Aug 19, 2018

The International Monetary Fund (IMF) recently concluded their visit to Kenya where they were holding discussions with the Kenyan Government on the second review under a precautionary Stand-By Arrangement (SBA), which was extended to Kenya on 14th March 2016. The SBA is a lending arrangement extended by the IMF to member countries in emerging markets in need of financial assistance, normally arising from financial crisis. In a press statement after the Kenyan visit, the IMF stated that their mission to assess the Kenyan economy achieved significant progress, but it remains uncertain if Kenya’s access to the standby facility will be extended as talks with the government are set to continue. As such, this week we are focusing on whether Kenya needs the facility. In this note we shall address the following items:

- The IMF’s available programs and engagement with Kenya,

- The IMF’s visit to Kenya in 2018 and the key take outs,

- Economic factors that warrant the need for the IMF Facilities,

- Our view on the way forward.

Section I: The IMF’s available programs and engagement with Kenya:

The International Monetary Fund was created to protect the stability of financial systems globally. The IMF does this by offering loan facilities to countries facing Balance of Payment problems to stabilize and restore their economic growth while maintaining safe level of reserves on affordable terms as compared to financing from capital markets. Unlike the World Bank and other development agencies, the IMF does not finance projects and its main role is crisis resolution through various forms of lending, which include:

- Stand-By Arrangement (SBA): The SBA is the main lending arrangement advanced to emerging markets. It is a non-concessional lending arrangement with a market-based interest rate, though almost always lower than the rates from private markets financing arrangements,

- Flexible Credit Line (FCL): The FCL is advanced to countries with good track records and strong policies. A country has the flexibility of treating the FCL as a precautionary or draw from it once it is approved. The facility could be for either 1 or 2-years with the option of renewal. Once approved, the country is given the rights to access these resources without pre-set conditions on economic policies or in disbursements set in phases like in emerging countries. Countries that qualify for FCL must exhibit a strong track record and as a result the IMF has confidence that their economic policies would remain strong even in the event of external shocks,

- The Precautionary and Liquidity Line (PLL): The PLL serves as insurance for countries with strong economic policies, by providing financing to meet potential balance of payments needs a country may be facing. It has similar qualification process to FCL, but unlike FCL it has ex-post conditions with the purpose of addressing the likely vulnerabilities that might have been identified during the qualification process,

- Rapid Financing Instrument (RFI): Under this facility, member countries facing immediate Balance of Payment issues including those emerging from natural disasters, commodity price shocks, among others, can access financing without the need for a full-fledged program,

- Extended Fund Facility: This facility is advanced to address balance of payments resulting from structural problems a country may be facing that may require a long time to correct. The program is usually backed by measures aimed at improving the workings of the markets as well as institutions through measures such as financial sector and tax reforms,

- The Rapid Credit Facility (RCF): which is advanced low-income countries that are facing urgent balance of payment needs. The program mainly focuses on reduction of the country’s poverty levels as well as enhance its growth objectives by providing high levels of concessions as compared to market rates, and,

- The Standby Credit Facility (SCF): The program provides financing to low-income countries that are facing short-term Balance of Payments needs. The facility as well focuses mainly on poverty reduction while promoting the country’s growth objectives by charging low interest rates as compared to market rates. The facility can also be used on a precautionary basis to cushion the country from external shocks.

Kenya has in the past been able to access various forms of financing from the IMF dating back to 7th July 1975, with the latest ones being approved on 14th March 2016, where the IMF advanced a new arrangement totaling to USD 1.5 bn through a standby arrangement (SBA) and a standby credit facility (SCF) of USD 989.8 mn and USD 494.9 mn, respectively.

|

Amounts in USD, converted from SDR at current exchange rate 1 SDR=USD 1.39 (as at 15 August 2018) |

|||||||||||

|

Facility |

Date of Arrangement |

Expiration Date |

Amount Agreed |

Amount Drawn |

Amount Outstanding |

||||||

|

Standby Arrangement |

14-Mar-2016 |

13-Mar-2018 |

985,870.0 |

0 |

0 |

||||||

|

Standby Credit Facility |

14-Mar-2016 |

13-Mar-2018 |

492,934.3 |

0 |

0 |

||||||

|

Standby Credit Facility |

2-Feb-2015 |

14-Mar-2016 |

188,623 |

0 |

0 |

||||||

|

Standby Arrangement |

2-Feb-2015 |

14-Mar-2016 |

490,419.8 |

0 |

0 |

||||||

|

Extended Credit Facility |

31-Jan-2011 |

19-Dec-2013 |

679,042.8 |

679,042.8 |

642,072.9 |

||||||

|

Extended Credit Facility |

21-Nov-2003 |

20-Nov-2007 |

208,500 |

208,500 |

5,212.5 |

||||||

|

Extended Credit Facility |

4-Aug-2000 |

3-Aug-2003 |

264,100 |

46,704 |

0 |

||||||

|

Extended Credit Facility |

26-Apr-1996 |

25-Apr-1999 |

207,874.5 |

34,645.8 |

0 |

||||||

|

Extended Credit Facility |

22-Dec-1993 |

21-Dec-1994 |

62,869.7 |

62,869.7 |

0 |

||||||

|

Extended Credit Facility |

15-May-1989 |

31-Mar-1993 |

363,346 |

300,472.1 |

0 |

||||||

|

Structural Adjustment Facility Commitment |

1-Feb-1988 |

15-May-1989 |

138,166 |

39,476 |

0 |

||||||

|

Standby Arrangement |

1-Feb-1988 |

15-May-1989 |

118,150 |

87,014 |

0 |

||||||

|

Standby Arrangement |

8-Feb-1985 |

7-Feb-1986 |

118,428 |

118,428 |

0 |

||||||

|

Standby Arrangement |

21-Mar-1983 |

20-Sep-1984 |

244,570.5 |

244,570.5 |

0 |

||||||

|

Standby Arrangement |

8-Jan-1982 |

7-Jan-1983 |

210,585 |

125,100 |

0 |

||||||

|

Standby Arrangement |

15-Oct-1980 |

7-Jan-1982 |

335,685 |

125,100 |

0 |

||||||

|

Standby Arrangement |

20-Aug-1979 |

14-Oct-1980 |

170,240.3 |

0 |

0 |

||||||

|

Standby Arrangement |

13-Nov-1978 |

19-Aug-1979 |

23,977.5 |

23,977.5 |

0 |

||||||

|

Extended Fund Facility |

7-Jul-1975 |

6-Jul-1978 |

93,408 |

10,703 |

0 |

||||||

|

Total |

|

|

5,396,790 |

2,106,603 |

647,285 |

||||||

|

*SDR (Special Drawing Rights) - Artificial currency instrument used by the IMF, and is built from a basket of important national currencies. The IMF uses SDRs for internal accounting purposes 1 SDR=USD 1.39 (as at 15 August 2018) |

|||||||||||

On a letter of intent dated January 16th, 2015, the Government of Kenya made a request to the IMF to be granted access to a blended program supported by a Stand-By Credit Facility (SCF), with total access of SDR 488.5 mn (about USD 679.0), over the next 12-months, of which SDR 352.8 mn (about USD 490.4) under the SBA and SDR 135.7 mn (About USD 188.6) under the SCF. While noting that the country did not have balance of payments needs, the government cited concerns of possible vulnerabilities from exogenous shocks. This was due to the expected capital expenditure from the planned acceleration of infrastructural projects, which included (i) the Standard Gauge Railway, (ii) expansion of expansion of geo-thermal power generation capacity at the Olkaria III complex whose completion in 2016 added 29 MW, increasing the facility’s capacity to 139 MW, (iii) expansion of the port of Mombasa, and (iv) enhancement of food security by expanding irrigation. The expected reforms, coupled with incidences of terrorism, which has previously adversely affected investor’s risk, represented additional challenges and as such, the government saw the need for the program as a way of mitigating possible exogenous risks. The Executive Board of the IMF later on 2nd February 2015 approved a 1-year arrangement comprising of a SDR 352.8 mn (about USD 497.1 mn) Stand-By Arrangement and a SDR 135.7 mn (about USD 191.2 mn) arrangement under the Stand-By Credit Facility.

On 14th March 2016, after the expiry of the previous SBA and SCF for Kenya, the IMF approved a new arrangement totaling USD 1.5 bn comprising of a SDR 709.3 mn (about USD 989.8 mn) 24-month Stand-By Arrangement (SBA) and a SDR 354.6 mn (about USD 494.9 mn) 24-month Standby Credit Facility (SCF). Before the recent visit to Kenya by the IMF officials, only the 1st review had been completed on 25th January 2017. The Executive Board of the International Monetary Fund (IMF) had approved the Kenyan Government’s request for a 6-month extension of the Stand-By Arrangement (SBA) on 12th March, 2018, to allow more time for the completion of the outstanding reviews. Key to note, the 6-months extension request was only for the SBA arrangement and not the SCF since the SCF arrangement can be approved up to a maximum of 24-months, which had already lapsed. The 2nd and 3rd reviews of the arrangement had been pending since the fiscal balance, which is a key performance criterion, had not been met as at the end of December 2016 and June 2017 attributed to the shortfall in revenues and pressure on government spending, which was partly due to the challenging operating environment. An understanding could not be reached on corrective measures the government was to undertake to tackle the problems on account of the prolonged electioneering period thus the request for an extension. To resolve the fiscal deficit problem, the government highlighted its intention to reduce the expenditure as well as increase revenues through the introduction of the Finance Bill, which would have several tax reforms.

Section II: The IMF’s Visit to Kenya in 2018 and the key take outs:

A team from the International Monetary Fund (IMF) later visited Kenya from July 23rd to August 2nd, 2018, to hold discussions on the second review under a precautionary Stand-By Arrangement (SBA). From the discussions with the Kenyan authorities, they noted that:

- Kenya’s economy had continued to perform well with the GDP having expanded by 5.7% in Q1’2018, up from 4.9% growth experienced in Q1’2017, with the growth being driven by strengthened investor confidence following the conclusion of the prolonged electioneering period, improved weather conditions in 2018 with the country having experienced a drought in 2017 and a recovery in tourism, which can be evidenced by an increase in the total number of visitors arriving through Jomo Kenyatta International Airport and Moi International Airports, that increased by 2.1% to 76,608 in June 2018 from 75,028 in May 2018, despite a 4.4% decline y/y from 80,121 in June 2017, as per data from Kenya National Bureau of statistics (KNBS),

- Inflation has remained within the 2.5% - 7.5% government set target since July 2017. Inflation has been low, coming in at 4.4% in July and averaging 4.3% for the 1st 7-months of 2018, compared to 9.5% in a similar period in 2017. We expect inflation to remain within target in 2018 despite the expectations of upward pressure in H2’2018, partly due to the base effect, and the expected rise in fuel and transport prices with the introduction of 16.0% VAT on petroleum products as from September 2018 and other tax reforms proposed under the Finance Bill 2018,

- Kenya had managed to meet the IMF’s program fiscal target for the FY2017/2018, with the budget deficit for the 2017/2018 fiscal year coming in at Kshs 614.6 bn (equivalent to 7.0% of GDP), which is a significant narrowing from 9.0% of GDP previously,

- The current account deficit has started to adjust in 2018 after widening to 6.7% of GDP in 2017 from 5.2% in 2016, which was mainly driven by higher food imports and weaker agricultural exports due to the drought experienced during the year, coupled with higher fuel imports owing to rising global oil prices. The lower current account deficit so far in 2018, which narrowed to 5.8% in the 12-months to June 2018 from 6.3% in March 2018, has been attributed to improved agriculture exports, and lower capital goods imports following the completion of Phase I of the SGR project, and,

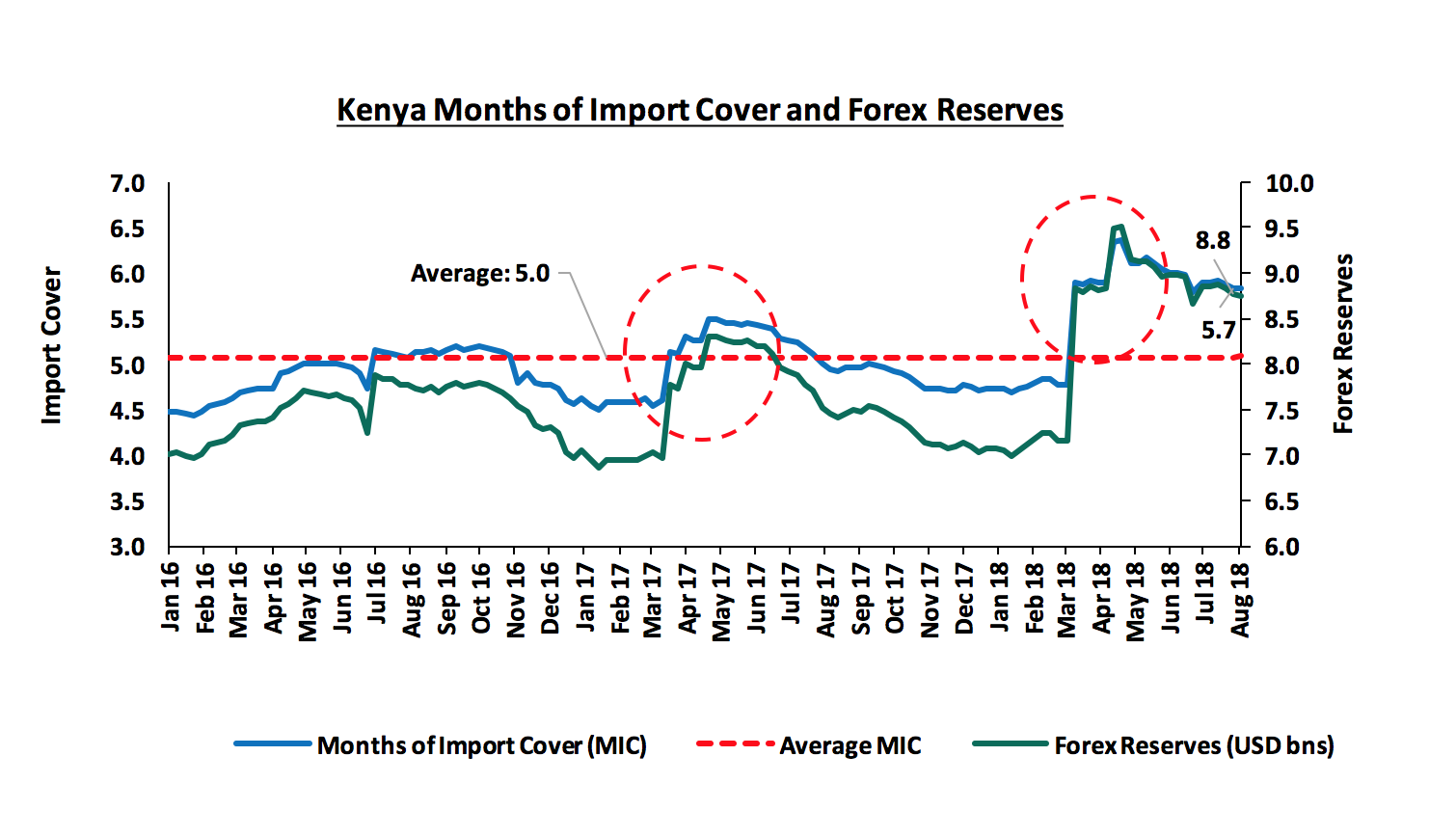

- The Kenyan Shilling has remained resilient against major currencies, while foreign exchange reserves have been relatively high currently standing at about USD 8.7 bn (equal to 5.8-months of projected imports for 2018).

Based on the above, GDP growth, inflation and the performance of the Kenyan shilling are positive while we are neutral on the fiscal deficit and the current account deficit. As such, we are of the view that Kenya is on the right trajectory towards improving the macroeconomic conditions of the country. From the FY 2018/2019 budget, the government is set to focus on a fiscal consolidation plan aimed at narrowing the fiscal deficit to 5.7% of GDP from 7.2% of GDP in the FY 2017/18 and further to around 3.0% of GDP by FY 2021/22. The government plans to achieve this through revenue enhancement measures, projected to raise revenue by 17.5% to Kshs 1.9 tn (equivalent to 20.0 percent of GDP) in the FY 2018/19 from the estimated Kshs 1.7 tn collected in the FY 2017/18, and a reduction in Government expenditure, which will in turn lead to reduced dependency on debt with the total borrowing requirement to plug in the deficit expected to decline to Kshs 558.9 bn from Kshs 620.8 bn, in a bid to reduce Kenya’s public debt burden. The existing program is set to expire on September 14th 2018 and it remains uncertain if Kenya’s access to the stand-by facility will be extended as talks with the government are set to continue in the coming week with the IMF team expected to submit final report to the IMF Board by the end of August.

Section III: Economic Factors that warrant the need for the IMF Facilities

Since the approval of the standby credit facility, Kenya has not tapped into the facility. We believe that the following economic factors may warrant the need for Kenya to take up the IMF facilities;

- Sustaining the strong performance of the Kenyan Shilling

The Kenyan Shilling has continued to be resilient against major global currencies having gained by 2.7% against the US dollar on a year to date basis, being the best performing currency in Sub Saharan Africa despite the dollar index also gaining by 4.9% in a similar period. The shilling has continued to be stable despite the extended electioneering period and global disturbances resulting from monetary policy decisions such as the Fed-rate hikes for the first time in 9-years that were expected to result in capital outflows from emerging markets as well as the tax-cutting policies being implemented in the USA. The stability of the shilling has further been supported by the high forex reserves currently at USD 8.7 bn (equivalent to 5.7 months of import cover) that are adequate to cushion the Kenyan Shilling against major global currencies. The high forex reserves have however mainly been boosted by debt capital as seen from the chart below, with the hike in 2017 being attributed to the USD 800 mn syndicated loan from 4 international banks and the USD 500 mn facility from the African Export-Import Bank (Afreximbank). The 2018 hike in the reserves has also been boosted by Kenya’s issue of a 10-year and 30-year Eurobond where it raised USD 2.0 bn, which propped up the Kenyan Shilling, coupled with the support from the improvements in primary exports, which include coffee, tea and horticulture, which increased by 10.8% during the month of May to Kshs 24.3 bn from Kshs 21.9 bn in April, with the exports from coffee, tea and horticulture improving by 11.0%, 19.1% and 2.0% m/m, respectively. The availability of the Standby-facility as a precautionary measure would be essential in cushioning the Kenyan shilling to eventualities of unforeseen external shocks.

- Unsustainable Debt Levels

Kenya’s debt portfolio is high having hit 55.6% by the end of 2017, 5.6% above the East African Community (EAC) Monetary Union Protocol, the World Bank Country Policy and Institutional Assessment Index, and the IMF threshold of 50.0%. This was a rise from 43.9%, 5-years ago, and 38.4%, 10-years ago. It was estimated that Kenya would use approximately 40.3% of the revenues raised from tax collection to finance debt payments in the fiscal year 2017/18. Kenya’s current Public & Publicly Guaranteed External debt stood at USD 24.9 bn as at March 2018. With the expectations of outflows due to debt financing of the outstanding external debt, coupled with major infrastructural projects under the Big 4 Agenda, we expect the forex reserves to decline and as such, the IMF reserve would be essential as a precautionary measure to safeguard the country from any external shocks. As detailed in our topical on Kenya’s Public Debt, Should We Be Concerned?, the Kenyan Government has started embarking on measures to improve debt management, as detailed in the budget, which include:

- Raising revenue targets in order to minimize the reliance on debt,

- Building an export-driven economy by encouraging growth in the manufacturing sector to increase the value-added exports in a bid to improve the Balance of Payment,

- Active private sector involvement in development projects in order to reduce the strain on government expenditure and hence borrowing.

- The government is also recruiting debt management experts who will be tasked with providing guidance on determination of borrowing ceilings for national and county governments, as well as preparing proposals for debt restructuring and liaising with the Central Bank of Kenya (CBK) and other Treasury departments for effective debt management.

Section IV: Our View on the Way Forward:

We need to do all we can to qualify for the renewal of the SBA program because:

- Programs from the IMF largely comes attached with conditions aimed at enhancing fiscal discipline, which if implemented would reduce risk perception of Kenya and reassures investors. Conditions include - policy changes, such as the targeted inflation that the country must maintain, increased taxation in a bid to increase government revenues while minimizing dependency on debt, cutbacks of government spending and reduction of fiscal deficits. As such, this reduces the risk perception of countries while improving investor sentiments as signing up to undertake the fiscal policy measures in order to be granted access to the facilities would provide reassurance to investors of expected improvements and stability in the macroeconomic conditions of such a country. In the event of the country issuing more external debt, the availability of the facilities would lead to a reduction in the risk premium demanded by investors due to the improved risk perception,

- Cushioning from shocks: Despite the high forex reserves and improving macroeconomic conditions currently being experienced in Kenya, with the country having expanded by 5.7% in Q1’2018 and positive adjustments in the current account deficit having narrowed to 5.8% in the 12-months to June 2018, from 6.3% in March 2018, we are of the view that the availability of the program as a precautionary facility would be essential in cushioning the country from unforeseen exogenous shocks such as sharp rises in global oil prices, massive dollar outflows that would to a volatile dollar exchange rate, and other risks which would threaten forex reserves. The facility would also be essential in enhancing offshore investments, as it would show the level of preparedness of the country to eventualities of a weakening currency thus reducing currency risk.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma