Oct 28, 2018

Infrastructure refers to the fundamental structure of an organization or system, which is necessary for its operation, and entails public water, energy, and systems for communication and transport. It is thus, considered the backbone of any country’s economic growth. Infrastructural improvements such as road and rail networks enhance a nation’s connectivity thus, unlocking the economic potential of a region by opening it up for trade and investments, as it allows for easy transport of labor, goods and services to where they are in demand. In real estate, infrastructure acts facilitate the sector’s growth as its availability, or lack thereof, determines the growth momentum of the real estate sector in a given location. Transport systems, for instance, enhance accessibility from home to the work place and vice versa, whereas utilities such as water, sewage disposal and electricity are essential for human living.

In the recent past, we have witnessed the Kenyan Government’s dedication to improving the infrastructural levels in Kenya, especially transport, as part of its efforts to elevate the country to upper middle-class status by 2030. For instance, according to the KNBS Economic Survey 2018, the development expenditure on roads is set to grow by 19.2% to Kshs 134.9 bn in 2017/18 from Kshs 109.0 bn 2016/17. Additionally, the Kenya Roads Board (KRB) is set to increase disbursements to the various road agencies and County Governments by 5.0% to Kshs 63.5 bn in 2017/18, from Kshs 60.5 bn in 2016/17. Examples of key road projects launched within the Nairobi Metropolitan Area since 2017 include the Western Bypass, and the dualling of Ngong Road Phase 3, among others. We anticipate that such projects will have a positive impact on the economic development in the region through driving sectoral growth including that of real estate.

Given our continued focus on real estate investment, with majority of our projects being in the Nairobi Metropolitan Area, this week we look at the state of infrastructure in the Nairobi Metropolitan Area, ongoing infrastructural projects and the areas expected to benefit from these and then take a view of the potential areas for real estate investment. To cover this, we shall address the following;

- Factors Affecting Infrastructure in the Nairobi Metropolitan Area; Drivers, Challenges, and Recent Developments,

- The State of Infrastructure in the Nairobi Metropolitan Area,

- Impact of Infrastructure on Real Estate, and,

- Conclusion – Recommended Areas for Real Estate Investment.

- Factors Affecting Infrastructure in the Nairobi Metropolitan Area; Drivers, Challenges, and Recent Developments

In the last few years, there has been increased investment in infrastructure in the Nairobi Metropolitan Area by both public and private sector players. The main factors driving investment in the sector include:

- Positive Demographics:

Nairobi Metropolitan Area has a relatively high population growth rate of 3.1% against the national and global average growth rate of 2.5% and 1.2%, respectively, as at 2018, which continues to outstrip infrastructure and service capacity thus creating demand for the same as required to serve the growing population. Nairobi County has the highest population density at 6,474 people per SQKM and growing at 4.1% p.a, followed by Kiambu County with a density of 818 people per SQKM and growing at 2.8% p.a, according to the Kenya National Bureau of Statistics (KNBS). Below is a summary table of the various counties’ demographics;

|

Nairobi Metropolitan Area Demographics |

||||

|

County |

Population (2018) |

Land Size(SQ.KM) |

No of people per SQ.KM 2018 |

Population Growth Rate |

|

Kajiado |

1,112,305 |

21,910 |

51 |

5.5% |

|

Nairobi |

4,499,785 |

695 |

6,474 |

4.1% |

|

Kiambu |

2,080,109 |

2,543 |

818 |

2.8% |

|

Machakos |

1,317,022 |

6,208 |

212 |

2.5% |

|

Murang'a |

976,564 |

2,559 |

382 |

0.4% |

|

Average |

|

|

294 |

3.1% |

Source: Kenya National Bureau of Statistics

- Government Initiatives:

These include:

- Establishment of the Road Annuity Fund:

The Roads Annuity Fund was established under the Public Finance Management (Roads Annuity Fund) Regulations, in 2015, for the purposes of providing capital to meet the National Government’s annuity payment obligations for the development and maintenance of roads under the Roads Annuity Programme (RAP). Some of the roads in the Nairobi Metropolitan Area that have been tarmacked or improved using the fund include; Uplands-Githunguri-Ngewa-Ruiru and Bomas-Karen-Dagoretti-Ruiru Road,

- Establishment of the Infrastructure Bond:

In 2016, the Government of Kenya issued a 15-year infrastructure bond of USD 300 Million to fund infrastructure projects. The fund aims to facilitate infrastructural development by acting as a bridge between the public and private sectors, helping eliminate the bottlenecks for private projects and Public Private Partnership Projects,

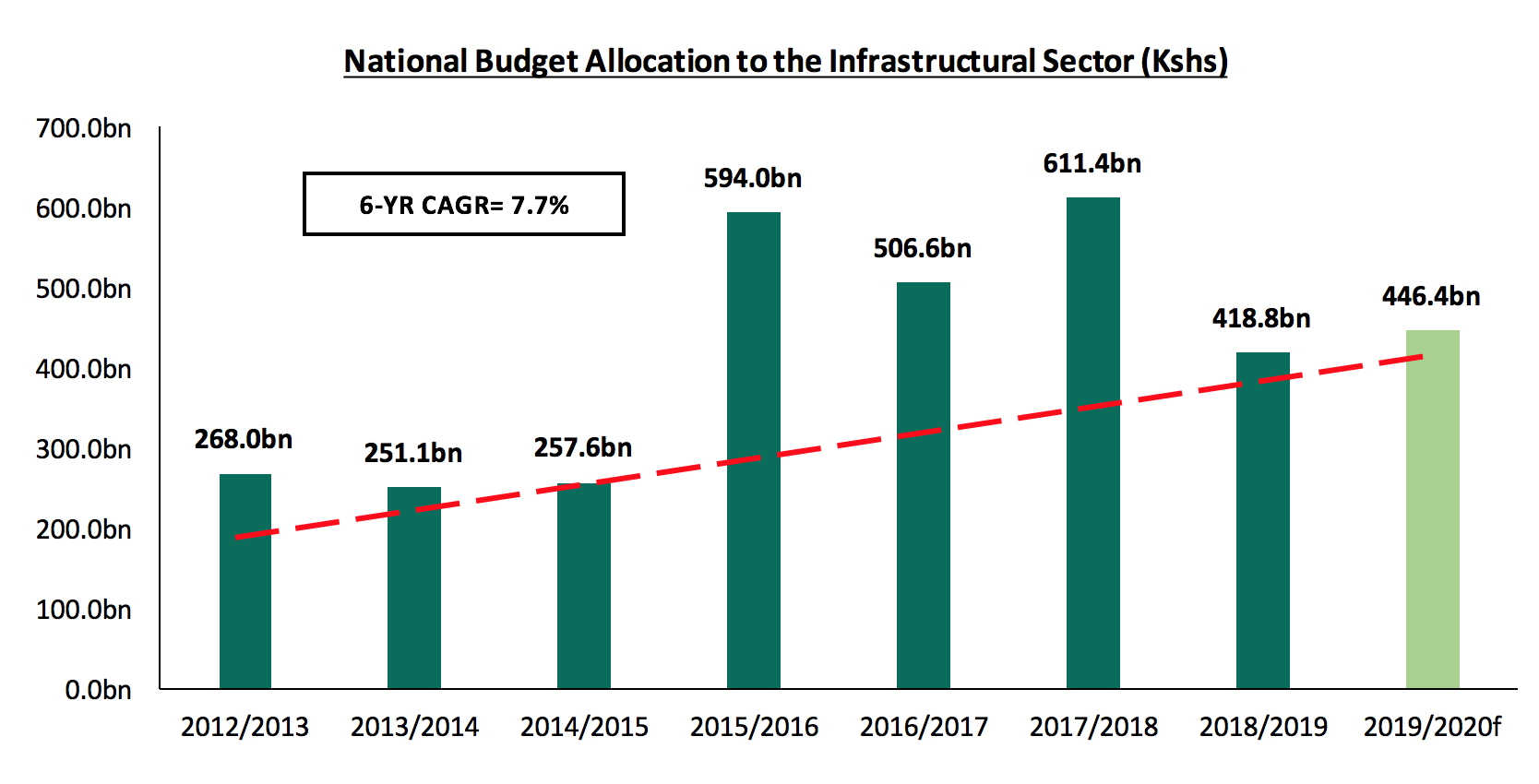

- Increased Budgetary Allocation to Improve Infrastructure in the Country:

The government has intensified efforts to enhance infrastructural development throughout the country, the Nairobi Metropolitan Area included. This is evidenced by the significant National Budget allocation, which recorded a 6-year CAGR of 7.7% from 2012 to 2019. For the year 2018/2019, the budget allocation to infrastructure came in at Kshs 418.8 bn, which is 13.6% of the national budget, as shown below:

Source: The National Treasury

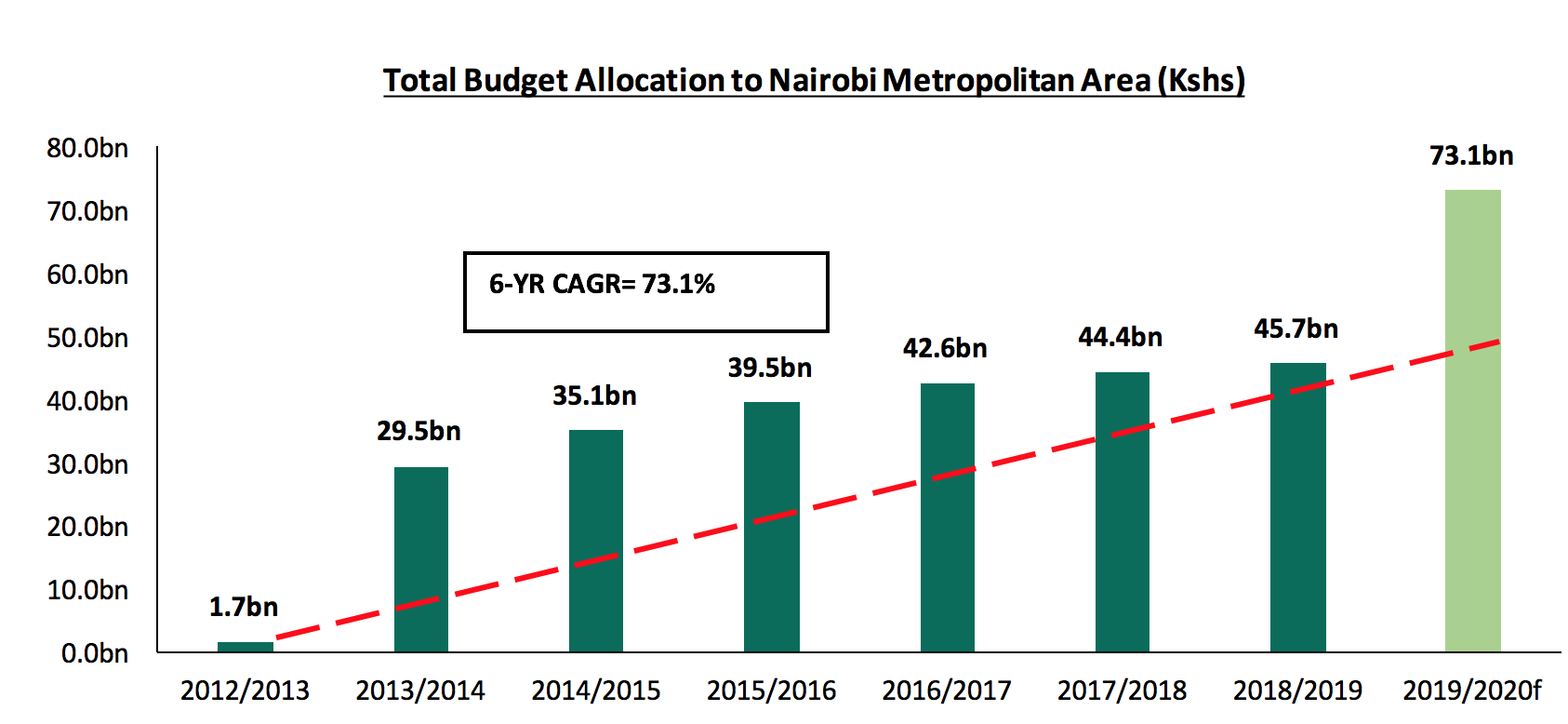

For the Nairobi Metropolitan Area, the total budget allocation made to counties continues to increase, growing by a 6-year CAGR of 73.1%, and a 2.9% increase from Kshs 44.4 bn allocated in the 2017/2018 budget to Kshs 45.7 bn allocated in 2018/2019. This has resulted in continued funding of projects at Kenyan County level, including infrastructural projects. The county’s allocation is as illustrated below:

Source: The National Treasury

- Rising Foreign Direct Investment (FDI) in Infrastructure:

Kenya saw FDI inflow increase by 71.8% from Kshs 39.0 bn in 2016 to Kshs 67.0 bn in 2017, which was attributed to buoyant domestic demand and inflows into the country’s ICT industries. As a result, the country was ranked the 4th highest FDI recipient in East Africa after Ethiopia, Tanzania and Uganda in the World Investment 2018 Report, by the United Nations Conference on Trade and Development (UNCTAD). In line with the same, the infrastructural sector has witnessed entry of foreign institutions such as Bechtel, a global leader in engineering, procurement, and construction. The firm will be constructing the first high-speed expressway in the country, designed to run between Nairobi and the seaport at Mombasa,

- Increasing Private Sector Investment:

Kenya continues to develop programs to foster private sector participation in infrastructure investments to help address the funding gap in the sector. This has resulted in the emergence of Private Public Partnerships (PPP), which boosts the prospects of local construction companies and financial institutions that can offer finance to the companies. Some of the factors encouraging private sector investment include;

- Incentives to encourage private sector involvement: The government continues to encourage private sector investment into the sector through introduction of incentives. For example, through a 25.0% tax exemption, which allows investors in commercial property who spend on social infrastructure such as power, water, sewer lines, and roads to recover their expenses within 4-years, according to the Finance Bill 2012, and,

- Introduction of Power Purchase Agreements to Boost Investment in Energy: Since 2016, Kenya Power has entered into arrangements in the form of Power Purchase Agreements (PPA); an investor, usually a private power company establishes a power plant and sells to Kenya Power at a predetermined rate over a fixed period of approximately 20-years enabling them to recoup their investment. Some of the firms that have entered into a PPA agreement are Akiira Geothermal Limited, who are developing a 70 MW geothermal facility in Kajiado, and Kipeto Power Limited, who are developing a 100 MW wind energy also in Kajiado. Both projects will be sold to Kenya Power as per the PPA.

In spite of the factors boosting the sector’s growth, development of infrastructure also faces various constraints including:

- Huge capital outlay required to develop infrastructural projects, which has continued to discourage potential investors especially from the private sector,

- Encroachment and illegal occupation of land meant for infrastructural projects resulting in delay of projects and escalated project completion costs. For instance, the railway reserve in Kibera, which had been encroached by approximately 9,000 families, thus affecting the operation of cargo trains,

- Vandalism of facilities, such as petroleum products pipeline, electricity transformers and fiber optic lines, have resulted in high maintenance costs and capital loss, thus crippling infrastructural development,

- Lengthy legislative requirements, which include elongated processes of approval discourage investors from taking up infrastructural projects, as they are time consuming and expensive,

In terms of recent trends, some of the new developments in the last 2-years, which are likely to influence the sector include:

- Reintroduction of Toll Roads - The Kenyan Government is now reintroducing toll roads as a way of enhancing the expansion and maintenance of roads. Some of the key highways earmarked for tolling include; the Jomo Kenyatta International Airport (JKIA)-Rironi Highway, the proposed Nairobi-Mombasa Expressway, Nairobi Southern Bypass and the Thika Superhighway, and,

- Government’s Big Four Agenda: The Kenyan Government has embarked on increased focus on infrastructure, which must precede development of projects and has been identified as a key enabler of its Big Four Pillars, which include; a) provision of affordable housing with the delivery of 500,000 housing units by 2022, b) affordable healthcare, c) manufacturing and d) ensuring food security.

- State of Infrastructure in The Nairobi Metropolitan Area

We covered the current supply of infrastructure in the Nairobi Metropolitan Area and projects that are currently underway with a focus on roads, railways, water, sewerage, electricity and airports in the Nairobi, Kiambu, Machakos, Kajiado and Murang’a Counties. From our analysis, majority of the current provision of infrastructure is concentrated in the Nairobi County ranking the highest, followed by Kiambu County. We attribute this to Nairobi’s positioning as not only the capital city of Kenya, but also a key regional commercial hub, thus attracting a large portion of investments by both the public and private sectors.

Below is the analysis of the infrastructure provision in the Nairobi Metropolitan Area;

- Roads

Roads are the most common mode of transport in Kenya accounting for 62.9% of the total value of output from the transport sector as at 2018, according to the Kenya National Bureau of Statistics (KNBS). In 2011, it was estimated that, with the exception of Nairobi, 9.6% of roads in the Nairobi Metropolitan Region were paved compared to a national average of 13.7%. Excluding Nairobi County, Kiambu had the highest percentage of paved roads at 16.0%, Murang’a at 9.7%, Machakos at 6.9% and Kajiado had the lowest at 5.9%. We anticipate that the number of paved roads has significantly increased since then given the increased investment in the roads sector.

Between 2012 and 2018, Nairobi County has received the largest share of funds allocated to road projects at 61%. This is because of completion of roads such as the Southern Bypass, Eastern Bypass and Northern Bypass. In terms of road length, Kiambu County has the highest percentage at 39% attributable to construction roads in the county such as: the 80 km road from Muigai Inn through Kiandutu and Kiganjo to Muthaiga, and the 40 km road from Gatundu to Karinga.

|

Roads Completed in Nairobi Metropolitan Area (2012-2018) |

||||

|

County |

Scope (KM) |

Amount (Kshs) |

Percentage of Roads |

Percentage of Funds |

|

Nairobi |

111.6 |

29,319m |

24% |

61% |

|

Murang’a |

126.9 |

9,393m |

27% |

19% |

|

Kiambu |

184.0 |

6,331m |

39% |

13% |

|

Machakos |

48.0 |

3,240m |

10% |

7% |

|

Grand Total |

470.5 |

48,283m |

100% |

100% |

Source: KenHA, KERRA, KURA

With the increased disbursements of funds for roads development, construction of over 1000 kms of roads within the Nairobi Metropolitan Area has been underway, with Murang’a County having the largest road kilometers under construction at 29.0% of the total road projects. In terms of value, Nairobi has the highest value of investments in roads at 53.2% of the total amounts investments, as most of the roads under construction are class A roads, as Nairobi is the center of the country’s road network.

Some of the key roads under construction include; Western Bypass being built by China Road and Bridge Corporation and running for 31 km starting from Ruaka to the Nakuru highway at Gitaru in Kiambu County. Dualling of Ngong Road (Dagoretti Corner - Karen Roundabout Section) stretching up to 9.8 km in Nairobi County, while in Machakos County; construction of the 8 km Mombasa road to Daystar University Road and the Athi River – Machakos Turn off road covering 21 km. In Murang’a County, one of the major roads under construction is the 40 km road from Murang’a through Gitungi to Njumbi Mioro.

Below is a summary of roads under construction within the Nairobi Metropolitan Area:

|

Summary of Roads Under Construction Within Various Counties Within Nairobi Metropolitan Area |

||||

|

County |

Distance (KM) |

Cost (Kshs) |

% of Road Km |

% of Amounts Investment |

|

Nairobi |

260.8 |

79,192m |

14.0% |

53.2% |

|

Murang’a |

533.1 |

22,700m |

29.0% |

15.3% |

|

Kiambu |

464.5 |

19,505m |

13.2% |

13.2% |

|

Machakos |

314.2 |

19,101m |

17.1% |

12.8% |

|

Kajiado |

267.0 |

8,223m |

14.5% |

5.5% |

|

Total |

1,839.6 |

148,722m |

100.0% |

100.0% |

Source: KenHA, KERRA, KURA

- Railways

The use of rail transport is still low in Kenya accounting for only 0.5% of the value of output from the transport sector in 2017 compared to roads at 62.9%. The total Nairobi Metropolitan Area railway network coverage is 206 km. It consists of 75 km and 15 railway stations within the Nairobi County, and 131 km and 5 railway stations within Kiambu County.

The main railway routes serving the Nairobi Metropolitan Area include:

|

Main Railway Routes in Nairobi Metropolitan Area |

|||

|

Railway Routes |

Intermediate Stops |

Services Per Day |

Average Boarding Per Train |

|

Ruiru - Nairobi |

Kahawa, Githurai, Mwiki, Maili Saba, Dandora, S. Mtwinda, Makadara |

2 |

900 |

|

Embakasi Village - Nairobi |

Aviation, Tai Mall, Avenue Park, Quarry, Donholm, Makadara |

2 |

800 |

|

Kikuyu - Nairobi |

Thogoto, Dagoretti Station, Lenana, Satellite, Kibera, Gatwekera, Mashomoni, Laini Saba |

2 |

800 |

|

Syokimau - Nairobi |

Imara, Makadara |

6 |

732 |

Source: Nairobi Rail Service

To improve public rail transportation for both passengers and cargo, railway infrastructure is undergoing expansion through a number of projects that will serve to improve access within the Metropolitan Area.

Some of the new railway stations recently launched include, Makadara railway station and Imara Daima launched in 2013. Some of the upcoming projects include the Upgrading of Nairobi Railway Station and the Rail flyover project, which is part of Nairobi Integrated Urban Development Master Plan 2030, which will connect Enterprise Road to the Nairobi Central Business District.

|

List of Ongoing and Complete Railway Projects |

||||

|

Ongoing Projects |

Timeline |

Status |

Length |

Value(Kshs) |

|

Kahawa Railway Station |

20 18 |

Completed |

353mn |

|

|

Mombasa-Nairobi |

2017 |

Completed |

472km |

327bn |

|

Nairobi Commuter Rail Network |

2018 |

Ongoing |

149km |

24bn |

|

Nairobi – Naivasha SGR Section 2A |

2019 |

Ongoing |

120km |

172bn |

Source:Kenya Railway Corporation

Other upcoming projects include:

- Naivasha - Kisumu (Section 2B)

- Upgrading of Nairobi Railway Station

- Rehabilitation and Remodeling of Kenya Railway passenger sleeper coaches

- Installation of Commissioning integrated parking system to all the passenger stations

- Water

The main sources of water in the Nairobi Metropolitan Area include piped water, water vendors and boreholes. According to research by the Water Services Regulatory Board (WASREB) 2018, the average rate of access to piped water in the Nairobi Metropolitan Area stood at 59% with Nairobi having the highest coverage at 81%. However, access to piped water in Nairobi’s satellite towns mainly in Kajiado and Machakos Counties still remains low at 42% and 48%, respectively. This has created opportunities for the private sector to invest in other water sources such as water vendors and drilling boreholes to supplement the inadequate and inconsistent water supply to several satellite towns.

|

Nairobi Metropolitan Water Coverage Summary 2018 |

|

|

County |

Water Coverage |

|

Nairobi |

81% |

|

Kiambu |

75% |

|

Murang'a |

47% |

|

Kajiado |

42% |

|

Machakos |

48% |

|

Average |

59% |

Source: Water Services Regulatory Board 2018

The main water service providers for Nairobi and its surrounding areas include:

|

No. |

Water Service Provider |

Jurisdiction |

|

1 |

Nairobi City Water and Sewerage Company |

Nairobi CBD and its environs |

|

2 |

Runda Water Company |

Runda area |

|

3 |

Kiambu Water and Sanitation Company |

Kiambu Township and its environs |

|

4 |

Ruiru – Juja Water & Sewerage Company Ltd |

Ruiru and Juja Towns and its environs |

|

5 |

Oloolaiser Water & Sewerage Co. Ltd |

Kajiado Township and its environs |

|

6 |

Kikuyu Water Company |

Kikuyu Township and its environs |

|

7 |

Karuri Water and Sanitation Company |

Karuri Township, Kiambu county and its environs |

|

8 |

Murang’ a Water and Sanitation Company |

Murang’a County |

|

9 |

Mavoko Water and Sewerage Company (MAVWASCO) |

Syokimau,Mlolongo, Athiriver, Kinanie and Chumvi |

Source: Water Services Regulatory Board

In order to meet the rising demand of water services by the growing population, the government has facilitated several water service projects. Some of the proposed projects include:

- Gatamathi And Kahuti Water Supply Project in Murang’a County,

- Ruiru-Juja / Greater Githurai Water Supply System in Kiambu County,

- Mwala Cluster & Machakos Water Supply Works in Machakos County,

- Kiserian – Ongata Rongai Water Supply System in Kajiado County.

Other projects include:

|

Completed, Ongoing & Proposed Water Water Projects |

|||||

|

No. |

Projects |

Region |

Status |

Timeline (Year) |

Value (Kshs) |

|

1 |

Eastern Transmission (Kiambu-Embakasi) Pipeline |

Kiambu/Nairobi |

Completed |

2018 |

2,012m |

|

2 |

Ruiru II Dam |

Kiambu |

Completed |

2018 |

21,391m |

|

3 |

Construction of Augmentation Works for Theta Dam |

Kiambu |

Completed |

2018 |

67m |

|

4 |

Karemenu Dam |

Kiambu |

Ongoing |

2020 |

24,000m |

|

5 |

Limuru Water Supply Project |

Nairobi |

Ongoing |

2018 |

71m |

|

6 |

Construction of the Western Transmission (Kabete-Uthiru-Karen) Pipeline |

Nairobi |

Ongoing |

2018 |

1,085m |

|

7 |

Kahuti Community Water Supply Project |

Murang'a |

Ongoing |

2018 |

63m |

|

8 |

Mavoko Water Supply Project |

Machakos |

Ongoing |

2019 |

25,000m |

|

9 |

Extension of 250mm diameter mainline from Kenol to Makuyu |

Murang'a |

Ongoing |

2018 |

125m |

|

10 |

Upgrading the sections of Kenol and Kabati |

Murang'a |

Ongoing |

2018 |

7m |

|

11 |

Construction of 315mm Diameter mainline from Wanyaga intake to Mungaria tank |

Murang'a |

Proposed |

2019 |

170m |

|

12 |

Construction of 500mm diameter main from Kinyona intake works to New Mariira Tank |

Murang'a |

Proposed |

2021 |

500m |

Source: Athi Water Services Board

d. Sewerage

Sewerage connectivity in the Nairobi Metropolitan area and nationally still remains poor, with statistics from the World Health Organization showing that only 3% of Kenya's population had a sewer line connection by 2016. Nairobi City currently has 162.7Km of sewer lines covering its area of 695 SQKM. The existing sewer infrastructure in Nairobi serves areas such as Kilimani, Kileleshwa, and the CBD, leaving a majority of the city residents who live in low-end areas such as in the informal settlements with no access to sewer lines.

The situation is similar in other parts of the metropolitan area, with Kiambu County having only 11km of sewer line serving its total area of 2,543.4 SQKM, while Mavoko sub-county currently has only 31.1km of sewer lines serving its 963 SQKM total jurisdiction. Kajiado County also suffers from the same predicament, with none of its towns having sewerage connections, a situation that in September 2018 led residents of Kitengela to unveil plans to build their own sewer line. In Murang’a County, only Murang’a town has access to a sewer, with other towns such as Kangema, Kenol and Maragua lacking sewer connectivity.

A comparison of sewerage coverage according to counties in the Nairobi Metropolitan Area is as shown below;

|

Sewerage Coverage in Nairobi Metropolitan Area |

|

|

County |

Sewer Coverage (%) |

|

Nairobi |

50% |

|

Machakos |

17% |

|

Kiambu |

15% |

|

Murang’a |

3% |

|

Kajiado |

0% |

|

Average |

17% |

Source: Water Services Regulatory Board

Due to the inadequate sewer coverage, majority of residents rely on septic tanks and other forms of improved sanitation such as pit latrines and bio-digesters.

With the growing population, and urbanization particularly in satellite towns in Kiambu, Machakos and Kajiado Counties, concerted efforts have been made to improve sewer connectivity, with various projects being initiated mainly by the Athi Water and Sewerage Services Board.

|

Ongoing & Proposed Sewerage Projects in Nairobi Metropolitan Area |

||||||

|

Project |

County |

Areas of coverage |

Length(km) |

Value Kshs ‘Mn’ |

Tender Award Date |

|

|

Kikuyu water & sewerage project |

Kiambu |

Kikuyu, Waithaka |

45.0 |

635 |

15th Aug 2018 |

|

|

River Kibarage trunk sewer |

Nairobi/Kiambu |

|

0.9 |

73 |

16th Feb 2018 |

|

|

Ruiru |

Kiambu |

Wembley, Gitambaya, Ruiru town, Muthura, Gatongora and Kiwanja |

56.0 |

280 |

8th Feb 2018 |

|

|

Enhancement of Nairobi, Gitathuru, Ngong and Mathare River |

Nairobi/Kajiado/ Kiambu |

|

0.9 |

77 |

16th Feb 2018 |

|

|

Kiambu and Ruaka* |

Kiambu |

Ruaka, Ndenderu, Muchatha, Kirigiti, Thindigua, Kiamumbi |

53.0 |

|

|

|

|

Kiserian sewerage project |

kajiado |

|

2.0 |

709 |

17th Nov 2014 |

|

|

Ruai Outfall Trunk Sewer |

Kiambu |

Ruai, Dandora, Githurai, Mwiki |

9.0 |

|||

|

Gatharaini North Trunk Sewer* |

Kiambu |

Muiruri Estate, Gatharani North, Mwiki |

9.3 |

|||

|

Gatharaini South Trunk Sewer* |

Kiambu |

Kasarani Stadium area, ICIPE, Safari Park, Thome Estate |

8.2 |

|||

|

Clay Works Trunk Sewer* |

Kiambu |

Allsops, KBL, Garden Estate, Ridgeways |

3.0 |

|||

|

Ruaraka Trunk Sewer* |

Nairobi/Kiambu |

|

3.3 |

|||

|

Machakos Sewer line |

Machakos |

Machakos |

60.0 |

Yet to be awarded |

||

|

Muranga Sewer |

Muranga |

Kenol, Maragua, Kiriaini, Kangema and Kangari |

|

4000 |

Yet to be awarded |

|

|

*Value of project to be established |

|

|||||

Source: Athi Water Services Board

A summary of the ongoing and planned projects per county is as below, with Kiambu and Machakos Counties having the largest share of proposed sewer projects at 65.5% and 23.9%, respectively;

|

Ongoing and Planned sewerage projects in Nairobi Metropolitan area |

||

|

County |

Length (Km) |

Percentage of sewer Coverage |

|

Kiambu |

164.2 |

65.5% |

|

Machakos |

60.0 |

23.9% |

|

Nairobi |

24.4 |

9.7% |

|

Kajiado |

2.0 |

0.8% |

|

Muranga* |

0.0 |

0.0% |

|

Total |

250.6 |

100% |

|

*Length of sewer line to be confirmed |

||

Source: Water Services Regulatory Board

Kiambu County has the largest share of proposed sewer projects at 65.5% attributable to the low sewer connectivity in the area coupled with the high population growth in its fast-growing towns such as Ruaka, Ruiru and Kikuyu, thus necessitating an improvement in sewer connectivity.

Generally, the Nairobi Metropolitan Area is continuously expanding and the population growing, thus the need to improve the sewerage system. The ongoing and planned sewerage systems, apart from improving sanitation and hygiene, are expected to reduce construction costs for developers as they eliminate need for septic tanks, bio digesters and other forms of sanitation.

e. Electricity

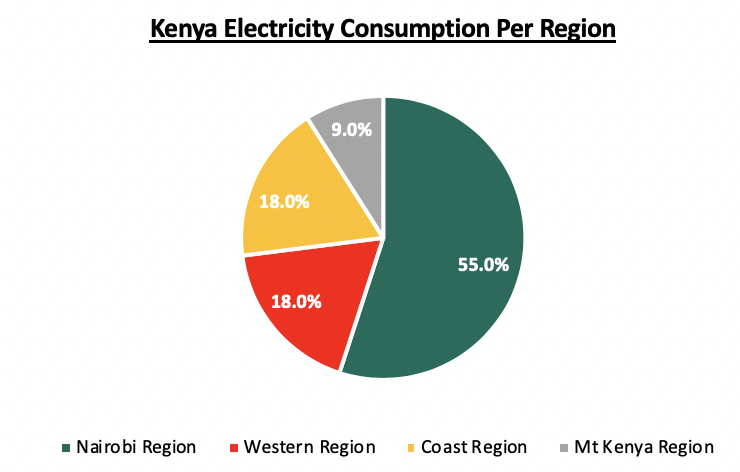

According to the Kenya Power Financial Report 2017, the Nairobi Metropolitan Area consumes more than 50.0% of Kenya’s electricity supply. This is largely a result of the industrial nature of the capital city with majority of Kenya’s manufacturing industries based in Nairobi in areas such as the Industrial Area and along Mombasa Road, and its satellite towns such as Ruiru and Thika. Furthermore, in addition to being the main commercial hub in Kenya, Nairobi is regarded as one of the key regional hubs in the continent, and thus it hosts several local and international firms. Key business nodes include Upperhill, Central Business District, Westlands and Kilimani areas. According to Kenya Power, Nairobi Region that includes Nairobi, Kiambu, Machakos, Makueni and Kajiado, recorded the highest electricity consumption in 2017, accounting for 55.0% of the total Kenya Power purchases.

Source: Kenya Power

The Kenya Power and Lighting Company Limited (KPLC) is the sole distributor and transmitter of electricity in Kenya while KETRACO (Kenya Electricity Transmission Company) is the authority responsible for design, operating and maintenance of transmission lines and power stations. While the government is the main controller of the aforementioned companies, we have seen increased involvement of the private sector in the production of electricity.

The key firms that undertake generation of electricity include:

- Kenya Electricity Generating Company Limited (KenGen),

- Independent Power Producers (IPPs) such as IberAfrica, Or-power4 Inc., Imenti, Thika Power, Golf Power, Triumph Generating Company, and Gikira Small Hydro,

- External sources such as Uganda Electricity Transmission Company Limited (UETCL) and Tanzania Electric Supply Company Limited (TANESCO).

Electricity Access

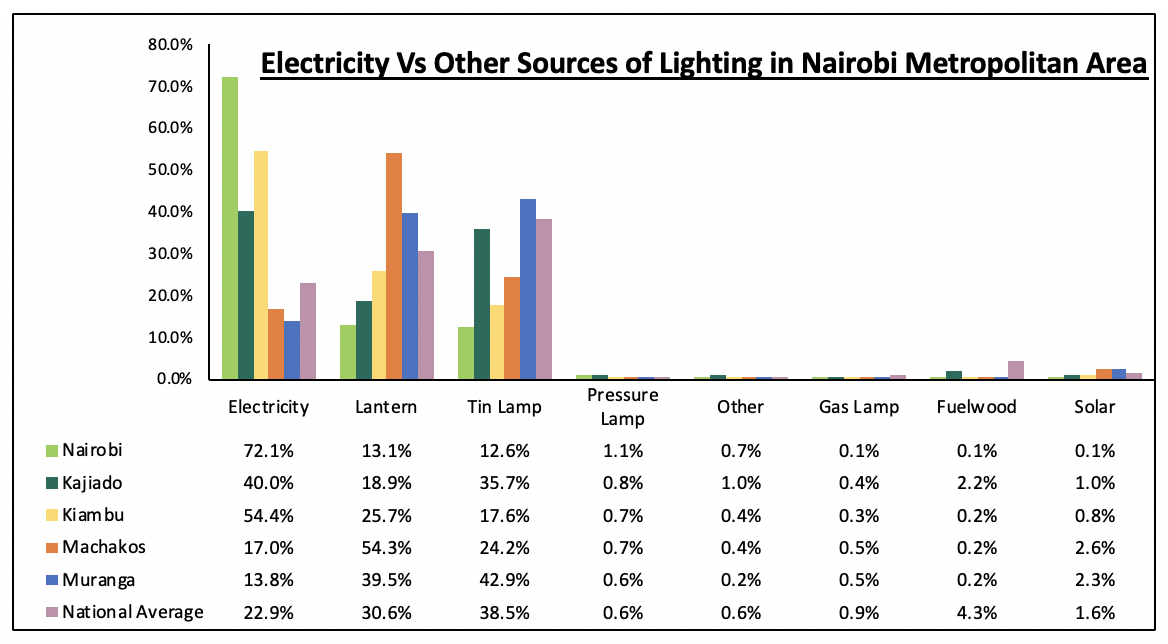

According to a KNBS and SID International’s National Inequality Survey carried out in 2013, 39.5% of Nairobi Metropolitan Area residents use electricity as a source of lighting, in comparison to the national average of 22.3%. Nairobi County had the highest access to electricity with 72.1% of the population relying on the utility for lighting in comparison to other counties such as Murang’a, which had the least electricity penetration of 13.8%.

Source: KNBS/SID International

Key to note, however, is that electricity penetration has significantly improved over the past five years. According to Kenya Power, the number of customers was 6.5 mn as at March 2018 compared to 2.3 mn customers in March 2013, a 5-year CAGR of 23.6%. This represents an electricity access rate of 72.6%, which is a 50.3% points’ growth from the 22.3% recorded in 2013. This has been achievable through the rigorous efforts to improve electricity access to Kenya as a whole.

In line with its economic development strategies, the government has embarked on various programs aimed at promoting electricity access and they include:

- Least Cost Power Development Plan: The aim is to guide energy sector stakeholders on how to meet the energy needs of the nation for subsistence and development at least cost to the economy and the environment,

- Last Mile Project: The aim is to increase electricity access to Kenyans and is implemented by the Kenya Power. Under this project, the entity will maximize the utilization of the 40,000 existing distribution transformers spread across the country as well as installation of new transformers, while Rural Electrification Authority will focus on expansion of the low voltage network lines to improve reticulation in rural areas,

- Kenya Electricity Expansion Project (KEEP): The aim is to enhance the electricity network, establish new primary substations and upgrade works on existing ones in identified locations countrywide,

- Global Partnership for Output Based Aid project: The partnership between the Government of Kenya and the World Bank aims at providing safe, legal and quality power supply to people living in informal settlements at subsidized costs,

- Nairobi City Centre Network Upgrade and Reinforcement Project: The government aims at improving the quality of power supplied in the city and its environs. In line with this, earlier this year, the President of Kenya launched the Nairobi City Centre 220/66kV Gas Insulated station (GIS) sub-station that is set to boost the county’s Bulk Power supply system. The Kshs 13.0 bn project serves the Industrial Area, Mombasa Road, Upperhill, Central Business District, and Kilimani areas; providing industries and investors with reliable and uninterrupted power supply.

In response to the high demand for electricity, the government has also put in place other projects, with most pending financing partners. According to the KPLC Grid Plan for 2016 - 2021, there are Kshs 201.7 bn worth of planned transmission projects with a due date of 2021, where 30.8% of these, worth Kshs 62.0 bn, will be within the Nairobi Metropolitan Area.

|

Ongoing Transmission Projects at Preparation & Financing Stage |

|||||

|

Planned Projects |

Project Details |

Cost (Kshs) |

|||

|

Ngong - Magadi |

84km, 132KV double circuit transmission line, |

2.3 bn |

|||

|

Silali/Baringo - Rongai |

180km 400kV double circuit line |

6.6 bn |

|||

|

Menengai - Rongai |

33km 400V double circuit line |

3.5 bn |

|||

|

Uplands (Limuru) substation |

132/33KV Substation |

0.8 bn |

|||

|

Kamburu – Embu - Thika |

196km 220kV Line, with one substation in Thika |

6.8 bn |

|||

|

Gilgil – Thika – Nairobi East - Konza |

205km 400kV double circuit line, with substations in, Thika and Kangundo |

10.3 bn |

|||

|

Isinya - Konza |

45km 400kV double circuit line, with substation in Konza |

4.7 bn |

|||

|

Murang'a |

33/11kv Primary Substation in Murang’a |

454,545 |

|||

|

Konza-Nairobi East |

52km, 400kV double circuit line |

5.2 bn |

|||

|

Nairobi Ring |

220 KV Ring around Nairobi Metropolitan Area |

20.0 bn |

|||

|

Suswa - Ngong |

40km, 220kV double circuit line |

1.9 bn |

|||

|

Total |

62.0 bn |

||||

Source: Kenya Power

With these projects, the government aims to achieve universal electricity connectivity as part of the Millennium Development Goals, while also enabling the economic plans such as the Government’s Big 4 Agenda on housing and manufacturing.

f. Airports

The Nairobi Metropolitan Area is mainly served by two major airports, the Jomo Kenyatta International Airport (JKIA), located along Mombasa Road, with a capacity of 7.5 mn passengers annually and 43 aircraft, and the Wilson Airport, located along Lang’ata Road, and has a capacity of approximately 120,000 passengers and 33 small-scale aircraft. However, the region also boasts of other airstrips which mainly serve specific entities as shown below:

|

Other Airports/Airstrips Within Nairobi Metropolitan Area |

|

|

Name |

Serves: |

|

Amboseli Airport |

Amboseli National Park |

|

Ol Kiombo Airstrip |

Maasai Mara |

|

Musiara Airstrip |

Maasai Mara |

|

Kichwa Tembo |

Maasai Mara |

|

Orly/Olooitikoshi Airport |

Kajiado County |

|

Keerok Airport |

Keerok lodge and environs |

|

Moi Airbase/Eastleigh Airport |

Kenya Air Force |

|

Mara Serena Airstrip |

Maasai Mara-Lewa Downs/Nanyuki/Samburu |

Source: Online Sources

The Kenya Airports Authority oversees the aviation infrastructure whereas the Kenya Civil Aviation Authority is mandated to regulate and operate the aviation system.

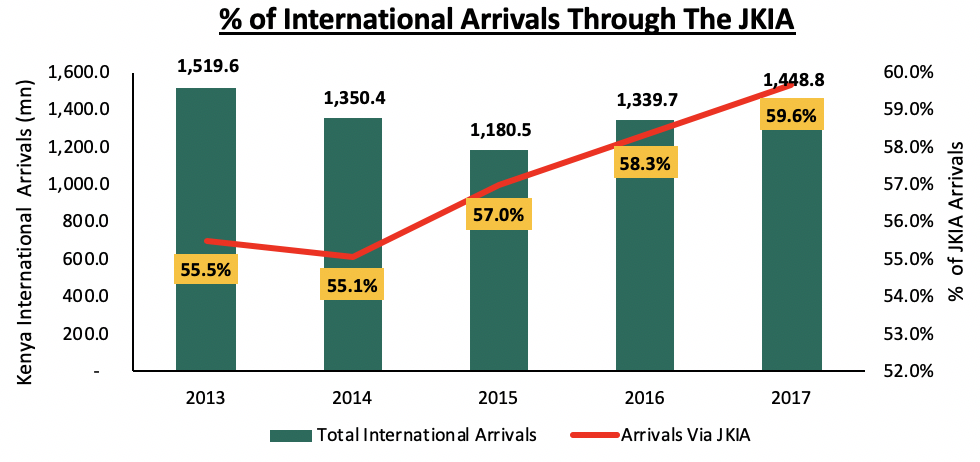

Wilson Airport, a domestic flights airport, serves local airlines such as Fly-SAX, Silverstone, Safarilinks, and AirKenya Express with destinations served from the Airport including Maasai Mara, Mombasa, Amboseli, Lamu, Kilimanjaro Diani, Lokichogio and Nanyuki. On the other hand, JKIA is vital to Kenya’s economy due to its significant contribution to the nation’s tourism and hotel industry, as more than 50.0% of the country’s international arrivals arrive through the busy airport. In 2017, 59.6% of international arrivals to Kenya passed through the JKIA, and this trend is set to continue, especially given the ongoing infrastructural developments at the airport meant to enhance its capacity and efficiency.

Source: KNBS

Planned Developments

Various improvements have seen the Jomo Kenyatta International Airport increase in size and capacity over the years to become the largest and busiest airport in East and Central Africa, and one of the most renowned in Africa. According to online sources, the airport is set for an expansion from the current 25,662 SQM to approximately 55,222 SQM, with the government’s planned expansion strategy - the JKIA Airfield Expansion Project - which was set to commence in 2018 (although it is still in the planning stage) at a cost of Kshs 22.0 bn. This will see the airport’s terminals increased as well as construction of a second runway.

The presence of an international standards airport, the Jomo Kenyatta International Airport, boosts Nairobi’s status as a regional hub thus contributing to its economic growth. The airport currently operates approximately 43 passenger airlines and 25 cargo airlines. (Currently, there are no expansion plans for Wilson Airport)

The expansion plans for JKIA are set to increase the airport’s passenger capacity by a 15-year CAGR of 10.4% from 5.5 mn in 2010 to 24.2 mn in 2025.

|

JKIA Passenger Traffic |

||||||||

|

Year |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2020 F |

2025 F |

|

Number of Passengers |

5,480,188 |

6,849,035 |

8,247,618 |

8,914,851 |

9,518,627 |

10,519,835 |

16,606,754 |

24,246,405 |

|

% Increase |

|

25.0% |

20.4% |

8.1% |

6.8% |

10.5% |

57.9% |

46.0% |

|

· Key to note, however, is that despite the projections, JKIA has not quite met its target as it currently has a capacity of 7.5 mn compared to the projected 12.0 mn |

||||||||

Source: KAA

III. Impact of Infrastructure on Real Estate

Infrastructural development plays a key role in the development of the economy as a whole through enhancing connectivity and the creation of a better operating environment for individuals and businesses alike. We look at the impact of infrastructure on the real estate sector, particularly in the Nairobi Metropolitan Area;

A. Increased Real Estate Development Projects

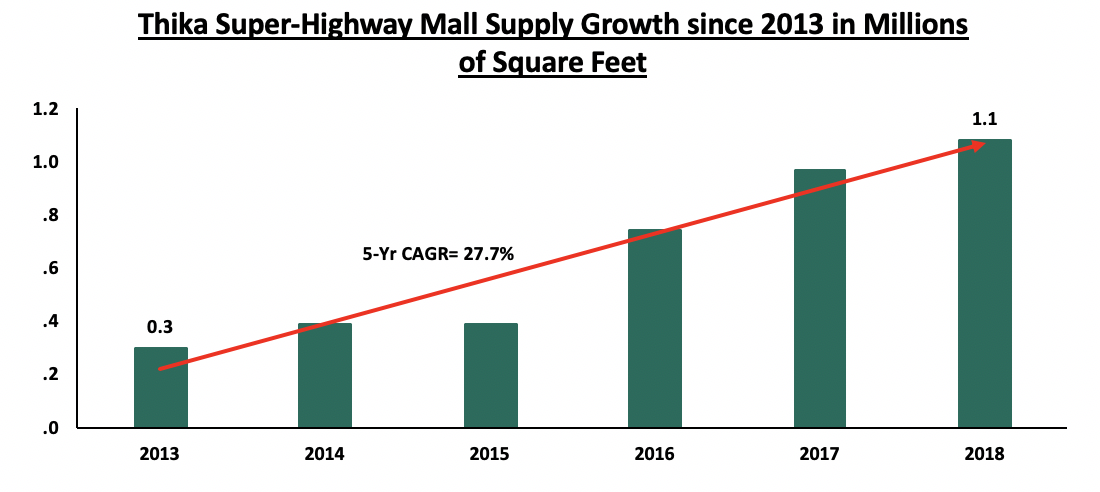

Infrastructural development opens up previously inaccessible areas and improves connectivity thus making areas more attractive for investment. The completion of the Thika Super-highway in 2012, for instance, led to an influx of residential and commercial developments in areas such as Kasarani, Thika, Ruiru and Juja. Since then we have seen the springing up of several shopping malls as real estate investors and retailers sought to tap into a growing middle class around the area. From our analysis, through the development of malls such as the Garden City, the Thika Road Mall and Juja City Mall, the mall supply along the Thika Superhighway has grown at a CAGR of 27.7% from 0.3-mn sqft in 2013 to 1.3 mn sqft as at 2018.

Source: Cytonn Research

Similar effects have also been witnessed elsewhere, with the construction of the Northern Bypass opening up areas such as Ruaka, Marurui and Membley, leading to sprouting of several residential projects and key commercial developments such as the 0.7 mn SQFT Two Rivers Mall along the route.

B. Increased Value of Properties

Investment in infrastructure results in increased demand for property, which then causes an increase in property prices. Completion of the Thika Superhighway led to opening up of areas such as Thika Town, Juja and Ruiru, leading to significant increases in land prices. For instance, Juja experienced an increase in land prices from Kshs 3.0 mn per acre in 2011 to Kshs 9.0 mn in 2016, attributable to the improved accessibility into the area facilitated by the highway. With the completion of the Northern Bypass, land prices in Ruaka appreciated by 15.7% from an average of Kshs 40.0 mn per acre in 2011 to Kshs 83.0 mn per acre in 2016, on account of increased demand for property in the area.

Below is an analysis of changes in land prices in areas along major roads constructed between 2009-2012 in the Nairobi Metropolitan Area;

|

Changes in Land Prices along Major Road Developments |

|||||||

|

Road Development |

Start |

Completion |

Location |

Average Price -2011(Mn) |

Average Price-2014 (Mn) |

Average Price-2016 (Mn) |

Price Appreciation (5-year CAGR) |

|

Thika Superhighway |

2009 |

2012 |

Juja |

3 |

7 |

9 |

24.6% |

|

Ruiru |

7 |

15 |

19 |

22.1% |

|||

|

Thika |

5 |

7 |

8 |

9.9% |

|||

|

Kasarani |

32 |

51 |

60 |

13.4% |

|||

|

Kahawa |

33 |

51 |

60 |

12.7% |

|||

|

Muthaiga |

125 |

197 |

9.5% |

||||

|

Average |

|

|

|

|

|

|

15.4% |

|

Eastern Bypass |

2009 |

2012 |

Utawala |

6 |

9 |

11 |

12.9% |

|

Ruai |

8 |

12 |

13 |

10.2% |

|||

|

Ruiru |

7 |

15 |

19 |

22.1% |

|||

|

Average |

|

|

|

|

|

|

15.1% |

|

Northern Bypass |

2009 |

2012 |

Ruaka |

40 |

58 |

83 |

15.7% |

|

Ridgeways |

24 |

51 |

62 |

20.9% |

|||

|

Runda |

33 |

58 |

67 |

15.2% |

|||

|

Average |

|

|

|

|

|

|

17.3% |

|

Grand Average |

|

|

|

|

|

|

15.8% |

Source: Cytonn Research

Land in areas along major highways registered consistent price appreciation, with an average 5-Year CAGR of 15.8%, signaling increased demand for the properties as a result of infrastructural development.

Installation of sewer lines also results in increased development as it allows for densification, given that developers are then better able to sufficiently cater for the sanitation needs of the numerous families in a single facility. In Nairobi, most sewered areas such as Kilimani, Upperhill and the CBD have allowance for high-rise developments and thus attract higher property value with an average price of Kshs 510 mn per acre compared to low rise areas such as Runda, Spring Valley, Karen and Ridgeways with an average price of Kshs 85.5 mn per acre.

C. Reduced Development Costs

According a Centre for Affordable Housing Finance in Africa report, infrastructural costs in Kenya account for approximately 25.6% of construction costs. By providing infrastructure, therefore, the government provides an impetus for real estate developers to develop more affordable units, as the cost of construction reduces considerably. With the expected roll out of affordable housing projects in the Nairobi Metropolitan Area, in areas such as Ngara, Jogoo Road, Mavoko and Shauri Moyo, the commitment of the government to provide on-site and off-site infrastructure, will therefore act as an incentive for private developers to participate.

From the above points, it is evident that infrastructure, particularly, transport routes are vital for the growth of the real estate market. Investors are therefore likely to align their projects with infrastructural projects given the expected benefits including higher demand, price appreciation and savings on construction costs.

IV. Conclusion - Recommended Areas for Real Estate Investment

To gauge investment opportunities based on infrastructure, we looked at the key infrastructural sectors weighting them in terms of importance, as follows:

- Roads – Accessibility of an area is the most important factor in real estate, especially for homebuyers and commercial real estate investors. Thus, the county with the highest road coverage got the highest weight, and vice versa,

- Water – its reliable availability is one of the key factors that homebuyers look for when investing in a home. It is also vital for commercial activities and therefore, the more connected an area, the more reliable water supply is and thus, the higher the weight,

- Sewer Connectivity – The county with the most sewer coverage got the highest weight, and vice versa,

- Number of railway stations – This plays a significant role in pulling real estate clients as it provides an alternative means of transport to the commonly used roads. However, an area has to have a railway station for this to be effective, thus, the region with the highest number of railway stations got the highest weight,

- Proximity to airports – This is especially crucial for commercial real estate. The proximity to the Jomo Kenyatta Airport, therefore, gave more weight compared to regions that are more than 20 Km away from an airport

In terms of infrastructure supply, Nairobi County offers the best investment opportunity due to presence of relatively good coverage of all infrastructure sub-sectors, in comparison to other counties. The investment opportunity within the county is thus in areas along Ngong Road, which is currently being upgraded, such as Kilimani, Race Course, and, Karen. These areas also have relatively sufficient water and sewerage coverage while also being in close proximity to the JKIA and Wilson Airport.

The ranks are as shown below:

(The points are 0-5, with 5 being the highest and 0 the lowest)

|

Recommended Areas for Real Estate Investment 2018 |

||||||||

|

Weights: |

20% |

20% |

25% |

25% |

5% |

5% |

|

|

|

County |

Completed Roads |

Planned Roads |

Water |

Sewer Coverage |

Railway Stations |

Airport Proximity |

Total Marks |

Rank |

|

Nairobi |

5 |

5 |

5 |

5 |

5 |

5 |

5.0 |

1 |

|

Kiambu |

4 |

3 |

4 |

4 |

3 |

3 |

3.7 |

2 |

|

Machakos |

2 |

4 |

3 |

3 |

4 |

4 |

3.1 |

3 |

|

Murang’a |

3 |

2 |

2 |

1 |

0 |

1 |

1.8 |

4 |

|

Kajiado |

1 |

1 |

1 |

2 |

0 |

3 |

1.3 |

5 |

|

In summary, the best areas for investment are: · Nairobi offers the best investment opportunity due to a high paved road coverage within the county, relatively sufficient water coverage, relatively high sewer connectivity, a high number of railway stations compared to other counties, and presence of airports. In Nairobi, we recommend areas along Ngong Road, which is currently being upgraded, such as Kilimani, Upperhill, Race Course, and, Karen. These areas also have relatively sufficient water and sewerage coverage (Kilimani & Upperhill) while also having easy access to the JKIA and Wilson Airport, · This was followed by Kiambu, where the investment opportunity is in areas like Thika, Ruiru, and Kikuyu which carry majority of the county’s infrastructural projects, · For Machakos, areas to invest in are Athi River, Syokimau and Mlolongo, and areas in close proximity to the upcoming Konza due to the incoming infrastructure aimed at supporting the ICT park |

||||||||

In conclusion, the presence and quality of infrastructure, that is, transportation and utilities, is one of the most important factors influencing real estate investments, and the country’s economy as a whole. We, therefore, expect the infrastructural development to remain a top priority for the government in line with its Big Four Agenda to improve the housing deficit and scale up the manufacturing sector. However, due to the current unfavorable financial environment, we expect to see a rise in private investments into this segment of the economy as a way of bridging the financing gap, especially in the energy and road sectors, which provide a ready niche for private investors.

Disclaimer: The Cytonn Weekly is a market commentary published by Cytonn Asset Managers Limited, an Affiliate of Cytonn Investments Management Plc that is regulated by the Capital Markets Authority. However, the views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma