Kenya’s Real Estate Investment Trusts (REITs) FY’2024 Report & Cytonn #15.2025

By research team, Apr 13, 2025

Executive Summary

Fixed Income

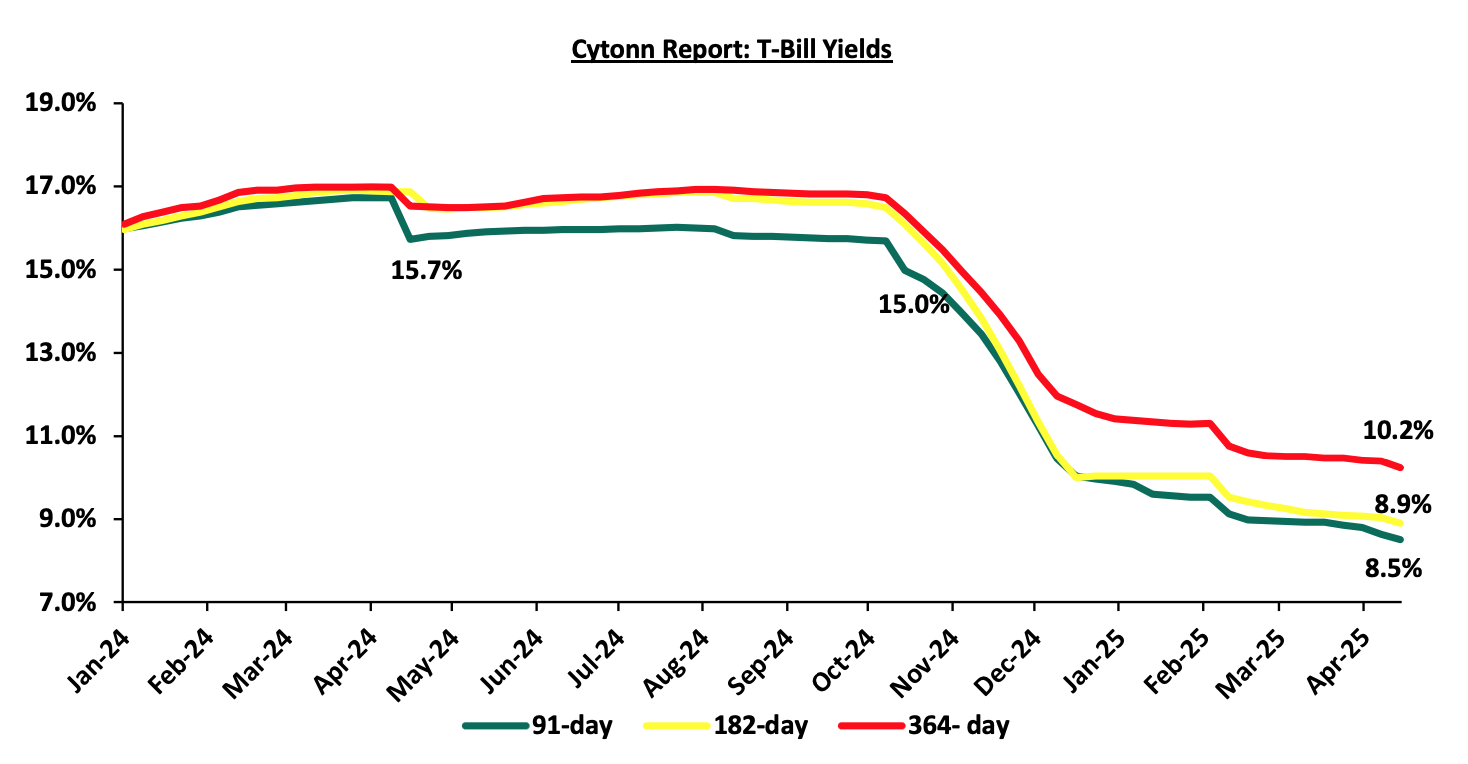

During the week, T-bills were oversubscribed for the second consecutive time, with the overall subscription rate coming in at 224.0%, an increase from the oversubscription rate of 169.5% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 17.4 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 435.4%, higher than the oversubscription rate of 279.5%, recorded the previous week. The subscription rates for the 182-day and 364-day papers increased to 110.7% and 252.7%, from the 44.9% and 250.1% recorded the previous week, respectively. The government accepted a total of Kshs 43.5 bn worth of bids out of Kshs 53.8 bn bids received, translating to an acceptance rate of 81.0%. The yields on the government papers were on a downward trajectory with the yields on the 364-day paper decreasing the most by 15.5 bps to 10.2% from 10.4% recorded the previous week. The yields on the 182-day paper decreased by 14.1 bps to 8.9% from the 9.0% recorded the previous week, while the 91-day paper decreased by 12.9 bps to 8.5% from the 8.6% recorded the previous week;

During the week, the Central Bank of Kenya (CBK) released the auction results for the FXD1/2020/15 Tap Sale with a tenor to maturity of 9.8 years. The bond was oversubscribed with the overall subscription rate coming in at 132.4%, receiving bids worth Kshs 13.2 bn against the offered Kshs 10.0 bn. The government accepted bids worth Kshs 12.6 bn, translating to an acceptance rate of 95.1%. The weighted average yield of accepted bids came in at 13.7%, equal to the rate recorded for the reopened bond last week, while the coupon rate for the bond was fixed at 12.8%. With the Inflation rate at 3.6% as of March 2025, the real return of the bonds is 10.1%;

During the week, The monetary policy committee met on April 8th, 2025, to review the outcome of its previous policy decisions against a backdrop of elevated uncertainties to the global outlook for growth, lower but sticky inflation in advanced economies, heightened trade tensions as well as persistent geopolitical tensions. The MPC decided to lower the CBR rate by 75.0 bps to 10.00%, from 10.75% in February 2025 which was in line with our expectation for the MPC to lower the CBR rate to within a range of 10.00%-10.50%;

Equities

During the week, the equities market was on a downward trajectory, with NSE 10 declining the most by 3.9% while NASI, NSE 25 and NSE 20 lost by 3.6%, 3.3% and 2.6% respectively, taking the YTD performance to gains of 5.2% and 1.1% for NSE 20 and NASI respectively, and losses of 2.7% and 1.1% for NSE 10 and NSE 25, respectively. The equities market performance was driven by losses recorded by large-cap stocks such as DTB-K, Absa and Safaricom of 6.3%, 5.8%, and 5.4%, respectively. The performance was however supported by gains recorded by large cap stocks such as Stanbic of 0.2%;

During the week, Sanlam Kenya’s Board of Directors announced commencement of Sanlam Kenya PLC’s rights issue following prior clearance by the shareholders, the Capital Markets Authority (CMA), the Nairobi Stock Exchange (NSE) and the Insurance Regulatory Authority (IRA), paving the way for a significant capital-raising initiative aimed at lowering the company’s outstanding long-term debt and to offer management operational and financial flexibility to support the company’s growth and return to profitability. Sanlam Kenya’s rights issue involves the issuance of up to 500.0 mn new ordinary shares, priced at Kshs 5.0 each;

During the week, the East African Securities Exchanges Association (EASEA) launched the East Africa Exchanges (EAE) 20 Share Index. The EAE 20 Share Index comprises of the top 20 listed companies in Kenya, Tanzania, Uganda and Rwanda securities exchanges;

Real Estate

During the week, Gulf Cap Real Estate launched a Kshs 20.0 bn housing project in Nairobi, aiming to address Kenya’s acute housing shortage by delivering mid- and low-cost units. This initiative, underscores the developer’s commitment to easing the country’s estimated 2.0 mn-unit housing deficit, which grows by 250,000 units annually against a supply of just 50,000. The project comprises two key developments—InCity Suites and Starehe Point located in Starehe constituency, Nairobi—both designed to provide affordable homes in the residential market.

During the week, KCB Bank and Mi Vida Homes entered a partnership to accelerate the development of eco-friendly, affordable housing in Kenya. This collaboration supports the government’s Affordable Housing Programme, which aims to deliver 250,000 units annually to bridge the country’s significant housing deficit. Under the agreement, KCB will provide construction financing for Mi Vida’s projects and also offer mortgage loans to buyers, aiming to make homeownership more accessible. Mi Vida plans to develop 5,000 homes over the next five years, focusing on well-planned, sustainable communities.

During the week, Hotel Chain Development Pipeline in Africa 2025 report noted that Kenya’s hospitality sector is undergoing a major transformation, with new hotel developments increasingly moving away from Nairobi and into upcountry regions. Nearly half of the hotel rooms currently under construction in the country are now located outside the capital, up from just over a quarter the previous year. Out of the 4,344 rooms being developed across 26 hotels, 2,038 are in towns and cities outside Nairobi, which now only accounts for 2,306 rooms.

On the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 25.4 and Kshs 22.2 per unit, respectively, as per the last updated data on 4th April 2025. The performance represented a 27.0% and 11.0% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. Additionally, ILAM Fahari I-REIT traded at Kshs 11.0 per share as of 4th April 2025, representing a 45.0% loss from the Kshs 20.0 inception price;

Focus of the Week

Following the release of the FY’2024 results by all four authorized Real Estate Investment Trusts (REITs) in Kenya, the Cytonn Real Estate Research Team undertook an analysis of the financial performance of the REITs and identified the key factors that shaped the performance of the sector. The report will discuss the background and structure of REITs in Kenya, and assess the financial performance of the current REITs in the market during FY’2024 in terms of operational metrics, profitability metrics, leverage ratios, liquidity ratios and valuation metrics;

Investment Updates:

- Weekly Rates: Cytonn Money Market Fund closed the week at a yield of 15.02 % p.a. To invest, dial *809# or download the Cytonn App from Google Play store here or from the Appstore here;

- We continue to offer Wealth Management Training every Tuesday, from 7:00 pm to 8:00 pm. The training aims to grow financial literacy among the general public. To register for any of our Wealth Management Trainings, click here;

- If interested in our Private Wealth Management Training for your employees or investment group, please get in touch with us through wmt@cytonn.com;

- Cytonn Insurance Agency acts as an intermediary for those looking to secure their assets and loved ones’ future through insurance namely; Motor, Medical, Life, Property, WIBA, Credit and Fire and Burglary insurance covers. For assistance, get in touch with us through insuranceagency@cytonn.com;

- Cytonn Asset Managers Limited (CAML) continues to offer pension products to meet the needs of both individual clients who want to save for their retirement during their working years and Institutional clients that want to contribute on behalf of their employees to help them build their retirement pot. To more about our pension schemes, kindly get in touch with us through pensions@cytonn.com;

Hospitality Updates:

- We currently have promotions for Staycations. Visit cysuites.com/offers for details or email us at sales@cysuites.com;

Money Markets, T-Bills Primary Auction:

During the week, T-bills were oversubscribed for the second consecutive time, with the overall subscription rate coming in at 224.0%, an increase from the oversubscription rate of 169.5% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 17.4 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 435.4%, higher than the oversubscription rate of 279.5%, recorded the previous week. The subscription rates for the 182-day and 364-day papers increased to 110.7% and 252.7%, from the 44.9% and 250.1% recorded the previous week, respectively. The government accepted a total of Kshs 43.5 bn worth of bids out of Kshs 53.8 bn bids received, translating to an acceptance rate of 81.0%. The yields on the government papers were on a downward trajectory with the yields on the 364-day paper decreasing the most by 15.5 bps to 10.2% from 10.4% recorded the previous week. The yields on the 182-day paper decreased by 14.1 bps to 8.9% from the 9.0% recorded the previous week, while the 91-day paper decreased by 12.9 bps to 8.5% from the 8.6% recorded the previous week.

The charts below show the yield performance of the 91-day, 182-day and 364-day papers from January 2024 to April 2025:

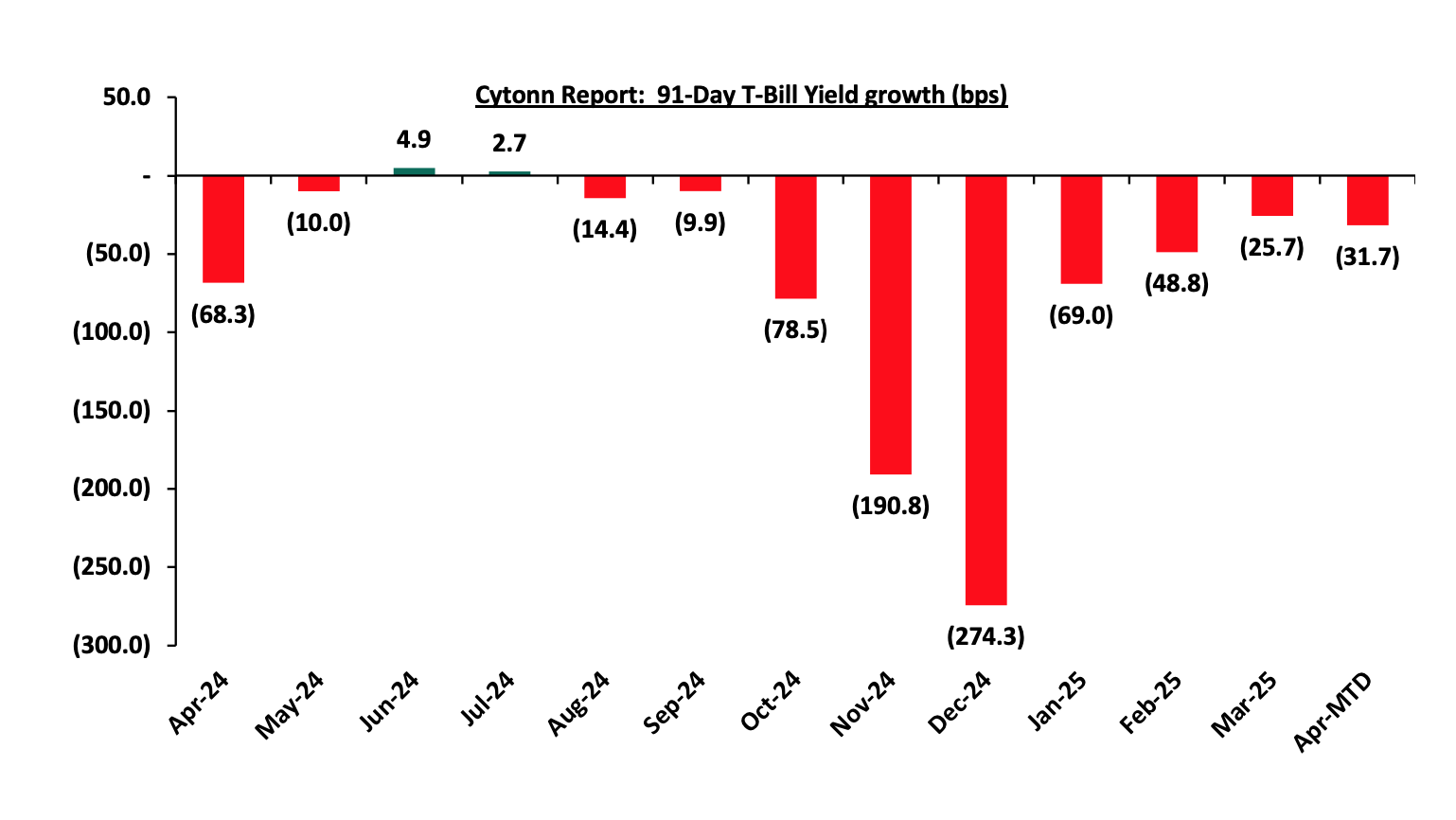

The chart below shows the yield growth for the 91-day T-bill:

