Apr 28, 2019

Following the announcement of the formation of the Kenya Mortgage Refinancing Company (KMRC) by the National Treasury Cabinet Secretary, Hon. Henry Rotich in April 2018, we released the Kenya Mortgage Refinancing Company Note, where we introduced the facility and its main functions, highlighted the successes of other mortgage refinance companies in Africa, and emphasized on the conditions necessary for the KMRC to thrive. To recapture the Note, the KMRC is an initiative of the National Treasury and the World Bank, whose main objective is to grow Kenya’s mortgage market by providing long-term funding to primary mortgage lenders. The initiative aims to support the affordable housing agenda by increasing the availability and affordability of housing finance, thus boosting home ownership.

Primarily, a mature mortgage market is made up of:

- Institutions that originate loans (primary mortgage market/lenders) such as banks and mortgage banking institutions,

- The markets in which they are transferred (secondary mortgage market), such as mortgage refinancing companies. The secondary markets’ main function is to get money to lenders in the primary market so they can loan it to consumers, thus facilitating the flow of funds for real estate financing, and,

- Investors, who are made up of institutional investors such as pension funds, insurance firms, and investment funds. They purchase the mortgage-backed securities, thus creating capital needed to make mortgage loans.

In February this year, Central Bank of Kenya (CBK) published draft regulations intended to provide a clear framework for licensing, capital adequacy, liquidity management, corporate governance, risk management and reporting requirements of mortgage refinance companies. Once approved, the regulations will guide the launch and beginning of operations of the KMRC. The MRC will complement other measures that the government has already undertaken to enable home ownership, such as;

- Exemption of first-time homebuyers from paying stamp duty tax,

- A 15.0% tax relief for first-time buyers up to a maximum of Kshs 108,000 p.a., and,

- Establishment of the National Housing Development Fund to manage funds set aside for the provision of social housing.

In this topical we will focus on Mortgage Refinancing Companies, reintroduce what they are, why they are needed, how they operate, what benefits are expected, finalizing with a case study review of Tanzania, and key take-outs for KMRC. As such, we shall cover the following:

- Introduction to Mortgage Refinance Companies

- The Need for Housing Finance in Kenya

- Formation & Operationalization of Mortgage Refinance Companies

- Expected Benefits & Challenges of MRCs

- Case Study: Tanzania MRC

- Lessons for Kenya MRC from Tanzania MRC

- Introduction to Mortgage Refinance Companies

A Mortgage Refinance Company (MRC) is a non-bank financial institution, incorporated as a limited liability company to provide affordable long-term funding and capital market access to primary mortgage lenders such as banks and financial co-operatives. The facility creates liquidity for primary mortgage lenders making it possible for mortgage originators to offer long-term mortgages, at relatively low interest rates and better terms and conditions. Acting as an intermediary between the primary mortgage lenders and the capital markets, the facility packages loan products into securities, which are collateralized by the underlying mortgage assets. This ensures a continuous flow of long-term financing to mortgage lenders and ultimately to borrowers, stimulating the real estate industry and the financial markets in general.

As highlighted in our previous topical on Affordable Housing in Kenya, one of the main limitations to home ownership in Kenya is limited access to debt funding for home purchases due to (i) relatively low incomes that cannot service a mortgage, (ii) high property prices, (iii) high interest rates and deposit requirements, which lock out many borrowers, and (iv) lack of capital markets funding towards real estate purchases for end-buyers. The MRC will help to alleviate the housing shortage by supporting the activities of mortgage lenders, enabling them to lower the cost of mortgage rates as well as extending their maturity. In addition, the provision of long-term financing to mortgage lenders irrespective of their size is likely to lead to increased competition amongst the lenders resulting in a higher bargaining power for borrowers, and as a result the Primary Mortgage Lenders (PMLs) are likely to charge affordable rates. This means more people will qualify for mortgage finance, boosting home-ownership.

- The Need for Housing Finance in Kenya

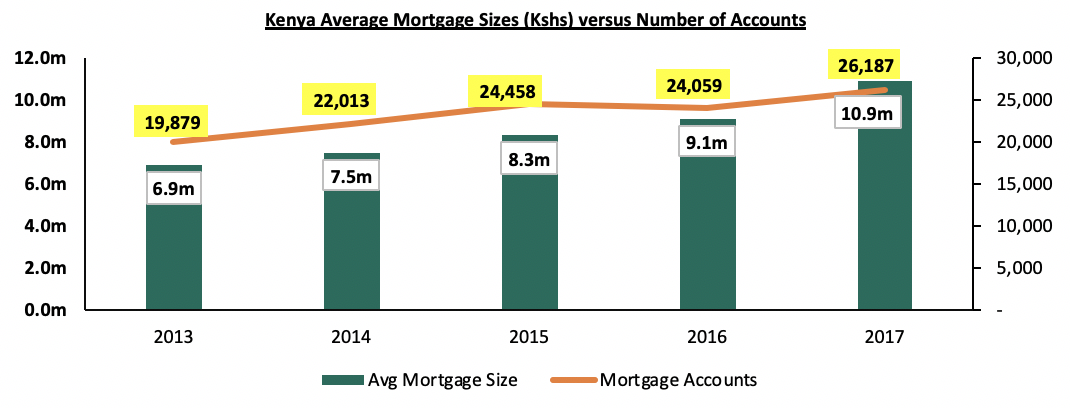

Affordability is a major constraint to the growth of the housing and mortgage markets, and a key challenge to accessing decent housing in Kenya. According to the 2015/16 Kenya Integrated Household Budget Survey (KIHBS), only 26.1% of Kenyans living in urban areas own the homes they live in, with the main factor causing this being the unaffordability of housing units in the market. Those who own homes rely mainly on savings and other sources of financing including mortgage loans, commercial bank loans, local investment groups commonly referred to as chamas, and Savings & Credit Co-operative Societies (SACCOs). Out of an adult population of about 23 mn, there were only 26,187 mortgage loans as at December 2017, according to the CBK Bank Sector Annual Report 2017. While the number of mortgage loans has been growing by an annual CAGR of 5.7% since 2013, the average mortgage size in Kenya has been growing at a higher CAGR of 9.6%, from Kshs 6.9 mn in 2013 to Kshs 10.9 mn in 2017, as shown below:

Mortgage Accounts 5-Year CAGR – 5.7%

Average Mortgage Size 5-Year CAGR – 9.6%

Source: Central Bank of Kenya (CBK)

According to Kenya National Bureau of Statistics (KNBS), approximately 74.5% of the formal working population in Kenya earns Kshs 50,000, and below, per month. With the average mortgage size in Kenya at Kshs 10.9 mn, interest rates at 13.6% and an average tenor of 12-years, therefore, an average Kenyan household earning Kshs 100,000 per month (assuming it has two persons each earning Kshs 50,000) is required monthly repayments of Kshs 153,905, which is unaffordable to this income class. However, using 40% of their gross income on monthly mortgage payments under similar market conditions, the household can afford a Kshs 2.8 mn home.

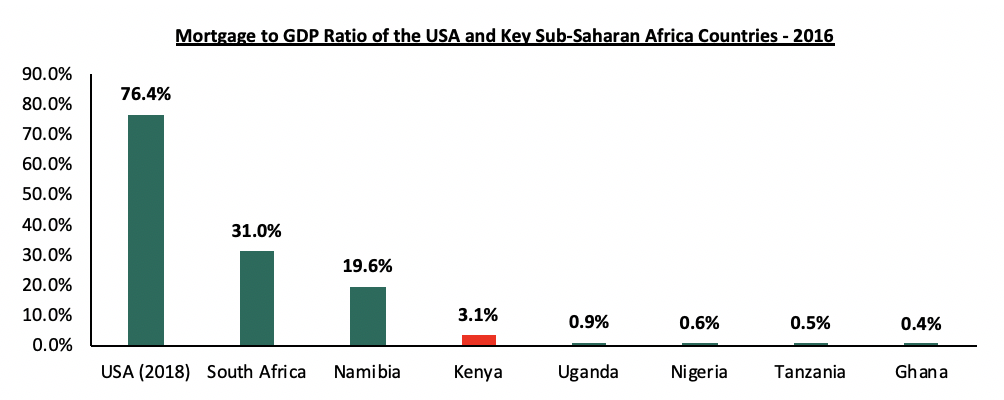

As a result, the Kenyan mortgage market still lags behind, with a mortgage to GDP ratio of 3.1% in 2016, significantly lower than more mature markets like South Africa, and the United States of America as shown below according to World Bank:

Source: World Bank

The Banking Sector

In Kenya, banks are the main providers of mortgage financing. According to Bank Supervision Annual Report 2017, 77.5% of all mortgage lending was originated by 6 banks, out of a total of 44 banks in the country, showing the reluctance of financial institutions to expand their mortgage portfolios. The main barriers to mortgage issuance include;

- Asset-liability mismatch by tenor due to the relatively long-term nature of mortgage loans and short-term nature of bank deposits,

- Limited access to capital markets funding for mortgages thus low supply of long- term capital,

- A complex legal and regulatory framework as well as collateral requirements making mortgages exceedingly expensive,

- Insufficient credit risk information, particularly on the informal sector, despite the sector making up a significant 83.4% of the total employment, according to KNBS Leading Economic Indicators 2018, and,

- An inefficient land and property registration process, which affects mortgage credibility for home-buyers.

To help bridge the funding gap in the housing finance market, there is need for better systems encompassing alternative sources of long-term financing, improved land and property registration, an expansive credit bureau coverage and an efficient legal system.

Mortgage Refinancing Companies address the liquidity issue, by (i) using the capital markets to raise large amounts of funds to support the lending activities of PMLs in a sustainable manner, and (ii) increased liquidity also helps to reduce risk premiums on mortgages for borrowers.

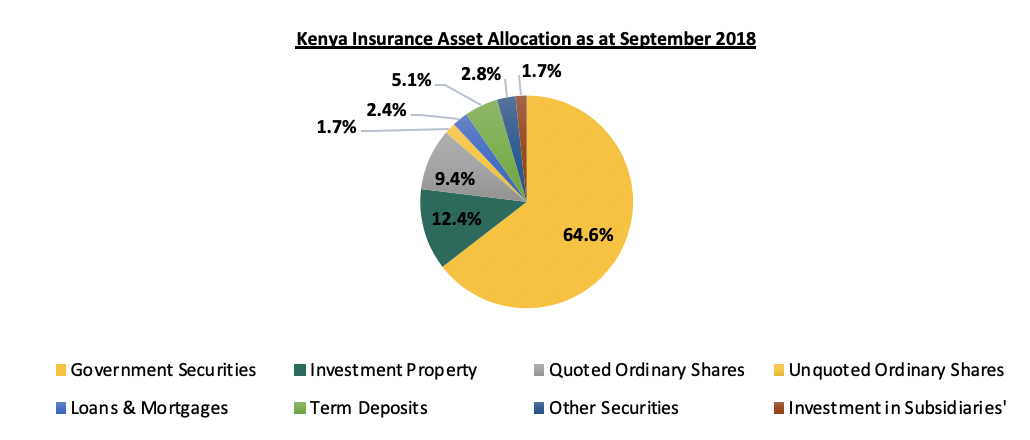

Some of the capital market products that could be considered include Housing Bonds, Asset-Backed Securities, and Real Estate Investment Trusts (REITS), targeting both retail and institutional investors. Institutions such as pension funds and insurance firms offer a viable market for these securities, especially given their rapidly growing pool of long-term funds. In Nigeria, for instance, pension funds account for 70.0% of the total subscriptions for mortgage-backed securities in 2018. In Kenya, data from the Retirement Benefits Authority (RBA) showed that the retirement benefits assets under management grew by 8.0% from Kshs. 1,080.1 billion in December 2017 to Kshs. 1,166.6 billion in June 2018. While the Retirement Benefits Authority (RBA) allows up to 30.0% of pension scheme’s assets to be invested in real estate, the current allocation stands at 19.8%, thus, there is still room for more real estate-based investments.

Insurance companies are also potential investors, holding 2.4% of their portfolios in loans and mortgages as at September 2018. Below is the allocation of the long-term insurance business investments as at September 2018:

Source: Insurance Regulatory Authority

Increased allocation of pension and insurance funds to alternative assets will not only diversify their pension funds’ portfolios and generate stable returns, but also provide the much-needed home financing.

- Formation & Operationalization of Mortgage Refinance Companies

Having looked at what MRCs are, and why we need them, in this section we will look at how MRCs are formed, operated and governed.

In brief, the MRC operates in four key steps, as shown below:

- Borrowers cede their property to a primary mortgage lender (PML) as security for a long-term mortgage loan,

- The MRC will lend its funds to PMLs with the mortgages as collateral,

- The MRC provides a bond to private institutions and investors, with the mortgages as collateral. Institutions with medium to long-term liabilities buy the bonds at a margin above the usual government securities,

- The MRC obtains the minimum core capital to enable its launch. KMRC is expected to obtain at least Kshs 1.0 bn as the minimum core capital, from the seed investors such as World Bank, the national treasury and commercial banks and SACCOs each pledging to contribute Kshs. 16.0 bn, Kshs. 1.5 bn and Kshs. 200 mn, respectively to facilitate its launch.

According to the World Bank, mortgage-refinancing companies operate under four key features;

- Taking Loans as Security – The MRC facility takes the underlying mortgage portfolios from the PML as security. This is done by either (i) extending wholesale loans to the mortgage lenders collateralized by the lenders’ mortgage portfolios, or (ii) directly buying mortgage portfolios “with recourse” from the PML. This means that the PML is bound to replace any loans, which go into default with performing credits.

MRC’s have the following lending requirements:

- The refinanced PML, must meet safety and soundness criteria to be eligible to the facility, and are subject to concentration limits, and,

- Good quality of underlying assets based on mortgage rank, Loan-to-Value ratio, credit scores, residential purposes etc.

MRC’s must be protected against a fall in the value of the security/collateral due to market fluctuations or if the replacement of defaulting loans in the cover pool does not happen continuously. This is usually addressed by over-collateralisation levels of up to 120% of refinance loans by underlying mortgages.

- Issuance of Bonds - The mortgage refinancing company issues a bond to the bond market targeting private institutions and investors who buy bonds at a margin above the usual government securities. Given the low risk nature of MRCs and their specialization in assessing the credit risk of the mortgage portfolio, their bonds need not be collateralized, however, mostly MRC use the mortgages portfolio as collateral on its bond issuance.

- Balance Sheet Management – This involves the way assets (mortgages) and liabilities (bonds) are matched. Generally, in emerging markets, the duration of the bonds is shorter than the mortgages they refinance resulting in balance sheet mismatches for the lenders or the MRC, and a need to manage the mismatches and the interest rate risk. The popular balance sheet management approach is for the MRC to turnover its debt by extending medium term refinance loans. In this case, the PMLs would typically reset the interest rates on their mortgages in line with the new funding rate following each change. This means PMLs do not incur interest risks in this They would only face a minimal liquidity risk in the case of the MRC being unable to refinance the loans if it was unable to roll over its debt. For example, in Malaysia, the rate resetting on the mortgage loans is disconnected from the refinancing, which creates at the minimum a basis risk for the lenders, but the gap between bonds – generally with a bullet repayment profile – and mortgage loans – amortizable on long periods- can stay open. This approach is however viable in mature markets where hedging instruments are available. In emerging markets such as Kenya, the two possible solutions are to either (i) keep the mismatch at the PML level, or (ii) transfer it onto the MRC’s balance sheet.

- Pricing - The intermediation role carries a price which varies from one country to another, depending on; i) the size of the balance sheet, ii) the risks transferred to the MRC, and iii) its corporate structure. Facilities that manage large assets and do not incur financial risks do not charge fees on the loans, so they transfer funds to the banks at the same rate that the bonds are issued at, such as CRH France. The only profit it makes is from the investment income derived from its capital, to which users must subscribe. Younger facilities without large-scale benefits charge up to 1.0% over their cost of fund. The Tanzanian Mortgage Refinance Company currently charges 0.5%-0.75% above the government risk free rate government bonds dependent on tenure ranging from 5 – 25 years. KMRC falling under younger facilities is likely to charge a fee of approximately 1.0% above the minimum of the risk-free rate for a 20-year bond, which currently stands at 12.8%, or 13.1% for a 25-year bond, thus is likely to trade at a yield between 13.8% to 14.1%, this compared to the current mortgage price of about 13.6%, which indicates that KMRC is likely to (i) improve accessibility of mortgages by increasing the amounts available to lend and (ii) also increase the tenors from the current 12 years to say 20 years, therefore reducing the monthly payment; KMRC in its current proposal may not improve the price / cost of mortgages, unless it’s able to get Development Finance Institutions to offer below market price debt financing.

In summary, MRC operates under the above four steps with an aim to fund primary mortgage lenders (PML) and provide relatively low interest rates and long tenure to mortgage borrowers at minimum possible risks, translating to increased mortgage uptake, thus addressing the key challenge to accessing decent housing in Kenya.

Governance, Monitoring & Evaluation

The governance of the MRC is structured in the following two ways;

- Cooperative Approach – This involves joint ownership between the government and the private sector and given the extensive government involvement in the creation of MRC, and the initial start-up risk, the main equity holder in the initial phase of an MRC is often the government owned institution,

- Government Support – The government does not participate as a shareholder, however, takes a lead role in the creation of the MRC. The objectives of the government involve improving affordability through lowering of mortgage interest rates translating to increase in the level of home-ownership and implementing of the social agenda for housing. Therefore, generally government provides support at least during a ramp-up phase of MRCs independently, by holding a stake in their capital and guaranteeing the bond issuance of the MRC.

The KMRC is established under the Companies Act, licensed by the CBK to conduct mortgage refinance business according to CBK (Mortgage Refinance Companies) Regulations 2019, which are intended to provide a clear framework for licensing, capital adequacy, liquidity management, corporate governance, risk management as well as reporting requirements of MRCs. The draft regulations for MRCs are almost similar to those of commercial banks. According to the draft, which was subjected to public comments:

- Minimum core capital of MRCs will be at least Kshs 1.0 bn, which is the same level as that of commercial banks and will need to be availed before the launch,

- The MRCs will be required to have a master servicing and refinancing agreement governing the lending operations between the mortgage refinance company and the participating primary mortgage lenders, and,

- CBK proposes that no MRC shall grant direct finance to any primary mortgage lender of amounts exceeding 25.0% of core capital.

Generally, KMRC will be subject to regulation and supervision of the Central Bank of Kenya (CBK), with Capital Markets Authority (CMA) providing oversight over its bond issuance in the capital market.

- Expected Benefits & Challenges of MRCs

Once operational, the expected benefits of MRCs will include;

- Increased home ownership

The sole aim of KMRC is to increase the number of people eligible to take up mortgages thus increasing home ownership among Kenyans. The facility is expected to enable the lenders to offer longer mortgage tenures of 20-years on average, and at relatively cheaper rates, to be capped at 10% per annum according to current proposals. However, it is not yet clear how the market will achieve such low rates without any special government subsidies, because even a risk free 20-year government bond rate is 12.8%. We therefore assume the rates will be maintained at 13.3%-13.8%, which is 0.5%-1.0% points above the 20-year bond rate of 12.8%.

The table below shows the monthly payments for a standard 3-bedroomed affordable housing unit going for Kshs 3.0 mn. At the prevailing market conditions with average interest rates at 13.6% and tenure of 12-years, the required monthly payments are Kshs 42,359. Assuming this accounts for 40.0% of the household’s monthly income, this means the household earns a gross income of Kshs 106,000. If the facility maintains the current average mortgage interest rates but prolongs average tenure to 20 years, the monthly payments reduce by 14.0% to Kshs 36,437, which is affordable to households earning Kshs 92,000 per month.

All figures in Kshs unless stated otherwise

|

Mortgage Affordability |

||||||

|

Market Rates |

Amount Borrowed |

Interest Rate |

Tenure (Years) |

Total Interest |

Monthly Payments |

Affordability (Gross Income by 2 persons) |

|

Current Rates |

3.0m |

13.6% |

12 |

3.1m |

42,359 |

106,000 |

|

KMRC |

3.0m |

13.6% |

20 |

5.7m |

36,437 |

92,000 |

|

KMRC |

3.0m |

13.8% |

20 |

5.8m |

36,870 |

93,000 |

- Growth of the Kenyan Mortgage Market

Despite the progress in recent years, the Kenyan mortgage market still lags behind more mature markets like South Africa and Morocco. The KRMC is expected to improve the primary and secondary mortgage markets, by providing secure, long-term funding to the mortgage lenders, thus increasing the number and financial muscle of mortgage lending financial institutions in the country.

- Increased Liquidity for Banks

The KMRC will provide the needed long-term funding to mortgage lenders, thus, creating liquidity for the institutions. This will increase the lenders’ ability to advance mortgages to applicants therefore increasing the vibrancy of the mortgage market and lead to a rise in the number of mortgages issued in the market.

- Standardization, Improved Lending Practices, and Increased Inclusivity

As a non-bank financial institution, KMRC will be partly owned by financial institutions, World Bank and the Government of Kenya while being regulated by the CBK, and overall oversight being provided by the Capital Markets Authority (CMA). SACCOs, which primarily represent the low-income masses, will also be brought on-board, leading to increased inclusivity. Once operational, KMRC targets 50,000 mortgages within 5-years. This is expected to increase competitiveness in the mortgage market, leading to improved lending practices among the mortgage lenders in terms of rates, tenures and processing fees, thus resulting in a more streamlined, standardized and cost-efficient market.

- Expansion of the Bond Market

KMRC will create more opportunities for investors by introducing new investment products such as mortgage-backed securities to the local capital market. This will provide an extra market for investors willing to subscribe to bonds, thus increasing their options and ultimately leading to a more competitive market.

The main challenges that are likely to face KMRC include:

- High Cost of Debt

In order to raise funds, the KMRC will issue mortgage-backed bonds, where investors are likely to demand high yields of between 13.5% - 13.8%, assuming a 1.0%-point margin above the minimum of the risk-free rate for a 15-year bond, which currently stands at 12.5%, or 12.8% for a 20-year bond. This, in our view, is still high for financing end user mortgages as it might mean high costs of debt, and will thus pose a challenge to the KMRC’s target of providing mortgages at 9% interest, potentially locking out low-income earners from accessing mortgages.

- Competition from Government Instruments

The KMRC may face challenges in its efforts to raise funds through issuing of bonds, due to competition from government instruments such as treasury bills, treasury bonds and government stocks. The KMRC will primarily focus on reducing cost of mortgages, thus may issue bonds at lower rates than the government instruments in order to maintain affordability of the mortgages offered. This will lead investors to shy away from the KMRC issued bonds, and instead subscribe to government instruments.

- Maturity Mismatch/Lack of Access to Secure Long-Term Funding

Maturity mismatch arise when the tenure of the mortgage-backed bonds is shorter than the mortgages they refinance. Typically, lenders in emerging markets tend to shy away from issuing long-term mortgages with tenures of 20-years for instance, backed by relatively shorter bonds of 10 years on average. According to the World Bank, the main challenge for the Tanzanian Mortgage Refinance Company was lack of access to long-term funds among lenders in Tanzania. This is a challenge that is also likely to face the Kenya Mortgage Refinancing Company, thus negatively affecting its operations because of inadequate funding.

- Bureaucracy and Inefficiencies in State Departments

Prolonged due diligence processes due to bureaucracy in departments offering critical services such as registration of properties and title deeds is likely to slow down operations of the KMRC. Inefficiencies also reduce the number of people eligible for mortgages thus negatively affecting the KMRC’s effort to increase mortgage uptake.

- Case Study: Tanzania MRC

In Africa, the average mortgage to GDP ratio is estimated to be at 5.0% with South Africa, Namibia, Morocco and Tunisia leading with 31%, 20%, 15%, and 13%, respectively, as at 2018. With the intensified focus on the affordable housing deficit in Africa, various countries have attempted to improve the mortgage markets, which are key impediments to the success of filling in the housing deficit gaps. To this end, we have seen countries such as Tanzania, Egypt and Nigeria establish mortgage refinancing facilities ultimately leading to increased mortgage products that are affordable to mid and low-income earners in the respective countries. We selected Tanzania as our case study due to comparability to the Kenyan market in terms of financial markets structuring as well as prevailing market conditions.

Introduction

With an estimated population of 56.9 mn as at 2018, according to the World Bank, Tanzania has a fast-growing housing demand which is also bolstered by the strong and sustained economic growth with GDP growth averaging at 6.0%-7.0% over the past decade. Furthermore, with majority of the population falling under low- and mid-income class, the country has a huge affordable housing deficit estimated at 3.0 mn units and growing annually by 200,000 units, as per the Tanzania National Housing Corporation. The deficit has been attributed to high property prices that are out of reach for majority of Tanzanians coupled by relatively high costs of finance. The fast-growing Tanzanian population is expected to more than double by 2050 with 50.0% living in urban areas, calling for efforts by the government to meet the growing demand of affordable housing. Consequently, TMRC, a non-banking institution owned by Tanzanian banks, was launched in 2011 with the sole purpose of financing mortgage lending banks’ portfolios in order to grow the mortgage market and increase home ownership rates in Tanzania.

Initially, TMRC began operations by using World Bank’s loan of USD 30.0 mn (Kshs 3.0bn) as well as the equity funds by the shareholders, whose requirement was a minimum subscription of Kshs 21.8 mn each, to finance primary lenders’ mortgage portfolios.

Bond Issuance

In 2017, TMRC managed to place bonds worth Kshs 174.4 mn with three pension funds; Government Employees Provident Fund (GEPF), Parastatal Pensions Fund (PPF), and Workers Compensation Fund (WCF). In 2018, TMRC offered the public its first issue of a corporate five-year bond worth Kshs 523.4 mn, which managed to raise Kshs 545.3 mn, a 4.3% oversubscription (Bank of Tanzania). The TMRC bond fixed-interest rate was 11.79%, set at 0.5% points above the 5-year Treasury bond whose interest rate was 11.29%.

TMRC Achievements

As at 2018, Mortgage to GDP ratio in Tanzania was at 0.3% from virtually zero 8-10 years ago, and as at December 2017, total mortgage loans by banks in Tanzania amounted to Kshs 15.0 bn, a 34% 5-Year CAGR, from Kshs 4.9 bn as at December 2012. The growth of Tanzania’s mortgage market is attributable to (i) favorable interest rates, (ii) increased awareness on mortgage loans among borrowers due to public awareness campaigns by major banks, (iii) extended tenor of mortgages, and (iv) increased competition due to continued entry of new lenders in the market.

The key achievements by TMRC are as indicated below:

- Mortgage refinance and pre-finance loans grew by a 5-Year CAGR of 64% from Kshs 187.6 mn in 2012 to Kshs 3.6 bn in 2017, bolstered by increased uptake by the primary mortgage market,

- Number of banks offering mortgage loans grew by 933.3% from 3 in 2011 to 31 by 2017,

- Mortgage repayment periods increased from a maximum of 5-7 years to 15-25 years. Initially, demand for the TMRC did not materialize as a result of banks’ reluctance to take on any maturity mismatches ahead of refinancing. Therefore, TMRC was redesigned to offer a pre-financing mechanism, through loans collateralized by government treasury bonds to the primary lenders, who then develop mortgage portfolios. The chance of banks misusing the funds is overseen through strict policies and penalties,

- Typical mortgage interest rates in Tanzania currently stand at 15%-19% on average, compared to 22%-24% in 2011. The interest rates were largely brought down as a result of growing competition from increasing number of lenders.

Key Challenges Facing TMRC

Demand for housing in Tanzania continues to be extremely high as a result of limited affordable units further constrained by relatively high interest rates that lock out the average Tanzanians. The key challenges to the maturity of Tanzania’s mortgage market include:

- Insufficient housing stock that can qualify for mortgages,

- High cost of land for development which is passed through to end-buyers,

- Low income levels leading to low mortgage affordability, and

- Bureaucratic processes with regards to issuance of titles, which negatively affects mortgage eligibility for homebuyers

As a result, the Government of Tanzania through institutions such as the National Housing Corporation, the Tanzania Building Authority and pension bodies such as NSSF are actively involved in development, selling and renting of houses for the Tanzania residents in order to address the housing shortage. NHC’s major ongoing projects in Dar es Salaam include the 711 Kawe, Morocco Square, and Victoria Place. Completed projects include Mwongozo and Kigamboni Housing Projects whose price points of Kshs 2.4 mn - Kshs 6.9 mn and Kshs 2.4 mn – Kshs 2.8 mn respectively, saw the projects achieve annual uptake of 84.0% and 100.0%, respectively. Upcoming projects include 559.4 acres SafariCity in Arusha and Iyumbu Satellite Town in Dodoma, both targeting low- and mid-income earners. See Cytonn Research Report on Dar

- Lessons for Kenya MRC from Tanzania MRC

TMRC has been fairly successful in improving its mortgage market as seen through the longer mortgage repayment periods and lower interest rates. The key takes for Kenya from Tanzania’s case are:

- Financial Capacity is Key: TMRC’s initial goal of tapping the capital markets was hampered by high treasury bond interest rates and inflation rates. At this stage, the facility received its financing from International Development Association through the Bank of Tanzania at 10.0% and loaning this to mortgage lenders at 11.5%, allowing the facility to create interest income as its own funds. KMRC’s goal to raise funds through the capital markets is also likely to experience its own challenge as the current interest rates for 15 and 20 year bonds stand at 12.5% and 12.8%, respectively. Therefore, assuming a 1.0% risk premium, KMRC bond interest rates would be 13.5%-13.8% which would mean refinancing lenders at higher rates and ultimately raising the mortgage interest rates to the borrower. Therefore, if the KMRC refinances at the market clearing levels, its financing costs may surpass the current average mortgage interest rates of 13.6%, leaving no spread for the facility or the lenders while also defying the intended purpose of reducing or maintaining current mortgage interest rates. To this end, the KMRC would either:

- Refinance at cost which would mean no spread for the facility, as well as competition from treasury bonds, possibly leading to undersubscription,

- Opt for medium-term bonds, say five-year, which would have lower interest rates. Currently, interest rates for a five-year treasury bond stands at 10.8%, or

- Refinance lenders’ mortgage portfolios using finance from the World Bank and other shareholders’ equity as they build up on entry to capital market

- Affordable Housing: Improving home affordability to the average-income homebuyers is a key component as seen in Tanzania’s NHC subsidized homes. Additionally, in Tanzania, the affordability project entailed the transformation of NHC into a master developer whose main role is to prepare land, devise an overall plan and create a conducive investment environment for private real estate developers. This has seen the corporation deliver affordable units on land belonging to the Government of Tanzania with units going for as low as Kshs 2.4 mn for a three-bedroom bungalow. Therefore, the Government of Kenya should channel its efforts towards ensuring the operationalization of KMRC goes hand in hand with realization of the affordable housing initiative,

- Awareness Campaign: Initially, TMRC failed at creating demand from primary lenders largely due to lack of sufficient knowledge amongst lenders and borrowers. KMRC, therefore, should create awareness among investors and lending institutions in order to ensure it begins operations on a firm ground. In addition to this, KMRC should be designed in such a way that it offers incentives to its various stakeholders to enable it to raise its own funds,

- Complementary Solutions: Tanzania, and other countries such as Nigeria and India, supplement their housing efforts with microfinance markets, to enable even the informal workers to access housing finance. Therefore, the government should strengthen the microfinance and housing cooperatives market in order to provide long-term housing microfinance/ cooperatives to low income earners who may not access the conventional mortgage finance.

In summary, we expect the KMRC to:

- Increase the amounts of monies available for mortgage lending, and

- Lengthen typical mortgage tenures in Kenya from the current average of 12 years to 20 years, bringing down monthly payments by 14%, assuming current average interest rates of 13.6%,

- Maintain the current market interest rates of 13.6% - 13.8%, (noting mortgages are fairly priced at just 100 bps above 15-year and 20-year government bonds at 12.5% and 12.8%, respectively. There has been talk of KMRC bringing down cost of mortgages to 10%, but not clear how that would be achieved as even the government has to pay 12.5%).

With the above impacts, we expect that the facility will help in addressing Kenya’s housing deficit by extending the range of qualifying mortgage borrowers, resulting in growth of home ownership rate and a vibrant mortgage market.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma