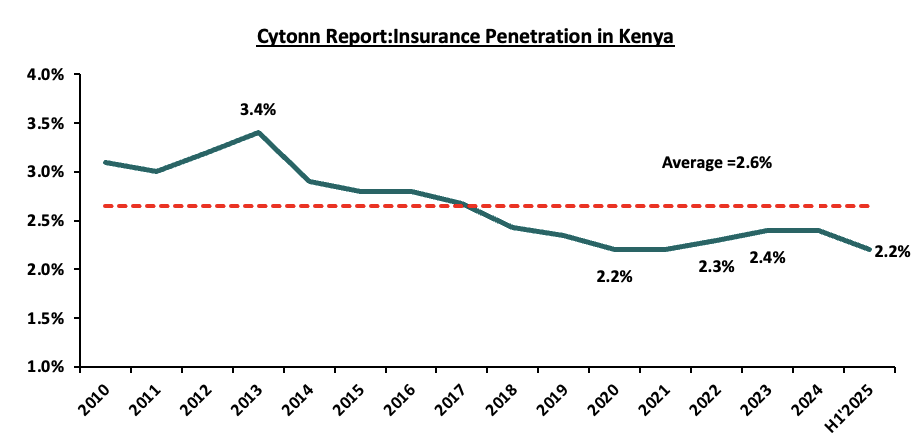

Insurance uptake in Kenya remains low compared to other key economies with the insurance penetration coming in at 2.2% as at H1’2025, according to Q2’2025 Insurance Regulatory Authority (IRA) and Central Bank of Kenya. The low penetration rate, which is below the global average of 7.4%, according to Allianz Global Insurance Report 2025, is attributable to the fact that insurance uptake is still seen as a luxury and mostly taken only when it is necessary or a regulatory requirement. Notably, insurance penetration declined by 0.2% points from 2.4% recorded in 2024, despite the mild economic recovery that saw a slight improved business environment in the country with the Stanbic Purchasing Managers Index for H1’2025 coming in at 50.5, up from 50.0 in H1’2024. The chart below shows Kenya’s insurance penetration for the last 15 years:

Source: Cytonn Research

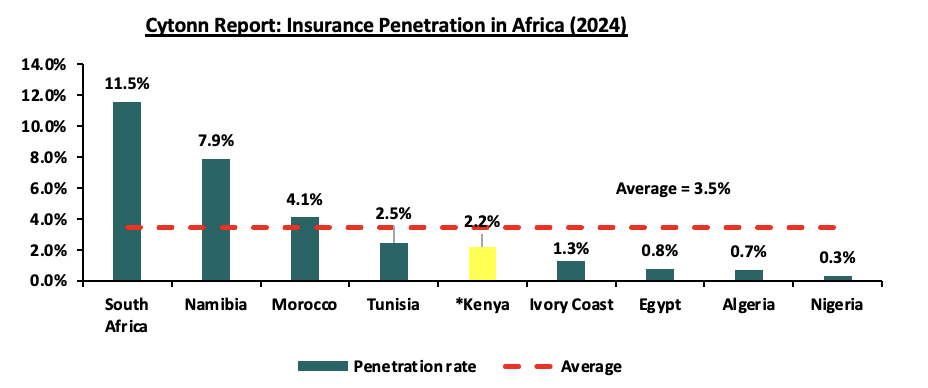

The chart below shows the insurance penetration in other economies across Africa:

*Data as of H1’2025

Source: Atlas Magazine

Insurance penetration in Africa has remained relatively low, averaging 3.5% in 2024, mainly attributable to lower disposable income in the continent and slow growth of alternative distribution channels such as mobile phones to ensure wider reach of insurance products to the masses. South Africa remains the leader in insurance penetration in the continent, owing to a mature and highly competitive market, coupled with strong institutions and a sound regulatory environment.

Section II: Key Themes that Shaped the Insurance Sector in H1’2025

In H1’2025, the country experienced a more favourable operating environment due to relatively stable inflation and stronger Shilling. Notably, the inflation rate in H1’2025 averaged 3.7%, 1.9% points lower than the 5.6% average in H1’2024, with the Kenyan Shilling having appreciated by 5.5 bps against the USD in H1’2025 to close at Kshs 129.2, from Kshs 129.3 at the beginning of the year. As such, according to the Q2’2025 Insurance Regulatory Authority Insurance industry report, the insurance sector showcased resilience recording a 13.4% growth in gross premium to Kshs 241.3 bn in H1’2025, from Kshs 212.8 bn in H1’2024. This was supported by improved economy as the overall GDP growth rate improved to 5.0% in Q2’2025, from 4.6% recorded in a similar period last year according to Q2’2025 Quarterly Gross Domestic Product Report. Insurance claims also increased by 34.6% to Kshs 67.6 bn in H1’2025, from Kshs 50.2 bn in H1’2024.

Notably, the general insurance business contributed 53.8% of the industry’s premium income in H1’2025 compared to 45.7% contribution by long term insurance business in the same period. During the period, the long-term business premiums increased by 17.7% to Kshs 110.4 bn, from Kshs 93.8 bn in H1’2024 while the general business premiums grew by 10.4% to Kshs 129.9 bn, from Kshs 117.7 bn in 2024. Additionally, motor insurance and medical insurance classes of insurance accounted for 67.6% of the gross premium income under the general insurance business, compared to 64.0% recorded in H1’2024. As for long-term insurance business, the major contributors to gross premiums were deposit administration and life assurance classes accounting for 54.8% in H1’2025, compared to the 54.6% contribution by the two classes in H1’2024.

Microinsurance is also shaping Kenya’s insurance landscape, expanding coverage to low-income and informal sector groups. Licensed underwriters are using mobile platforms, SACCOs, and cooperatives to reach underserved populations. Governed by the Insurance (Microinsurance) Regulations, 2020, the framework caps premiums at Kshs 40.0 per day, the insured amount at Kshs 500,000.0, and limits policies to 12 months. The number of licensed microinsurers stands at six with Britam Microinsurance Kenya having the highest market share of 79.4%. In H1’2025 microinsurance premiums amounted to Kshs 1.07 bn, with the general class contributing the majority share at 97.1% while the microinsurers incurred claims amounting to Kshs 304.8 mn during the same period. The total investments under microinsurance business as at end of Q2’2025 amounted to Kshs 540.6 mn with term deposits having the highest allocations of 67.0%.

Key highlights from the industry performance:

- The sector’s investments income increased by 19.3% to Kshs 1,205.1 bn in H1’2025, from Kshs 1,010.5 bn in H1’2024, mainly attributable to the 22.6% increase in the investment income in the long-term to Kshs 933.8 bn, from Kshs 761.6 bn in 2023, coupled with the 12.5% increase in investment income in the general insurance business to Kshs 189.8 bn, from Kshs 168.7 bn in H1’2024,

- Continued recovery from the ripple effects of the pandemic witnessed in 2020 that saw both individuals and businesses seek insurance uptake to cover for their activities, leading to growth in gross premiums which increased by 13.4% to Kshs 241.3 bn in H1’2025, from Kshs 212.8 bn in H1’2024,

- The insurance industry’s asset base grew by 18.4% to Kshs 1.4 tn at the end of Q2’2025, up from Kshs 1.2 tn in Q2’2024. Of this total,87.8% was invested in income-generating investments.

- Enhanced convenience and operational efficiency driven by the use of alternative distribution and premium collection channels, including Bancassurance and strengthened agency networks, and,

- Technological advancements and innovation have enabled premium payments to be made easily via mobile phones.

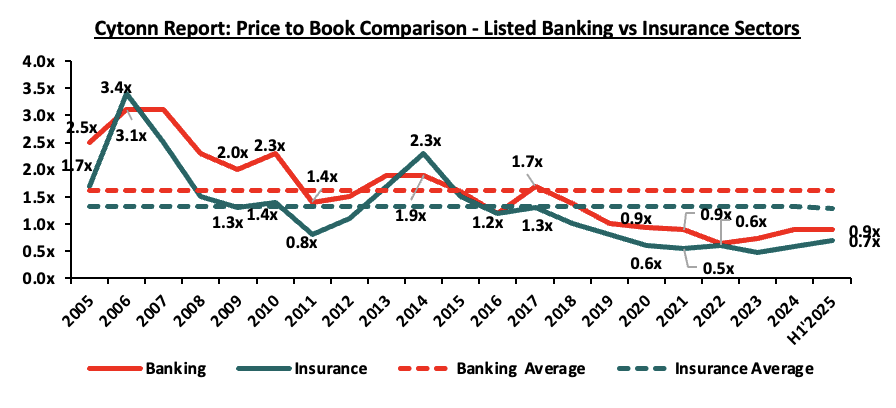

On valuations, listed insurance companies are trading at a price to book (P/Bv) of 0.7x, lower than listed banks at 0.9x, but both are lower than their 16-year historical averages of 1.3x and 1.6x, for the insurance and banking sectors respectively. These two sectors are attractive for long-term investors supported by the strong economic fundamentals. The chart below shows the price to book comparison for Listed Banking and Insurance Sectors:

\

\

Source: Cytonn Research

The key themes that have continued to drive the insurance sector include:

- Technology and Innovation

The insurance industry was slow to adopt digital solutions, but the COVID-19 pandemic in 2020 made online distribution essential. Since then, many insurers have turned to digital platforms to drive growth and expand insurance coverage nationwide. In April 2024, CIC Group announced the launch of Easy Bima, a digital motor insurance product. This solution enables customers to spread the cost of their comprehensive motor insurance premiums into equal monthly instalments over a 12-month period, offering greater flexibility and affordability. By utilizing digital platforms, it enhances accessibility to insurance, particularly for individuals who find it challenging to make lump-sum payments. Consumers often term insurance as difficult and complex to understand. This sentiment has been established through various studies carried out to establish reasons for low uptake of insurance, the latest being the 2024 Fin Access Survey. The survey found that 63.2% of the respondents do not afford premiums while 19.4% lacks awareness of the products. Additionally in February 2025, Jubilee insurance launched J-Force a digital solution aimed at improving efficiency in insurance distribution by simplifying policy administration, client interaction, and transaction handling. In addition to providing real-time business analytics, J-Force empowers intermediaries to work faster and more accurately facilitating client onboarding, lead management, policy issuance, and renewal tracking in a smooth, fully digital environment.

- Regulation

To position the sector within a globally competitive financial services landscape, the regulator has been actively implementing regulations aimed at tackling both longstanding and emerging challenges. The COVID-19 environment proved challenging especially on the regulatory front, as it was a balance between remaining prudent as an underwriter and adhering to the set regulations given the negative effects the pandemic. Regulations used for the insurance sector in Kenya include the Insurance Act Cap 487 and its accompanying schedule and regulations, Retirement Benefits Act Cap 197 and The Companies Act. In H1’2025, regulation remained a key aspect affecting the insurance sector and the key themes in the regulatory environment include;

- IFRS 17- IFRS 9, Financial Instruments was replaced with IFRS 17. The adoption of IFRS 17 has reshaped financial reporting in the insurance sector by emphasizing transparency, consistency, and market-based valuation of insurance contracts. Insurers are now experiencing more volatile earnings due to the recognition of contractual service margins and the impact of changing discount rates. Balance sheets have been restructured as liabilities and reserves are reassessed to reflect future obligations, while disclosures have become more detailed to explain performance drivers across insurance service results, investment income, and reinsurance. The transition has also increased compliance costs and reporting complexity as firms adjust systems and data frameworks.

- Risk Based Supervision - IRA has been implementing risk-based supervision through guidelines that require insurers to maintain a capital adequacy ratio of at least 200.0% of the minimum capital. The regulation requires insurers to monitor the capital adequacy and solvency margins on a quarterly basis, with the main objective being to safeguard the insurer’s ability to continue as a going concern and provide shareholders with adequate returns. We expect more mergers within the industry as smaller companies struggle to meet the minimum capital adequacy ratios. We also expect insurance companies to adopt prudential practices in managing and taking on risk and reduction of premium undercutting in the industry as insurers will now have to price risk appropriately.

- Insurance Professionals- The Insurance Professionals Act, 2025 introduced mandatory licensing, examinations, and a code of conduct for all insurance practitioners through the Insurance Institute of Kenya and the Insurance Professionals Examinations Board. It aims to enhance accountability, professionalism, and consumer confidence. Alongside the Insurance (Amendment) Act, 2023, which raised penalties for management misconduct and failure to settle claims, the reform framework emphasizes stricter oversight, ethical practice, and better protection for policyholders.

- Capital Raising and share purchase.

The move to a risk-based capital adequacy framework presented opportunities for capital raising initiatives mostly by the small players in the sector to shore up their capital and meet compliance measures. With the new capital adequacy assessment framework, capital is likely to be critical to ensuring stability and solvency of the sector to ensure the businesses are a going concern. According to the updated Insurance act 2022,General insurers are required to have at least Kshs 600 mn while life insurance providers are required to have Kshs 400 mn in minimum capital and Kshs 50.0 mn for microinsurers. In May 2022, Sanlam Limited, a South African financial services group listed on the Johannesburg Stock Exchange, announced that it had entered into a definitive Joint Venture agreement for a term of 10 years with Allianz SE, with the aim to leverage on the two entities footprints in Africa and create a leading Pan-African financial services group, with an estimated equity value of Kshs 243.7 bn. Key to note, Sanlam Limited, indirectly owns 100.0% in Hubris Holdings Limited, which is the majority shareholder in Sanlam Kenya Plc, a listed insurance and financial services entity on the Nairobi Stock Exchange. The initial shareholding split of the Joint Venture was announced to be 60:40, Sanlam Limited to Allianz respectively, with the effective date of the proposed transaction being within 12-15 months of the announcement, subject to relevant approvals. However, given the length of the Agreement we expect that the Joint Venture will provide for Sanlam Kenya Plc, Allianz General Insurance Kenya and Jubilee General Insurance (which Allianz owns the majority stake in – 66.0%), to combine operations to grow their market share, asset base and bottom lines.

Additionally, insurance companies have increasingly turned to capital raising initiatives such as rights issues to strengthen their financial positions. A recent example is Sanlam Kenya, which undertook a rights issue offering 500.0 mn new shares at an offer price of Kshs 5.00 per share. The capital raised is to direct towards key strategic areas, primarily aimed at reducing the Group’s long-term debt exposure and supporting its return to profitability.

Section III: Interest rates

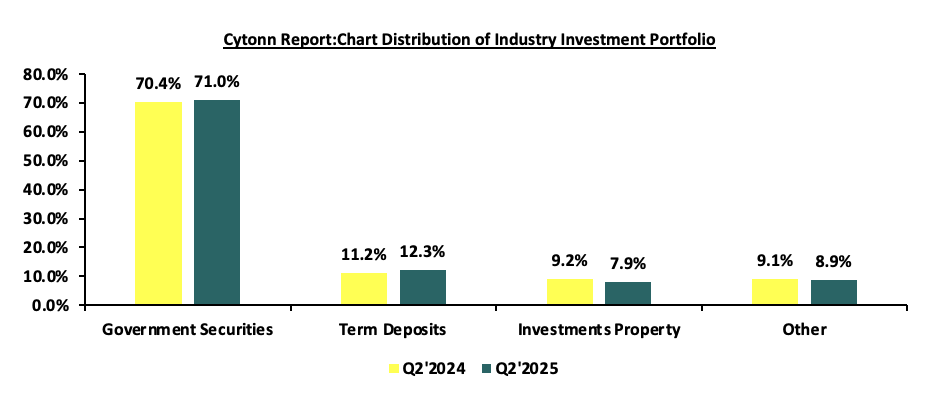

The interest rate environment has been declining in H1’2025.With Central Bank rates declining in 2025, insurers capitalized on longer tenor higher-yielding treasury bills and bonds, with 364-day, 182-day, and 91-day papers decreased by 6.2% points, 7.5% points, and 7.4% points to 10.4%, 9.1%, and 8.8% in H1’2025, respectively, from 16.7%, 16.6%, and 16.2%, respectively, in H1’2024. According to the IRA report, Investments in income-generating assets registered growth, increasing by 19.3% to Kshs 1.2 tn in Q2’2025, up from Kshs 1.0 tn recorded in Q2’2024. The table below shows insurance industry investments:

|

Cytonn Report: Insurance Industry Investments |

||||

|

Investments |

Q2'2025 |

Q2'2024 |

y/y Change |

Q2'2025 % Distribution |

|

Government Securities |

855.6 |

711.5 |

20.3% |

71.0% |

|

Term Deposits |

147.8 |

113.6 |

30.1% |

12.3% |

|

Investments Property |

94.7 |

93.0 |

1.8% |

7.9% |

|

Investment in Related Companies |

30.6 |

28.4 |

7.9% |

2.5% |

|

Ordinary Shares Quoted |

30.6 |

22.2 |

37.5% |

2.5% |

|

Loans & Mortgages |

10.4 |

7.9 |

31.6% |

0.9% |

|

Other Securities |

35.4 |

33.9 |

4.6% |

2.9% |

|

Total |

1,205.1 |

1,010.5 |

19.3% |

100.0% |

|

* Figures in Kshs Bns |

||||

Source: IRA

Government securities grew by 20.3% to Kshs 855.6 bn in Q2’2025, up from Kshs 711.5 bn in Q2’2025. Insurers increased their portfolios to in government securities despite the declining yields. The share of government securities rose 0.6% points year-on-year to 71.0% in Q2’2025 from 70.4% in Q2’2024 attributable to low risk profile from government securities. Investments in term deposits increased by 30.1% points to Kshs 147.8 bn in Q2’2025, up from 113.6 bn in Q2’2024 with the allocation increasing by 1.1% to 12.3%, from 11.2% in Q2’2024.Investment property increased by 1.8% to Kshs 94.7 bn in Q2’2025 ,up from Kshs 93.0 bn in Q2’2024 ,while the allocation of the portfolio declined by 1.3% points to 7.9%, from 9.2% in Q2’2024. The chart below shows comparison of investments portfolio allocations for the industry:

Source: IRA

Section IV: Industry Highlights and Challenges

The insurance sector has grown steadily over the past decade, and this momentum is expected to continue at a moderate pace. The outlook is supported by stronger economic outlook and a corresponding increase in insurance premiums, factors which are likely to enhance the industry's capacity to maintain profitability.

On the regulatory front, the rejected Finance Bill 2024 included provisions that sought to expand taxes on insurance premiums and extend VAT to certain insurance services. These included a new 2.5% tax on the value of motor vehicles, payable when issuing insurance cover and limiting VAT exemptions to insurance and reinsurance premiums only, subjecting other related services to the standard VAT rate of 16.0%. These measures were aimed at increasing government revenue but were met with opposition from industry stakeholders, including the Association of Kenya Insurers (AKI) due to concerns over increased insurance costs. The rejection of the Finance Bill has provided a temporary reprieve for the insurance sector, though discussions on balancing fiscal policy and market growth continue to shape the regulatory landscape.

Industry Challenges:

- Insolvency: A major challenge facing the insurance industry is the financial instability and insolvency of key players, as evidenced by cases in 2024 like Resolution Insurance and United Insurance Company. These companies have been placed under statutory management like Xplico Insurance Company and provisional liquidation by the Insurance Regulatory Authority (IRA) and through court orders. The issues arise from extended financial struggles, internal boardroom disputes, and declining market share, especially in unprofitable areas such as Public Service Vehicle (PSV) insurance. The collapse of these insurers undermines customer trust, destabilizes the industry, and compels policyholders to find alternative coverage. To regain stability and rebuild consumer confidence, the sector must tackle issues related to governance, risk management, and liquidity,

- High Market competition: Despite low insurance penetration in the country, the sector is served by 57 insurance companies offering the same products. The sector is increasingly facing competition from banking institutions and telecommunications companies, which pose a growing threat to its market share. New players like Safaricom, which was recently licensed by the Insurance Regulatory Authority (IRA) as an insurance broker, along with Equity Group’s ongoing expansion into the insurance space through the launch of Equity Life Assurance, are intensifying competition for traditional insurers. Some insurers have resorted to shady tactics in the fight for market dominance, such as premium undercutting, which involves offering clients implausibly low premiums in order to gain competitive advantage and protect their market share. This is a significant factor in the industry's underwriting losses. Plans to hire a consultant to review industry pricing in March 2021 were retaliated against by the regulator, but the plans are still in the works. However, this is against a background of weak insurance uptake, which could be made worse by higher premium prices. Industry participants have debated pricing,

- Insurance fraud: Insurance Fraud is an intentional deceit performed by an applicant or policyholder for financial advantage. In recent years, there has been an upsurge in fraudulent claims, particularly in medical and motor insurance, with estimates indicating that one in every five medical claims are fraudulent. This is mainly through exaggerating medical costs and hospitals by making patients undergo unnecessary tests. Fraudsters also collude with hospitals to file false claims, including fabricated surgeries and treatments, while some healthcare providers inflate charges for insured patients. To curb these challenges, the industry has adopted implementing blockchain technology and artificial intelligence to detect and prevent fraud. In Q2’2025, the number of fraud cases reported to the Insurance Fraud Investigation Unit (IFIU) increased by 11.1% to 50 cases, from 45 cases reported in Q2’2024,

- Regulation compliance: Due to updates on the laws governing insurance sector, such as capital requirements, smaller insurance businesses and new market entrants have found it challenging to operate without raising capital or combining to expand their capital base. Additionally, the implementation of IFRS 17, is expensive since accounting and actuarial systems need to be updated and realigned. There is lack of adequate skilled professionals due to the complexity of IFRS 17 which requires a solid grasp of both accounting and actuarial concepts. This skills gap has resulted in difficulties in fully understanding and applying the requirements of the framework, and,

- Declining consumer confidence in the insurance industry: In Q2’2025, IRA received 423 complaints from policyholders and beneficiaries lodged against insurers. The general insurance accounting for majority of the complaints at 78.7%, while long-term insurers recording 21.3%. The complaints range from insurance companies failing to settle claims and constant haggling over terms of insurance. Such experiences have led to scepticism toward insurers thus leading to declined consumer confidence.

Section V: Performance of the Listed Insurance Sector in H1’2025

The table below highlights the performance of the listed insurance sector, showing the performance using several metrics, and the key take-outs of the performance.

|

Listed Insurance Companies H1’2025 Earnings and Growth Metrics |

|||||||||

|

Insurance |

Core EPS Growth |

Insurance revenue growth |

Claims growth |

Loss Ratio |

Expense Ratio |

Combined Ratio |

ROaE |

ROaA |

|

|

Sanlam |

(94.7%) |

6.1% |

5.3% |

89.1% |

60.0% |

149.1% |

1.2% |

0.1% |

|

|

Liberty |

(29.8%) |

(37.4%) |

(20.0%) |

73.6% |

80.0% |

153.6% |

4.4% |

0.9% |

|

|

Jubilee Insurance |

20.4% |

32.6% |

36.6% |

92.2% |

108.4% |

200.7% |

5.5% |

1.4% |

|

|

Britam |

(15.0%) |

10.6% |

11.4% |

76.8% |

96.4% |

173.2% |

6.0% |

1.2% |

|

|

CIC |

(23.3%) |

8.4% |

23.4% |

92.2% |

117.2% |

209.4% |

6.0% |

1.3% |

|

|

*H1'2025 Weighted Average |

(6.6%) |

13.7% |

19.8% |

85.2% |

102.5% |

187.7% |

5.6% |

1.3% |

|

|

**H1'2024 Weighted Average |

39.6% |

51.7% |

(18.2%) |

81.1% |

68.2% |

149.4% |

7.3% |

1.6% |

|

|

*Market cap weighted as at 09/10/2025 |

|

||||||||

|

**Market cap weighted as at 18/10/2024 |

|

||||||||

The key take-outs from the above table include;

- Core EPS growth recorded a weighted decline of 6.6%, lower compared to the weighted growth of 39.6%, in H1’2024. The decline in earnings was attributable to decreased premiums during the period following declined yields from government papers during the period,

- Insurance revenue grew at a slower pace of 13.7% in H1’2025, compared to a growth of 51.7% in H1’2024, while claims also grew at a rate of 19.8% in H1’2025, a reversal from the 18.2% decline recorded in H1’2024 on a weighted average basis,

- The loss ratio across the sector increased to 85.1% in H1’2025 from 81.1% in H1’2024,

- The expense ratio increased to 102.5% in H1’2025, from 68.2% in H1’2024, owing to increase in operating expenses, a sign of decreased efficiency,

- The insurance core business still remains unprofitable, with a combined ratio of 187.8% as at H1’2025, higher than the 149.4% in H1’2024, and higher than the desired ratio of 100.0%, and,

- On average, the insurance sector delivered a Return on Average Equity (ROaE) of 5.6%, a decrease from a weighted Return on Average Equity of 7.6% in H1’2024.

Based on the Cytonn H1’2025 Insurance Report, we ranked insurance firms from a franchise value and from a future growth opportunity perspective with the former getting a weight of 40.0% and the latter a weight of 60.0%.

For the franchise value ranking, we included the earnings and growth metrics as well as the operating metrics shown in the table below in order to carry out a comprehensive review:

|

Listed Insurance Companies H1’2025 Franchise Value Score |

||||||

|

Insurance Co. |

Loss Ratio |

Expense Ratio |

Combined Ratio |

Tangible Common Ratio |

Franchise Value Score |

Ranking |

|

Sanlam Kenya |

89.1% |

60.0% |

149.1% |

8.3% |

15 |

1 |

|

Britam Holdings |

76.8% |

96.4% |

173.2% |

12.9% |

15 |

1 |

|

Jubilee Holdings |

92.2% |

108.4% |

200.7% |

21.6% |

18 |

3 |

|

Liberty Holdings |

73.6% |

80.0% |

153.6% |

19.2% |

19 |

4 |

|

CIC Group |

92.2% |

117.2% |

209.4% |

15.6% |

23 |

5 |

|

* H1’2025 Weighted Average |

85.2% |

102.5% |

187.7% |

17.0% |

|

|

The Intrinsic Valuation is computed through a combination of valuation techniques, with a weighting of 40.0% on Discounted Cash-flow Methods, 35.0% on Residual Income and 25.0% on Relative Valuation. The overall H1’2025 ranking is as shown in the table below:

|

Listed Insurance Companies H1’2025 Comprehensive Ranking |

|||||

|

Bank |

Franchise Value Score |

Intrinsic Value Score |

Weighted Score |

H1’2025 Ranking |

H1’2024 Ranking |

|

Sanlam Kenya |

1 |

2 |

1.6 |

1 |

4 |

|

CIC Group |

5 |

3 |

3.8 |

2 |

1 |

|

Britam Holdings |

1 |

4 |

2.8 |

3 |

5 |

|

Liberty Holdings |

4 |

5 |

4.6 |

4 |

3 |

|

Jubilee Holdings |

3 |

1 |

1.8 |

5 |

2 |

Major Changes from the H1’2025 Ranking are;

- Sanlam Kenya improved to position 1 in H1’2025 driven by strong intrinsic and franchise score, attributable to the low combined ratio of 149.1%,

- CIC Group declined to position 2 in H1’2025 driven by declined franchise score, attributable to the increase in the claims growth to 23.4%, from a 6.9% decline recorded in H1’2025.

- Liberty Holdings declined to position 4 in H1’2025 mainly due to weakened intrinsic score in H1’2025,

- Britam Holdings improved to position 3 in H1’2025, mainly due to increase in franchise scores in H1’2025, driven by the decrease in claims growth to 11.4%, from the 14.6% growth recorded in H1’2024, and,

Section VI: Conclusion & Outlook of the Insurance Sector

Kenya’s improving economic conditions have created a more positive outlook for the insurance sector. With easing inflation and a stabilizing shilling, households are likely to have more disposable income, supporting higher insurance uptake. Although challenges persist, the industry continues to gain from the digital transformation and innovation that accelerated during the pandemic. Ongoing regulatory reforms and a stronger focus on customer needs remain central priorities. The more favourable economic environment offers insurers a solid foundation for growth, with opportunities to refine product offerings, strengthen customer relationships, and develop policies that reflect the evolving financial needs and capabilities of consumers.

The insurance sector should build on the following strategies to sustain growth and capitalize on the economic upturn:

- Partnerships and alternative distribution channels - We expect underwriters to keep forming strategic partnerships and expanding their distribution channels in the future. This can be accomplished by collaborating with other financial service providers such as fund managers who have ventured into offering insurance-related products alongside existing bancassurance arrangements with banks. Additionally, insurers can leverage the penetration of banking products to increase awareness and uptake of their own offerings. For instance, in July 2024, NCBA Group announced the completion of 100% acquisition of AIG Kenya Insurance Company (AIG Kenya). This move allows NCBA to leverage its physical and digital platforms to boost insurance penetration in Kenya and the wider East African region. This acquisition aligns with the broader trend of partnerships and alternative distribution channels, as NCBA’s collaboration with AIG Kenya demonstrates how banks and insurance providers can work together to broaden access to insurance products. According to AKI released state of the Bancassurance Market in Kenya 2024 report, Bancassurance distribution channel market share grew to 10.0% with the channels gross written premium growing to Kshs 35.0 bn in 2023,

- Regulations - To ensure the sector's solvency and sustainability, we anticipate more regulation from the regulatory body and other international stakeholders. The regulator's quest for the targeted capital adequacy levels will almost certainly result in further consolidations as insurers struggle to achieve the capital requirements, particularly for small firms. Furthermore, regulators, governments, and policymakers are working harder to make Environmental, Social, and Governance (ESG) standards a requirement in the insurance industry,

- Diversification - As insurers look to expand their portfolios and mitigate risks, entering new markets can provide growth opportunities and help spread exposure across multiple economies. This strategy allows companies to tap into underpenetrated regions, improving overall revenue streams and reducing dependence on local markets. By entering emerging and underserved markets, insurers can gain access to new customer bases, diversify their product offerings, and strengthen their positions across Africa and beyond. For instance, in June 2025, Britam announced successful entry into the Ugandan market through new life insurance operations, coupled with the rollout of microinsurance products targeting underserved markets. Additionally, the Insurance Regulatory Authority (IRA) should review the current Kshs 50.0 mn minimum capital requirement for microinsurers under the 2020 regulations that limits existing insurers who wish to expand into microinsurance, as they are required to set up separate licensed entities to do so. Allowing insurers to offer microinsurance under their existing licenses, would ease regulatory barriers, promote innovation, and accelerate insurance inclusion across underserved markets,

- Technology and Innovation: To aid portfolio expansion and growth, insurers must harness the digital insurance solutions at their disposal in order to improve internal efficiency and accelerate time to market. As such, we anticipate cooperation between insurers and InsurTechs. For instance, in February 2024, Britam launched BetaLab a new insurance innovation hub, as it aims to nurture budding InsurTech and fintech start-ups, and fast track product development in the industry. The lab’s mission is to incubate, innovate, and accelerate start-ups, nurturing and empowering innovation among internal staff, while also exploring innovation opportunities with insuretechs and fintechs. Additionally, insurers should embrace use of artificial intelligence to improve efficiency by integrating Artificial Intelligence (AI) into underwriting, automating claims processes, and using chatbots for customer support, thereby streamlining overall operations. For instance, in April 2024, M-tiba announce the successful integration of AI into their claims processing system, leading to significant reductions in claims approval process to just hours. Additionally, use of AI enhances their efficiency and fraud management resulting in low administrative and healthcare costs for health insurers,

- Insurance awareness campaigns – Low insurance penetration is significantly impacted by the persistent information gap about insurance products and their significance. Insurance is still largely assumed to be regulatory compliance rather than a necessity. The regulators, insurers, and other stakeholders should enhance insurance awareness campaigns to increase understanding of insurance products. According to Finaccess survey 2024, the second largest contributor to low insurance uptake at 19.4% is a lack of awareness of the various insurance products and their benefits. As such, there is a lot of headroom for insurers to educate, repackage, and tailor their products to different potential clients, and,

- Investment diversification – To enhance profitability and minimize losses, underwriters should prioritize diversifying their investments through avenues like pension schemes, unit trusts, fund management, and investment advisory services. The combined ratios were 108.3% and 102.1% in H1’2025 for general insurance businesses and Microinsurance business respectively, pointing toward losses in insurers' core operations, as rising underwriting costs and claims have outpaced insurance revenue growth. In addition, we anticipate insurers will continue to investigate non-traditional asset types such as infrastructure.

For more information, please read our H'12024 Listed Insurance Sector full report

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma