Progress of Retirement Benefits Schemes in Kenya - 2024, & Cytonn Weekly #21/2024

By Research Team, May 26, 2024

Executive Summary

Fixed Income

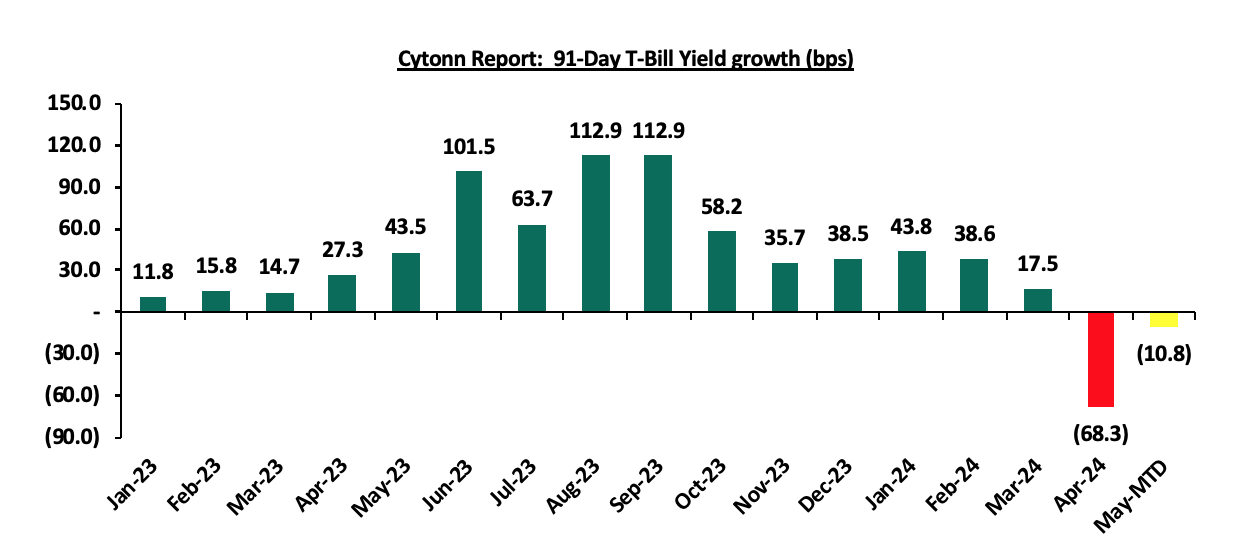

During the week, T-bills were oversubscribed for the fourth consecutive week, with the overall oversubscription rate coming in at 100.1%, albeit lower than the oversubscription rate of 194.8% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 7.1 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 177.6%, significantly lower than the oversubscription rate of 325.4% recorded the previous week. The subscription rate for the 182-day and 364-day papers decreased to 116.5% and 52.8% from 180.4% and 156.8% respectively recorded the previous week. The government accepted a total of Kshs 23.7 bn worth of bids out of Kshs 24.0 bn bids received, translating to an acceptance rate of 98.7%. The yields on the government papers were on an upward trajectory, with the yields on the 91-day, 182-day, and 364-day papers increasing by 0.8 bps, 4.6 bps, and 9.4 bps to 15.95%, 16.56%, and 16.62% from 15.94%, 16.52% and 16.53% respectively recorded the previous week;

During the week, the Kenya National Bureau of Statistics (KNBS) released the 2024 Economic Survey, highlighting that the Kenyan economy recorded a 5.6% growth in FY’2023, faster than the 4.9% growth recorded in FY’2022. The main contributor to Kenyan GDP remains to be the Agriculture, Fishing and Forestry sector which grew by 6.5% in FY’2023 compared to a contraction of 1.5% in FY’2022. All sectors in FY’2023, except Mining and Quarrying, recorded positive growths, with varying magnitudes across activities. Most sectors recorded improved growth compared to FY’2022, with Agriculture, Forestry and Fishing, Accommodation and Food Services, and Real Estate Sectors recording the highest growth improvements of 7.9% points, 6.8% points, and 2.8% points, respectively;

Also, during the week, the Kenya National Bureau of Statistics released the FY’2023 Economic Survey Report highlighting that Kenya’s balance of payments position improved by 46.4% in FY’2023, coming in at a deficit of Kshs 134.8 bn, from a deficit of Kshs 251.5 bn in FY’2022, and a slight deterioration from the Kshs 131.5 bn deficit recorded in Q3’2023;

Additionally, we are projecting the y/y inflation rate for May 2024 to come in at the range of 4.7% - 5.1% mainly on the back of reduced fuel prices, the maintenance of the Central Bank Rate (CBR) at 13.00%, the strengthening of the Kenyan Shilling and the reduction in electricity costs;

Equities

During the week, the equities market was on an upward trajectory, with NSE 10 gaining the most by 4.0%, while NASI, NSE 25, and NSE 20 gained by 2.3%, 2.7%, and 0.7% respectively, taking the YTD performance to gains of 29.2%, 24.5%, 23.0%, and 13.8% for NSE 10, NSE 25, NASI and NSE 20 respectively. The equities market performance was driven by gains recorded by large-cap stocks such as KCB Group, NCBA, and Cooperative Bank of 10.4%, 7.2%, and 4.3% respectively. The performance was, however, weighed down by losses recorded by large-cap stocks such as Stanbic Bank of 12.8%;

During the week, four of the listed banks released their Q1’2024 results. KCB Group released its Q1’2024 financial results, with its Core Earnings per Share (EPS) increasing by 69.0% to Kshs 5.1, from Kshs 3.0 in Q1’2023. HF group released its Q1’2024 financial results, with its Core Earnings per Share (EPS) increasing by 80.4% to Kshs 0.4 bn, from Kshs 0.2 bn in Q1’2023. NCBA Group released its Q1’2024 financial results, with its Core Earnings per Share (EPS) increasing by 4.7% to Kshs 3.2, from Kshs 3.1 in Q1’2023. Lastly, I&M Group released its Q1’2024 financial results, with its Core Earnings per Share (EPS) increasing by 35.4% to Kshs 2.2, from Kshs 1.2 in Q1’2023;

Real Estate

During the week, the Kenya Bureau of Statistics released the 2024 Economic Survey, which highlighted the performance of various sectors of the economy. The report indicated a general improvement in the hospitality and tourism sectors, with notable gains in the number of international arrivals and monthly bed occupancy;

In the infrastructure sector, President Ruto signed an agreement with Everstrong Capital, a U.S. firm, for the construction of the 440-kilometer Nairobi-Mombasa Expressway. The project, estimated to cost Kshs 470.0 bn (USD 3.6 bn), will be a six-lane dual carriageway. The project received approval from the National Assembly last year to proceed under a public-private partnership model;

In the industrial sector, President Ruto's visit to the U.S. resulted in an agreement being signed between G42 and Microsoft to build a data center worth Kshs 131.0 bn (USD 1.0 bn) at the KenGen Green Park in Olkaria. The data center will run on 100% renewable geothermal power from the Olkaria Geothermal fields in Naivasha, Nakuru County;

In the REITs segment, Acorn Holdings secured Ksh 23.6 bn (USD 180 mn) in funding from the U.S. Development Finance Corporation (DFC) for affordable student housing. The funding will be channeled towards the development of 35 affordable student housing units, adding 48,000 student beds to Acorn Holdings’ portfolio;

Additionally, Laptrust released the FY’2023 financial results for the Imara I-REIT for the period ended 31st December 2023. Rental and related income for the REIT stood at Kshs 305.2 mn in FY’2023, an 82.6% increase from Kshs 167.1 mn in H1’2023, implying a gross rental yield of 4.5% in FY’2023 on interest-earning assets, higher than the 2.4% rental yield recorded during H1’2023. This increase in rental income was driven by upward review in rental prices for several properties within the portfolio;

On the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 24.5 and Kshs 22.0 per unit, respectively, as of 17th May 2024. The performance represented a 22.5% and 10.0% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price;