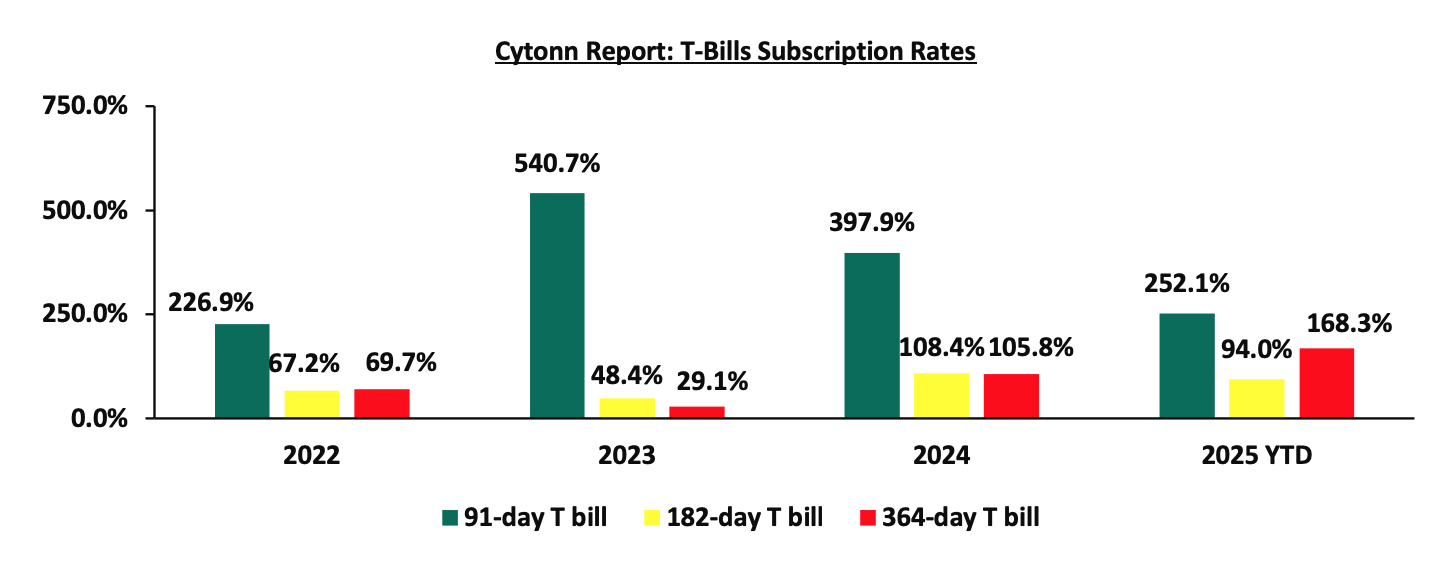

The chart below compares the overall average T-bill subscription rates obtained in 2022,2023, 2024 and 2025 Year-to-date (YTD):

In the primary bond market, the Central Bank of Kenya (CBK) released the auction results for the FXD1/2020/15 Tap Sale with a tenor to maturity of 9.8 years. The bond was oversubscribed with the overall subscription rate coming in at 132.4%, receiving bids worth Kshs 13.2 bn against the offered Kshs 10.0 bn. The government accepted bids worth Kshs 12.6 bn, translating to an acceptance rate of 95.1%. The weighted average yield of accepted bids came in at 13.7%, equal to the rate recorded for the reopened bond last week, while the coupon rate for the bond was fixed at 12.8%. With the Inflation rate at 3.6% as of March 2025, the real return of the bonds is 10.1%

Money Market Performance:

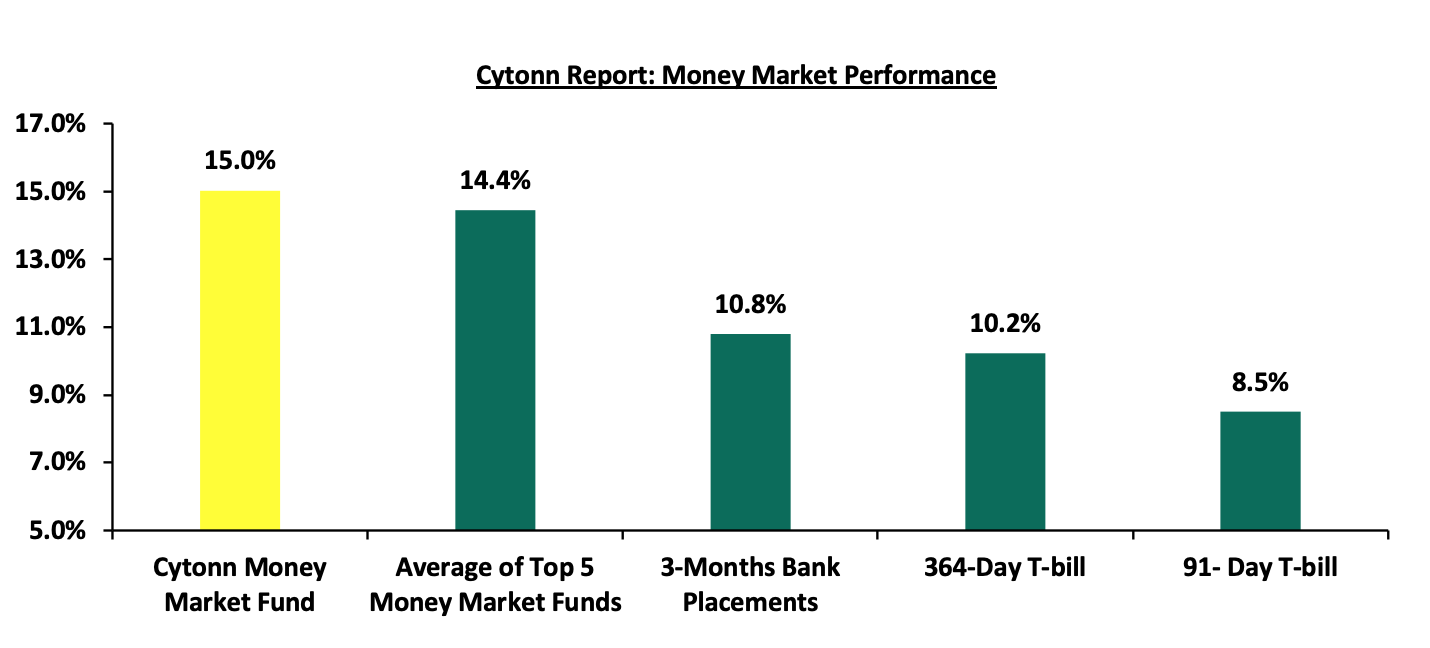

In the money markets, 3-month bank placements ended the week at 10.8% (based on what we have been offered by various banks). The yield on the Cytonn Money Market Fund increased by 12.0 bps to 15.0% from the 14.9% recorded the previous week, while the average yields on the Top 5 Money Market Funds decreased by 35.8 bps to close the week at 14.4%, from the 14.8% recorded the previous week.

The table below shows the Money Market Fund Yields for Kenyan Fund Managers as published on 11th April 2025:

|

Cytonn Report: Money Market Fund Yield for Fund Managers as published on 11th April 2025 |

||

|

Rank |

Fund Manager |

Effective Annual Rate |

|

1 |

Gulfcap Money Market Fund |

16.3% |

|

2 |

Cytonn Money Market Fund (Dial *809# or download the Cytonn app) |

15.0% |

|

3 |

Etica Money Market Fund |

13.9% |

|

4 |

Kuza Money Market fund |

13.7% |

|

5 |

Lofty-Corban Money Market Fund |

13.4% |

|

6 |

Orient Kasha Money Market Fund |

13.3% |

|

7 |

Ndovu Money Market Fund |

13.1% |

|

8 |

Enwealth Money Market Fund |

12.7% |

|

9 |

British-American Money Market Fund |

12.7% |

|

10 |

Old Mutual Money Market Fund |

12.4% |

|

11 |

Arvocap Money Market Fund |

12.4% |

|

12 |

Apollo Money Market Fund |

12.4% |

|

13 |

Madison Money Market Fund |

12.4% |

|

14 |

Nabo Africa Money Market Fund |

12.2% |

|

15 |

Dry Associates Money Market Fund |

11.9% |

|

16 |

Jubilee Money Market Fund |

11.8% |

|

17 |

Sanlam Money Market Fund |

11.8% |

|

18 |

Faulu Money Market Fund |

11.8% |

|

19 |

Co-op Money Market Fund |

11.7% |

|

20 |

GenAfrica Money Market Fund |

11.5% |

|

21 |

Absa Shilling Money Market Fund |

11.2% |

|

22 |

CIC Money Market Fund |

11.2% |

|

23 |

ICEA Lion Money Market Fund |

10.8% |

|

24 |

KCB Money Market Fund |

10.8% |

|

25 |

Mali Money Market Fund |

10.5% |

|

26 |

AA Kenya Shillings Fund |

10.4% |

|

27 |

Genghis Money Market Fund |

10.3% |

|

28 |

Mayfair Money Market Fund |

9.7% |

|

29 |

Stanbic Money Market Fund |

7.6% |

|

30 |

Ziidi Money Market Fund |

7.4% |

|

31 |

Equity Money Market Fund |

5.7% |

Source: Business Daily

Liquidity:

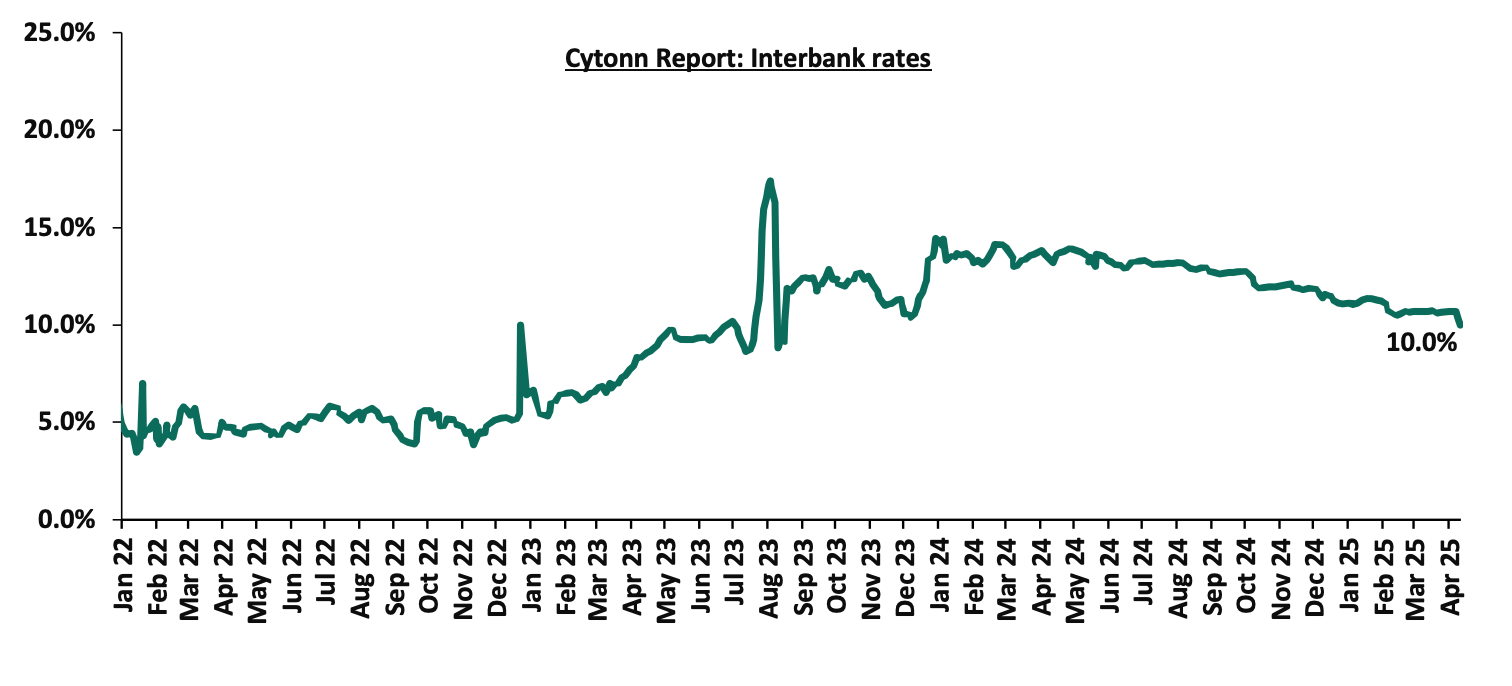

During the week, liquidity in the money markets eased, with the average interbank rate decreasing by 31.6 bps, to 10.4% from the 10.7% recorded the previous week, partly attributable to tax remittances that were offset by government payments. The average interbank volumes traded increased by 216.9% to Kshs 19.8 bn from Kshs 6.3 bn recorded the previous week. The chart below shows the interbank rates in the market over the years:

Kenya Eurobonds:

During the week, the yields on Kenya’s Eurobonds were on an upward trajectory, with the yield on the 10-year issued in 2018 increasing the most by 1.6% to 11.2% from the 9.6% recorded the previous week. The table below shows the summary performance of the Kenyan Eurobonds as of 10th April 2025;

|

Cytonn Report: Kenya Eurobonds Performance |

|

||||||

|

|

2018 |

2019 |

2021 |

2024 |

2025 |

||

|

Tenor |

10-year issue |

30-year issue |

7-year issue |

12-year issue |

13-year issue |

7-year issue |

11-year issue |

|

Amount Issued (USD) |

1.0 bn |

1.0 bn |

0.3 bn |

1.2 bn |

1.0 bn |

1.5 bn |

1.5 bn |

|

Years to Maturity |

2.9 |

22.9 |

2.1 |

7.1 |

9.2 |

5.8 |

11.0 |

|

Yields at Issue |

7.3% |

8.3% |

7.0% |

7.9% |

6.2% |

10.4% |

9.9% |

|

02-Jan-25 |

9.1% |

10.3% |

8.5% |

10.1% |

10.1% |

10.1% |

|

|

01-Apr-25 |

8.8% |

10.8% |

7.5% |

10.4% |

10.4% |

10.4% |

|

|

03-Apr-25 |

9.6% |

11.2% |

8.0% |

10.9% |

10.9% |

11.0% |

|

|

04-Apr-25 |

10.7% |

11.9% |

8.6% |

11.7% |

11.6% |

12.0% |

|

|

07-Apr-25 |

11.6% |

12.4% |

9.1% |

12.3% |

12.1% |

12.6% |

|

|

08-Apr-25 |

11.1% |

12.0% |

9.1% |

12.0% |

11.8% |

12.2% |

|

|

09-Apr-25 |

11.7% |

12.3% |

9.5% |

12.5% |

12.2% |

12.7% |

|

|

10-Apr-25 |

11.2% |

12.1% |

9.2% |

12.1% |

11.8% |

12.2% |

|

|

Weekly Change |

1.6% |

0.9% |

1.3% |

1.2% |

1.0% |

1.2% |

- |

|

MTD Change |

2.4% |

1.3% |

1.8% |

1.7% |

1.4% |

1.9% |

- |

|

YTD Change |

2.1% |

1.8% |

0.7% |

2.0% |

1.7% |

2.1% |

- |

Source: Central Bank of Kenya (CBK) and National Treasury

Kenya Shilling:

During the week, the Kenyan Shilling depreciated against the US Dollar by 36.0 bps, to Kshs 129.7 from the Kshs 129.2 recorded the previous week. On a year-to-date basis, the shilling has depreciated by 31.3 bps against the dollar, compared to the 17.4% appreciation recorded in 2024.

We expect the shilling to be supported by:

- Diaspora remittances standing at a cumulative USD 4,972.0 mn in the twelve months to March 2025, 13.5% higher than the USD 4,380.0 mn recorded over the same period in 2024. These has continued to cushion the shilling against further depreciation. In the March 2025 diaspora remittances figures, North America remained the largest source of remittances to Kenya accounting for 53.0% in the period,

- The tourism inflow receipts which came in at Kshs 452.2 bn in 2024, a 19.8% increase from Kshs 377.5 bn inflow receipts recorded in 2023, and owing to tourist arrivals that improved by 14.6% to 2,394,376 in 2024 from 2,089,259 in 2023, and,

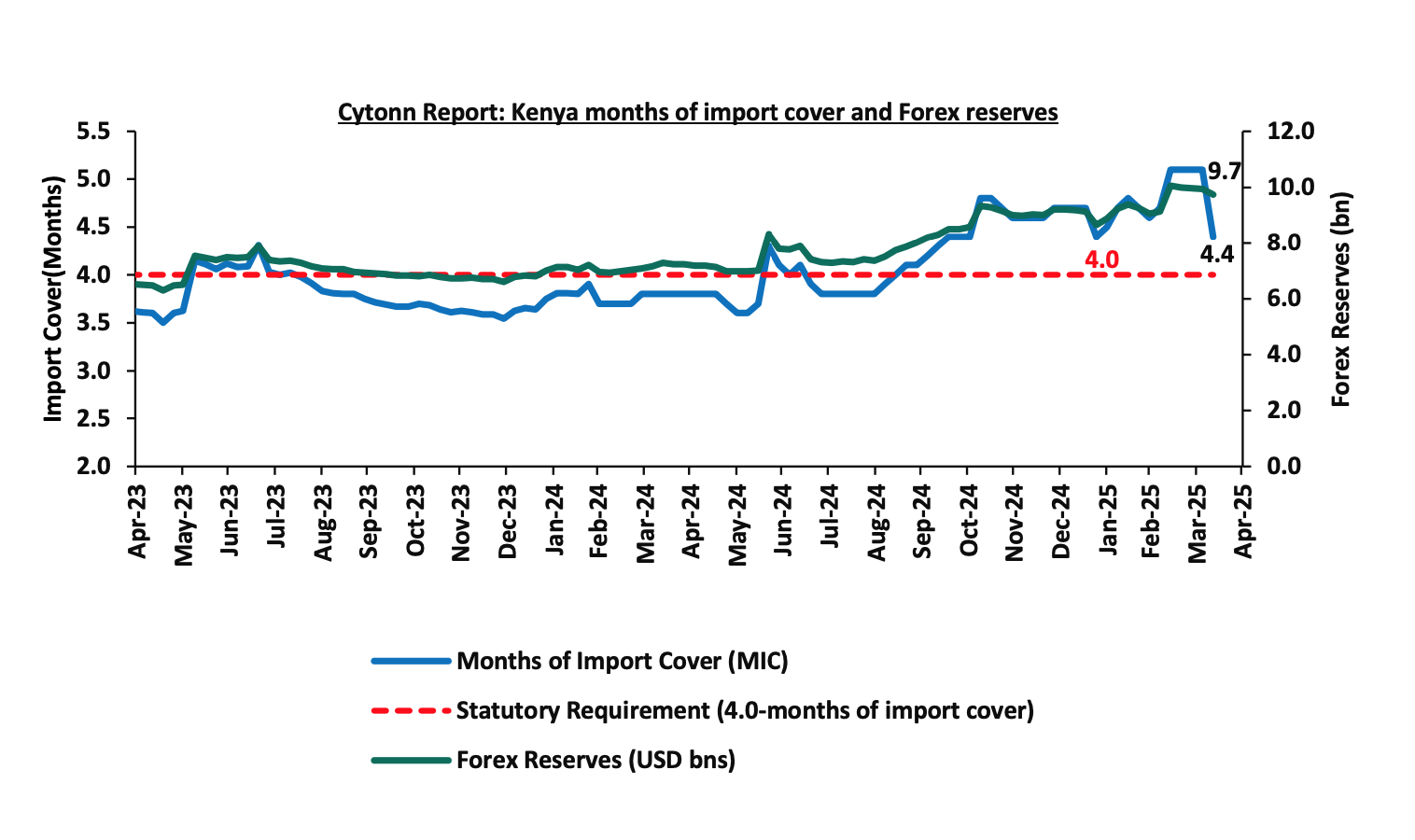

- Improved forex reserves currently at USD 9.7 bn (equivalent to 4.4-months of import cover), which is above the statutory requirement of maintaining at least 4.0-months of import cover and above the EAC region’s convergence criteria of 4.5-months of import cover.

The shilling is however expected to remain under pressure in 2025 as a result of:

- An ever-present current account deficit which came at 3.1% of GDP in the twelve months to February 2025, and,

- The need for government debt servicing, continues to put pressure on forex reserves given that 62.1% of Kenya’s external debt is US Dollar-denominated as of September 2024.

Key to note, Kenya’s forex reserves decreased by 2.1% during the week, to USD 9.7 bn from the USD 9.9 bn recorded in the previous week, equivalent to 4.4 months of import cover (based on updated import data), from the 5.1 months of import cover recorded last week, and above the statutory requirement of maintaining at least 4.0-months of import cover.

The chart below summarizes the evolution of Kenya's months of import cover over the years:

Weekly Highlights

- Monetary Policy Committee (MPC) April Meeting

The monetary policy committee met on April 8th, 2025, to review the outcome of its previous policy decisions against a backdrop of elevated uncertainties to the global outlook for growth, lower but sticky inflation in advanced economies heightened trade tensions as well as persistent geopolitical tensions. The MPC decided to lower the Central Bank Rate(CBR) by 75.0 bps to 10.00%, from 10.75% in February 2025 which was in line with our expectation for the MPC to lower the CBR rate to within a range of 10.00%-10.50%. Our expectation to cut the rate was mainly on the back of the need to support the economy by adopting an accommodative policy that will ease financing activities, rate cuts by some major economies, as well the continued stability of the Shilling against major currencies. Notably, inflation rates remain anchored and remained within the CBK preferred range of 2.5%-7.5% for the twenty first consecutive month, despite the marginal increase by 0.1% points to 3.6% in March 2025, from 3.5% in February 2025. The MPC additionally approved the narrowing of the width of the interest rate corridor around the CBR from the current ±150 basis points to ±75 basis points and in line with this the committee also approved the adjustment of the applicable interest rate on the Discount Window from the current 300.0 basis points above CBR to 75.0 basis points which will be the upper bound of the interest rate corridor. Key to note, the MPC had cut the CBR rate to 10.75% in the previous meeting in February from 11.25% in December 2024. Below are some of the key highlights from the April meeting:

- The overall inflation increased marginally by 0.1% points to 3.6% in March 2025, from 3.5% in February 2025, positioning it below the mid-point of the preferred CBK range of 2.5%-7.5%. Core inflation increased to 2.2% in March 2025, from 1.9% in February, reflecting increasing demand pressures in the economy. This increase was largely attributed to higher prices of processed food items, particularly sugar, maize, and wheat products. Conversely, non-core inflation decreased to 7.4% in March 2025, from 7.7% in February, driven by lower prices of food crops, especially vegetables, due to seasonal factors. Lower energy and utilities costs, including reduced electricity and fuel prices, continued to help moderate non-core inflation. Overall inflation is expected to stay below the mid-point of the target range in the near term, supported by low and stable core inflation, an anticipated reduction in energy prices, and a stable exchange rate.

- The performance of the Kenyan economy slowed down in 2024, with real GDP estimated at 4.6% compared to 5.6% in 2023.This was attributable to deceleration in growth in most sectors of the economy. The economy is expected to continue to strengthen in 2025 with real GDP growth projected at 5.4%, from the 4.6% growth recorded in 2024 supported by resilient services sector and agriculture, expected recovery in growth of credit to the private sector and enhanced exports. However, this positive outlook is tempered by potential domestic and external risks.

- The Kenya National Bureau of Statistics (KNBS) updated the balance of payments data to better capture cross-border transactions, especially those involving petroleum imports and re-exports under government-to-government deals. The revisions also include the use of alternative data sources to enhance accuracy in reporting international trade in services, notably travel and financial services. These adjustments refine the recording of regional oil product re-exports and international travel earnings.

- Based on the revised balance of payments data goods exports increased by 13.1% in the 12 months to February 2025, compared to 2024, reflecting a rise in exports of agricultural commodities and re-exports. Goods imports rose by 10.6% reflecting increases in intermediate and capital goods imports. The current account deficit in 12 months to February 2025 is estimated at 3.1% of GDP, down from 3.3% in similar period in 2024, driven by stronger goods exports, robust diaspora remittance inflows, and reduced oil imports The current account deficit was fully financed by capital and financial inflows, leading to an overall balance of payments surplus of USD 1,380.0 mn. This surplus resulted in a USD 665.0 mn build-up in gross reserves. For 2025, the current account deficit is projected at 2.8% of GDP and is expected to be fully financed by capital and financial inflows, yielding a balance of payments surplus of USD 1380.0 mn and an increase in gross reserves of USD 665.0 mn.

- The CBK foreign exchange reserves, which currently stand at USD 9, 930.0 representing 4.4 months of import cover (based on the revised import data), continue to provide adequate cover and a buffer against any short-term shocks in the foreign exchange market,

- The banking sector remains stable and resilient, with strong liquidity and capital adequacy ratios. The ratio of gross non-performing loans (NPLs) to gross loans increased to 17.2% in February 2025 compared to 16.4% in December 2024. Increases in NPLs were noted in the real estate, personal and household, trade, building and construction and Manufacturing sectors. Banks have continued to make adequate provisions for the NPLs,

- The CEOs Survey and Market Perceptions Survey conducted ahead of the MPC meeting revealed sustained optimism about business activity and economic growth prospects for the next 12 months. The optimism was attributed to the stable macroeconomic environment reflected in the low inflation rate and stability in the exchange rate, expectations of a decline in interest rates and favorable weather conditions supporting agriculture. Nevertheless, respondents expressed concerns about high cost of doing business and subdued consumer demand,

- The Survey of the Agriculture Sector for March 2025 revealed an expectation for moderate downward pressure on overall headline inflation in the next three months, on account of expected lower food prices particularly of vegetables and cereals prices attributed to favorable weather conditions, stability in pump prices and the stable exchange rate,

- Global economic growth showed steady recovery in 2024, driven largely by strong performance in the United States and major emerging markets, especially India. However, the outlook for 2025 is clouded by uncertainty due to rising trade tensions spurred by new U.S. import tariffs and expected retaliatory measures as well as escalating geopolitical risks, particularly ongoing conflicts in the Middle East and the Russia-Ukraine war, which continue to threaten global growth prospects,

- Global headline inflation has eased, though uncertainty persists due to the potential inflationary effects of rising import tariffs. Central banks in advanced economies have continued to cut interest rates, albeit at varied speeds based on their respective inflation and growth outlooks. International oil prices have declined amid higher production and weak demand, yet volatility risks remain elevated due to trade tensions and ongoing geopolitical conflicts. Food inflation has also eased, largely due to lower prices of cereals and sugar, although inflation in edible oil prices remains high.

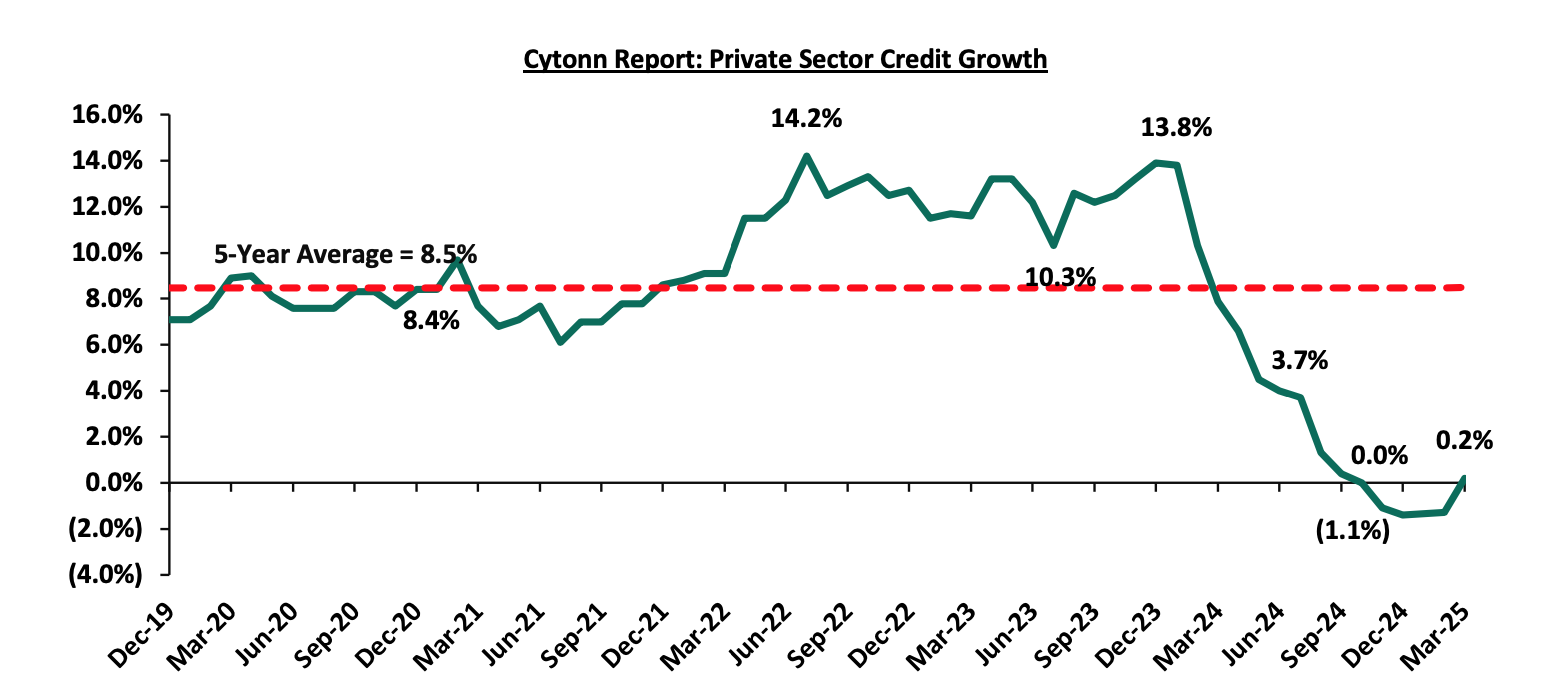

- Growth in private sector credit grew by modest 0.2% in March 2025 from a contraction of 1.3% in February, mainly attributed to the dissipation of exchange rate valuation effects on foreign currency-denominated loans due to the appreciation of the Shilling and increased demand attributable to declining lending interest rates. Average commercial banks’ lending rates declined to 15.8% in March 2025 from 16.4% in February 2025 and 17.2% in November 2024.

- The Committee acknowledged the ongoing implementation of the FY’2024/25 Supplementary Budget I and the proposed Supplementary Budget II. These measures are anticipated to further support fiscal consolidation, reducing the fiscal deficit to 5.1% of GDP in FY’2024/25, from 5.3% of GDP in FY’2023/24. The fiscal consolidation in the medium-term should reduce debt vulnerabilities while moving the present-value-of-debt to GDP ratio towards the target anchor of 55.0%.

- To strengthen the implementation of monetary policy ease, the MPC approved narrowing the interest rate corridor around the Central Bank Rate (CBR) from ±150 basis points to ±75 basis points. This adjustment aims to promote greater stability in the interbank rate and ensure it stays more closely aligned with the CBR. Additionally, the interest rate on the Discount Window was revised from 300.0 basis points above the CBR to 75.0 basis points, aligning it with the new upper limit of the interest rate corridor.

The MPC noted that overall inflation is expected to remain below the midpoint of the 2.5%-7.5% target range in the near term, supported by stable core inflation, low energy prices, and exchange rate stability. Additionally, central banks in major economies have continued to lower interest rates at varying paces. The Committee also noted that economic growth slowed in 2024, creating room for further easing of monetary policy to support economic activity while maintaining exchange rate stability. The MPC noted that it will continue to monitor the effects of these policy measures, as well as global and domestic economic developments, and will remain ready to take additional action if necessary. The next MPC meeting is scheduled for June 2025.

Rates in the Fixed Income market have been on a downward trend due to high liquidity in the money market which allowed the government to front load most of its borrowing. The government is 78.3% ahead of its prorated net domestic borrowing target of Kshs 468.1 bn, and 40.6% ahead of the total FY’2024/25 net domestic borrowing target of Kshs 593.7 bn, having a net borrowing position of Kshs 834.5 bn (inclusive of T-bills). However, we expect a continued downward readjustment of the yield curve in the short and medium term, with the government looking to increase its external borrowing to maintain the fiscal surplus, hence alleviating pressure in the domestic market. As such, we expect the yield curve to stabilize in the short to medium-term and hence investors are expected to shift towards the long-term papers to lock in the high returns

Market Performance

During the week, the equities market was on a downward trajectory, with NSE 10 declining the most by 3.9% while NASI, NSE 25 and NSE 20 lost by 3.6%, 3.3% and 2.6% respectively, taking the YTD performance to gains of 5.2% and 1.1% for NSE 20 and NASI respectively, and losses of 2.7% and 1.1% for NSE 10 and NSE 25, respectively. The equities market performance was driven by losses recorded by large-cap stocks such as DTB-K, Absa and Safaricom of 6.3%, 5.8%, and 5.4%, respectively. The performance was however supported by gains recorded by large cap stocks such as Stanbic of 0.2%.

During the week, equities turnover increased by 8.3% to USD 12.5 mn, from USD 11.5 mn recorded the previous week, taking the YTD total turnover to USD 226.6 mn. Foreign investors became net sellers for the first time in two weeks, with a net selling position of USD 3.8 mn, from a net buying position of USD 1.0 mn recorded the previous week, taking the YTD foreign net selling position to USD 28.0 mn, compared to a net selling position of USD 16.9 mn in 2024,

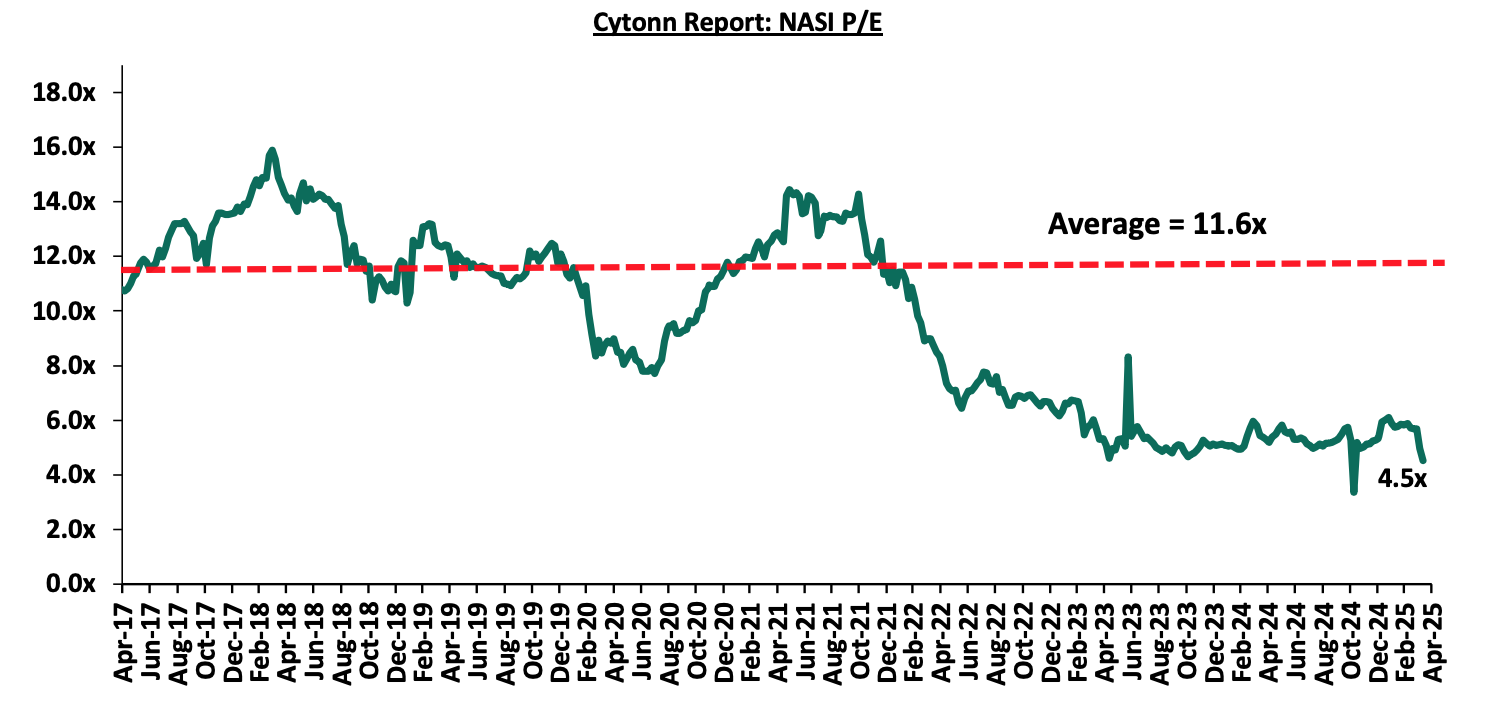

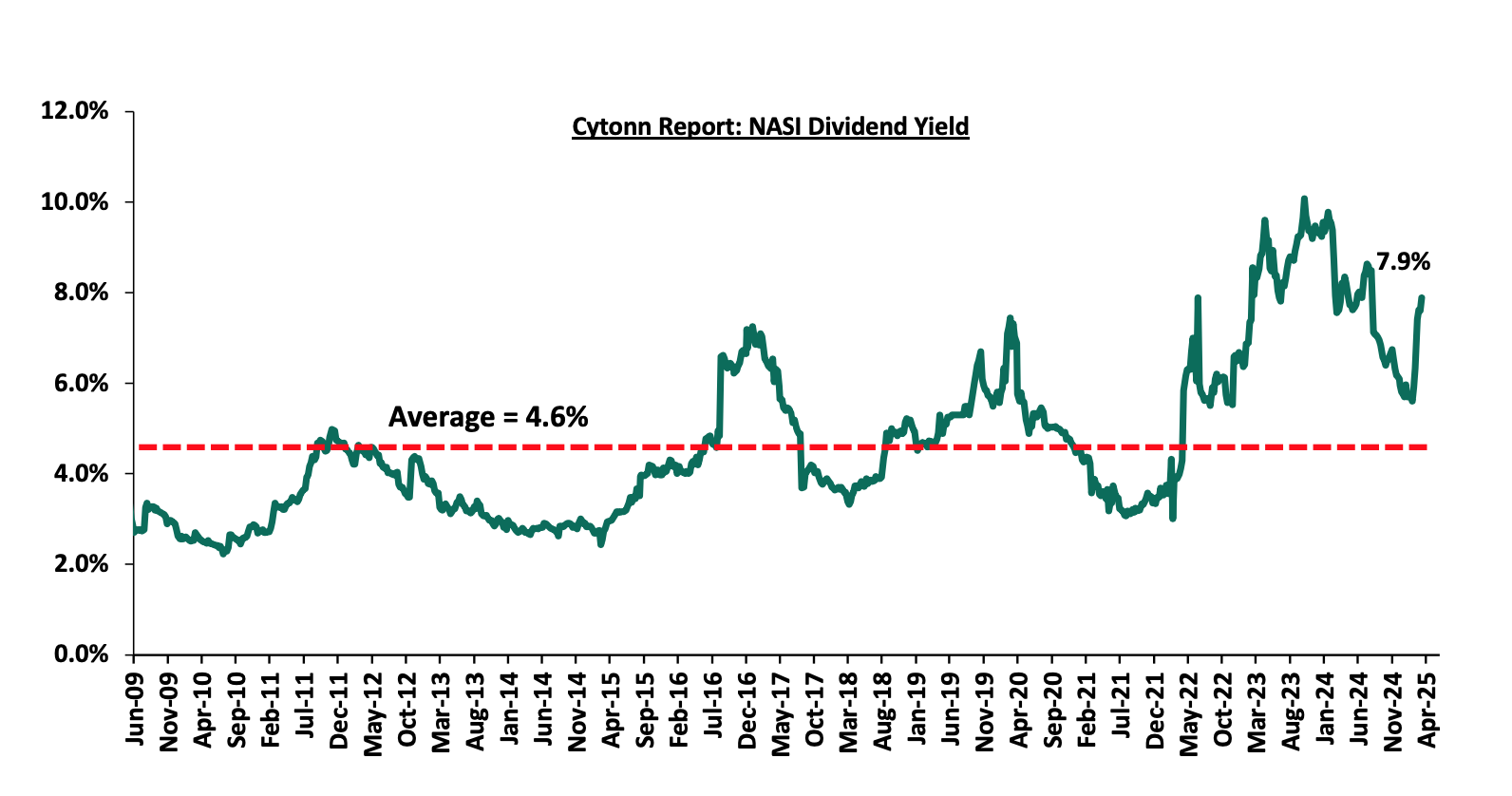

The market is currently trading at a price-to-earnings ratio (P/E) of 4.5x, 60.9% below the historical average of 11.6x. The dividend yield stands at 7.9%, 3.3% points above the historical average of 4.6%. Key to note, NASI’s PEG ratio currently stands at 0.6x, an indication that the market is undervalued relative to its future growth. A PEG ratio greater than 1.0x indicates the market is overvalued while a PEG ratio less than 1.0x indicates that the market is undervalued. The charts below indicate the historical P/E and dividend yields of the market;

Universe of Coverage:

|

Cytonn Report: Equities Universe of Coverage |

||||||||||

|

Company |

Price as at 04/04/2025 |

Price as at 11/04/2025 |

w/w change |

YTD Change |

Year Open 2025 |

Target Price* |

Dividend Yield |

Upside/ Downside** |

P/TBv Multiple |

Recommendation |

|

Equity Group |

47.1 |

44.6 |

(5.3%) |

(7.1%) |

48.0 |

60.2 |

9.5% |

44.5% |

0.9x |

Buy |

|

KCB Group |

39.8 |

38.3 |

(3.6%) |

(9.7%) |

42.4 |

50.4 |

7.8% |

39.4% |

0.4x |

Buy |

|

Co-op Bank |

16.2 |

16.0 |

(0.9%) |

(8.3%) |

17.5 |

20.3 |

9.4% |

36.1% |

0.7x |

Buy |

|

Jubilee Holdings |

210.0 |

203.3 |

(3.2%) |

16.3% |

174.8 |

260.7 |

6.6% |

34.9% |

0.3x |

Buy |

|

Diamond Trust Bank |

75.0 |

70.3 |

(6.3%) |

5.2% |

66.8 |

84.4 |

10.0% |

30.0% |

0.3x |

Buy |

|

ABSA Bank |

18.1 |

17.1 |

(5.8%) |

(9.5%) |

18.9 |

20.2 |

10.3% |

28.7% |

1.2x |

Buy |

|

Standard Chartered Bank |

300.3 |

299.0 |

(0.4%) |

4.8% |

285.3 |

328.6 |

15.1% |

24.9% |

1.7x |

Buy |

|

NCBA |

54.0 |

53.8 |

(0.5%) |

5.4% |

51.0 |

57.4 |

10.2% |

17.0% |

1.0x |

Accumulate |

|

Stanbic Holdings |

165.5 |

165.8 |

0.2% |

18.6% |

139.8 |

171.2 |

12.5% |

15.8% |

0.9x |

Accumulate |

|

Britam |

7.3 |

6.8 |

(7.1%) |

16.8% |

5.8 |

7.5 |

0.0% |

10.3% |

1.0x |

Accumulate |

|

CIC Group |

3.0 |

3.0 |

(1.0%) |

37.9% |

2.1 |

3.1 |

4.4% |

9.5% |

0.9x |

Hold |

|

I&M Group |

31.6 |

32.3 |

2.1% |

(10.4%) |

36.0 |

31.4 |

9.3% |

6.7% |

0.6x |

Hold |

|

*Target Price as per Cytonn Analyst estimates **Upside/ (Downside) is adjusted for Dividend Yield ***Dividend Yield is calculated using FY’2024 Dividends |

||||||||||

Weekly Highlights

- Commencement of Sanlam Kenya’s Rights Issue

On 3rd April, 2025, Sanlam Kenya’s Board of Directors announced commencement of Sanlam Kenya PLC’s rights issue following prior approval by the shareholders, the Capital Markets Authority (CMA), the Nairobi Stock Exchange (NSE) and the Insurance Regulatory Authority (IRA), paving the way for a significant capital-raising initiative aimed at lowering the company’s outstanding long-term debt and to offer management operational and financial flexibility to support the company’s growth and return to profitability. This move comes as part of Sanlam Kenya’s broader vision to reduce the Group’s debt to a manageable and sustainable level.

Sanlam Kenya’s rights issue involves the issuance of up to 500,000,000 new ordinary shares, priced at Kshs 5.0 each. This initiative, if fully subscribed, will generate Kshs 2.5 bn in gross proceeds.

The offer price of Kshs 5.0 per share represents a 20.9% discount on the six-month volume-weighted average share price as of April 3rd, 2025 of Kshs 6.3 per share, giving shareholders a financial incentive to participate. Eligible shareholders will be allotted 125 new shares for every 36 existing shares held on the record date. Additionally, the rights issue is fully underwritten by Sanlam’s parent company Sanlam Allianz Africa, which has agreed to buy any remaining rights that aren’t taken up by eligible shareholders after the rights issue allocation.

The proceeds from the rights issue will be directed towards several key areas aligned with Sanlam Kenya’s long-term strategy. Primarily, the Group aims to use this capital to reduce its long-term debt levels and support its return to profitability. Before the rights issue, Sanlam Kenya’s debt to equity ratio was significantly high, being the highest among peer insurance companies. Post-rights issue, Sanlam Kenya’s debt to equity will reduce by 59.3% to 7.9 from 19.4 attributable to the decline in its debt level. The table below shows the debt to equity ratio before and after the rights issue;

|

Sanlam Kenya's Leverage Ratio |

Before the rights issue |

Estimated After the rights issue |

Change (% points) |

|

Debt to Equity ratio |

19.4 |

7.9 |

(56.5%) |

Compared to peer insurance companies in Kenya, Sanlam Kenya will become sufficiently capitalized after accounting for the rights issue. The tables before show Sanlam Kenya’s debt to equity ratios compared to its peers;

|

Insurance Company |

Debt to Equity Ratio |

|

Kenya Re Insurance Corporation Ltd |

0.3 |

|

Jubilee Holdings Ltd |

3.2 |

|

Liberty Kenya Holdings Plc |

3.5 |

|

CIC Insurance Group Plc |

4.6 |

|

Britam Holdings Plc |

6.1 |

|

Sanlam Kenya Plc * |

19.4 |

|

Sanlam Kenya Plc ** |

7.9 |

*Before the rights issue

**After the rights issue

The table below summarizes the rights issue statistics;

|

Cytonn Report: Sanlam Kenya Rights Issue Summary |

|

|

Data |

Statistic |

|

Par value |

Kshs 5.0 each |

|

Offer value |

Kshs 5.0 per share |

|

Total Number of outstanding shares prior to the rights issue |

144,000,000 |

|

Number of new shares |

500,000,000 |

|

Total Number of outstanding shares after the rights issue |

644,000,000 |

|

Gross proceeds of Rights Issue assuming full subscription |

2,500,000,000 |

Source: Sanlam Kenya

As of December 31, 2024, Sanlam Kenya’s shareholder base included several key investors, with Hubris Holdings Limited as the largest shareholder. The table below outlines Sanlam Kenya’s major shareholders:

|

Cytonn report: Sanlam Kenya’s Major shareholders |

||

|

Shareholder |

No. of shares held |

Percentage shareholding |

|

Hubris Holdings Limited |

82,278,000 |

57.1% |

|

Aksaya Investment Holdings Limited |

30,298,077 |

21.0% |

|

Mwangi Peter Kingori |

2,217,784 |

1.5% |

|

Mayfair Insurance Company |

1,132,050 |

0.8% |

|

Standard Chartered Nominees A/C 95 95 |

852,600 |

0.6% |

|

Patel Anjay Vithalbhai |

847,800 |

0.6% |

|

Kenya Reinsurance Corporation Limited |

511,200 |

0.4% |

|

Thammo Holdings Limited |

457,949 |

0.3% |

|

Malde Anilkumar Virpar |

452,550 |

0.3% |

|

Carbacid Investments Limited |

390,000 |

0.3% |

|

Others |

24,561,990 |

17.1% |

|

Total |

144,000,000 |

100.0% |

Sanlam Kenya’s largest shareholder, Hubris Holdings Limited, which holds 57.1% directly, has committed to fully subscribing to its rights. Other major shareholders have expressed support for the transaction, indicating a strong likelihood of participation. With Hubris Holdings Limited’s substantial backing, Sanlam Kenya has a solid foundation to achieve significant subscription levels.

Going forward, it is our expectation that Sanlam Kenya’s success will hinge on its ability to effectively deploy the new capital to fuel growth and reduce its debt levels. In addition, the Group’s strategy of strengthening its capital and investments through divesting from real estate, restructuring its debt portfolio and closing dormant subsidiaries has proven to be effective. Following a return to profitability in 2024, with a significant 933.5% increase in Profit After Tax to Kshs 1.1 bn, from the Kshs 0.1 bn loss recorded in FY’2023 and the rights issue, shareholders will be watching closely for improved performance and increased market share in Kenya’s insurance sector.

- East Africa Exchanges (EAE) 20 Share Index Launch

During the week, the East African Securities Exchanges Association (EASEA) launched the East Africa Exchanges (EAE) 20 Share Index, the first regional index in East Africa. The EAE 20 Share Index comprises of the top 20 listed companies in Kenya, Tanzania, Uganda and Rwanda securities exchanges in terms of market capitalization. The table below shows the listed companies in the EAE 20 Share index and their market caps as of 11th April 2025:

|

Cytonn Report: EAE 20 Share Index Listed Companies |

||

|

Country |

Company |

Market Cap (USD mn) |

|

Kenya |

Safaricom Plc |

5,452.2 |

|

KCB Group Plc |

948.9 |

|

|

Equity Group Holdings Plc |

1,297.7 |

|

|

The Co-operative Bank of Kenya Limited |

723.8 |

|

|

Absa Bank Kenya |

714 |

|

|

Tanzania |

CRDB Bank Plc |

771.3 |

|

NMB Bank Plc |

1,121.5 |

|

|

Tanzania Breweries Limited |

1,202.3 |

|

|

Tanga Cement Company Limited |

42.8 |

|

|

Tanzania Cigarette Corporation |

635.5 |

|

|

Rwanda |

Bralirwa Limited |

98.5 |

|

BK Group Plc |

206.7 |

|

|

I&M Bank (Rwanda) Plc |

24.8 |

|

|

Cimerwa Plc |

75.8 |

|

|

MTN Rwandacell Plc |

134.1 |

|

|

Uganda |

MTN Uganda Limited |

1,654.8 |

|

Stanbic Uganda Holdings |

653.8 |

|

|

Bank of Baroda (Uganda) |

100.0 |

|

|

Airtel Uganda Limited |

1,032.7 |

|

|

Quality Chemical Industries Limited |

86.3 |

|

To be included in the index, a company must meet specific criteria: its shares should be primarily listed in one of the East African exchanges, it should maintain consistent profitability, a proven record of dividend payments, maintain a continuous listing of a minimum of one year and demonstrate stability as a blue-chip firm. The constituent firms will be reviewed semi-annually by the EASEA Index Management Committee, which oversees updates such as additions and removals based on mergers, restructuring, delisting or other market factors.

A reserve list is maintained with five top-ranking non-constituent securities to allow immediate replacements if any constituent is removed. New issues of securities can be added to the index either during periodic reviews or earlier if deemed critical to market representation.

Daily index values and updates are published by member exchanges and the EA Securities Exchanges website to ensure transparency and accessibility for stake holders. As of 11th April 2025, the index declined by 0.1% to close at 100.1 from the 100.2 recorded previously.

This launch aligns with ongoing efforts to deepen financial integration across East Africa, harmonize market operations and foster innovation in financial instruments. For the Kenyan market, the index enhances the visibility of local blue chip-companies on a broader stage, potentially attracting more foreign direct investment and portfolio inflows.

We are “Bullish” on the Equities markets in the short term due to current cheap valuations, lower yields on short-term government papers and expected global and local economic recovery, and, “Neutral” in the long term due to persistent foreign investor outflows. With the market currently trading at a discount to its future growth (PEG Ratio at 0.6x), we believe that investors should reposition towards value stocks with strong earnings growth and that are trading at discounts to their intrinsic value. We expect the current high foreign investors sell-offs to continue weighing down the economic outlook in the short term.

- Residential Sector

- Kshs 20.0 bn housing project launched by Gulf Cap Real Estate

During the week, Gulf Cap Real Estate launched a Kshs 20.0 bn housing project in Nairobi, aiming to address Kenya’s acute housing shortage by delivering mid- and low-cost units. This initiative, underscores the developer’s commitment to easing the country’s estimated 2.0 mn-unit housing deficit, which grows by 250,000 units annually against a supply of just 50,000. The project comprises two key developments—InCity Suites and Starehe Point located in Starehe constituency, Nairobi—both designed to provide affordable homes in the residential market.

Gulf Cap, has adopted a model that minimizes reliance on external loans, opting instead for internal financing. This strategy is especially relevant given the country’s high Real Estate non-performing loan ratio of 14.8% as of Q3’2024, which has curtailed credit access. The firm also utilizes cost-effective procurement methods and innovative construction technology—particularly tunnel and aluminum formwork, which significantly speeds up building timelines and reduces expenses. While common in the Middle East and Europe, this technology is still rare in Africa, positioning Gulf Cap as a pioneer in modern construction practices within the region.

The project is part of a broader portfolio that includes developments like Buxton in Mombasa and LV Marina in Kisumu, further establishing Gulf Cap as a key player in the affordable housing segment. However, despite its promise, the initiative faces structural challenges. Mortgage affordability remains low, with a typical monthly repayment of Kshs 60,000 on a Kshs 6.0 mnunit proving unreachable for many informal workers, even with government-backed schemes like the Kenya Mortgage Guarantee Trust.

We expect that, the initiative arrives at a critical moment for Kenya’s real estate sector. As government housing programs face delays, private investments like Gulf Cap’s could help bridge the supply gap, create jobs, and revive the real estate sector. For long-term impact, however, broader systemic reforms are essential. These include expanding access to affordable financing, enforcing strict construction standards, and enhancing infrastructure. If successfully executed, Gulf Cap’s Nairobi project could reshape the affordable housing landscape and catalyze more private-sector involvement in tackling Kenya’s housing crisis.

- KCB Bank, Mi Vida Homes Team Up to Build Affordable Homes

During the week, KCB Bank and Mi Vida Homes entered a partnership to accelerate the development of eco-friendly, affordable housing in Kenya. This collaboration supports the government’s Affordable Housing Programme, which aims to deliver 250,000 units annually to bridge the country’s significant housing deficit. Under the agreement, KCB will provide construction financing for Mi Vida’s projects and also offer mortgage loans to buyers, aiming to make homeownership more accessible. Mi Vida plans to develop 5,000 homes over the next five years, focusing on well-planned, sustainable communities. The initiative is positioned as a solution to the growing demand for affordable housing, particularly in urban and peri-urban areas.

The impact on the real estate sector could be significant. First, the planned delivery of thousands of units contributes directly to addressing the housing shortfall, which currently stands at around kshs 2 mn units. Second, KCB’s end-user financing is expected to ease access to mortgages, though affordability remains a challenge. Many low-income earners, especially those in informal employment, may still be unable to meet repayment terms, even with initiatives like the Kenya Mortgage Guarantee Trust that reduce risk for lenders. A standard mortgage for a KShs 6.0 mn home still requires monthly payments well above what most Kenyans can afford.

Economically, the construction of these homes is expected to generate employment and stimulate growth in sectors like construction materials and real estate services. This could help revive a property market that has shown signs of strain, with a reported contraction in late 2024. Additionally, Mi Vida’s commitment to sustainable construction, through projects certified by international green building standards, aligns with broader environmental goals and may set new benchmarks in the market.

However, challenges persist. The mortgage market remains constrained by a high rate of non-performing loans, which has made banks more cautious. There are also risks tied to market saturation in Nairobi, where some areas already show signs of oversupply. Furthermore, the success of the partnership will depend on consistent construction quality and safety, especially in light of recent incidents that have raised concerns about building standards in Kenya.

We expect that the partnership will mark a step forward for private sector involvement in housing, its long-term success will depend on addressing systemic affordability barriers and ensuring that such developments remain accessible to the population segments most in need.

- Hospitality sector

During the week, Hotel Chain Development Pipeline in Africa 2025 report noted that Kenya’s hospitality sector is undergoing a major transformation, with new hotel developments increasingly moving away from Nairobi and into upcountry regions. Nearly half of the hotel rooms currently under construction in the country are now located outside the capital, up from just over a quarter the previous year. Out of the 4,344 rooms being developed across 26 hotels, 2,038 are in towns and cities outside Nairobi, which now only accounts for 2,306 rooms. This shift has seen Nairobi lose its place among Africa’s top 10 cities for hotel development, a significant change driven by evolving investment patterns.

This transition reflects Nairobi’s maturity as a hospitality hub, with most major international hotel brands already present. Developers are now focusing on untapped regions, spurred by improved infrastructure and growing tourism potential. Areas such as the Maasai Mara have attracted significant interest, including the recent launch of a luxury safari camp by Marriott International hotel chain. Although Nairobi still hosted six new hotel brands in the past year, investors are clearly diversifying their interests beyond the capital to take advantage of new opportunities and avoid saturated markets.

The growing interest in upcountry regions has substantial implications for the real estate sector. As hotel chains establish themselves in new locations, demand for related infrastructure such as residential housing, commercial spaces, and utilities is expected to rise. This could drive land value appreciation in areas around key tourist destinations, similar to what has occurred in peri-urban zones like Kitengela. At the same time, Nairobi’s hospitality market faces growing pressure, with signs of oversupply that could result in falling returns for hotel property investments.

Going forward we expect that tourism growth will continue to support this upcountry expansion, with international arrivals rising by over 13.5% in the past year. However, the success of this trend will depend on continued infrastructure improvements, such as roads, power, and water supply, which remain inconsistent in many rural regions. While developers are capitalizing on the promise of new markets, the shift is also partially influenced by challenges in Nairobi, including financial constraints, high loan default rates, and a rise in property auctions. Some developers may see upcountry locations as a strategic move to reduce exposure to the economic pressures affecting the capital. This ongoing redistribution of hospitality investment presents both opportunities for regional development and challenges that must be addressed to ensure long-term sustainability.

- Real Estate Investments Trusts (REITs) Performance

On the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 25.4 and Kshs 22.2 per unit, respectively, as per the last updated data on 4th April 2025. The performance represented a 27.0% and 11.0% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. The volumes traded for the D-REIT and I-REIT came in at Kshs 12.8 mn and Kshs 35.6 mn shares, respectively, with a turnover of Kshs 323.5 mn and Kshs 791.5 mn, respectively, since inception in February 2021. Additionally, ILAM Fahari I-REIT traded at Kshs 11.0 per share as of 4th April 2025, representing a 45.0% loss from the Kshs 20.0 inception price. The volume traded to date came in at 138,600 shares for the I-REIT, with a turnover of Kshs 1.5 mn since inception in November 2015.

REITs offer various benefits, such as tax exemptions, diversified portfolios, and stable long-term profits. However, the ongoing decline in the performance of Kenyan REITs and the restructuring of their business portfolios are hindering significant previous investments. Additional general challenges include:

- Insufficient understanding of the investment instrument among investors leading to a slower uptake of REIT products,

- Lengthy approval processes for REIT creation,

- High minimum capital requirements of Kshs 100.0 mn for REIT trustees compared to Kshs 10.0 mn for pension funds Trustees, essentially limiting the licensed REIT Trustee to banks only

- The rigidity of choice between either a D-REIT or and I-REIT forces managers to form two REITs, rather than having one Hybrid REIT that can allocate between development and income earning properties

- Limiting the type of legal entity that can form a REIT to only a trust company, as opposed to allowing other entities such as partnerships, and companies,

- We need to give time before REITS are required to list – they would be allowed to stay private for a few years before the requirement to list given that not all companies maybe comfortable with listing on day one, and,

- Minimum subscription amounts or offer parcels set at Kshs 0.1 mn for D-REITs and Kshs 5.0 mn for restricted I-REITs. The significant capital requirements still make REITs relatively inaccessible to smaller retail investors compared to other investment vehicles like unit trusts or government bonds, all of which continue to limit the performance of Kenyan REITs.

We expect Kenya’s Real Estate sector to remain on a growth trend, supported by: i) demand for housing sustained by positive demographics, such as urbanization and population growth rates of 3.8% p.a and 2.0% p.a, respectively, against the global average of 1.7% p.a and 0.9% p.a, respectively, as at 2023,, ii) activities by the government under the Affordable Housing Program (AHP) iii) heightened activities by private players in the residential sector iv) increased investment by local and international investors in the retail sector. However, challenges such as rising construction costs, strain on infrastructure development (including drainage systems), high capital requirements for REITs, and existing oversupply in select Real Estate sectors will continue to hinder the sector’s optimal performance by limiting developments and investments.

Following the release of the FY’2024 results by all four authorized Real Estate Investment Trusts (REITs) in Kenya, the Cytonn Real Estate Research Team undertook an analysis of the financial performance of the REITs and identified the key factors that shaped the performance of the sector. For the earnings notes of the various REITs, click the links below:

- ILAM Fahari I-REIT FY’2024 Earnings Note

- LapTrust Imara I-REIT FY’2024 Earnings Note

- Acorn I-REIT FY’2024 Earnings Note

- Acorn D-REIT FY’2024 Earnings Note

In the report we will assess the financial performance of the current REITs in the market during FY’2024 in terms of operational metrics, profitability metrics, leverage ratios, liquidity ratios, and valuation metrics. In addition, we highlight the outlook regarding our expectations for the REITs sector going forward. This we will cover as follows;

- Overview of the REITs Sector in Kenya,

- Themes that shaped the Real Estate Sector in FY’2024,

- Summary Performance of the REITS in FY’2024, and,

- Conclusion and Outlook for the REITs sector.

Section I: Overview of the REITs Sector in Kenya

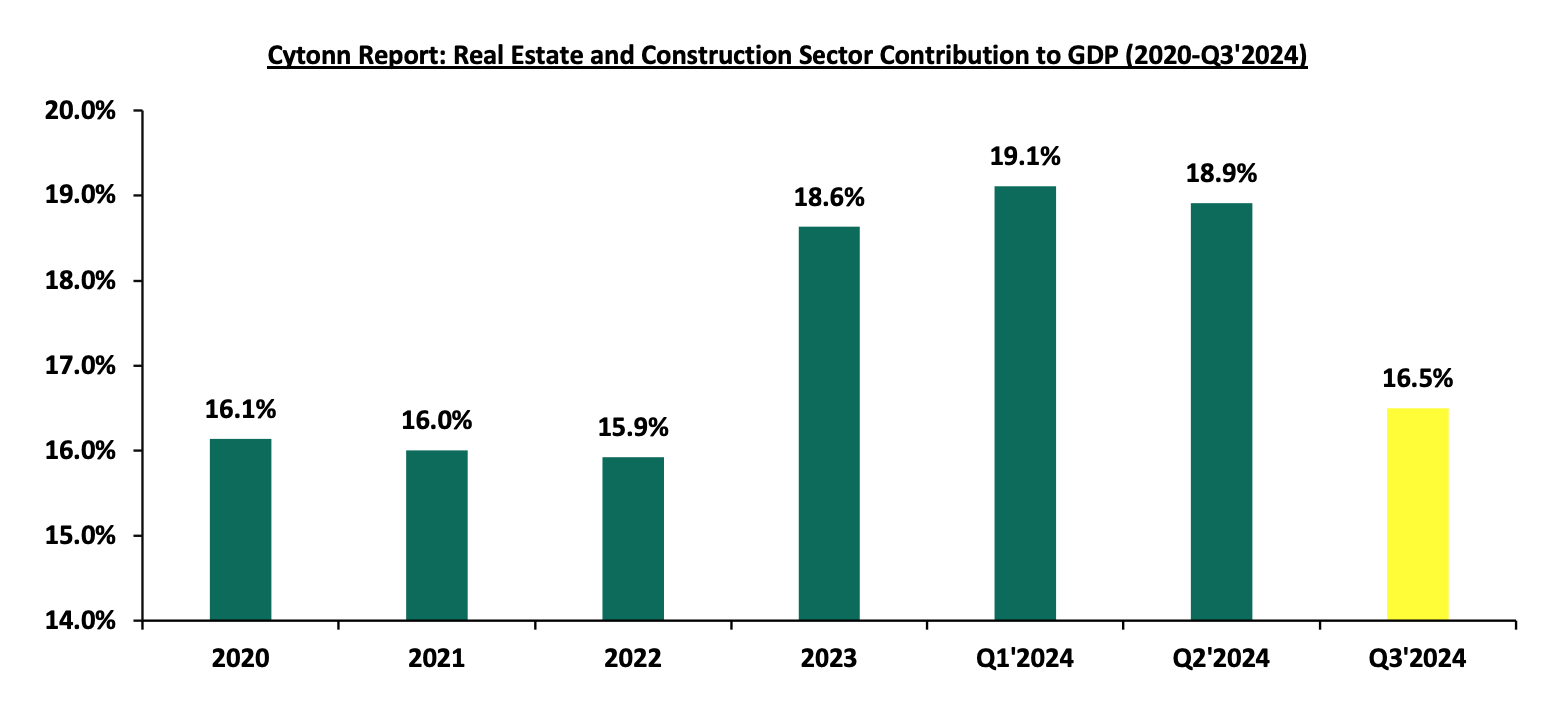

In FY’2024, the general Real Estate sector continued to witness considerable growth in activity in terms of property transactions and development activities. Consequently, the sector’s activity contribution to Gross Domestic Product (GDP) grew by 5.5 % to Kshs 283.8 bn in Q3’2024, from Kshs 268.9 bn recorded during the same period in 2023. In addition, the sector contributed 10.8% to the country’s GDP, 0.3% points increase from 10.5% recorded in Q3’2023. Cumulatively, the Real Estate and construction sectors contributed 16.5% to GDP, 0.2% points decrease from 16.7% in Q3’2023, attributable to decline in construction contribution to GDP by 0.4% points, to 5.7% in Q3’2024, from 6.1% recorded in Q3’2023. The decline in Construction sector was attributable to the high cost of building materials that led to a 2.0% contraction in the construction sector in Q3’2024, compared to a 4.0% increase in Q3’2023. The graph below highlights the Real Estate and Construction sectors’ contribution to GDP from 2020 to Q3’2024;

Source: Kenya National Bureau of Statistics (KNBS)

As the REITs continue to gain popularity in Kenya, we set to explore and review the REITs environment in 2024 building to the previous reports we did, which include: Real Estate Investment Trusts (REITs) progress in Kenya ,Kenya’s REITs H1’2024 ,Review of Real Estate Investments Trusts in Kenya 2024

Section I: Overview of the REITs Sector in Kenya

Real Estate Investment Trusts are crucial to the development given the limited funding available to the developers. Real Estate Investment Trusts (REITs) represent an innovative financing avenue for real estate development in Kenya. REITs provide a structured mechanism for pooling resources from multiple investors to finance or acquire income-generating real estate assets. The Capital Markets Authority (CMA) regulates REITs in Kenya, ensuring transparency and investor protection. Despite being relatively new in the Kenyan financial market, REITs have shown potential as a transformative tool for real estate financing.

In Kenya, REITs are classified into two main types:

- Development REITs (D-REITs): These focus on financing the construction of new real estate projects. Developers utilize D-REITs to raise capital for large-scale projects, such as residential complexes, commercial buildings, or mixed-use developments. Investors in D-REITs anticipate returns from the eventual sale or lease of the completed properties. Example of this REIT include Acorn D-REIT.

- Income REITs (I-REITs): These are designed for properties that generate consistent rental income. I-REITs appeal to investors seeking steady cash flow from established properties such as office buildings, shopping malls, or industrial parks. In Kenya examples of I-REITs include Acorn I-REIT and Stanbic Fahari I-REITs.

REITs in Kenya are governed by strict regulations aimed at safeguarding investors. They operate as collective investment schemes where a REIT manager oversees the fund's operations. Investors purchase units of the REIT, similar to shares in a company, granting them proportional ownership of the underlying real estate assets. These units are typically traded on the Nairobi Securities Exchange (NSE), providing liquidity and enabling investors to buy or sell their stakes easily.

REITs must allocate a significant portion of their income, often up to 90.0% to investors as dividends, making them attractive to those seeking regular income. Additionally, REITs benefit from tax incentives, such as exemptions on corporate tax, which enhance their appeal to both developers and investors.

In 2013, the Capital Markets Authority (CMA) introduced a detailed framework and regulations for REITs, enabling developers to secure capital through this investment avenue.

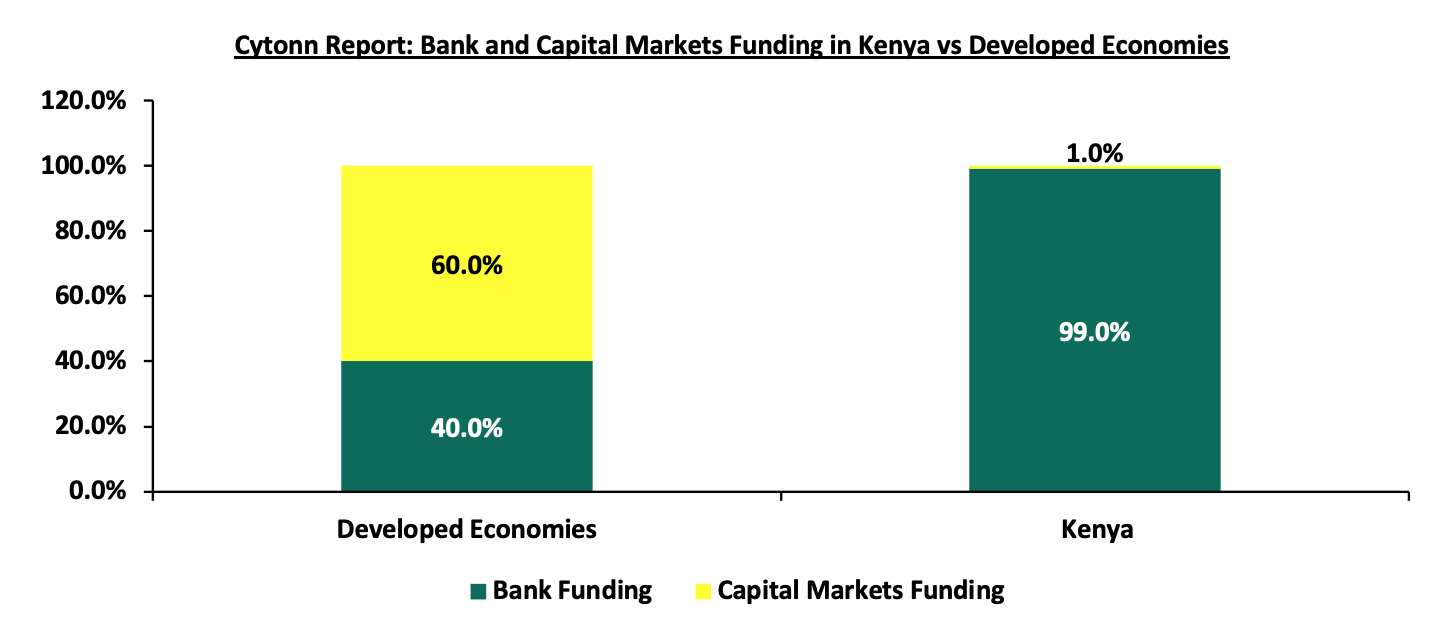

Kenya's Real Estate sector has been expanding due to ongoing construction activities driven by strong demand for real estate developments. The residential market is significantly under-supplied, with an 80.0% housing deficit; only 50,000 units are delivered annually against an estimated need for 200,000 units per year. Additionally, the formal retail market in Kenya is still in its nascent stages, with a penetration rate of approximately 30.0%, as reported by the world bank. Despite the high demand, developers in Kenya encounter limited financing options, with local banks providing nearly 99.0% of construction financing, in stark contrast to the 40.0% typically seen in developed countries. The graph below illustrates the comparison of construction financing in Kenya versus developed economies;

To bridge the funding gap, developers are increasingly turning to alternative financing methods. In 2013, the Capital Markets Authority (CMA) introduced a regulatory framework for Real Estate Investment Trusts (REITs) in Kenya. REITs are collective investment vehicles that pool funds from investors, who then acquire rights or interests in a trust divided into units. Investors benefit from profits or income generated by the real estate assets held within the trust. To ensure transparency, accountability, and the protection of investors' interests, four essential entities play key roles in the REIT structure in Kenya. Click here to read more on the key entities and how the REIT structure operates.

Since its introduction in 2013, the REIT market in Kenya has faced several hurdles that have hindered its growth. Key challenges include the hefty capital requirement of Kshs 100.0 mn for trustees, limiting this role largely to banks, and a protracted approval process for setting up REITs. Additionally, the high minimum investment threshold of Kshs 5.0 mn discourages potential investors, while a lack of sufficient investor education and awareness further impedes market expansion. As a result, the REIT market capitalization in Kenya remains significantly lower compared to other regions.

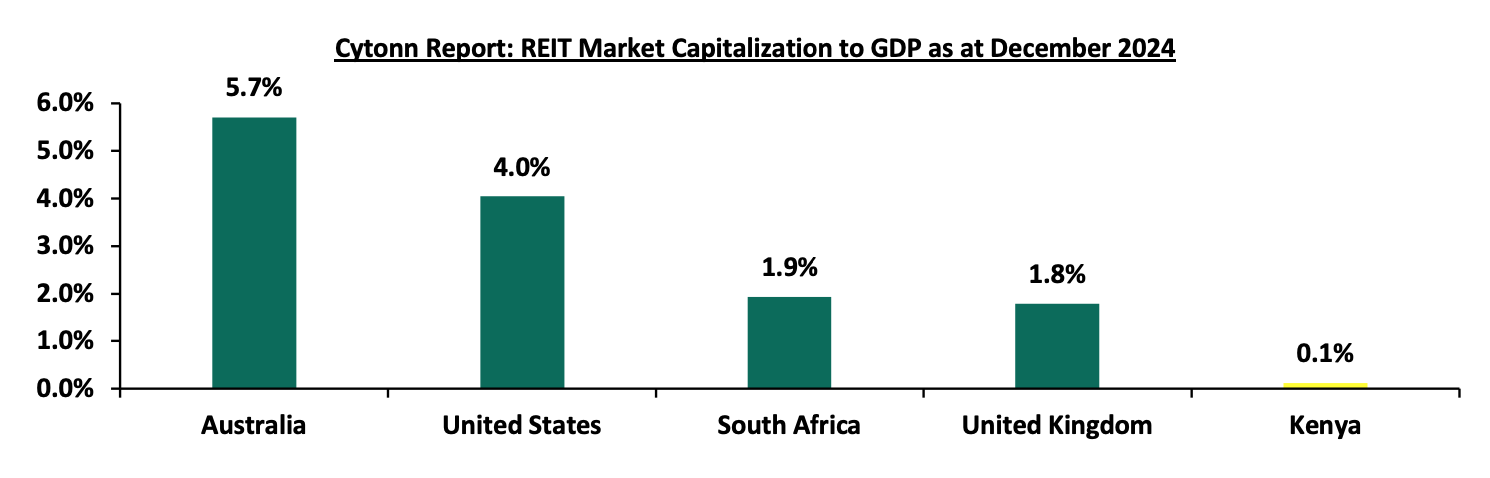

The underdeveloped capital markets in Kenya has continually failed to provide alternative means of financing Real Estate developments. Due to this, most property developers rely on conventional sources of funding such as banks, compared to other developed countries. As a result, Kenya’s REIT Market Capitalization to GDP has remained significantly low at 0.1%, compared to other countries such as South Africa with 1.9%, as shown below;

Source: European Public Real Estate Association (EPRA), World Bank, Cytonn Research

Most property developers in Kenya continue to rely on traditional funding sources, such as banks, unlike in more developed markets. Since the establishment of REIT regulations, four REITs have been approved in Kenya, all structured as closed-ended funds with a fixed number of shares. However, none of these REITs are actively trading on the Main Investment Market Segment of the Nairobi Securities Exchange (NSE). Following the recent delisting of ILAM Fahari I-REIT, LAPTrust Imara I-REIT is the only listed REIT in the country, quoted on the restricted market sub-segment of the NSE's Main Investment Market. It is important to note that Imara did not raise funds upon listing. The ILAM Fahari I-REIT, Acorn I-REIT and D-REIT are not listed but trade on the Unquoted Securities Platform (USP), an over-the-counter market segment of the NSE. The table below outlines all REITs authorized by the Capital Markets Authority (CMA) in Kenya

|

Cytonn Report: Authorized REITs in Kenya |

||||||

|

# |

Issuer |

Name |

Type of REIT |

Listing Date |

Market Segment |

Status |

|

1 |

ICEA Lion Asset Management (ILAM) |

Fahari |

I-REIT |

July 2024 |

Unquoted Securities Platform (USP) |

Trading |

|

2 |

Acorn Holdings Limited |

Acorn Student Accommodation (ASA) – Acorn ASA |

I-REIT |

February 2021 |

Unquoted Securities Platform (USP) |

Trading |

|

3 |

Acorn Holdings Limited |

Acorn Student Accommodation (ASA) – Acorn ASA |

D-REIT |

February 2021 |

Unquoted Securities Platform (USP) |

Trading |

|

4 |

Local Authorities Pension Trust (LAPTrust) |

Imara |

I-REIT |

March 2023 |

Restricted Market Sub-Segment of the Main Invesment Market |

Restricted |

Source: Nairobi Securities Exchange, CMA

Section II: Themes that Shaped the REIT Sector in FY’2024

In our report on review of the REITs sector, we explored how evolving regulations, strategic acquisitions, and capital-raising initiatives have influenced the REIT industry's trajectory. Additionally, we provide insights into the broader factors that have impacted the sector's performance and overall direction during this period. For more information on themes that shaped the REIT sector in 2024, please visit our report Review of Real Estate Investments Trusts in Kenya 2024

Section III: Summary Performance of the REITs in FY’2024

The tables below highlight the performance of the Kenyan REITs sector, showing the performance using several National Association of Real Estate Investments Trusts (NAREIT) approved metrics, and the key take-outs include;

|

Cytonn Report: Summary Performance Kenya REITs in FY’2024 |

|||||||||||||||

|

|

Imara I-REIT |

ILAM Fahari I-REIT |

Acorn I-REIT |

Acorn D-REIT |

Average FY'2023 |

Average FY'2024 |

y/y change |

||||||||

|

|

FY'2023 |

FY'2024 |

y/y Change |

FY'2023 |

FY'2024 |

y/y Change |

FY'2023 |

FY'2024 |

y/y Change |

Fy'2023 |

FY'2024 |

y/y Change |

|||

|

Operating Metrics |

|||||||||||||||

|

Net Operating Income (NOI) |

244.6 |

353.9 |

44.7% |

148.7 |

113.6 |

(23.6%) |

340.1 |

662.6 |

94.8% |

368.6 |

1152.7 |

212.7% |

1102.0 |

2282.8 |

107.1% |

|

Profitability Metrics |

|||||||||||||||

|

Funds from Operations |

57.2 |

283.1 |

394.8% |

(0.3) |

377.2 |

126831.0% |

501.8 |

972.5 |

93.8% |

368.6 |

1152.7 |

212.7% |

927.3 |

2785.6 |

200.4% |

|

Adjusted FFO |

57.2 |

283.1 |

394.8% |

(6.1) |

391.2 |

6526.8% |

501.8 |

972.5 |

93.8% |

368.6 |

1152.7 |

212.7% |

921.5 |

2799.6 |

203.8% |

|

Cash Available for Distribution (CAD) |

195.7 |

283.1 |

44.7% |

148.7 |

113.6 |

(23.6%) |

235.7 |

234.6 |

(0.5%) |

239.8 |

293.2 |

22.2% |

819.9 |

924.5 |

12.8% |

|

Cash Amounts Distributed (CAD) |

57.2 |

283.1 |

394.7% |

126.7 |

54.3 |

(57.1%) |

154.1 |

125.6 |

(18.5%) |

71.6 |

839.9 |

1073.8% |

409.6 |

1302.9 |

218.1% |

|

Valuation Metrics |

|||||||||||||||

|

Net Asset Value (NAV) |

6,981.9 |

6,452.0 |

(7.6%) |

3,306.4 |

0.1 |

7.6% |

7,377.5 |

8,122.1 |

10.1% |

6,560.9 |

7339.7 |

11.9% |

6,056.7 |

5,581.3 |

(7.8%) |

Source: Cytonn Research

Key takeaways from the table include:

- The combined Net Operating Income (NOI) of Kenyan REITs saw a 107.1 % increase, reaching Kshs 2,282.8 mn in FY’2024, up from Kshs 1102.0 mn in FY’2023. This growth was largely driven by a 212.7% rise in the net operating income of Acorn D-REIT, which increased to Kshs 1152.7 mn from Kshs 368.6 mn in FY’2023. Additionally, Acorn I-REIT reported a notable NOI growth of 94.8%, reaching to Kshs 662.6 mn from Kshs 340.1 mn in similar period in 2023, further contributing to the overall positive performance. ILAM Fahari I-REIT’s NOI saw the largest drop, falling by 23.6% to Kshs 113.6 mn from Kshs 148.7 mn in FY’2023

- Combined Funds from Operations (FFO) of Kenyan REITs increased by 200.4% in FY’2024, increasing to Kshs 2,785.6 mn from Kshs 927.3 mn in FY’2023. Similarly, Adjusted FFOs for Kenyan REITs increased by 203.8%, reaching Kshs 2799.6 mn in FY’2024 from Kshs 921.5 mn in FY’2023. This increase was largely due to significant increases in NOIs except for ILAM Fahari I-REIT which recorded a decrease of 23.6% during the period,

- The REITs combined Cash amounts available for paying dividends to REIT investors which we measured using the Cash Available for Distribution (CAD) metric increased by 12.8% in FY’2024 to Kshs 924.5 mn from Kshs 819.9 mn in FY’2023. The performance was propelled by Laptrust Imara I-REIT’s distributable earnings which increased by 394.7% to come in at Kshs 283.1 mn from Kshs 195.7 mn during the same period last year. Additionally, Acorn D-REIT distributed earnings stood at Kshs 293.2 mn which was an improvement from the Kshs 239.8 mn earnings recorded in FY’2023 which was a 22.2% improvement.

- Notably, the REIT managers of all four REITs recommended provisional dividends. For Laptrust Imara I-REIT, the REIT Manager suggested a first dividend distribution of Kshs 283.1 mn, amounting to Kshs 0.82 per unit, which was approved by the Trustee for the FY’2024, ILAM Fahari I-REIT’s manager proposed a first and final dividend of Kshs 0.3 per unit, making Kshs 54.3 mn available for distribution out of Kshs 113.6 mn. Acorn I-REIT increased its total distribution for the year to Kshs 125.6mn, translating to Kshs 0.4 per unit, marking a 18.5 % drop from the Kshs 154.1 mn distributed in FY’2023. Acorn D-REIT recommended a distribution of Kshs 293.2 mn, equivalent to Kshs 1.1 per unit, which was an improvement from the 0.9 per unit distribution in FY’2023, and,

- The combined Net Asset Values (NAV) for Kenyan REITs decreased by 7.8% to reach Kshs 22,325.1 mn in FY’2024, from Kshs 24,226.7 mn in FY’2023. This decline was driven by a 52.6% decrease in the NAV of Imara I-REIT, reaching Kshs 3,306.4 mn from Kshs 6,981.9 mn in FY’2023. All other REITS recorded an increase in NAV by 7.6%, 10.1% and 11.9% for ILAM Fahari I-REIT, Acorn I-REIT and D-REIT respectively.

The table below makes a comparison of the leverage and liquidity ratios of all four Kenyan REITs during FY’2024 and FY’2023;

|

Cytonn Report: Operation & Liquidity Ratios of Kenyan REITs |

|||||||||||||||

|

|

Imara I-REIT |

ILAM Fahari I-REIT |

Acorn I-REIT |

Acorn D-REIT |

FY'2023 |

FY'2024 |

y/y change |

||||||||

|

FY'2023 |

FY'2024 |

y/y Change |

FY'2023 |

FY'2024 |

y/y Change |

FY'2023 |

FY'2024 |

y/y Change |

FY'2023 |

FY'2024 |

y/y Change |

||||

|

Operating Metrics |

|||||||||||||||

|

Debt to Equity Ratios |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

16.5% |

59.2% |

42.7% |

7.5% |

24.5% |

17.0% |

|

Debt to Total Market Cap Ratio |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

16.0% |

66.2% |

50.2% |

7.3% |

27.5% |

20.1% |

|

Debt to Gross Book Value Ratio |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

9.4% |

28.3% |

18.9% |

4.3% |

11.7% |

7.4% |

|

Debt to EBITDA Multiple |

0.0 |

0.0 |

0.0% |

0.0 |

0.0 |

0.0% |

0.0 |

0.0 |

0.0% |

2.9 |

3.7 |

80.3% |

134.0% |

154.8% |

15.5% |

|

Liquidity Ratio |

|||||||||||||||

|

Debt Service Coverage Ratio |

0.0 |

0.0 |

0.0% |

- |

0.0 |

0.0% |

- |

- |

0.0% |

34.1% |

26.5% |

(7.6%) |

15.6% |

11.0% |

(4.6%) |

|

Implied Capitalization Rate |

3.6% |

21.3% |

17.8% |

21.3% |

7.4% |

(13.9%) |

4.0% |

6.8% |

2.8% |

3.5% |

9.0% |

5.5% |

8.1% |

11.1% |

3.0% |

Source: Cytonn Research

Key takeaways from the table include;

- Majority of the REITs remained ungeared during FY’2024, with their leverage ratios remaining at zero except Acorn D-REIT. Acorn D-REIT debt ratios increased in FY’2024 on account of a 301.9% increase in its long-term borrowings to Kshs 4.3 bn from Kshs 1.5 bn in FY’2023,

- Notably, Acorn D-REIT’s Debt to EBITDA Multiple increased by 80.3% to 3.7x in FY’2024, from 2.9x recorded in FY’2023. This was on the back of a faster rise in the REIT’s long-term borrowings which outpaced the EBITDA’s incline. Acorn D-REIT EBITDA in FY’2024 increased by 215.4% to Kshs 1,163.8 mn from Kshs 369.0 mn in FY’2023, compared to a 301.9% decrease in the REIT’s long-term debt, and,

- Imara I-REIT traded at the highest implied capitalization rate of 21.3%, signifying a higher return on investment compared to other REITs. In contrast, Acorn I-REIT had the lowest implied capitalization rate of 6.8%.

The table below presents a summary of key valuation metrics of Kenyan REITs in FY’2024;

|

Cytonn Report: Summary Performance Kenya REITs in FY’2024 |

|||||||||||||||

|

|

Imara I-REIT |

ILAM Fahari I-REIT |

Acorn I-REIT |

Acorn D-REIT |

FY'2023 |

FY'2024 |

y/y change |

||||||||

|

|

FY'2023 |

FY'2024 |

y/y Change |

FY'2023 |

FY'2024 |

y/y Change |

FY'2023 |

FY'2024 |

y/y Change |

FY'2023 |

FY'2024 |

y/y Change |

|||

|

Operating Metrics |

|||||||||||||||

|

Price/FFO per share |

121.0 |

24.5 |

(79.8%) |

(3830.5) |

(1.6) |

100.0% |

14.2 |

7.5 |

(47.2%) |

18.3 |

5.7 |

(68.9%) |

(919.3) |

9.0 |

(101.0%) |

|

Dividend Yield |

2.8% |

4.1% |

1.3% |

11.1% |

2.7% |

(8.4%) |

2.2% |

1.7% |

(0.4%) |

3.6% |

4.5% |

0.9% |

4.9% |

3.3% |

(1.7%) |

|

Dividend Coverage/Payout Ratio |

80.0% |

80.0% |

0.0% |

85.2% |

47.8% |

(37.4%) |

45.3% |

19.0% |

(26.3%) |

19.4% |

72.9% |

53.4% |

57.5% |

54.9% |

(2.6%) |

|

Net Asset Value |

6,981.9 |

6452.0 |

(7.6%) |

3,306.4 |

3556.9 |

7.6% |

7377.5 |

8122.1 |

10.1% |

6,560.9 |

7,339.7 |

11.9% |

24226.7 |

25470.7 |

5.1% |

|

Net Asset Value per share |

20.2 |

18.6 |

(7.6%) |

18.3 |

19.7 |

7.6% |

22.5 |

24.6 |

9.1% |

24.6 |

27.5 |

11.6% |

21.4 |

22.6 |

5.6% |

|

Implied Capitalization Rate |

3.6% |

5.1% |

1.5% |

21.3% |

7.4% |

(13.9%) |

4.0% |

6.8% |

2.8% |

3.5% |

9.0% |

5.5% |

8.1% |

7.1% |

(1.0%) |

|

Annualised Divided Yield |

5.7% |

8.2% |

2.5% |

11.4% |

2.7% |

(8.7%) |

2.2% |

1.7% |

(0.4%) |

3.6% |

4.5% |

0.9% |

5.7% |

4.3% |

(1.4%) |

Source: Cytonn Research

- Acorn I-REIT units are trading at a premium relative to its peers, with a Price to FFO per share multiple of Kshs 24.5, however this was a decrease of 79.8% from Kshs 121.0 price per FFO per share multiple,

- Laptrust Imara I-REIT’s and Acorn D-REIT posted the highest annualized dividend yield in FY’2024 at 8.2% and 4.5% respectively, surpassing ILAM Fahari I-REIT 2.7% and Acorn I-REIT’s 1.7%. On the payout side, Imara’s dividend payout was 85.2%, adhering to Kenya's REIT regulations that mandate distributing at least 80.0% of net profits after tax as dividends. Conversely, Acorn I-REIT and ILAM Fahari I-REIT had lower payouts of 19.0% and 47.8%, respectively, falling short of the regulatory threshold, which might raise compliance issues with CMA and,

- Acorn D-REIT recorded the highest NAV per share at Kshs 27.5, a 11.6% increase from FY’2023’s NAV per share of Kshs 24.6. This is on the back of an increase in the number of shares, which increased by 0.2% to 267.3 mn from Kshs 266.7 mn in FY’2023; and a 11.9% growth in the Net Asset Value (NAV) to Kshs 7.3 bn from Kshs 6.6 mn in FY’2023. Imara I-REIT had the lowest NAV per share at Kshs 18.6, a 7.6% decline from 20.2 recorded in FY’2023. This is attributable to a 4.0% decrease in total assets to Kshs 6.7 bn from Kshs 7.3 bn in FY’2023.

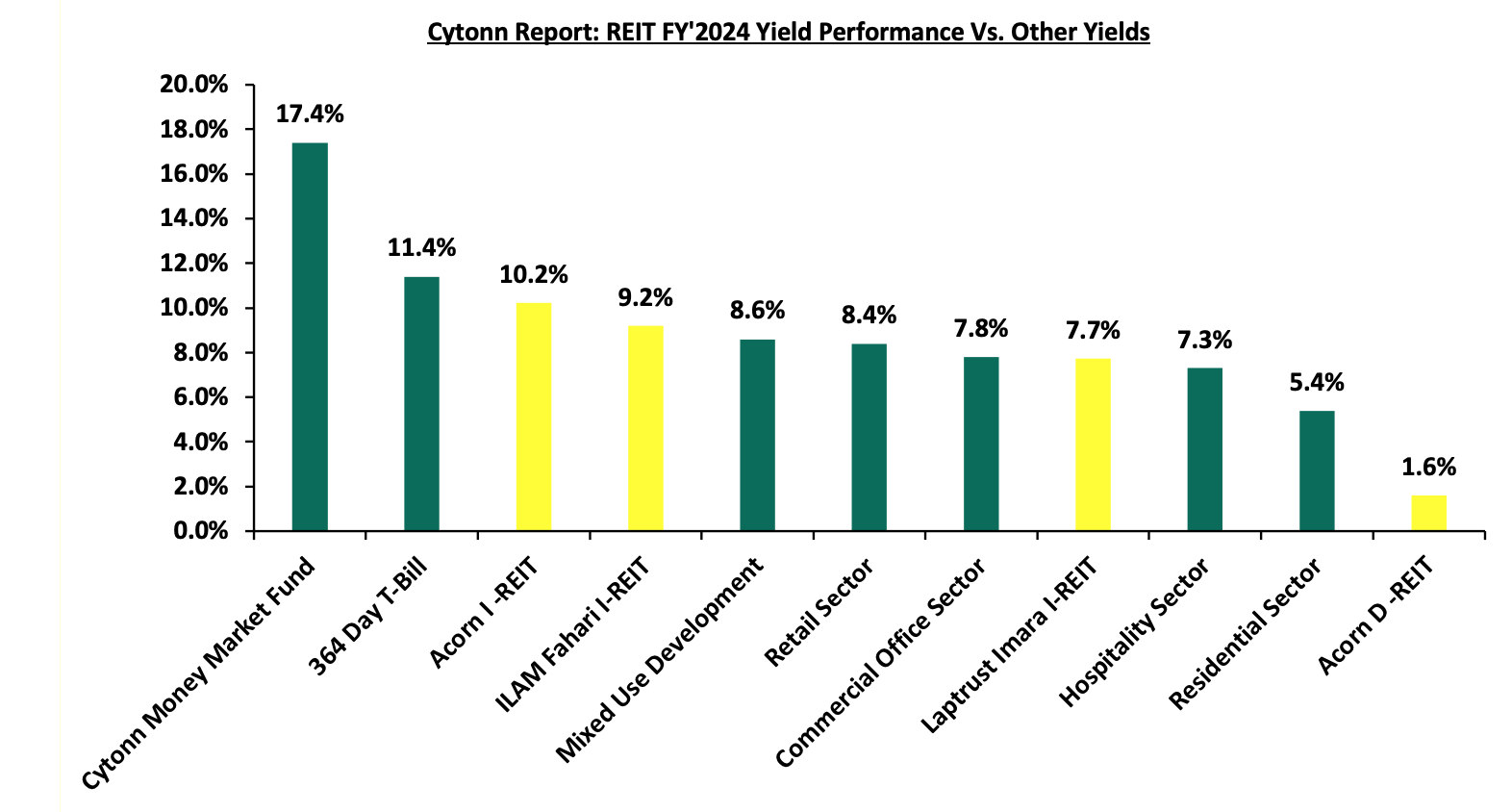

The REITs registered positive returns of 10.2%, 7.7%, 9.2% and 1.6% for Acorn I-REIT, Fahari I-REIT, Laptrust Amara IREIT and Acorn D-REIT respectfully. Acorn D-REIT registered the lowest yield due to reduction in the rental income by 44.0% to 181.7 bn in 2024 from 324.5 bn in 2023 majorly attributable to the sale of two residential properties Qwetu Hurlingham and Qwetu Aberdare Heights II. On average, REITS yields came in at 7.2% showing lower returns as compared to other assets. The chart below shows the comparison of REITs yield performance versus other assets.

Source: Cytonn Research

Section IV: Conclusion, Recommendations, and Outlook for the REITs Sector

Kenya's REITs market has seen moderate performance, shaped by various factors. Despite challenges, there are encouraging trends, such as growth in net operating incomes, indicating improved financial performance. Additionally, leverage ratios for most REITs have remained low, with many REITs being ungeared and relying on short-term debt for their operations to avoid overexposure to rising interest rates. This trend is expected to continue as REITs seek to maintain financial sustainability, as evidenced by Acorn Holdings' issuance of a green bond.

Recommendations to Enhance the REITs Sector:

- Stakeholder education: There is a pressing need to educate all key stakeholders on the REIT structure. Implementing comprehensive investor education and awareness campaigns is essential to inform potential investors about both the benefits and inherent risks of REIT investments. By enhancing investor knowledge and understanding, a larger pool of individuals can be encouraged to participate in the REIT market, ultimately driving its growth and fostering sustainable development.

- Expanding legal entities: In South Africa, the REIT framework allows for a variety of legal entities to form REITs, unlike in Kenya where the structure is predominantly limited to trusts. In countries like Belgium and the United States, REITs can be established using diverse legal structures such as public limited companies, limited liability companies, cooperatives, or trusts. This flexibility accommodates different investor preferences and business models. To strengthen the Kenyan REIT market, it is advisable to broaden the range of permissible structures beyond traditional trust models to include corporations, partnerships, and limited liability companies. Such diversification would better cater to various investor needs and lower the barriers to market entry, ultimately promoting a more robust and dynamic REIT sector.