Focus of the Week

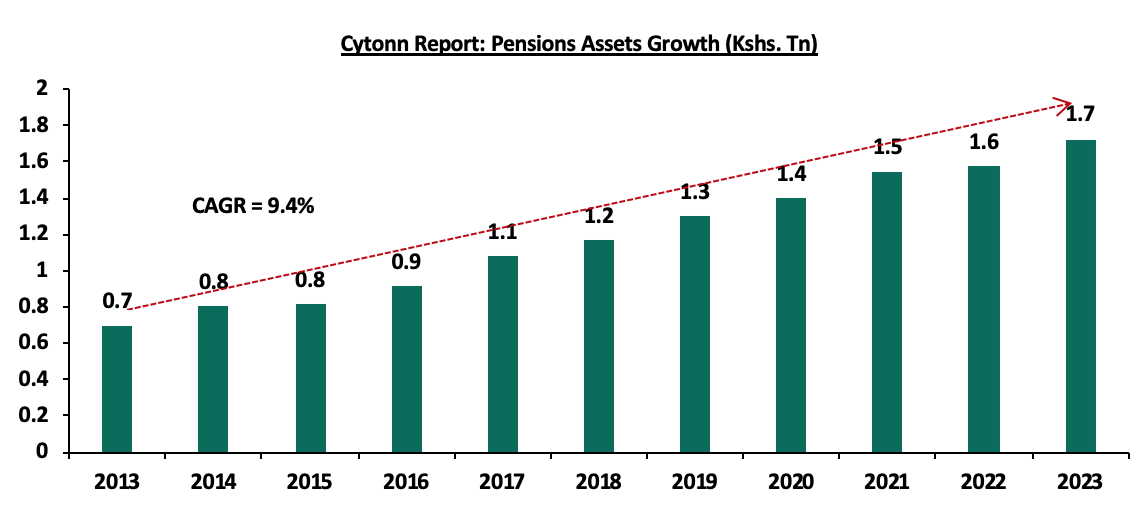

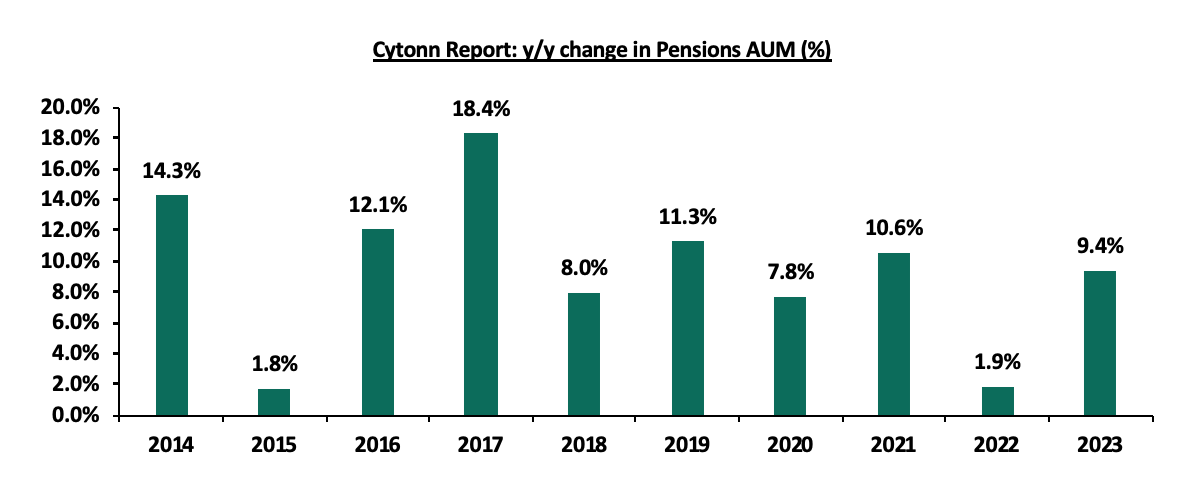

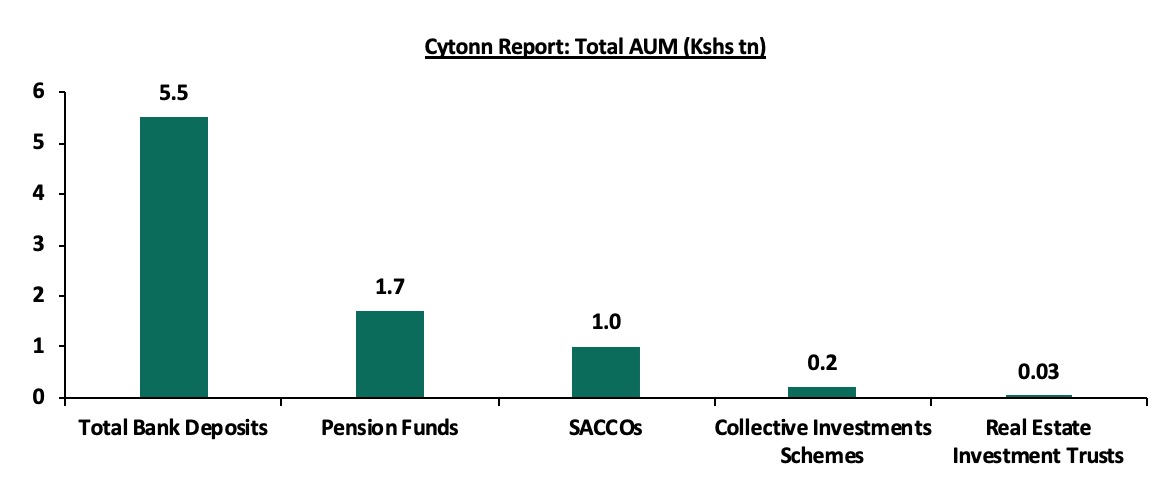

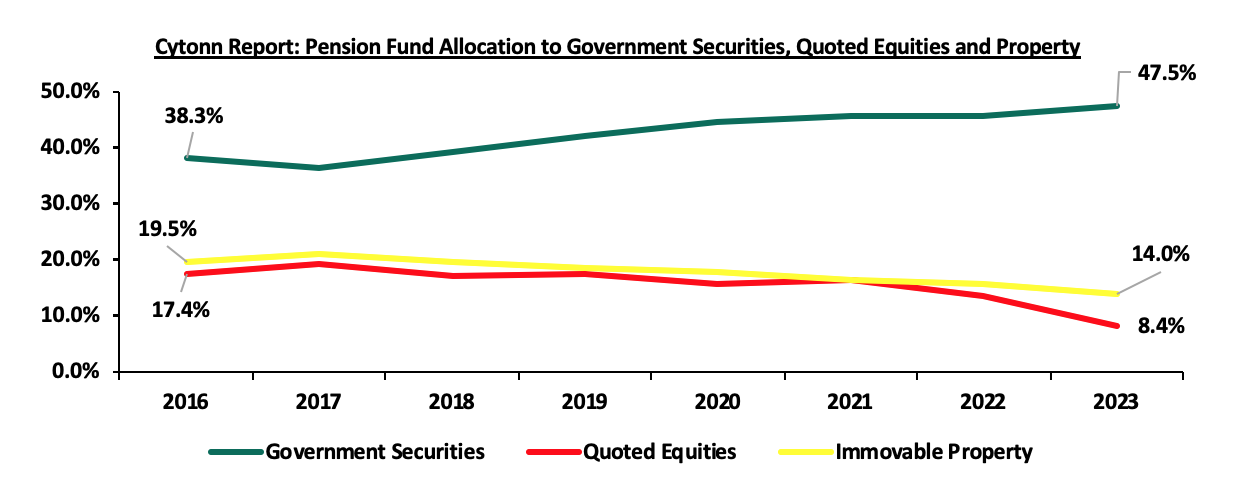

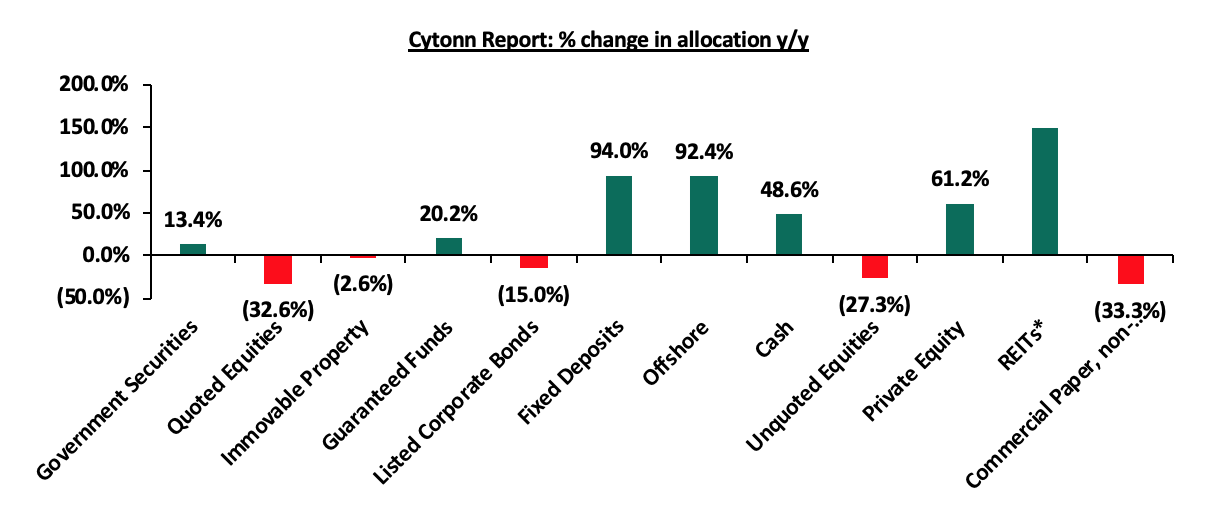

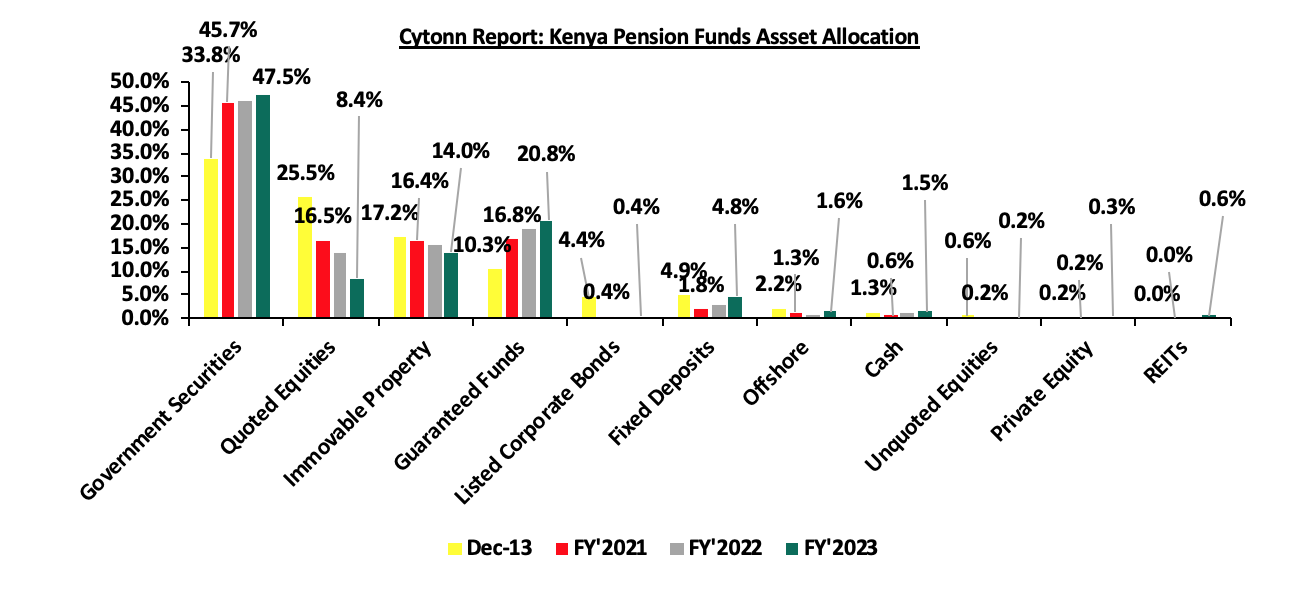

According to the Retirement Benefits Authority (RBA) Industry report for December 2023, assets under management for retirement benefits schemes increased by 9.4% to Kshs 1.7 tn in December 2023 from the Kshs 1.6 tn recorded in 2022. The growth of the assets can be attributed to the enhanced contributions to the mandatory scheme, NSSF, which began in earnest in February 2023 following the court of appeal ruling that set aside the initial ruling of the Employment and Labour Relations Court which had suspended implementation of the NSSF Act. The Act, which increased the contribution rates from Kshs 400 to 12.0% of an employee’s monthly earnings, with a 6% deduction from the employee and an equivalent 6% deduction from the employer, had been rendered unconstitutional by the lower court. Despite the continued growth, Kenya remains characterized by a low saving culture with research by the Federal Reserve Bank showing that only 14.2% of the adult population in the labor force save, including for their retirement in Retirement Benefits Schemes (RBSs), lower than Nigeria’s 26.3%, but higher than South Africa’s 13.6%. According to the World Bank, our gross savings to GDP stands at just 16.0%, indicating that more still needs to be done to boost the savings numbers. On a semi-annual basis, however, the assets grew by a paltry 1.3% to Kshs 1.73 tn in December from the Kshs 1.70 tn recorded in June 2023. This subdued growth of assets under management during the period is majorly attributed to negative movement in some asset classes such as quoted equities, listed corporate bonds, unquoted equities, and commercial papers. Quoted equities, for instance, recorded a 3.0% decline in Q4’2023;

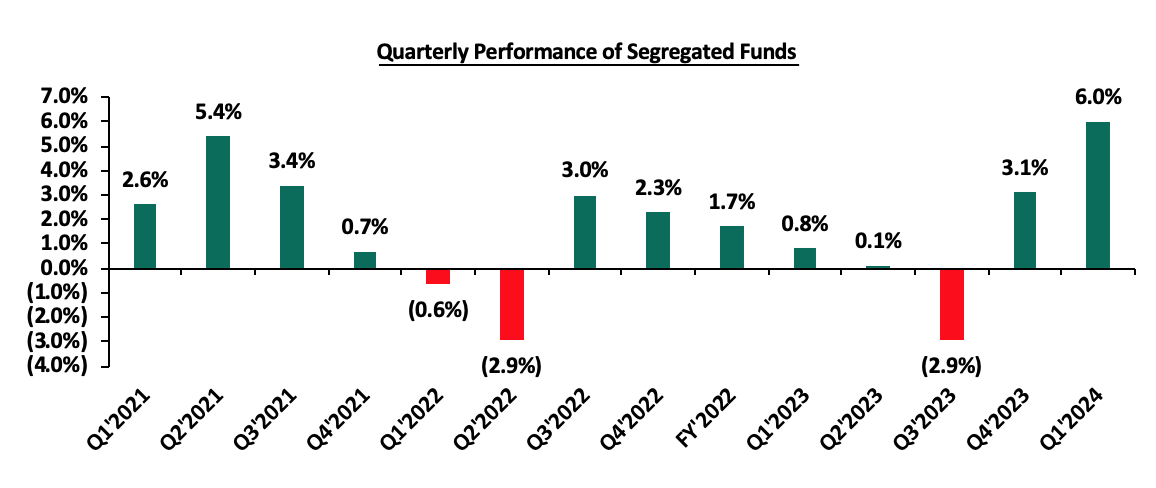

On a separate note, according to the ACTSERV Q1’2024 Retirement Benefits Schemes Investments Performance Survey, segregated retirement benefits schemes recorded a 6.0% return in Q1’2024, up from the 0.8% recorded in Q1’2023. The increase was largely supported by the performance of equities investments made by the schemes which recorded a significant 25.6% gain, a reversal from the 7.2% decline recorded in 2022, on the back of positive investor sentiment following the successful Eurobond buyback, easing inflation and the shilling appreciation which gradually slowed down investor flight from the market. This week, we shall focus on understanding Retirement Benefits Schemes and look into the historical and current state of retirement benefits schemes in Kenya with a key focus on 2023 and what can be done going forward;

Investment Updates:

- Weekly Rates:

- Cytonn Money Market Fund closed the week at a yield of 17.67% p.a. To invest, dial *809# or download the Cytonn App from Google Play store here or from the Appstore here;

- We continue to offer Wealth Management Training every Monday, from 10:00 am to 12:00 pm. The training aims to grow financial literacy among the general public. To register for any of our Wealth Management Trainings, click here;

- If interested in our Private Wealth Management Training for your employees or investment group, please get in touch with us through wmt@cytonn.com;

- Cytonn Insurance Agency acts as an intermediary for those looking to secure their assets and loved ones’ future through insurance namely; Motor, Medical, Life, Property, WIBA, Credit and Fire and Burglary insurance covers. For assistance, get in touch with us through insuranceagency@cytonn.com;

- Cytonn Asset Managers Limited (CAML) continues to offer pension products to meet the needs of both individual clients who want to save for their retirement during their working years and Institutional clients that want to contribute on behalf of their employees to help them build their retirement pot. To more about our pension schemes, kindly get in touch with us through pensions@cytonn.com;

Real Estate Updates:

- For more information on Cytonn’s real estate developments, email us at sales@cytonn.com;

- Phase 3 of The Alma is now ready for occupation and the show house is open daily. To join the waiting list to rent, please email properties@cytonn.com;

- For Third Party Real Estate Consultancy Services, email us at rdo@cytonn.com;

- For recent news about the group, see our news section here;

Hospitality Updates:

- We currently have promotions for Staycations. Visit cysuites.com/offers for details or email us at sales@cysuites.com;

Money Markets, T-Bills Primary Auction:

During the week, T-bills were oversubscribed for the fourth consecutive week, with the overall oversubscription rate coming in at 100.1%, albeit lower than the oversubscription rate of 194.8% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 7.1 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 177.6%, significantly lower than the oversubscription rate of 325.4% recorded the previous week. The subscription rate for the 182-day and 364-day papers decreased to 116.5% and 52.8% from 180.4% and 156.8% respectively recorded the previous week. The government accepted a total of Kshs 23.7 bn worth of bids out of Kshs 24.0 bn bids received, translating to an acceptance rate of 98.7%. The yields on the government papers were on an upward trajectory, with the yields on the 91-day, 182-day, and 364-day papers increasing by 0.8 bps, 4.6 bps, and 9.4 bps to 15.95%, 16.56%, and 16.62% from 15.94%, 16.52% and 16.53% respectively recorded the previous week. The chart below shows the yield growth rate for the 91-day paper over the period:

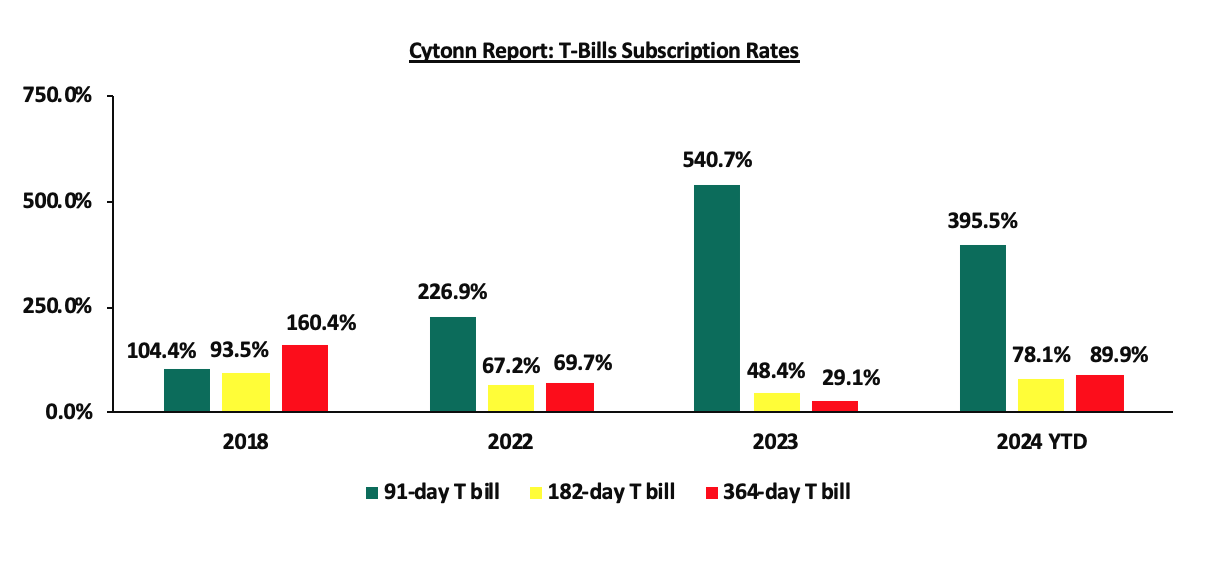

The chart below compares the overall average T-bill subscription rates obtained in 2018, 2022, 2023, and 2024 Year-to-date (YTD):

Money Market Performance:

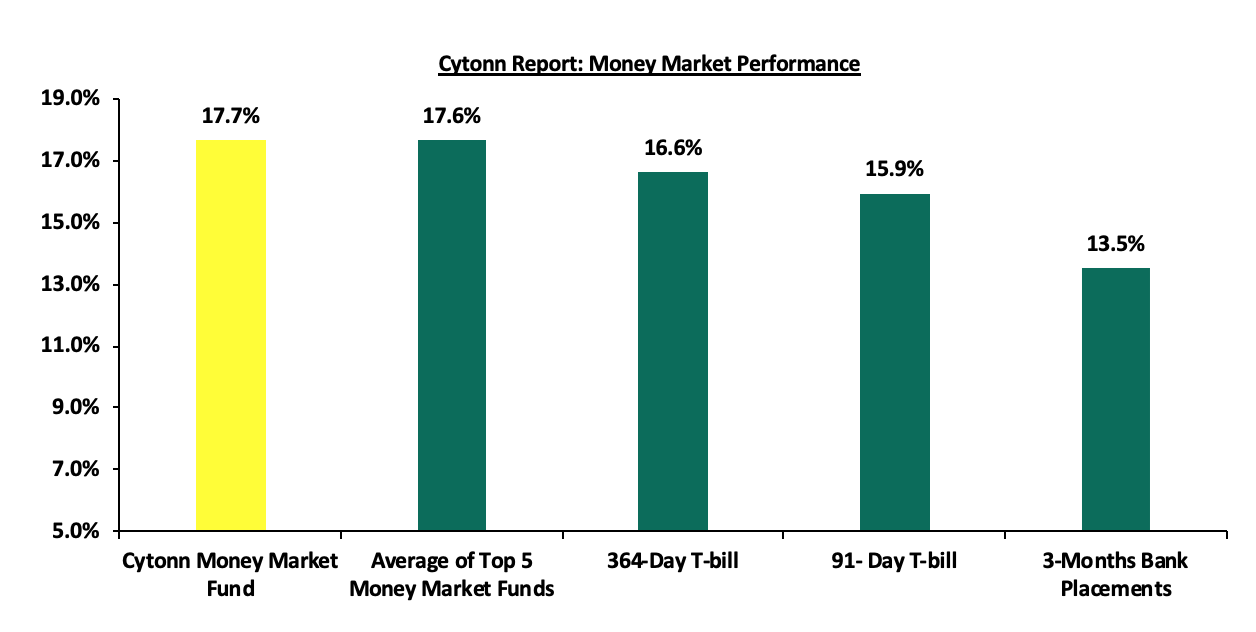

In the money markets, 3-month bank placements ended the week at 13.5% (based on what we have been offered by various banks), and the yields on the government papers were on an upward trajectory, with the yields on the government papers were on an upward trajectory, with the yields on the 91-day and 364-day papers increasing by 0.8 bps and 9.4 bps to 15.95% and 16.62% from 15.94% and 16.53% respectively recorded the previous week. The yields on the Cytonn Money Market Fund increased by 60.0 bps to 17.7% from 17.1% recorded the previous week, while the average yields on the Top 5 Money Market Funds increased by 28.8 bps to 17.6% from the 17.4% recorded the previous week.

The table below shows the Money Market Fund Yields for Kenyan Fund Managers as published on 24th May 2024:

|

Cytonn Report: Money Market Fund Yield for Fund Managers as published on 24th May 2024 |

||

|

Rank |

Fund Manager |

Effective Annual Rate |

|

1 |

Lofty-Corban Money Market Fund |

18.3% |

|

2 |

Etica Money Market Fund |

18.1% |

|

3 |

Cytonn Money Market Fund (Dial *809# or download the Cytonn App) |

17.7% |

|

4 |

Kuza Money Market fund |

17.5% |

|

5 |

Nabo Africa Money Market Fund |

16.6% |

|

6 |

GenAfrica Money Market Fund |

16.4% |

|

7 |

Jubilee Money Market Fund |

15.9% |

|

8 |

Enwealth Money Market Fund |

15.9% |

|

9 |

Apollo Money Market Fund |

15.8% |

|

10 |

Madison Money Market Fund |

15.7% |

|

11 |

Co-op Money Market Fund |

15.6% |

|

12 |

KCB Money Market Fund |

15.6% |

|

13 |

GenCap Hela Imara Money Market Fund |

15.6% |

|

14 |

Absa Shilling Money Market Fund |

15.4% |

|

15 |

Mali Money Market Fund |

15.3% |

|

16 |

Sanlam Money Market Fund |

15.3% |

|

17 |

AA Kenya Shillings Fund |

15.2% |

|

18 |

Mayfair Money Market Fund |

14.9% |

|

19 |

Dry Associates Money Market Fund |

14.0% |

|

20 |

Equity Money Market Fund |

13.9% |

|

21 |

Orient Kasha Money Market Fund |

13.9% |

|

22 |

Old Mutual Money Market Fund |

13.4% |

|

23 |

CIC Money Market Fund |

13.2% |

|

24 |

ICEA Lion Money Market Fund |

12.3% |

|

25 |

British-American Money Market Fund |

10.1% |

Source: Business Daily

Liquidity:

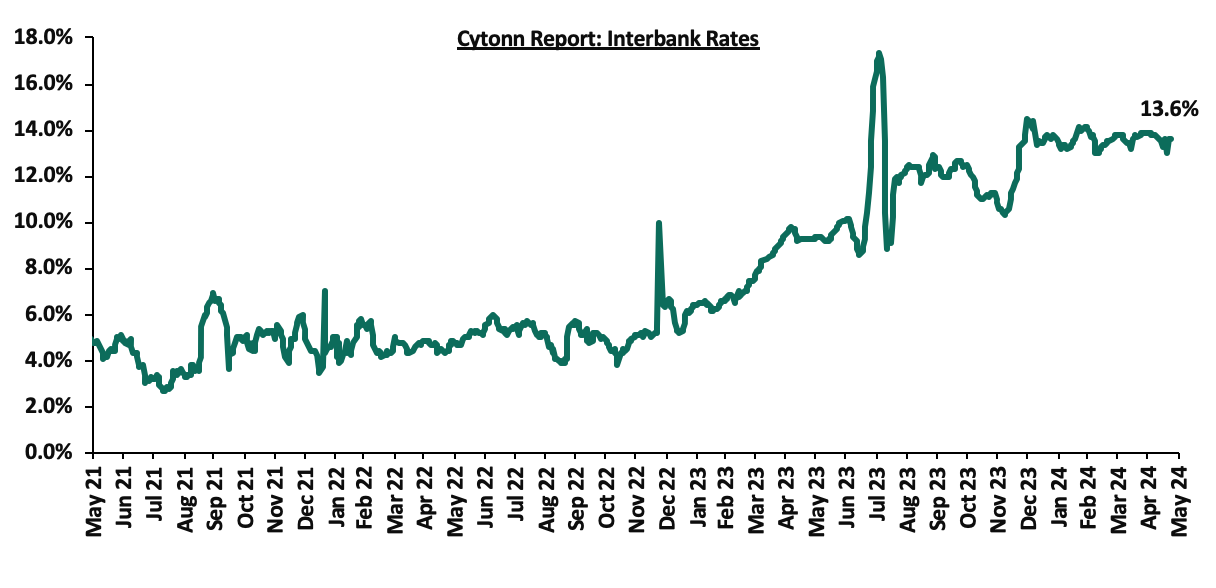

During the week, liquidity in the money markets eased, with the average interbank rate decreasing marginally by 0.8 bps, to remain relatively unchanged at 13.5% recorded the previous week, partly attributable to government payments that offset tax remittances. The average interbank volumes traded increased by 19.7% to Kshs 22.1 bn from Kshs 18.4 bn recorded the previous week. The chart below shows the interbank rates in the market over the years:

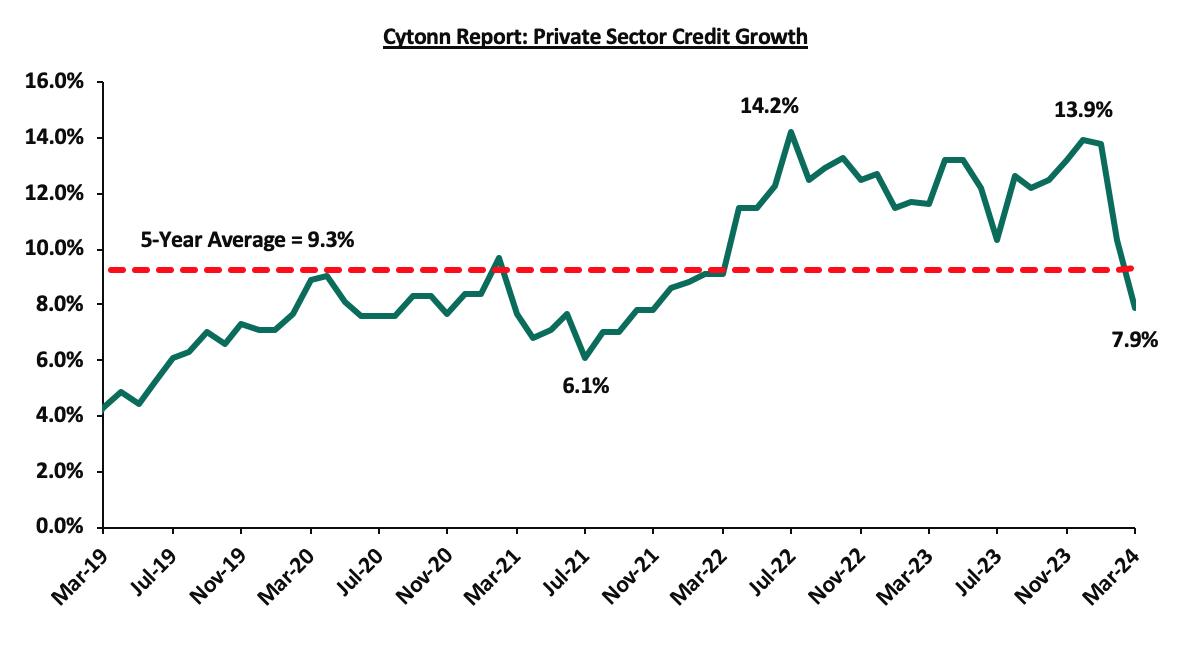

Private Sector Credit Growth:

The Kenyan private sector credit growth declined to 7.9% in March from 10.3% recorded in February 2024. This is partly attributable to the impact of monetary policy tightening following the Monetary Policy Committee’s (MPC) to maintain the Central Bank Rate (CBR) at 13.0% in addition to the effect of exchange rate appreciation on foreign currency. Notably, the 7.9% growth rate recorded in March 2024 is the lowest recorded figure in 28 months and is 1.4% points below the 5-year average growth rate of 9.3%. The chart below shows the movement of the private sector credit growth:

Kenya Eurobonds:

During the week, the yields on Eurobonds were on an upward trajectory, with the yields on the 7-year Eurobond issued in 2019 increasing the most by 53.0 bps to 9.1% from 8.5% recorded the previous week. The table below shows the summary of the performance of the Kenyan Eurobonds as of 23rd May 2024;

|

Cytonn Report: Kenya Eurobonds Performance |

||||||

|

|

2018 |

2019 |

2021 |

2024 |

||

|

Tenor |

10-year issue |

30-year issue |

7-year issue |

12-year issue |

13-year issue |

7-year issue |

|

Amount Issued (USD) |

1.0 bn |

1.0 bn |

0.9 bn |

1.2 bn |

1.0 bn |

1.5 bn |

|

Years to Maturity |

3.8 |

23.8 |

3.0 |

8.0 |

10.1 |

6.8 |

|

Yields at Issue |

7.3% |

8.3% |

7.0% |

7.9% |

6.2% |

10.4% |

|

1-Jan-24 |

9.8% |

10.2% |

10.1% |

9.9% |

9.5% |

|

|

1-May-24 |

9.3% |

10.2% |

9.3% |

10.0% |

10.0% |

10.0% |

|

17-May-24 |

8.8% |

9.8% |

8.5% |

9.4% |

9.4% |

9.4% |

|

20-May-24 |

8.8% |

9.8% |

8.6% |

9.4% |

9.5% |

9.4% |

|

21-May-24 |

9.0% |

9.9% |

8.7% |

9.5% |

9.6% |

9.5% |

|

22-May-24 |

9.0% |

10.0% |

8.8% |

9.6% |

9.7% |

9.6% |

|

23-May-24 |

9.2% |

10.1% |

9.1% |

9.8% |

9.8% |

9.8% |

|

Weekly Change |

0.4% |

0.3% |

0.5% |

0.4% |

0.4% |

0.4% |

|

MTD Change |

(0.2%) |

(0.0%) |

(0.2%) |

(0.2%) |

(0.2%) |

(0.2%) |

|

YTD Change |

(0.7%) |

(0.1%) |

(1.0%) |

(0.1%) |

0.3% |

9.8% |

Source: Central Bank of Kenya (CBK) and National Treasury

Kenya Shilling:

During the week, the Kenya Shilling depreciated against the US Dollar by 0.8%, to close at Kshs 131.7, from Kshs 130.7 recorded the previous week. On a year-to-date basis, the shilling has appreciated by 16.1% against the dollar, a contrast to the 26.8% depreciation recorded in 2023.

We expect the shilling to be supported by:

- Diaspora remittances standing at a cumulative USD 4,457.5 mn in the 12 months to April 2024, 11.9% higher than the USD 3,984.9 mn recorded over the same period in 2023, which has continued to cushion the shilling against further depreciation. In the April 2024 diaspora remittances figures, North America remained the largest source of remittances to Kenya accounting for 54.0% in the period, and,

- The tourism inflow receipts which came in at USD 352.5 bn in 2023, a 31.5% increase from USD 268.1 bn inflow receipts recorded in 2022, and owing to tourist arrivals that improved by 27.6% to 182,000 in the 12 months to January 2024, from 151,000 recorded during a similar period in 2023.

The shilling is however expected to remain under pressure in 2024 as a result of:

- An ever-present current account deficit which came at 4.0% of GDP in FY’2023 from 5.1% recorded in FY’2022,

- The need for government debt servicing, continues to put pressure on forex reserves given that 67.3% of Kenya’s external debt was US Dollar denominated as of December 2023, and 72.0% of revenues goes into debt services as of April 2024, and,

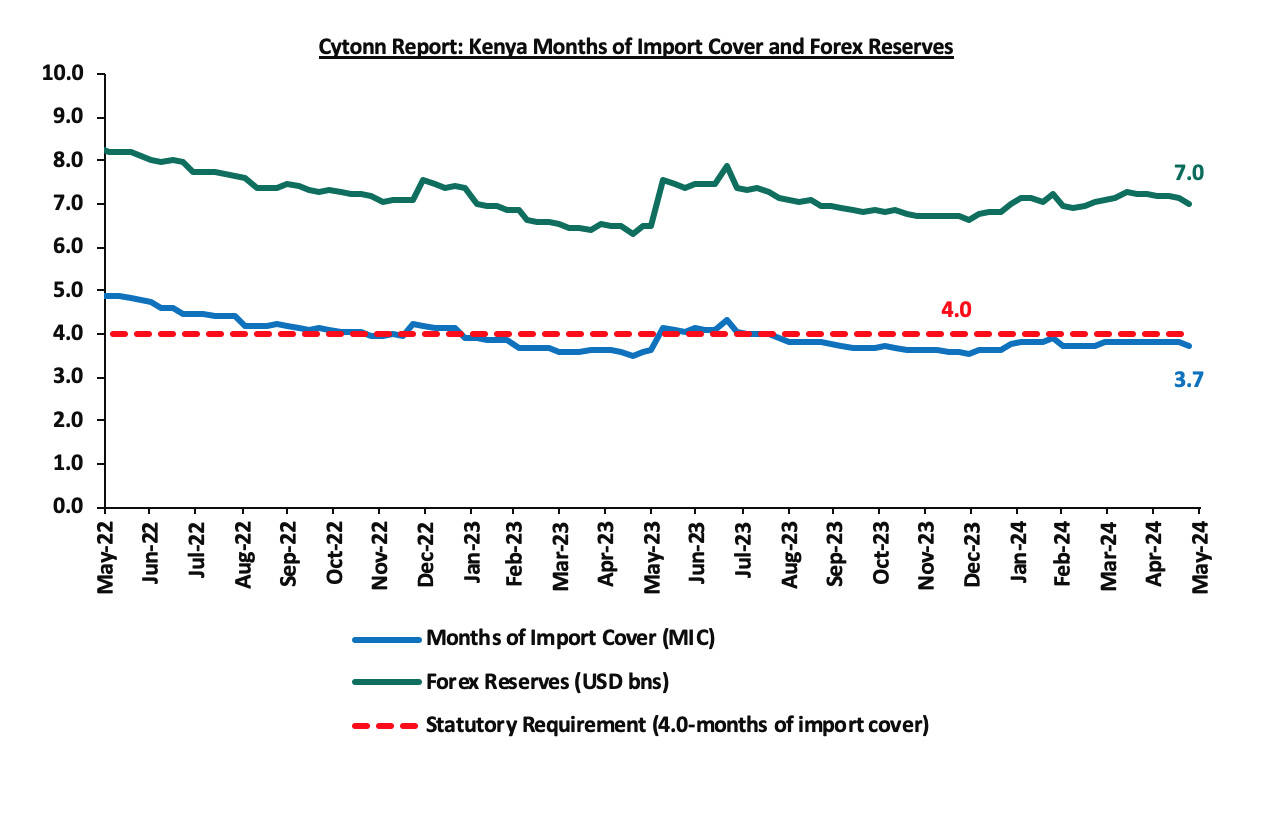

- Dwindling forex reserves, currently at USD 7.0 mn (equivalent to 3.7 months of import cover), which is below the statutory requirement of maintaining at least 4.0 months of import cover.

Key to note, Kenya’s forex reserves decreased by 2.0% during the week to USD 7.0 bn from USD 7.1 bn recorded the previous week, equivalent to 3.7 months of import cover down from 3.8 recorded the previous week, and remained below the statutory requirement of maintaining at least 4.0-months of import cover.

The chart below summarizes the evolution of Kenya's months of import cover over the years:

Weekly Highlights

- Kenya’s FY’2023 Gross Domestic Product (GDP) Growth

During the week, the Kenya National Bureau of Statistics (KNBS) released the 2024 Economic Survey, highlighting that the Kenyan economy recorded a 5.6% growth in FY’2023, faster than the 4.9% growth recorded in FY’2022. The main contributor to Kenyan GDP remains to be the Agriculture, Fishing and Forestry sector which grew by 6.5% in FY’2023 compared to a contraction of 1.5% in FY’2022. All sectors in FY’2023, except Mining and Quarrying, recorded positive growths, with varying magnitudes across activities. Most sectors recorded improved growth compared to FY’2022 with Agriculture, Forestry and Fishing, Accommodation and Food Services, and Real Estate Sectors recording the highest growth improvements of 7.9% points, 6.8% points, and 2.8% points, respectively. Other sectors that recorded expansion in growth rate, from what was recorded in FY’2022 were Financial Services Indirectly Measured, Transport and Storage and Health sectors, of 2.5%, 0.3%, and 1.5% points respectively.

The key take-outs from the report include;

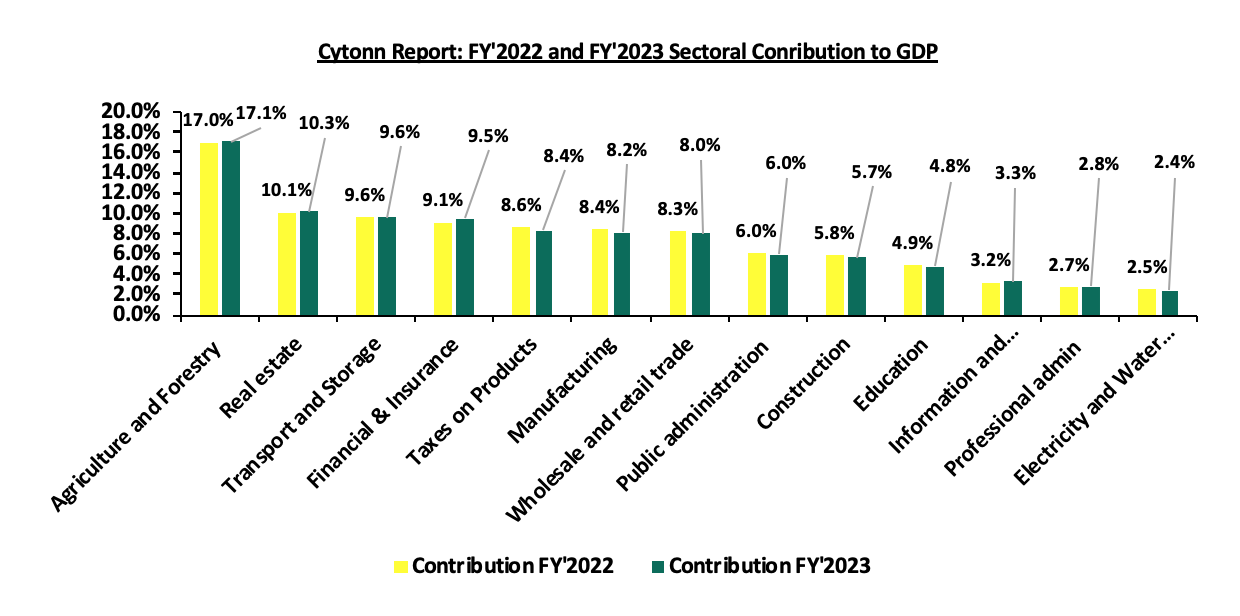

- Sectoral Contribution to Growth - The biggest gainer in terms of sectoral contribution to GDP was the Financial and Insurance sector, increasing by 0.4% points to 9.5% in FY’2023 from 9.1% in FY’2022, while the Manufacturing sector was the biggest loser, declining by 0.3% points to 8.2% in FY’2023, from 8.4% in FY’2022. Real Estate was the second largest contributor to GDP at 10.3% in FY’2023, up from 10.1% recorded in FY’2022, indicating sustained growth. The Accommodation and Food Services sector recorded the highest growth rate in FY’2023 growing by 33.6%, faster than the 26.8% growth recorded in FY’2022. The chart below shows the top contributors to GDP by sector in FY’2023:

Source: KNBS FY’2022 and FY’2023 GDP Report

- Rebound in the Agricultural Sector– Agriculture and Forestry recorded a growth of 6.5% in FY’2023. The performance was an increase of 8.1% points, from the contraction of 1.5% recorded in FY’2022. The positive growth recorded during the quarter was mainly attributable to favourable weather conditions that boosted crop and livestock production. Production of key food crops such as maize, beans, and potatoes increased significantly during the year

- Increased growth in the Transport and Storage Sector: The Transport and Storage sector registered a growth of 0.4% points to 6.2% in FY’2023 compared to the 5.8% in FY’2022. Some of the notable improvements include:

-

- Passenger and freight movements via Standard Gauge Railway (SGR) grew by 14.1% and 7.3% to 2,729 thousand passengers and 6,533.0 thousand tonnes, respectively, in 2023 from 2,392 thousand passengers and 6,088.5 thousand tonnes respectively in 2022,

- The total passenger air traffic expanded by 19.2% to 12,205.8 thousand passengers from 10,239.7 thousand passengers recorded in 2022, and,

- The volume of cargo traffic handled at the Port of Mombasa grew by 6.2% to 35,978 thousand metric tonnes in 2023 from 33,880 thousand metric tonnes in 2022.

- Decelerated growth in the manufacturing sector - The manufacturing sector recorded a decelerated growth of 2.0% in FY’2023 compared to a 2.6% growth in a similar period of review in 2022. Additionally, the sectoral contribution to GDP decreased to 8.2% in FY’2023, from 8.4% recorded in FY’2022.

- Significant growth in the Accommodation and Food Service sector: Accommodation and Food Services sector recorded the highest growth rate among all the sectors in FY’2023, having expanded by 6%, higher than the 26.8% recorded in FY’2022. Additionally, the contribution to GDP increased by 0.3% points, to 1.3% in FY’2023, compared to 1.0% recorded in FY’2022.

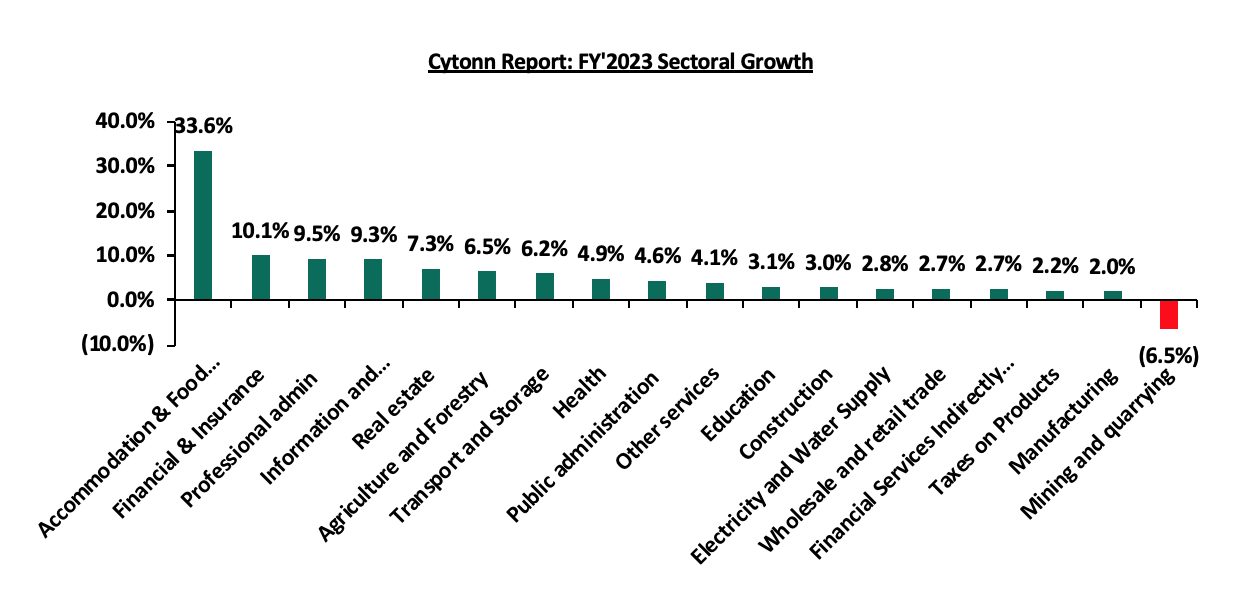

The chart below shows the different sectoral GDP growth rates for FY’2023

Source: KNBS FY’2023 GDP Report

In the near-term, we expect the economy to grow at a slower pace given the restrained business as a result of the difficult economic environment caused by increasing taxes, and an overall rise in the cost of living. Additionally, the Central Bank of Kenya’s Monetary Policy Committee’s (MPC) decision on 3rd April 2024 to maintain the Central Bank Rate (CBR) at 13.0% in a bid to curb inflation and maintain price stability is expected to curtail economic growth. The higher CBR is set to maintain the cost of credit issued by lenders high, hence discouraging borrowing, which will in turn lead to reduced investment spending in the economy by both individuals and businesses. Additionally, the inflation in the country remains within the Central Bank’s range of 2.5%-7.5%, and risks going high mainly on the back of a possible increase in fuel prices due to an increase in international fuel prices resulting from geo-political tensions. Thus, the consumer purchasing power remains low, resulting in reduced demand for goods and services and consequentially slowed economic growth. However, we expect the agricultural sector to continue backing economic growth in the country, as the country continues to experience sufficient rain during the year. The sector remains Kenya’s largest contributor to GDP, as well as food prices being a major contributor to headline inflation. Additionally, we expect we expect the economy to benefit from the strengthening Shilling and the ease in inflationary pressures.

For a more detailed analysis, see our FY’2023 GDP Note.

- Kenya’s FY’2023 Balance of Payments (BOP)

Kenya’s balance of payment (BoP) position improved by 46.4% in FY’2023, with the deficit narrowing to Kshs 134.8 bn, from a deficit of Kshs 251.5 bn in FY’2022, and a slight deterioration from the deficit of Kshs 131.5 bn recorded in Q3’2023. The y/y positive performance in BoP was mainly driven by a 13.0% improvement in the current account balance to a deficit of Kshs 603.7 bn in FY’2023, from a deficit of Kshs 694.2 bn in FY’2022, and the 4.6% increase in capital account balance to Kshs 17.3 bn from Kshs 16.5 bn recorded in a similar period in 2022. The performance was however weighed down by a 21.2% decrease in the financial account balance to a surplus of Kshs 384.7 bn from a surplus of Kshs 488.4 bn in FY’2022. The table below shows the breakdown of the various balance of payments components, comparing FY’2023 and FY’2022:

|

Cytonn Report: Kenya’s Balance of Payments |

||||

|

Item |

FY'2022 |

Q3'2023 |

FY'2023 |

Y/Y % Change |

|

Current Account Balance |

(694.2) |

(122.5) |

(603.7) |

(13.0%) |

|

Capital Account Balance |

16.5 |

3.4 |

17.3 |

4.6% |

|

Financial Account Balance |

488.4 |

(20.6) |

384.7 |

(21.2%) |

|

Net Errors and Omissions |

(62.3) |

8.3 |

66.9 |

(207.5%) |

|

Balance of Payments |

(251.5) |

(131.5) |

(134.8) |

(46.4%) |

All values in Kshs bns

Key take-outs from the table include;

- The current account deficit (value of goods and services imported exceeds the value of those exported) narrowed by 13.0% to Kshs 603.7 bn, from Kshs 694.2 bn in FY’2022, mainly attributable to a 0.3% improvement in the merchandise trade balance deficit to Kshs 1,401.6 bn, from Kshs 1,405.4 bn recorded in FY’2022,

- The financial account balance deficit (the difference between the foreign assets purchased by domestic buyers and the domestic assets purchased by the foreign buyers) recorded a surplus of Kshs 384.7 bn in FY’2023, a decrease of 21.2% from the surplus of Kshs 488.4bn recorded in FY’2022. Notably, reserve assets were depleted by Kshs 80.4 bn, and the government received Kshs 54.5 bn from the International Monetary Fund (IMF), a 27.7% decline from Kshs 75.3 bn in 2022, and,

- Consequently, the Balance of Payments (BoP) position improved to a deficit of Kshs 134.8 bn in FY’2023, from a deficit of Kshs 251.5 bn recorded in FY’2022.

Current Account Balance

Kenya’s current account deficit narrowed by 13.0% to Kshs 603.7 bn in FY’2023 from the Kshs 694.2 bn deficit recorded in FY’2022. The y/y contraction registered was driven by:

- The contraction of the merchandise trade (a scenario where imports are greater than exports of goods resulting in a negative net foreign investment) by 0.3% to Kshs 1,401.6 bn in FY’2023, from Kshs 1,405.4 bn recorded in FY’2022, and,

- A 27.2% improvement in the secondary income (transfer) balance to a surplus of Kshs 977.9 bn from a surplus of Kshs 768.8 bn in FY’2022.

The table below shows the breakdown of the various current account components, comparing FY’2022 and FY’2023:

|

Cytonn Report: Kenya’s Current Account Balance |

|||

|

Item |

FY'2022 |

FY'2023 |

Y/Y % Change |

|

Merchandise Trade Balance |

(1,405.4) |

(1,401.6) |

(0.3%) |

|

Services Trade Balance |

149.9 |

84.2 |

(43.9%) |

|

Primary Income Balance |

(207.4) |

(263.9) |

27.2% |

|

Secondary Income (transfer) Balance |

768.8 |

977.6 |

27.2% |

|

Current Account Balance |

(694.2) |

(603.7) |

(13.0%) |

All values in Kshs bns

Kenya's balance of payments improved in FY'2023, mainly on the back of a 13.0% improvement in the current account to a deficit of Kshs 603.7 bn in 2023, from a deficit of Kshs 694.2 bn in 2022 reflecting significant improvements in the country's external economic position. This positive shift was primarily driven by a 0.3% contraction in the merchandise trade deficit, occasioned by robust growth in merchandise exports, notably in horticulture and tea, coupled with a favourable exchange rate movement due to the depreciation of the Kenyan Shilling. Additionally, the secondary income balance saw a substantial increase, bolstered by strong growth in diaspora remittances. Looking ahead, the outlook for Kenya's current account is optimistic, as continued growth in key export sectors and sustained diaspora remittances are expected to further improve the current account balance. Efforts to diversify exports and enhance value addition in agricultural products, along with prudent fiscal and monetary policies, will be crucial in sustaining this positive trajectory. Furthermore, the ongoing strengthening of the Kenyan Shilling against most trading currencies is expected to lower the import bill hence narrowing the current account deficit. We expect that the current administration’s focus on fiscal consolidation will improve the balance of payments performance by minimizing the costs of servicing external debts. Additionally, the favorable weather conditions are set to boost agricultural production in the country, thereby increasing the export of agricultural products, and supporting the current account. We anticipate that the balance of payments will be more stable with the help of multiple trade agreements, such as the one between Kenya and the EU and the one among the EAC, SADC, and COMESA, as the agreements will boost the amount and variety of exports that are needed and offer more opportunities to sell them.

For a more detailed analysis, see our FY’2023 BOP Note

- May 2024 Inflation Projection

We are projecting the y/y inflation rate for May 2024 to come in at the range of 4.7% - 5.1% mainly on the back of:

- Reduced Fuel Prices – The prices for Super Petrol, Diesel, and Kerosene decreased by Kshs 1.0, Kshs 1.2, and Kshs 1.3 each respectively, and will retail at Kshs 192.8, Kshs 179.2, and Kshs 168.7 per litre respectively from the April 2024 prices of Kshs 193.8, Kshs 180.4 and Kshs 170.0 respectively according to the latest EPRA report, following the government's efforts to stabilize pump prices through the petroleum pump price stabilization mechanism which has so far expended Kshs 9.9 bn in the FY’2023/24 to cushion the increases applied to the petroleum pump prices. This decline in fuel prices is likely to contribute to the easing of inflationary pressures as it provides a stabilizing effect on consumer purchasing power as well as business operational costs since fuel is a major input cost for businesses,

- The maintenance of the Central Bank Rate (CBR) at 13.0% – In February this year, the monetary policy committee noted that there was need to tighten the monetary policy following the sustained depreciation of the Kenyan shilling as well as the heightened inflationary pressures which came in at 6.9% in the month of January, 0.3% points increase from the 6.6% in December and remaining within the upper bound of the inflation target range of 2.5% to 7.5%. In line with this, the committee increased the CBR by 50 bps to 13.00% from 12.50% in February. Additionally, on 3rd April 2024, the monetary policy committee decided to maintain the CBR at 13.0% to give the new rate time to take further effect in the economy, with inflation easing to 5.0% in April from 5.7% recorded in March 2024. Raising the CBR increases interest rates, which in turn reduces borrowing and spending, helping to curb inflation by cooling down demand in the economy.

- Strengthening of the Kenya Shilling against the US Dollar – The Kenya Shilling has recorded a 1.2% month-to-date gain to Kshs 131.7 as of 24th May 2024 from the Kshs 133.3 recorded at the beginning of the month in addition to the 16.1% year-to-date gain from the Kshs 157.0 recorded at the beginning of the year. This can be attributed to the recent buyback of the USD 2.0 bn Eurobond, alleviating the debt-risk on the country, the inflows from foreign loans and the infrastructure bond, which increased dollar supply in the economy coupled with the monetary policy committee’s decision to maintain the CBR at 13.0%. This gain in the exchange rate is expected to ease inflation further on the back of reduced import and input prices, and,

- Reduction in electricity prices – In April, EPRA announced a Kshs 3.3 decrease per unit in electricity consumer prices on the back of a reduction in the cost of fuel as a result of the strengthening of the Shilling against the dollar, with the Fuel Energy Cost decreasing to Kshs 3.3 from Kshs 4.7 and the foreign exchange rate fluctuation decreasing to Kshs 2.0 in April from Kshs 3.7 per unit in March. With electricity being one of the major inputs of inflation, this decline is expected to reduce production costs for businesses as well as reduce electricity costs for households thus easing inflation.

Going forward, we expect inflationary pressures to alleviate in the short term, while remaining in the CBK’s target range of 2.5%-7.5% aided by the strengthening of the Kenya shilling against the US Dollar, which has continued to contribute to a reduction in fuel prices. Furthermore, the decision to maintain the CBR at 13.0% during the latest MPC meeting is meant to continue reducing money supply, in turn easing inflation as well as support the exchange rate. We also anticipate that government initiatives to subsidize key inputs in agricultural production, such as fertilizers, will drive down the costs of farming inputs and support the easing of inflation in the long term.

Rates in the Fixed Income market have been on an upward trend given the continued high demand for cash by the government and the occasional liquidity tightness in the money market. The government is 21.7% ahead of its prorated net domestic borrowing target of Kshs 370.1 bn, and 10.7% ahead of the total domestic net borrowing target of Kshs 407.0 bn for FY’2023/2024, having a net borrowing position of Kshs 450.4 bn. However, we expect a downward readjustment of the yield curve in the short and medium term, with the government looking to increase its external borrowing to maintain the fiscal surplus, hence alleviating pressure in the domestic market. As such, we expect the yield curve to normalize in the medium to long-term and hence investors are expected to shift towards the long-term papers to lock in the high returns.

Market Performance:

During the week, the equities market was on an upward trajectory, with NSE 10 gaining the most by 4.0%, while NASI, NSE 25, and NSE 20 gained by 2.3%, 2.7%, and 0.7% respectively, taking the YTD performance to gains of 29.2%, 24.5%, 23.0% and 13.8% for NSE 10, NSE 25, NASI and NSE 20 respectively. The equities market performance was driven by gains recorded by large-cap stocks such as KCB Group, NCBA, and Cooperative Bank of 10.4%, 7.2%, and 4.3% respectively. The performance was, however, weighed down by losses recorded by large-cap stocks such as Stanbic Bank of 12.8%;

During the week, equities turnover increased significantly by 151.2% to USD 16.9 mn from USD 6.7 mn recorded the previous week, taking the YTD total turnover to USD 219.6 mn. Foreign investors became net buyers with a net buying position of USD 4.1 mn, from a net selling position of USD 0.02mn recorded the previous week, taking the YTD foreign net selling position to USD 3.6 mn.

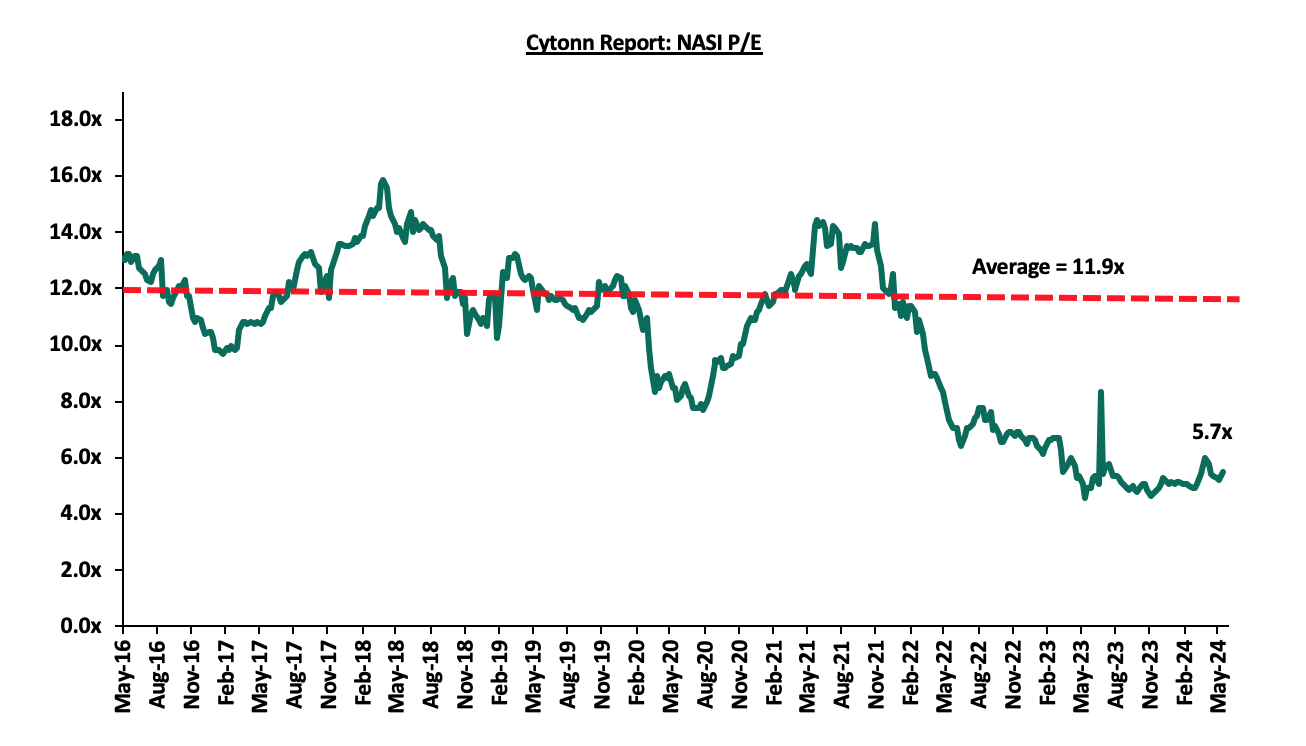

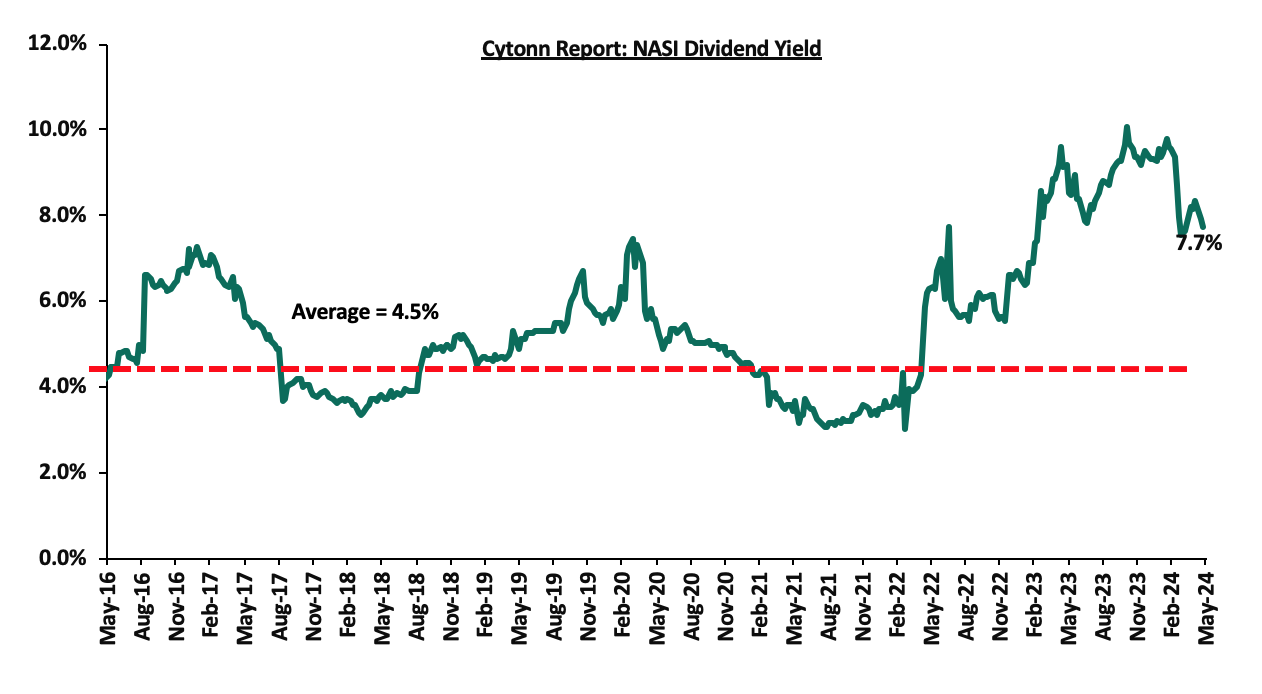

The market is currently trading at a price-to-earnings ratio (P/E) of 5.7x, 52.3% below the historical average of 11.9x. The dividend yield stands at 7.7%, 3.2% points above the historical average of 4.5%. Key to note, NASI’s PEG ratio currently stands at 0.7x, an indication that the market is undervalued relative to its future growth. A PEG ratio greater than 1.0x indicates the market is overvalued while a PEG ratio less than 1.0x indicates that the market is undervalued. The charts below indicate the historical P/E and dividend yields of the market:

Universe of Coverage:

|

Cytonn Report: Equities Universe of Coverage |

|||||||||

|

Company |

Price as at 17/05/2024 |

Price as at 24/05/2024 |

w/w change |

YTD Change |

Target Price* |

Dividend Yield |

Upside/ Downside** |

P/TBv Multiple |

Recommendation |

|

Stanbic Holdings |

124.8 |

108.8 |

(12.8%) |

2.6% |

145.3 |

14.1% |

47.7% |

0.7x |

Buy |

|

Jubilee Holdings |

176.0 |

184.8 |

5.0% |

(0.1%) |

260.7 |

6.5% |

47.6% |

0.3x |

Buy |

|

NCBA*** |

38.3 |

41.1 |

7.2% |

5.7% |

55.2 |

11.6% |

46.0% |

0.8x |

Buy |

|

Sanlam |

6.4 |

6.2 |

(2.5%) |

3.7% |

8.8 |

0.0% |

41.7% |

1.8x |

Buy |

|

Co-op Bank*** |

12.8 |

13.3 |

4.3% |

17.2% |

17.2 |

11.3% |

40.6% |

0.6x |

Buy |

|

Diamond Trust Bank*** |

50.0 |

50.0 |

0.0% |

11.7% |

65.2 |

10.0% |

40.4% |

0.2x |

Buy |

|

ABSA Bank*** |

13.0 |

13.5 |

4.2% |

16.9% |

17.3 |

11.5% |

39.6% |

1.1x |

Buy |

|

Equity Group*** |

44.9 |

46.5 |

3.7% |

36.0% |

60.2 |

8.6% |

38.1% |

0.9x |

Buy |

|

Standard Chartered*** |

185.0 |

187.0 |

1.1% |

16.7% |

225.2 |

15.5% |

35.9% |

1.3x |

Buy |

|

Kenya Reinsurance |

2.0 |

2.0 |

0.0% |

8.1% |

2.5 |

10.0% |

35.5% |

0.2x |

Buy |

|

I&M Group*** |

18.1 |

18.6 |

2.5% |

6.3% |

22.5 |

13.7% |

35.0% |

0.4x |

Buy |

|

CIC Group |

2.3 |

2.2 |

(1.3%) |

(3.1%) |

2.8 |

5.9% |

32.0% |

0.7x |

Buy |

|

KCB Group*** |

31.9 |

35.2 |

10.4% |

60.1% |

45.7 |

0.0% |

29.9% |

0.5x |

Buy |

|

Britam |

5.6 |

5.4 |

(3.2%) |

5.4% |

6.5 |

0.0% |

19.9% |

0.7x |

Accumulate |

|

Liberty Holdings |

5.5 |

5.6 |

1.8% |

45.1% |

6.1 |

6.7% |

15.6% |

0.4x |

Accumulate |

|

HF Group |

4.3 |

4.2 |

(3.7%) |

20.9% |

4.6 |

0.0% |

9.2% |

0.2x |

Hold |

Weekly Highlights

Earnings Release

- KCB Group’s Q1’2024 Financial Performance

During the week, KCB Bank Kenya released their Q1’2024 financial results. Below is a summary of the performance:

|

Balance Sheet Items |

Q1’2023 |

Q1’2024 |

y/y change |

|

Government Securities |

252.1 |

351.9 |

39.6% |

|

Net Loans and Advances |

928.8 |

1,017.4 |

9.5% |

|

Total Assets |

1,630.6 |

1,996.2 |

22.4% |

|

Customer Deposits |

1,196.6 |

1,501.0 |

25.4% |

|

Deposits per branch |

2.0 |

2.5 |

27.3% |

|

Total Liabilities |

1,415.8 |

1,757.6 |

24.1% |

|

Shareholders’ Funds |

208.1 |

231.5 |

11.2% |

|

Balance Sheet Ratios |

Q1’2023 |

Q1’2024 |

% points change |

|

Loan to Deposit Ratio |

77.6% |

67.8% |

(9.8%) |

|

Government Securities to Deposit Ratio |

21.1% |

23.4% |

2.4% |

|

Return on average equity |

20.9% |

20.1% |

(0.8%) |

|

Return on average assets |

2.9% |

2.4% |

(0.5%) |

|

Income Statement |

Q1’2023 |

Q1’2024 |

y/y change |

|

Net Interest Income |

22.1 |

31.1 |

40.8% |

|

Net non-Interest Income |

14.8 |

17.4 |

17.8% |

|

Total Operating income |

36.9 |

48.5 |

31.6% |

|

Loan Loss provision |

(4.1) |

(6.3) |

53.4% |

|

Total Operating expenses |

(23.0) |

(27.3) |

18.8% |

|

Profit before tax |

13.9 |

21.2 |

52.7% |

|

Profit after tax |

9.8 |

16.5 |

69.0% |

|

Core EPS |

3.0 |

5.1 |

69.0% |

|

Income Statement Ratios |

Q1’2023 |

Q1’2024 |

% points change |

|

Yield from interest-earning assets |

10.2% |

11.6% |

1.4% |

|

Cost of funding |

3.2% |

4.6% |

1.4% |

|

Net Interest Spread |

7.1% |

7.0% |

(0.1%) |

|

Net Interest Margin |

7.3% |

7.4% |

0.1% |

|

Cost of Risk |

11.2% |

13.0% |

1.9% |

|

Net Interest Income as % of operating income |

59.9% |

64.1% |

4.2% |

|

Non-Funded Income as a % of operating income |

40.1% |

35.9% |

(4.2%) |

|

Cost to Income Ratio |

62.4% |

56.4% |

(6.0%) |

|

Cost to Income Ratio (without LLPs) |

51.2% |

43.3% |

(7.9%) |

|

Capital Adequacy Ratios |

Q1’2023 |

Q1’2024 |

% points change |

|

Core Capital/Total Liabilities |

15.0% |

15.6% |

0.6% |

|

Minimum Statutory ratio |

8.0% |

8.0% |

0.0% |

|

Excess |

7.0% |

7.6% |

0.6% |

|

Core Capital/Total Risk Weighted Assets |

13.6% |

17.6% |

4.0% |

|

Minimum Statutory ratio |

10.5% |

10.5% |

0.0% |

|

Excess |

3.1% |

7.1% |

4.0% |

|

Total Capital/Total Risk Weighted Assets |

17.0% |

20.0% |

3.0% |

|

Minimum Statutory ratio |

14.5% |

14.5% |

0.0% |

|

Excess |

2.5% |

5.5% |

3.0% |

|

Liquidity Ratio |

43.7% |

47.9% |

4.2% |

|

Minimum Statutory ratio |

20.0% |

20.0% |

0.0% |

|

Excess |

23.7% |

27.9% |

4.2% |

Key Take-Outs:

- Increased earnings - Core earnings per share (EPS) increased by 69.0% to Kshs 5.1, from Kshs 3.0 in Q1’2023,

- Declined asset quality – The bank’s gross NPL ratio increased to 17.9% in Q1’2024, from 17.1% in Q1’2023, with a 16.3% increase in Gross non-performing loans to Kshs 205.3 bn, from Kshs 176.5 bn in Q1’2023, compared to the 11.2% increase in gross loans to Kshs 1,144.8 bn, from Kshs 1,029.9 bn recorded in Q1’2023, and,

- Improved Lending – The Group’s loan book recorded an expansion of 9.5% to Kshs 1,017.4 bn, from Kshs 928.8 bn in Q1’2023.

For a more detailed analysis, please see the KCB Group’s Q1’2024 Earnings Note

- HF Group‘s Q1’2024 Financial Performance

During the week, HF Group released their Q1’2024 financial results. Below is a summary of the performance:

|

Balance Sheet Items (Kshs bn) |

Q1'2023 |

Q1'2024 |

y/y change |

|

Net loans |

37.0 |

38.1 |

3.1% |

|

Government Securities |

9.5 |

10.1 |

6.4% |

|

Total Assets |

59.0 |

62.3 |

5.6% |

|

Customer Deposits |

41.2 |

43.8 |

6.2% |

|

Deposits Per Branch |

1.9 |

2.0 |

6.2% |

|

Total Liabilities |

50.2 |

53.3 |

6.1% |

|

Shareholder's Funds |

8.8 |

9.0 |

2.4% |

|

Balance Sheet Ratios |

Q1'2023 |

Q1'2024 |

% y/y change |

|

Loan to deposit ratio |

89.7% |

87.1% |

(2.6%) |

|

Government Securities to deposit ratio |

23.0% |

23.1% |

0.1% |

|

Return on Average Equity |

3.8% |

5.1% |

1.3% |

|

Return on Average Assets |

0.6% |

0.8% |

0.2% |

|

Income Statement (Kshs bn) |

Q1'2023 |

Q1'2024 |

y/y change |

|

Net Interest Income |

0.6 |

0.7 |

7.6% |

|

Net non-Interest Income |

0.3 |

0.4 |

40.7% |

|

Total Operating income |

0.9 |

1.1 |

17.7% |

|

Loan Loss provision |

(0.1) |

(0.1) |

7.2% |

|

Total Operating expenses |

(0.8) |

(0.9) |

11.2% |

|

Profit before tax |

0.1 |

0.2 |

76.2% |

|

Profit after tax |

0.1 |

0.2 |

80.4% |

|

Core EPS |

0.2 |

0.4 |

80.4% |

|

Income Statement Ratios |

Q1'2023 |

Q1'2024 |

y/y change |

|

Yield from interest-earning assets |

9.8% |

11.4% |

1.6% |

|

Cost of funding |

4.8% |

6.3% |

1.5% |

|

Net Interest Spread |

5.0% |

5.1% |

0.2% |

|

Net Interest Margin |

5.0% |

5.4% |

0.3% |

|

Cost of Risk |

11.3% |

10.3% |

(1.0%) |

|

Net Interest Income as % of operating income |

69.6% |

63.7% |

(6.0%) |

|

Non-Funded Income as a % of operating income |

30.4% |

36.3% |

6.0% |

|

Cost to Income Ratio (with LLP) |

90.0% |

85.1% |

(5.0%) |

|

Cost to Income Ratio (without LLP) |

78.8% |

74.8% |

(4.0%) |

|

Capital Adequacy Ratios |

Q1'2023 |

Q1'2024 |

% points change |

|

Core Capital/Total Liabilities |

6.7% |

4.5% |

(2.2%) |

|

Minimum Statutory ratio |

8.0% |

8.0% |

0.0% |

|

Excess |

(1.3%) |

(3.5%) |

(2.2%) |

|

Core Capital/Total Risk Weighted Assets |

7.2% |

5.2% |

(2.0%) |

|

Minimum Statutory ratio |

10.5% |

10.5% |

0.0% |

|

Excess |

(3.3%) |

(5.3%) |

(2.0%) |

|

Total Capital/Total Risk Weighted Assets |

11.0% |

8.8% |

(2.2%) |

|

Minimum Statutory ratio |

14.5% |

14.5% |

0.0% |

|

Excess |

(3.5%) |

(5.7%) |

(2.2%) |

|

Liquidity Ratio |

24.7% |

24.9% |

0.2% |

|

Minimum Statutory ratio |

20.0% |

20.0% |

0.0% |

|

Excess |

4.7% |

4.9% |

0.2% |

Key Take-Outs:

- Strong earnings growth - Core earnings per share (EPS) increased by 80.4% to Kshs 0.4 from Kshs 0.2 in Q1’2023,

- Asset quality deterioration – The bank’s gross NPL ratio increased to 24.1% in Q1’2024 from 19.9% in Q1’2023, attributable to the faster growth of 27.6% in Gross non-performing loans to Kshs 11.2 bn in Q1’2024 from Kshs 8.8 bn in Q1’2023, which outpaced the 5.3% increase in gross loans to Kshs 46.5 bn, from Kshs 44.1 bn recorded in Q1’2023, and,

- Sustained Efficiency – Cost to Income Ratio (CIR) improved by 5.0% points to 85.1%, from 90.0% in Q1’2024, owing to the 17.7% increase in total operating income to Kshs 1.1 bn from Kshs 0.9 bn in Q1’2023, which outpaced the 11.2% increase in total operating expenses to Kshs 0.9 bn, from Kshs 0.8 bn in Q1’2023. The cost-to-income ratio without loan loss provisions declined by 4.0% points to 74.8%, from 78.8% in Q1’2023.

For a more detailed analysis, please see the HF Group’s Q1’2024 Earnings Note

- NCBA Group’s Q1’2024 Financial Performance

During the week, NCBA Group released their Q1’2024 financial results. Below is a summary of the performance:

|

Balance Sheet |

Q1'2023 (Kshs bn) |

Q1'2024 (Kshs bn) |

y/y change |

|

Net Loans and Advances |

287.2 |

320.5 |

11.6% |

|

Kenya Government Securities |

207.1 |

178.0 |

(14.0%) |

|

Total Assets |

628.8 |

694.9 |

10.5% |

|

Customer Deposits |

499.7 |

548.1 |

9.7% |

|

Deposits Per Branch |

4.9 |

5.0 |

1.6% |

|

Total Liabilities |

540.9 |

596.1 |

10.2% |

|

Shareholders' Funds |

87.9 |

98.8 |

12.4% |

|

Key Ratios |

Q1'2023 |

Q1'2024 |

% point change |

|

Loan to Deposit ratio |

57.5% |

58.5% |

1.0% |

|

Government Securities to Deposits ratio |

41.4% |

32.5% |

(9.0%) |

|

Return on Average Equity |

18.4% |

23.2% |

4.9% |

|

Return on Average Assets |

2.5% |

3.3% |

0.7% |

|

Income Statement |

Q1'2023 (Kshs bn) |

Q1'2024 (Kshs bn) |

y/y change |

|

Net interest Income |

8.4 |

8.3 |

(1.2%) |

|

Net non-interest income |

7.2 |

7.7 |

7.4% |

|

Total Operating income |

15.5 |

16.0 |

2.8% |

|

Loan loss provision |

2.0 |

1.4 |

(30.9%) |

|

Total Operating expenses |

9.2 |

9.4 |

3.1% |

|

Profit before tax |

6.4 |

6.5 |

2.2% |

|

Profit after tax |

5.1 |

5.3 |

4.7% |

|

Core EPS |

3.1 |

3.2 |

4.7% |

|

Income Statement Ratios |

Q1'2023 |

Q1'2024 |

y/y change |

|

Yield from interest-earning assets |

10.4% |

12.2% |

1.8% |

|

Cost of funding |

4.6% |

6.5% |

1.9% |

|

Net Interest Margin |

6.0% |

6.0% |

0.0% |

|

Net Interest Income as % of operating income |

53.8% |

51.7% |

(2.1%) |

|

Non-Funded Income as a % of operating income |

46.2% |

48.3% |

2.1% |

|

Cost to Income Ratio |

58.9% |

59.1% |

0.2% |

|

Cost to Income without LLP |

46.3% |

50.6% |

4.3% |

|

Capital Adequacy Ratios |

Q1'2023 |

Q1'2024 |

% points change |

|

Core Capital/Total Liabilities |

16.8% |

17.1% |

0.3% |

|

Minimum Statutory ratio |

8.0% |

8.0% |

|

|

Excess |

8.8% |

9.1% |

0.3% |

|

Core Capital/Total Risk Weighted Assets |

17.7% |

18.5% |

0.8% |

|

Minimum Statutory ratio |

10.5% |

10.5% |

|

|

Excess |

7.2% |

8.0% |

0.8% |

|

Total Capital/Total Risk Weighted Assets |

17.8% |

18.6% |

0.8% |

|

Minimum Statutory ratio |

14.5% |

14.5% |

|

|

Excess |

3.3% |

4.1% |

0.8% |

|

Liquidity Ratio |

53.1% |

51.6% |

(1.5%) |

|

Minimum Statutory ratio |

20.0% |

20.0% |

|

|

Excess |

33.1% |

31.6% |

(1.5%) |

Key Take-Outs:

- Increased earnings - Core earnings per share (EPS) grew by 4.7% to Kshs 3.2, from Kshs 3.1 in Q1’2023,

- Improved asset quality – The bank’s gross NPL ratio decreased to 11.7% in Q1’2024, from 12.8% in Q1’2023, attributable to the slower 1.1% increase in Gross non-performing loans to Kshs 40.2 bn, from Kshs 39.7 bn in Q1’2023, compared to the 10.7% increase in gross loans to Kshs 342.9 bn, from Kshs 309.7 bn recorded in Q1’2023, and,

- Reduced Provisioning - On the back of reduced credit risk occasioned by the improving business environment, the bank decreased its provisions holdings meant to cover for anticipated losses in the future, with its general provisions decreasing by 13.3% to Kshs 12.6 bn, from Kshs 14.4 bn recorded in Q1’2023. Further, loan loss provisions expense reduced by 30.9% to Kshs 1.4 bn, from Kshs 2.0 bn recorded in Q1’2023.

For a more detailed analysis, please see the NCBA Group’s Q1’2024 Earnings Note

- I&M Group’s Q1’2024 Financial Performance

During the week, I&M Group released their Q1’2024 financial results. Below is a summary of the performance:

|

Balance Sheet Items |

Q1’2023 |

Q1’2024 |

y/y change |

|

Government Securities |

72.7 |

73.3 |

0.8% |

|

Net Loans and Advances |

257.7 |

291.5 |

13.1% |

|

Total Assets |

473.5 |

533.0 |

12.5% |

|

Customer Deposits |

324.7 |

383.9 |

18.2% |

|

Deposits per Branch |

3.9 |

4.5 |

15.4% |

|

Total Liabilities |

389.1 |

439.3 |

12.9% |

|

Shareholders’ Funds |

79.0 |

87.2 |

10.5% |

|

Balance Sheet Ratios |

Q1’2023 |

Q1’2024 |

% points change |

|

Loan to Deposit Ratio |

79.4% |

75.9% |

(3.4%) |

|

Government Securities to Deposit Ratio |

22.4% |

19.1% |

(3.3%) |

|

Return on average equity |

14.4% |

15.0% |

0.7% |

|

Return on average assets |

2.6% |

2.6% |

0.0% |

|

Income Statement |

Q1’2023 |

Q1’2024 |

y/y change |

|

Net Interest Income |

6.1 |

8.4 |

37.7% |

|

Net non-Interest Income |

3.5 |

3.2 |

(9.4%) |

|

Total Operating income |

9.6 |

11.5 |

20.6% |

|

Loan Loss provision |

(1.6) |

(1.5) |

(6.4%) |

|

Total Operating expenses |

(6.0) |

(6.6) |

10.0% |

|

Profit before tax |

3.7 |

5.1 |

36.2% |

|

Profit after tax |

2.7 |

3.6 |

35.4% |

|

Core EPS |

1.6 |

2.2 |

35.4% |

|

Income Statement Ratios |

Q1’2023 |

Q1’2024 |

% points change |

|

Yield from interest-earning assets |

10.9% |

14.5% |

3.6% |

|

Cost of funding |

4.2% |

6.3% |

2.1% |

|

Net Interest Margin |

6.7% |

8.0% |

1.4% |

|

Net Interest Income as % of operating income |

63.6% |

72.6% |

9.0% |

|

Non-Funded Income as a % of operating income |

36.4% |

27.4% |

(9.0%) |

|

Cost to Income Ratio |

63.0% |

57.5% |

(5.5%) |

|

CIR without LLP |

45.8% |

44.2% |

(1.7%) |

|

Cost to Assets |

0.9% |

1.0% |

0.1% |

|

Capital Adequacy Ratios |

Q1’2023 |

Q1’2024 |

% points change |

|

Core Capital/Total Liabilities |

22.0% |

20.5% |

(1.5%) |

|

Minimum Statutory ratio |

8.0% |

8.0% |

|

|

Excess |

14.0% |

12.5% |

(1.5%) |

|

Core Capital/Total Risk Weighted Assets |

15.6% |

15.0% |

(0.6%) |

|

Minimum Statutory ratio |

10.5% |

10.5% |

|

|

Excess |

5.1% |

4.5% |

(0.6%) |

|

Total Capital/Total Risk Weighted Assets |

19.9% |

18.3% |

(1.7%) |

|

Minimum Statutory ratio |

14.5% |

14.5% |

|

|

Excess |

5.4% |

3.8% |

(1.7%) |

|

Liquidity Ratio |

46.2% |

44.2% |

(2.0%) |

|

Minimum Statutory ratio |

20.0% |

20.0% |

|

|

Excess |

26.2% |

24.2% |

(2.0%) |

Key Take-Outs:

- Strong earnings growth - Core earnings per share increased by 35.4% to Kshs 2.2 from Kshs 1.6 in Q1’2023, mainly driven by 20.6% growth in total operating income to Kshs 11.5 bn in Q1’2024 from Kshs 9.6 bn in Q1’2023. The performance was however weighed down by the 10.0% increase in total operating expenses to Kshs 6.6 bn, from Kshs 6.0 bn in Q1’2023, and,

- Improved Lending – The Group’s loan book recorded an expansion of 13.1% to Kshs 291.5 bn in Q1’2024 from Kshs 257.7 bn in Q1’2023.

For a more detailed analysis, please see the I&M Group’s Q1’2024 Earnings Note

Asset Quality:

The table below shows the asset quality of listed banks that have released their Q1’2024 results using several metrics:

|

Cytonn Report: Listed Banks Asset Quality in Q1’2024 |

||||||

|

|

Q1'2024 NPL Ratio* |

Q1'2023 NPL Ratio** |

% point change in NPL Ratio |

Q1'2024 NPL Coverage* |

Q1’2023 NPL Coverage** |

% point change in NPL Coverage |

|

Stanbic Bank |

8.9% |

11.7% |

(2.9%) |

72.3% |

66.7% |

5.6% |

|

Equity Group |

14.2% |

10.0% |

4.2% |

58.3% |

62.0% |

(3.8%) |

|

Co-operative Bank of Kenya |

15.9% |

14.1% |

1.8% |

58.6% |

62.2% |

(3.6%) |

|

KCB Group |

17.9% |

17.1% |

0.8% |

62.0% |

57.3% |

4.8% |

|

NCBA |

11.7% |

12.8% |

(1.1%) |

55.7% |

56.8% |

(1.0%) |

|

I&M Group |

10.8% |

10.6% |

0.3% |

58.3% |

65.8% |

(7.5%) |

|

HF Group |

24.1% |

19.9% |

4.2% |

74.4% |

81.4% |

(7.0%) |

|

Mkt Weighted Average* |

14.3% |

12.6% |

1.7% |

60.1% |

63.7% |

(3.6%) |

|

*Market cap weighted as at 24/05/2024 |

||||||

|

**Market cap weighted as at 15/06/2023 |

||||||

Key take-outs from the table include;

- Asset quality for the listed banks that have released declined during Q1’2024, with market-weighted average NPL ratio increasing by 1.7% points to 14.3% from 12.6% in Q1’2023, and,

- Market-weighted average NPL Coverage for the listed banks decreased by 3.6% points to 60.1% in Q1’2024 from 63.7% recorded in Q1’2023. The decrease was attributable to I&M Group’s coverage ratio decreasing by 7.5% to 58.3% from 65.8% in Q1’2023, coupled with HF Group’s NPL coverage ratio decreasing by 7.0% points to 74.4% from 81.4% in Q1’2023. The performance was however supported by Stanbic Bank’s NPL Coverage ratio increasing by 5.6% to 72.3% from 66.7% in Q1’2023.

Summary Performance

The table below shows the performance of listed banks that have released their Q1’2024 results using several metrics:

|

Cytonn Report: Listed Banks Performance in Q1’2024 |

||||||||||||||

|

Bank |

Core EPS Growth |

Interest Income Growth |

Interest Expense Growth |

Net Interest Income Growth |

Net Interest Margin |

Non-Funded Income Growth |

NFI to Total Operating Income |

Growth in Total Fees & Commissions |

Deposit Growth |

Growth in Government Securities |

Loan to Deposit Ratio |

Loan Growth |

Return on Average Equity |

|

|

Stanbic |

2.8% |

53.9% |

130.2% |

19.6% |

8.4% |

(34.0%) |

36.9% |

(10.4%) |

22.2% |

(28.4%) |

71.9% |

11.1% |

20.8% |

|

|

Equity |

25.2% |

32.7% |

41.4% |

28.4% |

8.2% |

21.0% |

44.4% |

22.6% |

11.3% |

16.2% |

63.0% |

3.0% |

23.8% |

|

|

COOP Bank |

7.7% |

24.7% |

60.8% |

8.6% |

7.8% |

(0.3%) |

37.7% |

(7.3%) |

14.8% |

11.7% |

78.5% |

5.0% |

19.7% |

|

|

KCB Group |

69.0% |

46.0% |

56.0% |

40.8% |

7.4% |

17.8% |

35.9% |

2.4% |

25.4% |

39.6% |

67.8% |

9.5% |

20.1% |

|

|

NCBA |

4.7% |

29.8% |

70.8% |

(1.2%) |

6.0% |

7.4% |

48.3% |

16.9% |

9.7% |

(14.0%) |

58.5% |

11.6% |

23.2% |

|

|

I&M Group |

35.4% |

53.1% |

76.0% |

37.7% |

8.0% |

(9.4%) |

27.4% |

24.4% |

18.2% |

0.8% |

75.9% |

13.1% |

15.0% |

|

|

HF Group |

80.4% |

28.5% |

52.4% |

7.6% |

5.4% |

40.7% |

36.3% |

56.0% |

6.2% |

6.4% |

87.1% |

3.1% |

5.1% |

|

|

Q1'24 Mkt Weighted Average* |

28.4% |

37.0% |

61.1% |

23.9% |

7.7% |

8.8% |

40.3% |

10.2% |

16.1% |

12.0% |

67.5% |

7.2% |

21.4% |

|

|

Q1'23 Mkt Weighted Average* |

25.0% |

26.2% |

40.2% |

20.1% |

7.3% |

48.1% |

41.3% |

30.0% |

19.0% |

(1.2%) |

73.1% |

19.6% |

22.1% |

|

|

*Market cap weighted as at 24/05/2024 |

||||||||||||||

|

**Market cap weighted as at 15/06/2023 |

||||||||||||||

Key take-outs from the table include:

- The listed banks recorded a 28.4% growth in core Earnings per Share (EPS) in Q1’2024, compared to the weighted average growth of 25.0% in Q1’2023, an indication of improved performance attributable to the improved operating environment experienced during Q1’2024,

- Interest income recorded a weighted average growth of 37.0% in Q1’2024, compared to 26.2% in Q1’2023. Similarly, interest expenses recorded a market-weighted average growth of 61.1% in Q1’2024 compared to a growth of 40.2% in Q1’2023,

- The Banks’ net interest income recorded a weighted average growth of 23.9% in Q1’2024, an increment from the 20.1% growth recorded over a similar period in 2023, while the non-funded income grew by 8.8% in Q1’2024 slower than the 48.1% growth recorded in Q1’2023 despite the revenue diversification strategies implemented by most banks, and,

- The Banks recorded a weighted average deposit growth of 16.1%, lower than the market-weighted average deposit growth of 19.0% in Q1’2023.

We are “Neutral” on the Equities markets in the short term due to the current tough operating environment and huge foreign investor outflows, and, “Bullish” in the long term due to current cheap valuations and expected global and local economic recovery. With the market currently being undervalued for its future growth (PEG Ratio at 0.7x), we believe that investors should reposition towards value stocks with strong earnings growth and that are trading at discounts to their intrinsic value. We expect the current high foreign investors’ sell-offs to continue weighing down the equities outlook in the short term.

- Industry Reports

During the week, the Kenya Bureau of Statistics released the 2024 Economic Survey, which highlighted the performance of various sectors of the economy. The report indicated a general improvement in the hospitality and tourism sectors, with notable gains in the number of international arrivals and monthly bed occupancy. Below is a breakdown of the performance;

- International Arrivals

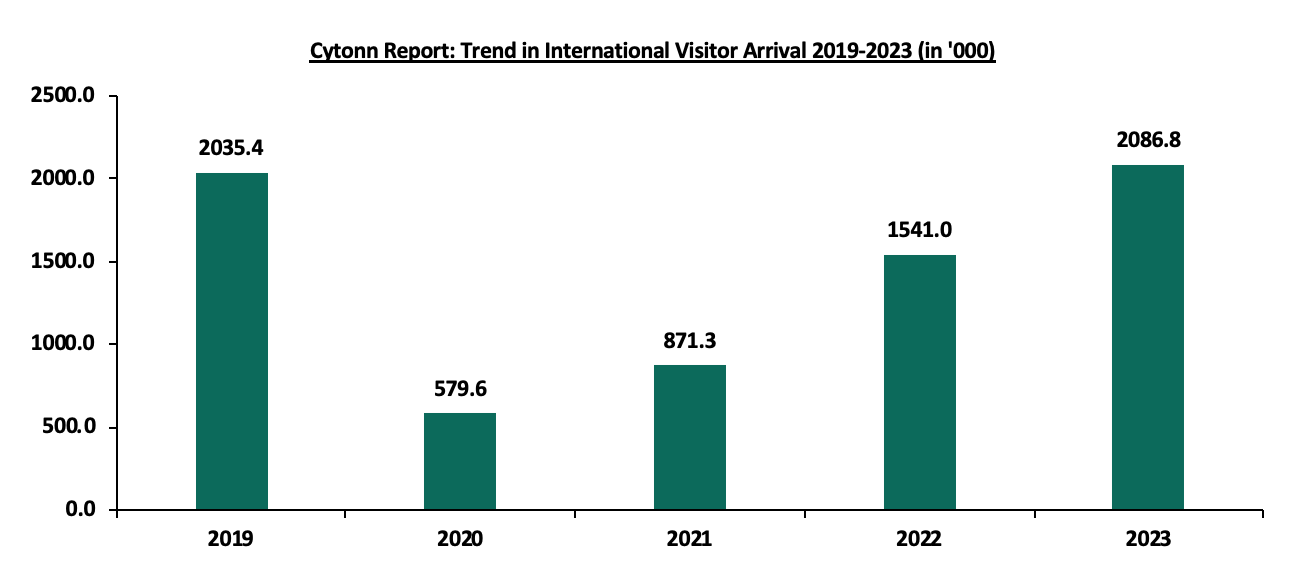

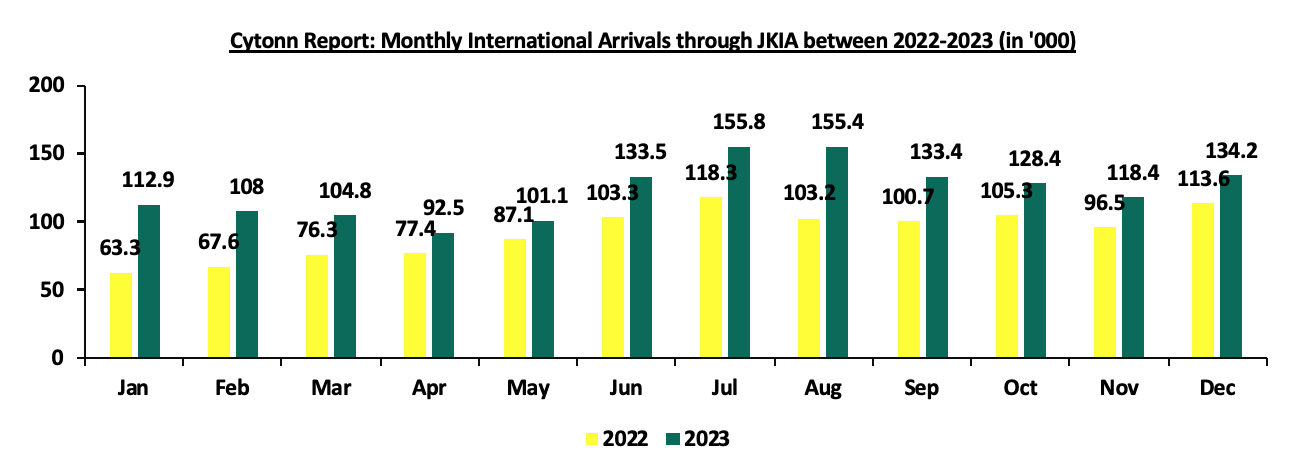

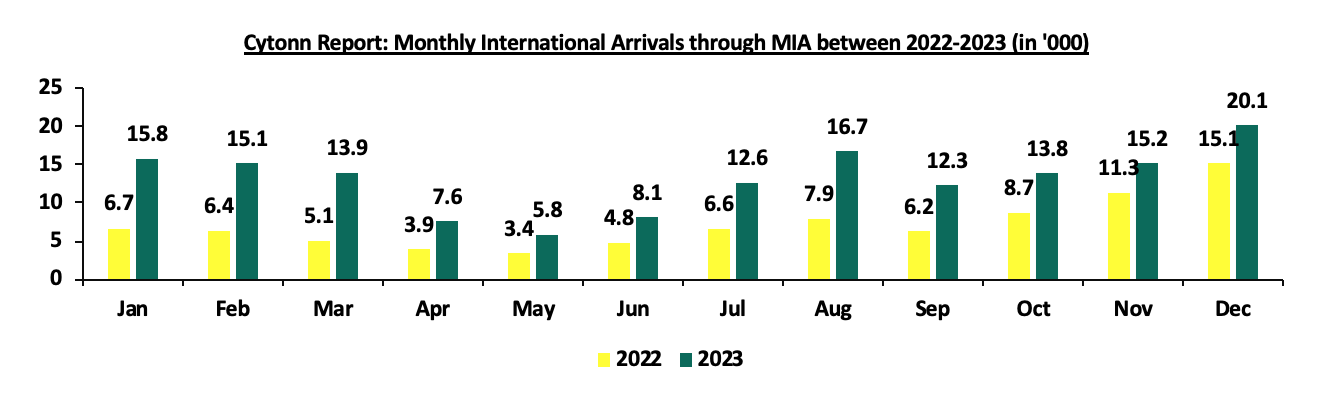

The number of international arrivals grew by 35.4%, reaching 2,086,800 in 2023 from 1,541,000 in 2022. This performance was supported by key developments in the aviation sector, including the introduction of direct flights by three new airlines: IndiGo (Mumbai-Nairobi), Fly Dubai (Dubai-Mombasa), and Airlink (Johannesburg-Nairobi). Additionally, major international conferences such as the Africa Climate Summit 2023 and the EU-Kenya Business Forum contributed to this growth. The number of international arrivals was further bolstered by Nairobi City being honored as the top city in the world by Lonely Planet, a United States-based travel agency. Moreover, the period under review saw an increase in the number of international conferences by 9.0%, rising to 977 from 896 in 2022. The number of local conferences grew by 11.0%, reaching 10,725 from 9,662 recorded in 2022. The charts below show the trend in international arrivals between 2019-2023 and the monthly international visitor arrivals through Moi International Airport (MIA) and Jomo Kenyatta International Airport (JKIA) between 2022-2023;

Source: KNBS, Economic Survey 2024

Source: KNBS, Economic Survey 2024

Source: KNBS, Economic Survey 2024

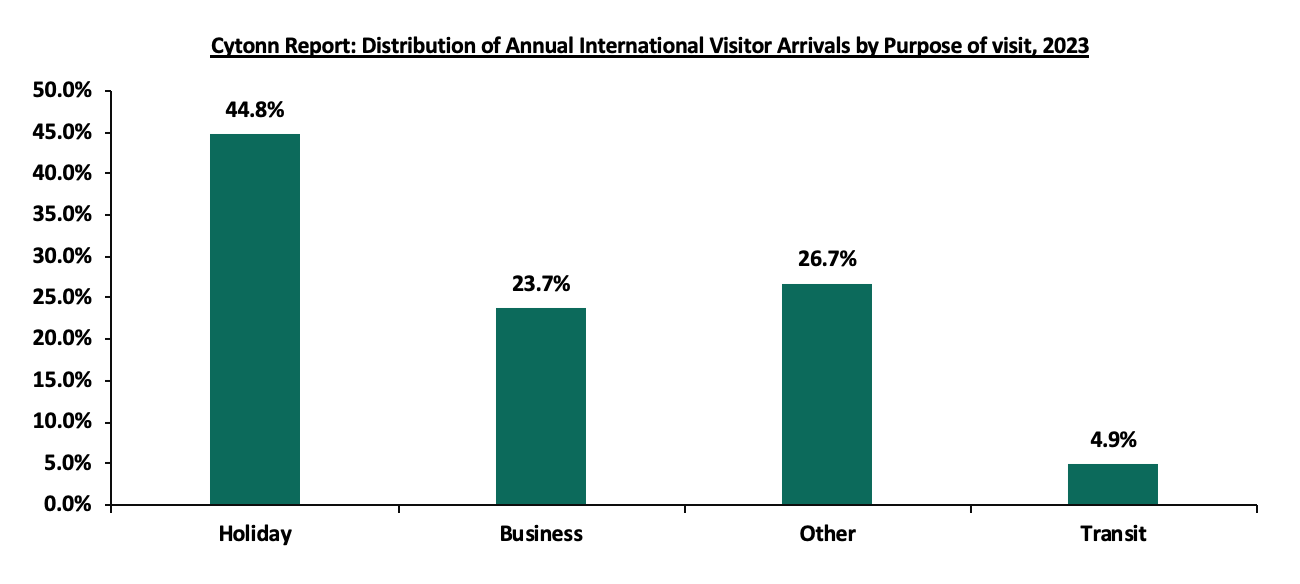

Futhermore, in the period under review, the number of visitor arrivals on holiday accounted for 44.8% of all international arrivals while those on business purposes accounted for 23.7%. The figure below shows the Annual Distribution of International Visitors Arrivals in 2023;

Source: KNBS, Economic Survey 2024

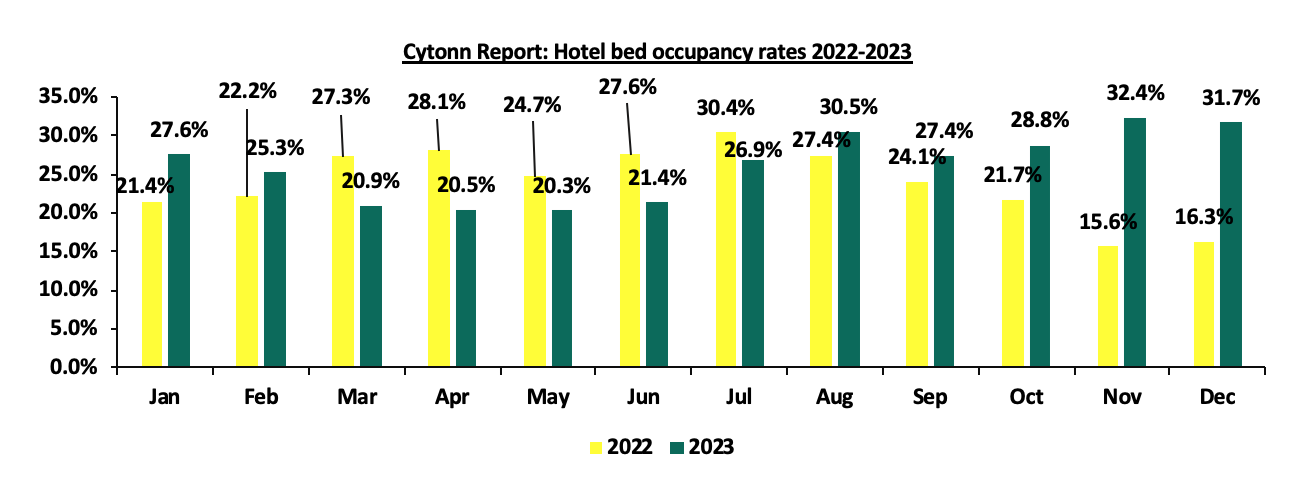

- Hotel bed occupancy

During the period under review, hotel bed occupancy in the country saw significant growth. November was the best-performing month, with a bed occupancy rate of 32.4%. This increase can be attributed to more people traveling within the country in preparation for Christmas Eve and to escape the harsh winter conditions in Europe. The National Statistician noted that the sector continues to stay alert to emerging trends, focusing on the development of wellness tourism, boutique hotels, technological advancements, and sustainable tourism practices. The figure below shows hotel bed occupancy rates in Kenya between 2022-2023;

Source: KNBS, Economic Survey 2024

We expect the sector to remain resilient, supported by several key factors. These include an increased number of international arrivals, continued development activities in the aviation sector, and expansion efforts in the hotel industry, such as the recent opening of the JW Marriott. Additionally, Nairobi's recognition as a major travel destination and the growing regional preference to hold international conferences in the city will further bolster the sector. However, we anticipate that the sector's performance may face challenges such as unpredictable weather conditions, leading to frequent flooding in the country, increased construction costs, and a rise in non-performing loans within the segement which are likely to impede the sector’s growth.

- Infrastructure Sector

During the week, President Ruto signed an agreement with Everstrong Capital, a U.S. firm, for the construction of the 440-kilometer Nairobi-Mombasa Expressway. The project, estimated to cost Ksh 470.0 bn (USD 3.6 bn), will be a six-lane dual carriageway. The project received approval from the National Assembly last year to proceed under a public-private partnership (PPP) model. It aims to reduce traffic congestion and decrease travel time between the two cities from the current average of 10.5 hours to 4 hours. Everstrong Capital will be responsible for designing the road and sourcing funds for its construction expected to take 4 years. Upon completion, the firm will operate the road for 30 years, charging toll charges on motorists to recoup the costs of construction and maintenance. The project is expected to attract investments from international investors, development agencies, pension funds, and Kenyan private investors. Additionally, the Usahihi Expressway will feature rest stops, electric vehicle charging infrastructure, and wildlife observation points.

The project is anticipated to offer job opportunities to local communities, promote business activities in the region, increase economic activity, reduce travel time by alleviating congestion, and bolster Kenya's status as a major economic hub.

- Industrial Sector

During the week, President Ruto's visit to the U.S. resulted in the signing of an agreement between G42 and Microsoft to build a data center worth Ksh 131.0 bn (USD 1.0 bn) at the KenGen Green Park in Olkaria. The data center will run on 100.0% renewable geothermal power from the Olkaria Geothermal fields in Naivasha, Nakuru County. G42, in collaboration with other partners, will design and construct the state-of-the-art facility, which will provide access to Microsoft Azure through a new East Africa Cloud Region. This region is expected to become operational within 24 months of the signing of the definitive agreements and will offer customers scalable, secure, high-speed cloud and AI services, thereby accelerating cloud adoption and the digital transformation of businesses, customers, and partners across Kenya and East Africa.

The project is expected to: i) promote the growth of the industrial sector and encourage industrialization in the region, ii) affirm Kenya’s position as a digital leader within Sub-Saharan Africa, and iii) open up Kenya to more global investment opportunities.

- Real Estate Investments Trusts (REITs)

During the week, Acorn Holdings secured Ksh 23.6 bn (USD 180 mn) in funding from the U.S. Development Finance Corporation (DFC) for affordable student housing. The funding will be channeled towards the development of 35 affordable student housing units, adding 48,000 student beds to Acorn Holdings’ portfolio. This will bring the total student bed capacity in Kenya to 69,000 and create over 50,000 direct jobs. The funding is concessional and will be backed by a USD 380.0 mn special arrangement with Stanbic Bank to manage foreign exchange.

Acorn aims to raise an additional USD 315.0 mn from Kenya’s capital markets, which will include domestic pension funds and asset managers, for a total financing of USD 700.0 mn over the 18-year life of the transaction. Acorn Student Accommodation Development-REIT will receive USD 90 mn for the construction of new Purpose-Built Student Accommodations (PBSAs). Additionally, Acorn plans to recycle funds up to two times during the loan tenure, facilitating up to USD 270.0 mn in financing through redeployment. The remaining USD 90.0 mn will be channeled towards the Acorn Student Accommodation Income-Real Estate Investment Trust (ASA I-REIT) for the acquisition of stabilized PBSAs from the D-REIT.

Additionally, during the week, Laptrust released the FY’2023 financial results for the Imara I-REIT for the period ended 31st December 2023. The table below includes a summary of the REIT’s performance in FY’2023.

Below is a summary of the Laptrust Imara I-REIT’s FY’2023 Performance;

|

Figures in Kshs bn unless stated otherwise |

|||

|

Balance Sheet |

H1'2023 |

FY'2023 |

FY'2023/H1'2023 Change |

|

Total Assets |

7.3 |

7.3 |

(0.6%) |

|

Total Equity |

7.0 |

7.0 |

(0.6%) |

|

Total Liabilities |

0.3 |

0.3 |

(1.3%) |

|

Income Statement |

FY'2023 |

|

Rental Income |

305.2 |

|

Income from Other Sources |

115.8 |

|

Operating Expenses |

176.4 |

|

Profit/Loss |

57.2 |

|

Basic EPS (Kshs) |

0.2 |

|

Figures in Kshs mn unless stated otherwise |

|||

|

Ratios Summary |

H1'2023 |

FY'2023 |

FY'2023/H1'2023 Change |

|

ROA |

2.74% |

0.79% |

(2.0%) |

|

ROE |

2.86% |

0.82% |

(2.0%) |

|

Debt Ratio |

4.2% |

4.2% |

(0.03%) |

|

PBT Margin |

59.6% |

18.8% |

(40.9%) |

|

Rental Yield |

2.4% |

4.5% |

2.1% |

- The basic earnings per unit came in at Kshs 0.2 in FY’2023, a 42.6% decline from 0.3 recorded in H1’2023. The performance was driven by a 42.6% decline in net earnings to Kshs 57.2 mn in FY’2023 from Kshs 99.6 mn recorded in H1’2023,

- Rental and related income for the REIT stood at Kshs 305.2 mn in FY’2023, implying a gross rental yield of 4.5% in FY’2023 on interest-earning assets. This rental income was driven by an upward review in rental prices for several properties within the portfolio. For instance, rental prices at Pension Towers increased from Kshs 78 per SQFT in Q2'2023 to Kshs 100 per SQFT in Q4'2023; a 33.3% increase. Moreover, there was a 14.8% increase in rental prices at CPF House to Kshs 463 per SQFT in 2024 from Kshs 403 per SQFT in 2023. The annual rental yield currently stands at 4.5%,

- Total operating expenses for the REIT came in at Kshs 176.4 mn, attributed to Kshs 62.8 mn incurred in utility expenses, 47.9 mn in property expenses, and Kshs 65.7 mn in fund operating expenses. Notably, property valuation fees stood at 2.9 mn, accounting for 6.1% of the total property expenses in FY’2023,

- Trustee fees in FY’2023 stood at Kshs 37.4 mn, accounting for 56.9% of the total fund operation expenses. Key to note, expenses made up 41.9% of the total operating income.

- Total assets for the REIT stood at Kshs 7.29 bn in FY’2023, a 0.6% decrease from Kshs 7.33 bn recorded in H1’2023, comprising of Kshs 6.7 bn in investment property that saw a 2.7% decrease from Kshs 6.9 bn in H1’2023 attributable to a fair value adjustment of Kshs 187.4 mn, Kshs 0.4 bn in cash and cash equivalents, and Kshs 0.1 bn in trade and other receivables,

- Total liabilities in FY’2023 came in at Kshs 304.2 mn, recording a 1.3% decrease from Kshs 308.1 mn in H1’2023 wholly attributable to a decrease in trade and other payables,

- The shareholder’s funds decreased by 0.6% to Kshs 6.98 mn from Kshs 7.02 bn in H1’2023, attributable to 6.9 bn in trust capital which recorded no change, and 57.2 mn in retained earnings which saw a 42.6% decline from 99.6 mn recorded in H1’2023, and,

- The REIT currently has a Return on Asset and a Return on Equity of 0.79% and 0.82% respectively.

For a more comprehensive analysis, please see our LapTrust Imara I-REIT FY’2023 Earnings Note.

On the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 24.5 and Kshs 22.0 per unit, respectively, as of 17th May 2024. The performance represented a 22.5% and 10.0% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. The volumes traded for the D-REIT and I-REIT came in at 12.3 mn and 30.7 mn shares, respectively, with a turnover of Kshs 257.5 mn and Kshs 633.8 mn, respectively, since inception in February 2021.REITs provide various benefits like tax exemptions, diversified portfolios, and stable long-term profits. However, the continuous deterioration in the performance of Kenyan REITs and the restructuring of their business portfolios is hampering major investments that had previously been made. The other general challenges include; i) inadequate comprehension of the investment instrument among investors, ii) prolonged approval processes for REIT creation, iii) high minimum capital requirements of Kshs 100.0 mn for trustees, and, iv) minimum investment amounts set at Kshs 5.0 mn, continue to limit the performance of the Kenyan REITs market.

We expect the performance of Kenya’s real estate sector to be supported by: i) increased investment activities by international investors driving growth in the industrial and retail sectors, ii) collaboration between Kenya and major economies promoting development in the infrastructure sector, iii) an increased number of international arrivals and Nairobi’s recognition as a major travel destination bolstering the hospitality sector, and iv) positive demographics driving housing demand in the country. However, factors such as rising construction costs, strain on infrastructure development like drainage systems, limited investor knowledge in REITs, and existing oversupply in select real estate sectors will continue to hinder the optimal performance of the sector by limiting developments and investments.