Retirement Benefits Schemes Q4’2024 Performance Report and Cytonn Weekly #11/2025

By Research Team, Mar 16, 2025

Executive Summary

Fixed Income

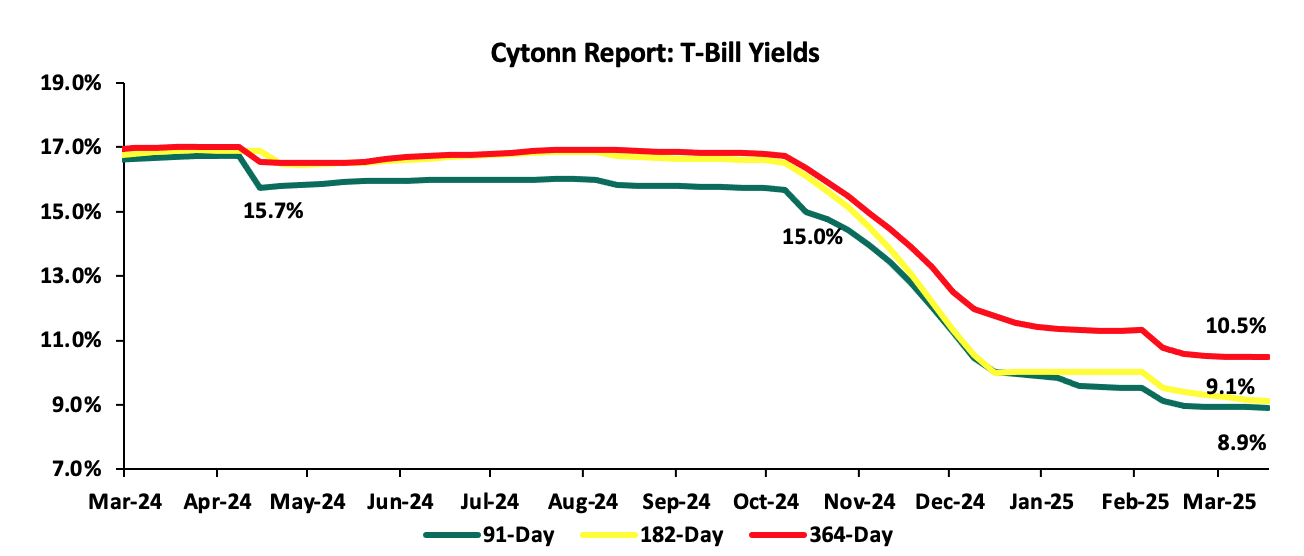

During the week, T-bills were oversubscribed for the sixth consecutive week, with the overall subscription rate coming in at 122.7%, albeit lower than the subscription rate of 210.7% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 7.5 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 188.1%, from the oversubscription rate of 598.8% recorded the previous week. The subscription rates for the 182-day and 364-day papers decreased to 98.0% and 121.1% respectively from the to 124.4% and 141.7% recorded the previous week. The government accepted a total of Kshs 26.9 bn worth of bids out of Kshs 29.4 bn bids received, translating to an acceptance rate of 91.3%. The yields on the government papers were on a downward trajectory with the yields on the182-day paper decreasing the most by 3.6 bps to 9.1% from 9.2% recorded the previous week. The yields on the 364-day and 91-day papers decreased by 2.3 bps and 0.5 bps respectively to remain relatively unchanged from 10.5% and 8.9% respectively recorded the previous week;

During the week, The Energy and Petroleum Regulatory Authority (EPRA) released their monthly statement on the maximum retail fuel prices in Kenya, effective from 15th March 2025 to 14th April 2025. Notably, the maximum allowed prices for Super Petrol, Diesel, and Kerosene remained unchanged at Kshs 176.6, Kshs 167.1, and Kshs 151.4 per litre respectively.

Equities

During the week, the equities market was on a downward trajectory, with NSE 20 declining the most by 4.3%, while NSE 10, NSE 25 and NASI lost by 3.3%, 3.1% and 3.1% respectively, taking the YTD performance to gains of 8.6%, 3.4%, 2.1% and 0.5% for NSE 20, NASI, NSE 25 and NSE 10, respectively. The equities market performance was driven by losses recorded by large-cap stocks such as Standard Chartered, Cooperative Bank and KCB of 12.4%, 10.9%, and 5.8% respectively;

During the week, KCB Group released their FY’2024 results, recording a 64.9% increase in Profit After Tax to Kshs 61.8 bn, from Kshs 37.5 bn in FY’2023. The performance was mainly driven by a 24.0% increase in total operating income to Kshs 204.9 bn, from Kshs 165.2 bn in FY’2023, which outpaced the 5.2% increase in total Operating expense to Kshs 122.9 bn in FY’2024, from Kshs 116.8 bn in FY’2023.

During the week, Sanlam Kenya Holdings released their FY’2024 results, recording a significant 933.5% increase in Profit After Tax to Kshs 1.1 bn, from the Kshs 0.1 bn loss recorded in FY’2023. The performance was mainly driven by a significant 396.9% increase in insurance investment revenue to Kshs 5.3 bn, from Kshs 1.1 bn in FY’2023, and supported by a 13.3% decrease in Net expenses from reinsurance contracts held to Kshs 1.0 bn in FY’2024, from Kshs 1.2 bn in FY’2023;

Real Estate

During the week, the Jogoo Road Phase I Affordable Housing Project, a 500 units residential development, was launched by President William Ruto. The project is a flagship initiative under Kenya’s Affordable Housing Program (AHP) aimed at addressing the housing deficit in urban areas. Located in Makadara Constituency, Nairobi County, the project targets low and middle-income families by offering affordable housing units in a region where demand for quality, cost-effective homes is high. This project is expected to provide a viable alternative by integrating modern housing with improved infrastructure, while also addressing past issues of displacement. The total project cost is estimated at approximately Kshs 1.0 bn. The construction phase is projected to last two years, with a completion timeline estimated at around March 2027.

During the week, the cabinet approved the construction of the Rironi-Mau Summit road project. This development is set to transform a critical transportation corridor in Kenya by upgrading the existing road from Rironi near Nairobi to Mau Summit in Nakuru County into a modern four-lane dual carriageway. The project, with an estimated cost of Kshs 175.0 bn, is scheduled to begin in June 2025 and conclude in June 2027, aligning with strategic government infrastructure plans ahead of the 2027 general elections.

On the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 25.4 and Kshs 22.2 per unit, respectively, as per the last updated data on 7th March 2025. The performance represented a 27.0% and 11.0% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. Additionally, ILAM Fahari I-REIT traded at Kshs 11.0 per share as of 7th March 2025, representing a 45.0% loss from the Kshs 20.0 inception price;

Focus of the Week

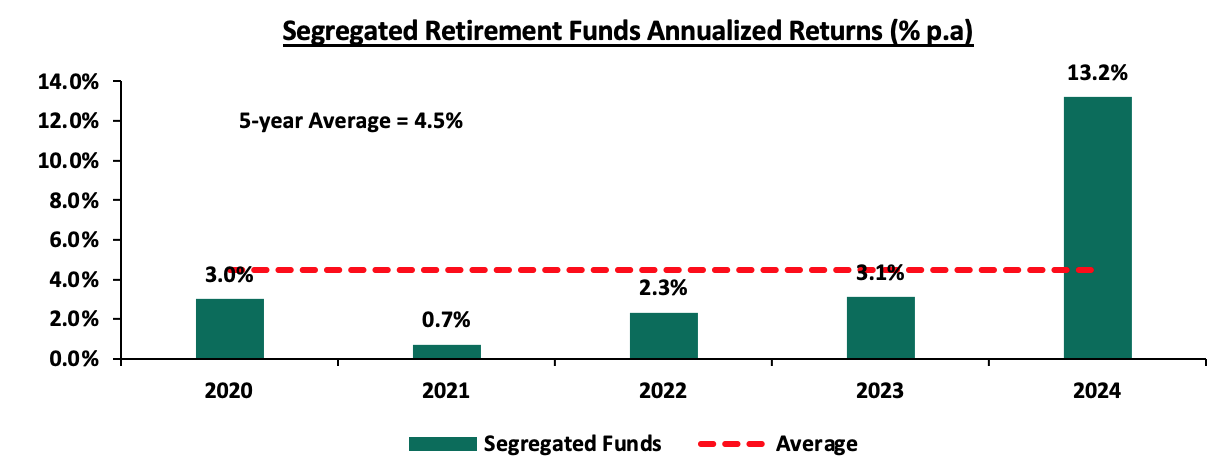

According to the ACTSERV Q4’2024 Pension Schemes Investments Performance Survey, the five-year average return for segregated schemes over the period 2020 to 2024 was 4.5% with the performance fluctuating over the years to a high of 13.2% in Q4’2024 and a low of 0.7% in Q4’2021 reflective of the markets performance. Notably, segregated retirement benefits scheme q/q returns increased to a 13.2% return in Q4’2024, up from the 3.1% gain recorded in Q4’2023. The y/y growth in overall returns was largely driven by the 18.7% points increase in returns from Equities to 15.7% from a loss of 3.0% in Q4’2023 attributable to the increased corporate earnings and attractive valuations as well as the 13.3% gain from fixed income. The performance was however weighed down by the 17.2% points decline in the Offshore returns to 0.8%, from 18.0% in Q4’2023 majorly attributable to the uncertainty about the US general election, China’s weak economic data and the appreciation of the shilling. This week, we shall focus on understanding Retirement Benefits Schemes and look into the quarterly performance and current state of retirement benefits schemes in Kenya with a key focus on Q4’2024;

Investment Updates:

- Weekly Rates:

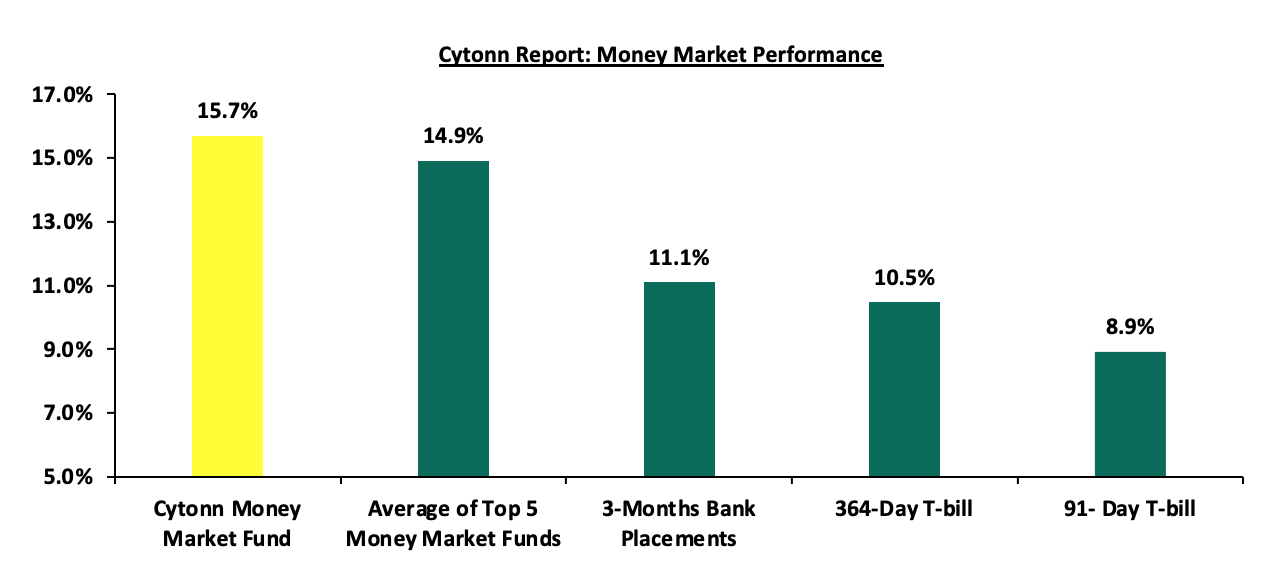

- Cytonn Money Market Fund closed the week at a yield of 15.70% p.a. To invest, dial *809# or download the Cytonn App from Google Play store here or from the Appstore here;

- We continue to offer Wealth Management Training every Tuesday, from 7:00 pm to 8:00 pm. The training aims to grow financial literacy among the general public. To register for any of our Wealth Management Trainings, click here;

- If interested in our Private Wealth Management Training for your employees or investment group, please get in touch with us through wmt@cytonn.com;

- Cytonn Insurance Agency acts as an intermediary for those looking to secure their assets and loved ones’ future through insurance namely; Motor, Medical, Life, Property, WIBA, Credit and Fire and Burglary insurance covers. For assistance, get in touch with us through insuranceagency@cytonn.com;

- Cytonn Asset Managers Limited (CAML) continues to offer pension products to meet the needs of both individual clients who want to save for their retirement during their working years and Institutional clients that want to contribute on behalf of their employees to help them build their retirement pot. To more about our pension schemes, kindly get in touch with us through pensions@cytonn.com;

Hospitality Updates:

- We currently have promotions for Staycations. Visit cysuites.com/offers for details or email us at sales@cysuites.com;

Money Markets, T-Bills Primary Auction:

During the week, T-bills were oversubscribed for the sixth consecutive week, with the overall subscription rate coming in at 122.7%, albeit lower than the subscription rate of 210.7% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 7.5 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 188.1%, from the oversubscription rate of 598.8% recorded the previous week. The subscription rates for the 182-day and 364-day papers decreased to 98.0% and 121.1% respectively from the to 124.4% and 141.7% recorded the previous week. The government accepted a total of Kshs 26.9 bn worth of bids out of Kshs 29.4 bn bids received, translating to an acceptance rate of 91.3%. The yields on the government papers were on a downward trajectory with the yields on the182-day paper decreasing the most by 3.6 bps to 9.1% from 9.2% recorded the previous week. The yields on the 364-day and 91-day papers decreased by 2.3 bps and 0.5 bps respectively to remain relatively unchanged from 10.5% and 8.9% respectively recorded the previous week.

The charts below show the yield performance of the 91-day, 182-day and 364-day papers from March 2024 to March 2025:

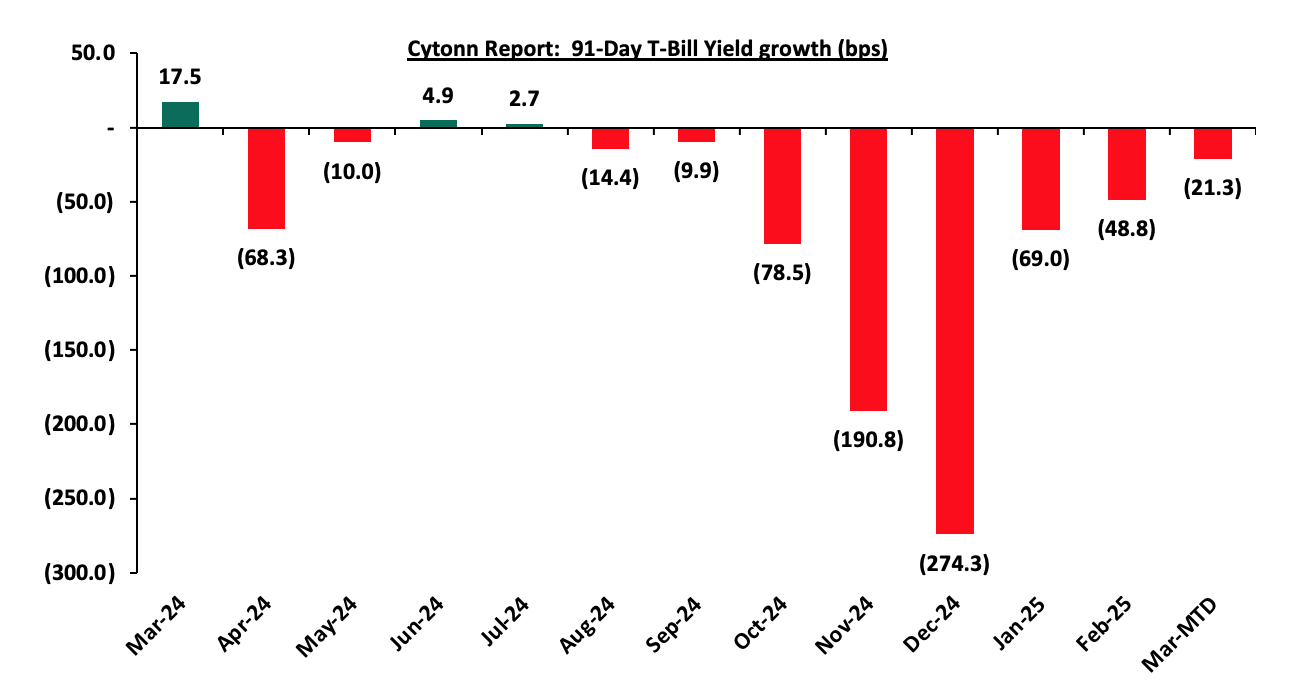

The chart below shows the yield growth for the 91-day T-bill:

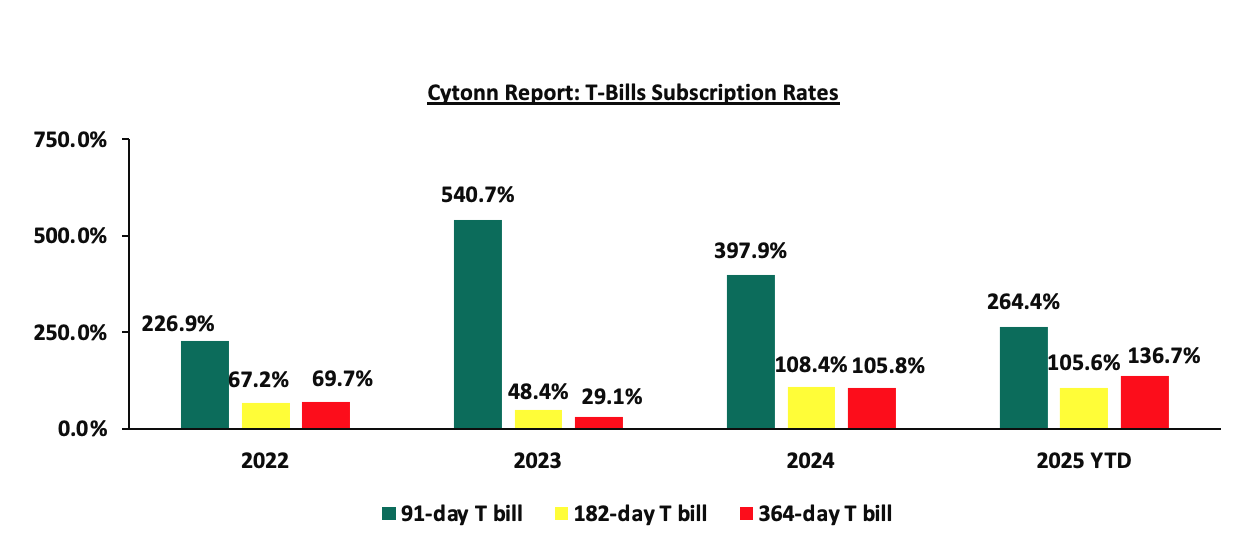

The chart below compares the overall average T-bill subscription rates obtained in 2022,2023, 2024 and 2025 Year-to-date (YTD):

Money Market Performance:

In the money markets, 3-month bank placements ended the week at 11.1% (based on what we have been offered by various banks), and the yields on the government papers were on a downward trajectory with the yields on the 364-day and 91-day papers decreasing marginally by 2.3 bps and 0.5 bps to remain relatively unchanged from the 10.5% and 8.9% recorded the previous week. The yield on the Cytonn Money Market Fund decreased by 34.0 bps to 15.7% from the 16.0% recorded the previous week, while the average yields on the Top 5 Money Market Funds decreased by 62.8 bps to close the week at 14.9%, from the 15.5% recorded the previous week.

The table below shows the Money Market Fund Yields for Kenyan Fund Managers as published on 14th March 2025:

|

Cytonn Report: Money Market Fund Yield for Fund Managers as published on 14th March 2025 |

||

|

Rank |

Fund Manager |

Effective Annual Rate |

|

1 |

Gulfcap Money Market Fund |

16.3% |

|

2 |

Cytonn Money Market Fund (Dial *809# or download the Cytonn app) |

15.7% |

|

3 |

Lofty-Corban Money Market Fund |

14.3% |

|

4 |

Etica Money Market Fund |

14.3% |

|

5 |

Kuza Money Market fund |

14.1% |

|

6 |

Arvocap Money Market Fund |

14.0% |

|

7 |

Orient Kasha Money Market Fund |

13.4% |

|

8 |

Ndovu Money Market Fund |

13.1% |

|

9 |

Enwealth Money Market Fund |

12.8% |

|

10 |

British-American Money Market Fund |

12.6% |

|

11 |

Old Mutual Money Market Fund |

12.5% |

|

12 |

GenAfrica Money Market Fund |

12.4% |

|

13 |

Madison Money Market Fund |

12.4% |

|

14 |

Dry Associates Money Market Fund |

12.4% |

|

15 |

Genghis Money Market Fund |

12.3% |

|

16 |

Sanlam Money Market Fund |

12.0% |

|

17 |

Apollo Money Market Fund |

12.0% |

|

18 |

Jubilee Money Market Fund |

11.8% |

|

19 |

Nabo Africa Money Market Fund |

11.8% |

|

20 |

Faulu Money Market Fund |

11.7% |

|

21 |

Co-op Money Market Fund |

11.5% |

|

22 |

KCB Money Market Fund |

11.4% |

|

23 |

ICEA Lion Money Market Fund |

11.3% |

|

24 |

CIC Money Market Fund |

11.2% |

|

25 |

Absa Shilling Money Market Fund |

11.1% |

|

26 |

Mali Money Market Fund |

11.1% |

|

27 |

AA Kenya Shillings Fund |

10.7% |

|

28 |

Mayfair Money Market Fund |

9.7% |

|

29 |

Stanbic Money Market Fund |

7.8% |

|

30 |

Ziidi Money Market Fund |

7.2% |

|

31 |

Equity Money Market Fund |

3.7% |

Source: Business Daily

Liquidity:

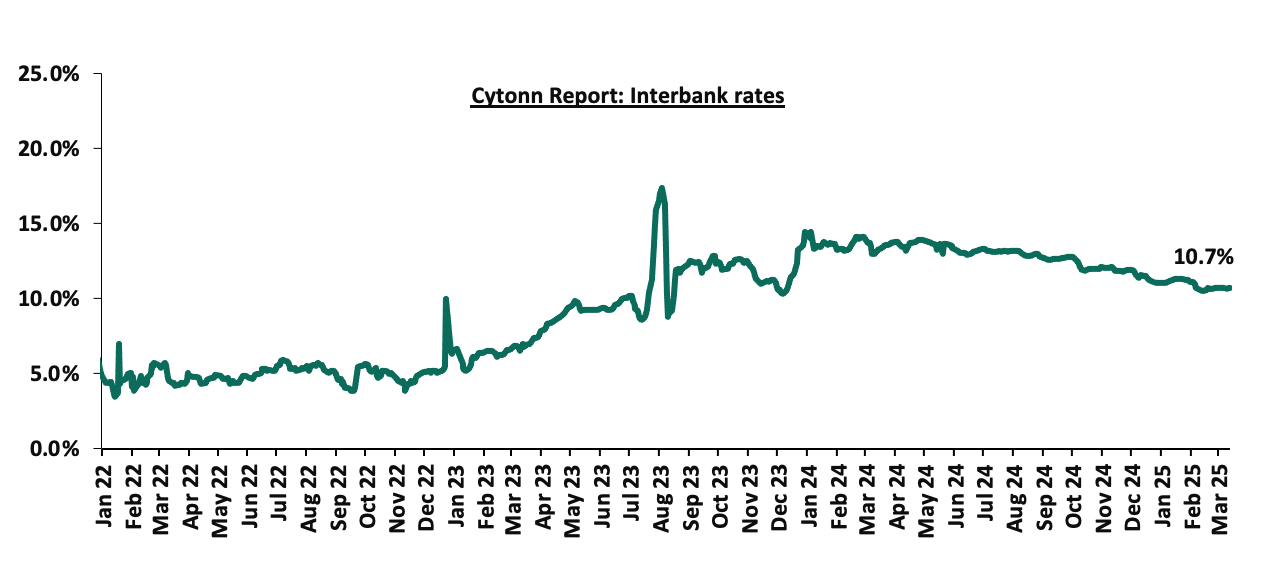

During the week, liquidity in the money markets marginally eased, with the average interbank rate decreasing by 2.0 bps, to remain unchanged from the 10.7% recorded the previous week, partly attributable government payments that offset tax remittances. The average interbank volumes traded increased by 85.3% to Kshs 21.8 bn from Kshs 11.8 bn recorded the previous week. The chart below shows the interbank rates in the market over the years:

Kenya Eurobonds:

During the week, the yields on Kenya’s Eurobonds were on an upwards trajectory, with the yield on the 13-year Eurobond issued in 2021 increasing the most by 13.5 bps to 10.1% from the 9.9% recorded the previous week. The table below shows the summary performance of the Kenyan Eurobonds as of 13th March 2025;

|

Cytonn Report: Kenya Eurobonds Performance |

|

||||||

|

|

2018 |

2019 |

2021 |

2024 |

2025 |

||

|

Tenor |

10-year issue |

30-year issue |

7-year issue |

12-year issue |

13-year issue |

7-year issue |

11-year issue |

|

Amount Issued (USD) |

1.0 bn |

1.0 bn |

0.3 bn |

1.2 bn |

1.0 bn |

1.5 bn |

1.5 bn |

|

Years to Maturity |

3.0 |

23.0 |

2.2 |

7.2 |

9.3 |

5.9 |

11.0 |

|

Yields at Issue |

7.3% |

8.3% |

7.0% |

7.9% |

6.2% |

10.4% |

9.9% |

|

02-Jan-25 |

9.1% |

10.3% |

8.5% |

10.1% |

10.1% |

10.1% |

|

|

03-Mar-25 |

8.0% |

10.0% |

7.3% |

9.5% |

9.6% |

9.4% |

|

|

07-Mar-25 |

8.4% |

10.3% |

7.3% |

9.8% |

9.9% |

9.8% |

|

|

10-Mar-25 |

8.4% |

10.3% |

7.2% |

9.9% |

10.0% |

9.9% |

|

|

11-Mar-25 |

8.5% |

10.3% |

7.4% |

9.9% |

10.0% |

9.9% |

|

|

12-Mar-25 |

8.4% |

10.3% |

7.3% |

9.9% |

10.0% |

9.8% |

|

|

13-Mar-25 |

8.5% |

10.4% |

7.3% |

10.0% |

10.1% |

9.9% |

|

|

Weekly Change |

0.1% |

0.1% |

0.0% |

0.1% |

0.1% |

0.1% |

- |

|

MTD Change |

0.5% |

0.3% |

0.0% |

0.5% |

0.4% |

0.5% |

- |

|

YTD Change |

(0.5%) |

0.1% |

(1.2%) |

(0.1%) |

(0.0%) |

(0.2%) |

- |

Source: Central Bank of Kenya (CBK) and National Treasury

Kenya Shilling:

During the week, the Kenyan Shilling depreciated marginally against the US Dollar by 20.7 bps, to Kshs 129.5 from the Kshs 129.2 recorded the previous week. On a year-to-date basis, the shilling has depreciated by 15.5 bps against the dollar, compared to the 17.4% appreciation recorded in 2024.

We expect the shilling to be supported by:

- Diaspora remittances standing at a cumulative USD 4,960.2 mn in the twelve months to January 2025, 16.6% higher than the USD 4,252.9 mn recorded over the same period in 2024. These has continued to cushion the shilling against further depreciation. In the January 2025 diaspora remittances figures, North America remained the largest source of remittances to Kenya accounting for 56.9% in the period,

- The tourism inflow receipts which came in at Kshs 452.2 bn in 2024, a 19.8% increase from Kshs 377.5 bn inflow receipts recorded in 2023, and owing to tourist arrivals that improved by 14.6% to 2,394,376 in 2024 from 2,089,259 in 2023, and,

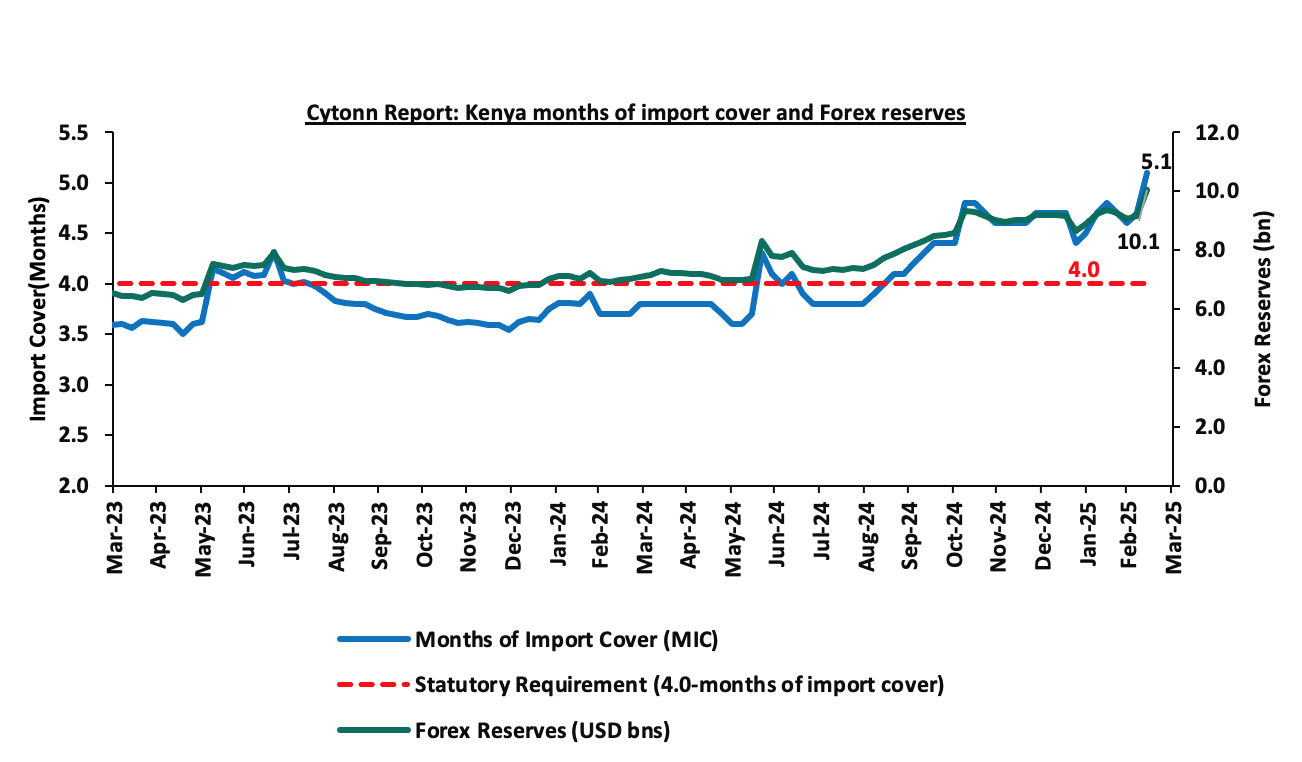

- Improved forex reserves currently at USD 10.1bn (equivalent to 5.1-months of import cover), which is above the statutory requirement of maintaining at least 4.0-months of import cover and above the EAC region’s convergence criteria of 4.5-months of import cover.

The shilling is however expected to remain under pressure in 2025 as a result of:

- An ever-present current account deficit which came at 4.0% of GDP in Q3’2024, and,

- The need for government debt servicing, continues to put pressure on forex reserves given that 62.1% of Kenya’s external debt is US Dollar-denominated as of September 2024.

Key to note, Kenya’s forex reserves increased by 10.0% during the week, to USD 10.1 bn from the USD 9.1 bn recorded in the previous week, equivalent to 5.1 months of import cover compared to 4.7 months of import cover recorded last week, and above the statutory requirement of maintaining at least 4.0-months of import cover. The increase in forex reserves can be attributable to the inflow of funds from the issuance of the new USD 1.5 bn bond which was issued to buy back the 7- year tenor USD 900.0 mn bond. The chart below summarizes the evolution of Kenya's months of import cover over the years:

Weekly Highlights

- Fuel Prices effective 15th March 2025 to 14thApril 2025

During the week, The Energy and Petroleum Regulatory Authority (EPRA) released their monthly statement on the maximum retail fuel prices in Kenya, effective from 15th March 2025 to 14th April 2025. Notably, the maximum allowed prices for Super Petrol, Diesel, and Kerosene remained unchanged at Kshs 176.6, Kshs 167.1, and Kshs 151.4 per litre respectively.

Other key take-outs from the performance include;

- The average landing costs per cubic meter for Diesel and Super Petrol increased by 1.4% and 1.3% respectively to USD 680.6 and USD 637.2 respectively in February 2025, from USD 671.1 and USD 628.8 respectively recorded in January while the average landing cost per cubic meter for Kerosene decreased by 1.4% to USD 672.1 in February from USD 681.4 in January.

- The Kenyan Shilling remained stable against the US Dollar, depreciating slightly by 27.4 bps to Kshs 129.5 from Kshs 129.2 recorded in February.

We note that fuel prices in the country have stabilized in recent months largely due to the government's efforts to stabilize pump prices through the petroleum pump price stabilization mechanism which expended Kshs 9.9 bn in the FY’2023/24 to cushion the increases applied to the petroleum pump prices, coupled with the appreciation of the Kenyan Shilling against the dollar and other major currencies, as well as a decrease in international fuel prices. However, despite an increase in landing costs in February, the government has increased spending through the price stabilization mechanism, subsidizing Kshs 7.0, Kshs 10.0 and Kshs 10.4 per litre for Petrol, Diesel and Kerosene respectively, compared to Kshs 2.4 and Kshs 5.6 and Kshs 8.7 per litre for Petrol, Diesel and Kerosene in February resulting in stabilization in fuel prices for the period under review. Going forward, we expect that fuel prices will stabilize in the coming months as a result of the government's efforts to mitigate the cost of petroleum through the pump price stabilization mechanism and a stable exchange rate. As such, we expect the business environment in the country to improve as fuel is a major input cost, as well as continued stability in inflationary pressures, with the inflation rate expected to remain within the CBK’s preferred target range of 2.5%-7.5% in the short to medium-term.

Rates in the Fixed Income market have been on a downward trend due to high liquidity in the money market which allowed the government to front load most of its borrowing. The government is 80.0% ahead of its prorated net domestic borrowing target of Kshs 411.0 bn, and 24.6% ahead of the total FY’2024/25 net domestic borrowing target of Kshs 593.7 bn, having a net borrowing position of Kshs 739.9 bn (inclusive of T-bills). However, we expect a continued downward readjustment of the yield curve in the short and medium term, with the government looking to increase its external borrowing to maintain the fiscal surplus, hence alleviating pressure in the domestic market. As such, we expect the yield curve to stabilize in the short to medium-term and hence investors are expected to shift towards the long-term papers to lock in the high returns

Market Performance

During the week, the equities market was on a downward trajectory, with NSE 20 losing the most by 4.3%, while NSE 10, NSE 25 and NASI lost by 3.3%, 3.1% and 3.1% respectively, taking the YTD performance to gains of 8.6%, 3.4%, 2.1% and 0.5% for NSE 20, NASI, NSE 25 and NSE 10, respectively. The equities market performance was driven by losses recorded by large-cap stocks such as Standard Chartered, Cooperative Bank and KCB of 12.4%, 10.9%, and 5.8% respectively.

During the week, equities turnover decreased by 18.8% to USD 15.5 mn, from USD 19.1 mn recorded the previous week, taking the YTD total turnover to USD 174.6 mn. Foreign investors remained net sellers for the third consecutive week, with a net selling position of USD 0.6 mn, from a net selling position of USD 4.7 mn recorded the previous week, taking the YTD foreign net selling position to USD 23.3 mn, compared to a net selling position of USD 16.9 mn in 2024,

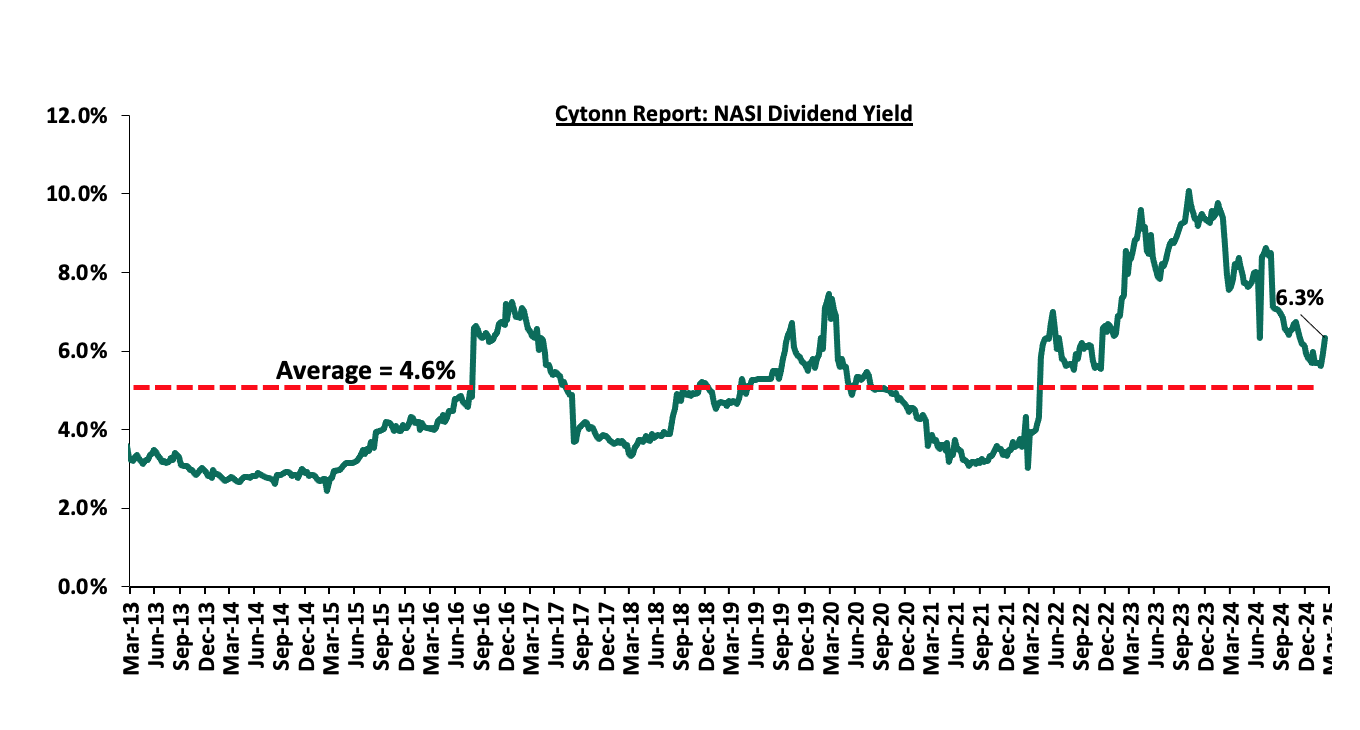

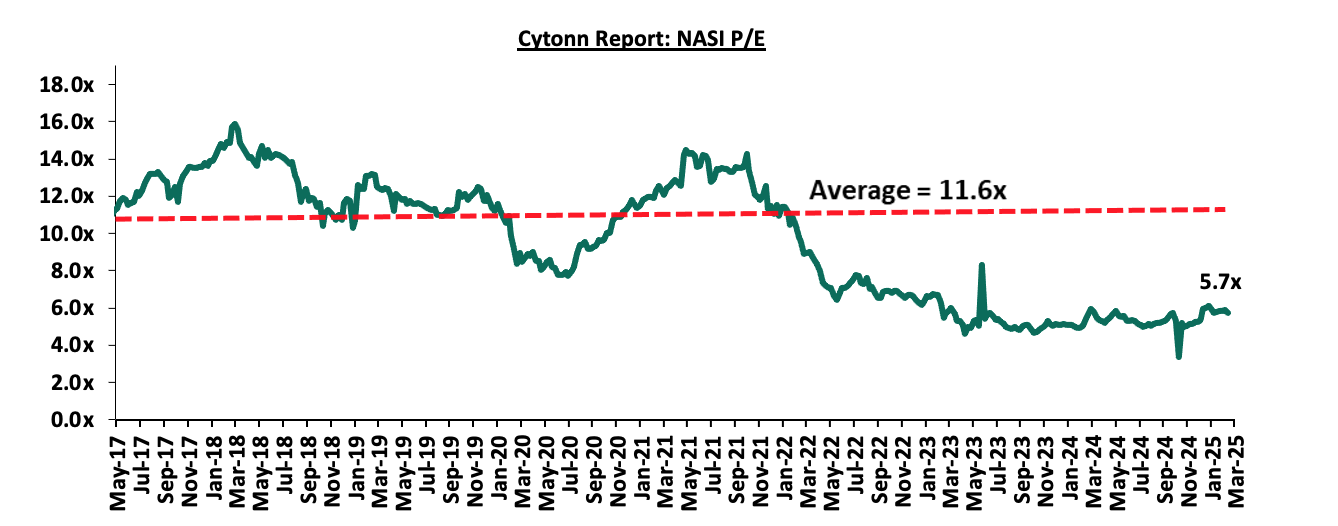

The market is currently trading at a price-to-earnings ratio (P/E) of 5.7x, 50.6% below the historical average of 11.6x. The dividend yield stands at 6.3%, 1.7% points above the historical average of 4.6%. Key to note, NASI’s PEG ratio currently stands at 0.7x, an indication that the market is undervalued relative to its future growth. A PEG ratio greater than 1.0x indicates the market is overvalued while a PEG ratio less than 1.0x indicates that the market is undervalued. The charts below indicate the historical P/E and dividend yields of the market;

Universe of Coverage:

|

Cytonn Report: Equities Universe of Coverage |

||||||||||

|

Company |

Price as at 07/03/2025 |

Price as at 14/03/2025 |

w/w change |

YTD Change |

Year Open 2025 |

Target Price* |

Dividend Yield*** |

Upside/ Downside** |

P/TBv Multiple |

Recommendation |

|

Co-op Bank |

16.9 |

15.1 |

(10.9%) |

(13.8%) |

17.5 |

18.8 |

10.0% |

34.9% |

0.7x |

Buy |

|

Equity Group |

48.5 |

47.6 |

(1.9%) |

(0.8%) |

48.0 |

60.2 |

8.4% |

34.9% |

0.9x |

Buy |

|

KCB Group |

44.8 |

42.2 |

(5.8%) |

(0.6%) |

42.4 |

50.4 |

7.1% |

26.7% |

0.6x |

Buy |

|

Jubilee Holdings |

210.0 |

225.3 |

7.3% |

28.9% |

174.8 |

260.7 |

6.3% |

22.1% |

0.4x |

Buy |

|

Stanbic Holdings |

166.5 |

160.5 |

(3.6%) |

14.8% |

139.8 |

171.2 |

12.9% |

19.6% |

1.0x |

Accumulate |

|

Standard Chartered Bank |

309.0 |

270.8 |

(12.4%) |

(5.1%) |

285.3 |

291.2 |

10.7% |

18.3% |

1.8x |

Accumulate |

|

NCBA |

51.8 |

51.8 |

0.0% |

1.5% |

51.0 |

53.2 |

9.2% |

12.0% |

1.0x |

Accumulate |

|

CIC Group |

3.0 |

2.9 |

(3.9%) |

36.4% |

2.1 |

3.1 |

4.5% |

10.6% |

0.9x |

Accumulate |

|

ABSA Bank |

19.3 |

19.1 |

(1.3%) |

1.1% |

18.9 |

19.1 |

8.1% |

8.4% |

1.5x |

Hold |

|

Diamond Trust Bank |

80.5 |

79.3 |

(1.6%) |

18.7% |

66.8 |

78.1 |

6.3% |

4.9% |

0.3x |

Lighten |

|

I&M Group |

36.1 |

35.1 |

(2.8%) |

(2.6%) |

36.0 |

32.3 |

7.3% |

(0.6%) |

0.7x |

Sell |

|

Britam |

7.8 |

7.7 |

(1.5%) |

32.3% |

5.8 |

7.5 |

0.0% |

(2.6%) |

1.1x |

Sell |

|

*Target Price as per Cytonn Analyst estimates **Upside/ (Downside) is adjusted for Dividend Yield ***Dividend Yield is calculated using FY’2023 Dividends |

||||||||||

Weekly Highlights

- KCB Group FY’2024 results

During the week, KCB Bank Kenya released their FY’2024 financial results. Below is a summary of the performance:

|

Balance Sheet Items |

FY'2023 |

FY'2024f |

y/y change |

|

Government Securities |

348.9 |

302.8 |

(13.2%) |

|

Net Loans and Advances |

1,095.9 |

990.4 |

(9.6%) |

|

Total Assets |

2,170.9 |

1,962.3 |

(9.6%) |

|

Customer Deposits |

1,690.9 |

1,382.0 |

(18.3%) |

|

Deposits/Branch |

2.8 |

2.6 |

(9.4%) |

|

Total Liabilities |

1,935.3 |

1,679.3 |

(13.2%) |

|

Shareholders’ Funds |

227.5 |

274.9 |

20.8% |

|

Balance Sheet Ratios |

FY'2023 |

FY'2024f |

% y/y change |

|

Loan to Deposit Ratio |

64.8% |

71.7% |

6.9% |

|

Government Securities to Deposit Ratio |

20.6% |

21.9% |

1.3% |

|

Return on average equity |

17.5% |

24.6% |

7.1% |

|

Return on average assets |

2.0% |

3.0% |

1.0% |

|

Income Statement (Kshs Bn) |

FY'2023 |

FY'2024f |

y/y change |

|

Net Interest Income |

107.3 |

137.3 |

28.0% |

|

Net non-Interest Income |

57.9 |

67.5 |

16.6% |

|

Total Operating income |

165.2 |

204.9 |

24.0% |

|

Loan Loss provision |

(33.6) |

(30.0) |

(11.0%) |

|

Total Operating expenses |

(116.8) |

(122.9) |

5.2% |

|

Profit before tax |

48.5 |

82.0 |

69.2% |

|

Profit after tax |

37.5 |

61.8 |

64.9% |

|

Core EPS |

11.7 |

19.2 |

64.9% |

|

Dividend Per Share |

0.0 |

3.0 |

- |

|

Dividend Payout Ratio |

0.0 |

15.6% |

- |

|

Dividend Yield |

0.0% |

7.5% |

- |

|

Income Statement Ratios |

FY'2023 |

FY'2024f |

y/y change |

|

Yield from interest-earning assets |

10.3% |

12.1% |

1.7% |

|

Cost of funding |

4.0% |

4.6% |

0.7% |

|

Net Interest Spread |

6.4% |

7.4% |

1.1% |

|

Net Interest Margin |

6.6% |

7.8% |

1.2% |

|

Cost of Risk |

20.4% |

14.6% |

(5.7%) |

|

Net Interest Income as % of operating income |

65.0% |

67.0% |

2.1% |

|

Non-Funded Income as a % of operating income |

35.0% |

33.0% |

(2.1%) |

|

Cost to Income Ratio |

70.7% |

60.0% |

(10.7%) |

|

Cost to Income Ratio (without LLP) |

50.3% |

45.4% |

(5.0%) |

|

Capital Adequacy Ratios |

FY'2023 |

FY'2024f |

% points change |

|

Core Capital/Total Liabilities |

14.2% |

19.4% |

5.2% |

|

Minimum Statutory ratio |

8.0% |

8.0% |

0.0% |

|

Excess |

6.2% |

11.4% |

5.2% |

|

Core Capital/Total Risk Weighted Assets |

12.2% |

16.8% |

4.6% |

|

Minimum Statutory ratio |

10.5% |

10.5% |

0.0% |

|

Excess |

1.7% |

6.3% |

4.6% |

|

Total Capital/Total Risk Weighted Assets |

17.8% |

19.4% |

1.6% |

|

Minimum Statutory ratio |

14.5% |

14.5% |

0.0% |

|

Excess |

3.3% |

4.9% |

1.6% |

|

Liquidity Ratio |

43.5% |

47.6% |

4.1% |

|

Minimum Statutory ratio |

20.0% |

20.0% |

0.0% |

|

Excess |

23.5% |

27.6% |

4.1% |

Key Take-Outs:

- Increased earnings - Core earnings per share (EPS) grew by 64.9% to Kshs 19.2, from Kshs 11.7 in FY’2023, driven by the 24.0% increase in total operating income to Kshs 204.9 bn, from Kshs 165.2 bn in FY’2023, which outpaced the 5.2% increase in total operating expenses to Kshs 122.9 bn from Kshs 116.8 bn in FY’2023,

- Deteriorated asset quality –The bank’s Asset Quality deteriorated, with Gross NPL ratio increasing to 19.8% in FY’2024, from 17.0% in FY’2023, attributable to an 8.4% increase in Gross non-performing loans to Kshs 225.7 bn, from Kshs 208.3 bn in FY’2023, compared to the 7.2% decline in gross loans to Kshs 1,137.2 bn, from Kshs 1,226.1 bn recorded in FY’2023,

- Contracted Balanced sheet - The balance sheet recorded a contraction as total assets declined by 9.6% to Kshs 1,962.3 bn, from Kshs 2,170.9 bn in FY’2024, mainly attributable to the 9.6% decline in net loans to customers to Kshs 990.4 bn, from Kshs 1,095.9 bn in FY’2024, coupled with a 13.2% decrease in governments securities holdings to Kshs 302.8 bn, from 348.9 bn in FY’2023,

- Declaration of dividends - The directors of KCB Group recommended a final dividend of 1.5, in addition to an interim dividend of 1.5 paid during the year, leading a to a total dividend of 3.0 in 2024, translating to a dividend yield of 7.5% and payout ratio of 15.6%, from zero dividends in FY’2023, and,

- Reduced lending- Customer net loans and advances decreased by 9.6% to Kshs 990.4 bn in FY’2024, from Kshs 1,095.9 bn in FY’2023 attributed to increased credit risk with high NPLs in the industry, with the lender preferring to limit customer lending.

For a more detailed analysis, please see the KCB Group’s FY’2024 Earnings Note

Asset Quality:

The table below shows the asset quality of listed banks that have released their FY’2024 results using several metrics:

|

Cytonn Report: Listed Banks Asset Quality in FY’2024 |

||||||

|

|

FY'2024 NPL Ratio* |

FY'2023 NPL Ratio** |

% point change in NPL Ratio |

FY'2024 NPL Coverage* |

FY’2023 NPL Coverage** |

% point change in NPL Coverage |

|

Stanbic Bank |

9.1% |

9.5% |

(0.4%) |

78.4% |

70.4% |

8.0% |

|

KCB Group |

19.8% |

17.0% |

2.8% |

65.1% |

62.5% |

2.6% |

|

Mkt Weighted Average* |

16.4% |

13.1% |

3.3% |

69.3% |

62.0% |

7.3% |

|

*Market cap weighted as at 14/03/2025 |

||||||

|

**Market cap weighted as at 18/04/2024 |

||||||

Key take-outs from the table include;

- Asset quality for the listed banks that have released results declined during FY’2024, with market-weighted average NPL ratio increasing by 3.3% points to 16.4% from 13.1% in FY’2023 largely due to KCB’s numbers, and,

- Market-weighted average NPL Coverage for the two listed banks increased by 7.3% points to 69.3% in FY’2024 from 62.0% recorded in FY’2023. The increase was attributable to Stanbic Bank’s coverage ratio increasing by 8.0% points to 78.4% from 70.4% in FY’2023, coupled with KCB Group’s NPL coverage ratio increasing by 2.6% points to 65.1% from 62.5% in FY’2023.

Summary Perfomance

The table below shows the performance of listed banks that have released their FY’2024 results using several metrics:

|

Cytonn Report: Listed Banks Performance in FY’2024 |

|||||||||||||

|

Bank |

Core EPS Growth |

Interest Income Growth |

Interest Expense Growth |

Net Interest Income Growth |

Net Interest Margin |

Non-Funded Income Growth |

NFI to Total Operating Income |

Growth in Total Fees & Commissions |

Deposit Growth |

Growth in Government Securities |

Loan to Deposit Ratio |

Loan Growth |

Return on Average Equity |

|

Stanbic Holdings |

12.8% |

37.8% |

105.7% |

(5.1%) |

5.9% |

(1.7%) |

38.8% |

(13.1%) |

(2.8%) |

70.6% |

71.6% |

(11.6%) |

19.1% |

|

KCB Group |

64.9% |

26.9% |

25.0% |

28.0% |

7.8% |

16.6% |

33.0% |

0.9% |

(18.3%) |

(13.2%) |

71.7% |

(9.6%) |

24.6% |

|

FY'24 Mkt Weighted Average* |

48.3% |

30.4% |

50.7% |

17.4% |

7.2% |

10.8% |

34.8% |

-3.6% |

-13.3% |

13.5% |

71.7% |

(10.3%) |

22.8% |

|

FY'23 Mkt Weighted Average* |

11.4% |

30.5% |

52.4% |

20.6% |

7.5% |

16.4% |

37.0% |

25.0% |

2.2% |

69.0% |

21.2% |

9.5% |

38.3% |

|

*Market cap weighted as at 14/03/2025 |

|||||||||||||

|

**Market cap weighted as at 18/04/2024 |

|||||||||||||

Key take-outs from the table include:

- The listed banks that have released their FY’2024 results recorded a 48.3% growth in core Earnings per Share (EPS) in FY2024, compared to the weighted average growth of 11.4% in FY’2023, an indication of improved performance attributable to the improved operating environment experienced during FY’2024,

- Interest income recorded a weighted average growth of 30.4% in FY’2024, compared to 30.5% in FY’2023. Similarly, interest expenses recorded a market-weighted average growth of 50.7% in FY’2024 compared to a growth of 52.4% in FY’2023,

- The Banks’ net interest income recorded a weighted average growth of 17.4% in FY’2024, a decline from the 20.6% growth recorded over a similar period in 2023, while the non-funded income grew by 10.8% in FY’2024 slower than the 16.4% growth recorded in FY’2023 despite the revenue diversification strategies implemented by most banks, and,

- The Banks recorded a weighted average deposit decline of 13.3%, compared to the market-weighted average deposit growth of 2.2% in FY’2023.

- Sanlam Kenya FY’2024 Results

During the week, Sanlam Kenya Holdings released their FY’2024 results, recording a significant 933.5% increase in Profit After Tax to Kshs 1.1 bn, from the Kshs 0.1 bn loss recorded in FY’2023. The performance was mainly driven by a significant 396.9% increase in insurance investment revenue to Kshs 5.3 bn, from Kshs 1.1 bn in FY’2023, and supported by a 13.3% decrease in Net expenses from reinsurance contracts held to Kshs 1.0 bn in FY’2024, from Kshs 1.2 bn in FY’2023.

Sanlam Kenya Holdings Plc’s FY’2024 Results

|

Cytonn Report: Sanlam Kenya Plc's Income Statement |

|||

|

Income Statement (Kshs bn) |

FY'2023 |

FY'2024 |

y/y change |

|

Insurance Revenue |

6.9 |

7.4 |

6.1% |

|

Insurance Service Expense |

(5.0) |

(5.7) |

12.4% |

|

Net Expense from reinsurance contracts held |

(1.2) |

(1.0) |

(13.3%) |

|

Insurance Service Result |

0.7 |

0.6 |

(6.2%) |

|

Interest Revenue Calculated Using The Effective Interest Method |

0.2 |

0.4 |

69.1% |

|

Other Investment Revenue |

2.8 |

2.6 |

(7.5%) |

|

Other Interest Revenue |

(1.9) |

2.3 |

218.9% |

|

Insurance Investment Revenue |

1.1 |

5.3 |

396.9% |

|

Net Insurance Finance expenses |

(0.8) |

(0.9) |

4.6% |

|

Profit before tax |

0.2 |

1.7 |

584.2% |

|

Income tax expense |

(0.4) |

(0.6) |

64.1% |

|

Profit after tax |

(0.1) |

1.1 |

933.5% |

|

Core EPS |

(0.9) |

7.3 |

933.5% |

|

Cytonn Report: Sanlam Kenya Plc's Balance Sheet |

|||

|

Balance Sheet items |

FY'2023 |

FY'2024 |

y/y change |

|

Financial Investments |

29.8 |

31.7 |

6.7% |

|

Insurance and Reinsurance contract assets |

1.2 |

0.4 |

(63.3%) |

|

Other assets |

4.6 |

7.0 |

51.2% |

|

Total assets |

35.5 |

39.2 |

10.2% |

|

Insurance contract liabilities |

27.9 |

27.5 |

(1.4%) |

|

Payables and Other liabilities |

6.7 |

9.7 |

44.1% |

|

Total liabilities |

34.7 |

37.2 |

7.4% |

|

Shareholder funds |

0.8 |

1.8 |

118.2% |

Key take outs from the results:

- Core Earnings Per share increased significantly by 933.5% to Kshs 7.3 from Kshs 0.9 loss per share in FY’2023, driven by a significant 396.9% increase in insurance investment revenue to Kshs 5.3 bn, from Kshs 1.1 bn in FY’2023, and supported by a 13.3% decrease in Net expenses from reinsurance contracts held to Kshs 1.0 bn in FY’2024, from Kshs 1.2 bn in FY’2023.

- Net Investment revenue increased significantly by 396.9% to Kshs 5.3 bn in FY’2024, from Kshs 1.1 bn in FY’2023. This was majorly attributable to a significant 218.9% increase in other investment revenue to Kshs. 2.3 bn from the Kshs 1.9 bn loss recorded in FY’2023 which outpaced a 7.5% decrease in other interest revenue to Kshs 2.6 bn from Kshs 2.8 bn in FY’2023.

- Insurance revenue increased by 6.1% to Kshs 7.4 bn in FY’2024 from Kshs 6.9 bn in FY’2023, while insurance expenses increased by 12.4% to Kshs 5.7 bn from Kshs 5.0 bn in FY’2023 which outpaced the 13.3% reduction in net expenses from reinsurance contracts held to Kshs 1.0 bn from Kshs 1.2 bn registered in FY’2023. This translated to a significant Net insurance service result decrease of 6.2% to Kshs 0.6 bn from Kshs 0.7 bn in FY’2023,

- The balance sheet recorded an expansion as total assets of 10.2% to Kshs 39.2 bn in FY’2024 from Kshs 35.5 bn in FY’2023 mainly driven by 6.7% increase in financial investments to Kshs 31.7 bn form Kshs 29.8 bn in FY’2023, coupled with a 51.2% increase in other assets to Kshs 7.0 bn from Kshs 4.6 bn in FY’2023.

- Total liabilities increased by 7.4% to Kshs 37.2 bn from Kshs 34.7 bn in FY’2023, majorly on the back of the 44.1% increase in payables and other liabilities to Kshs 9.7 bn from Kshs 6.7 bn in FY’2023

Other highlights from the release include:

- Non-declaration of dividends – The directors of Sanlam Kenya Plc have not recommended a dividend payment for FY’2024, marking the eleventh consecutive year without a dividend, with the last dividend being declared in 2013.

Going forward, the factors that would drive the company’s growth would be:

- Capital preservation – The directors have implemented strategies to return to profitability through sustainable business growth, effective controls, product innovation and effective investment strategies. The Board of Directors has not proposed payment of dividends in the period ending 31st December 2024. This is to enable the business to preserve capital and continue to service its operational and finance costs. Consequently, the Group’s witnessed a return to profitability for the first time in 5 years, recording a significant 933.5% increase in Profit After Tax to Kshs 1.1 bn, from the Kshs 0.1 bn loss recorded in FY’2023.

- Sanlam and Allianz Europe BV Joint Venture – In 2024, Allianz Increased its stake in Sanlam Kenya from 23.1% to 28.0%. The joint venture with Sanlam Group aims at creating a Pan-African non-banking financial services company, SanlamAllianz, with operations in 27 countries including Kenya. This joint venture aimed at expanding Sanlam’s market reach and achieving economies of scale with the creation of more efficient and cost-effective operations.

Valuation Summary:

- We are of the view that Sanlam Kenya Plc is an “Buy” with a target price of Kshs 12.8 representing an upside of 58.1%, from the current price of 8.1 as of 14th March 2025.

We are “Bullish” on the Equities markets in the short term due to current cheap valuations, lower yields on short-term government papers and expected global and local economic recovery, and, “Neutral” in the long term due to persistent foreign investor outflows. With the market currently trading at a discount to its future growth (PEG Ratio at 0.7x), we believe that investors should reposition towards value stocks with strong earnings growth and that are trading at discounts to their intrinsic value. We expect the current high foreign investors sell-offs to continue weighing down the economic outlook in the short term.

- Residential Sector

During the week, the Jogoo Road Phase I Affordable Housing Project, a 500 units residential development, was launched by President William Ruto. The project is a flagship initiative under Kenya’s Affordable Housing Program (AHP) aimed at addressing the housing deficit in urban areas. Located in Makadara Constituency, Nairobi County, the project targets low and middle-income families by offering affordable housing units in a region where demand for quality, cost-effective homes is high. This project is expected to provide a viable alternative by integrating modern housing with improved infrastructure, while also addressing past issues of displacement. The total project cost is estimated at approximately Kshs 1.0 bn. The construction phase is projected to last two years, with a completion timeline estimated at around March 2027.

A notable aspect of the project is its range of housing typologies, designed to cater to diverse family needs. The typologies and their expected sales price are as shown in the table below:

|

Cytonn report: Jogoo Road Phase I AHP |

|||

|

# |

Typology |

Size (SQM) |

Selling Price (Kshs) |

|

1 |

One Bedroom |

30 |

1.0 mn |

|

2 |

Two Bedrooms |

40 |

2.0 mn |

|

3 |

Three Bedrooms |

60 |

3.0 mn |

Sources: Cytonn research, Boma yangu

These unit types are offered at competitive selling prices, potentially supplemented by government subsidies to ensure homeownership remains accessible for the target demographic. The clear pricing structure is intended to foster transparency and consistency across the program, though variations in construction costs due to local factors—such as land acquisition and infrastructure development—could affect the final financial model.

The project not only aims to alleviate the housing deficit but also seeks to stimulate regional economic growth. Job creation during the construction phase is anticipated, and improvements in local infrastructure may spur ancillary investments in services such as education, retail, and transportation. Additionally, the redevelopment component of the project might involve upgrading existing estates, a factor that could lead to legal disputes or displacement concerns similar to those experienced in previous phases.

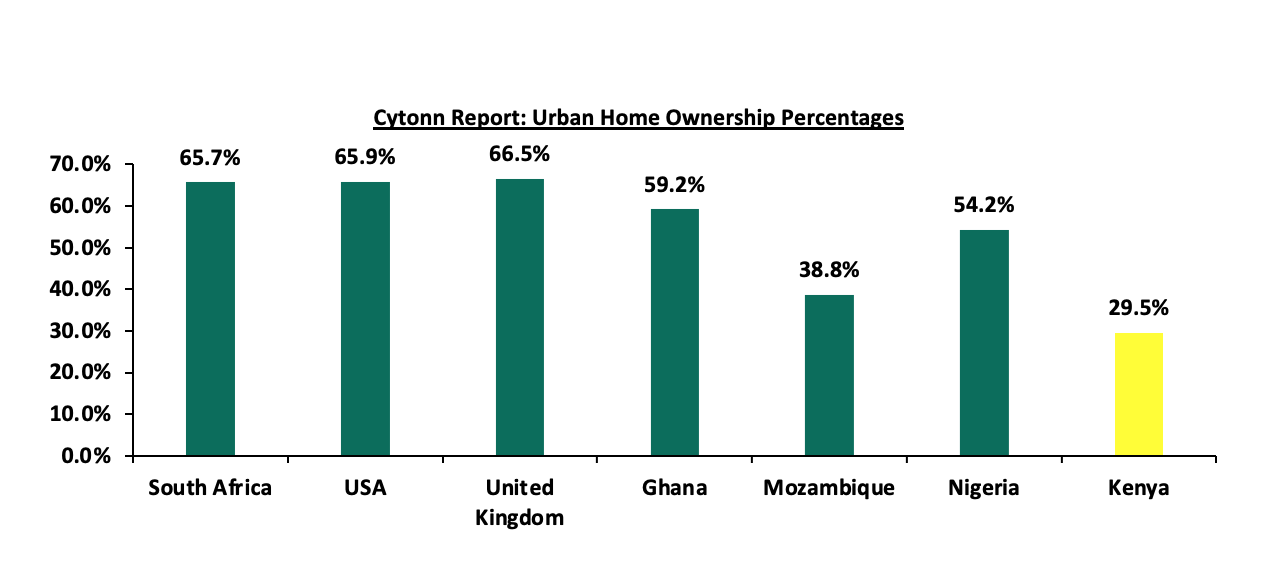

The Centre for Affordable Housing Finance Africa (CAHF) estimates that Kenya faces an annual housing deficit of 80.0%. Currently, only 50,000 new houses are built each year, while the demand stands at approximately 250,000 units, leaving a shortfall of about 200,000 homes annually. The Centre for Affordable Housing Finance in Africa (CAHF) reports that 61.3% of Kenyans own homes, compared to other African countries like Angola and Algeria with 75.4% and 74.8% national home ownership rates respectively. The national homeownership rate stands at approximately 29.5% in urban areas sprawling the national average of 61.3% while 78.7% of urban dwellers rent. The government's push for affordable housing aims to improve this rate by making homes more accessible to lower and middle-income earners. The graph below shows the home ownership percentages for different countries compared to Kenya;

Source: Centre for Affordable Housing Finance Africa (CAHF), US Census Bureau, UK Office for National Statistics

The AHP initiatives are expected to have transformative impact in the Real Estate sector. Improved housing and infrastructure in Eastlands will likely increase property values, attracting both residential and commercial investments. This could lead to the development of new residential estates, shopping centers, and community facilities, thereby boosting local economic activity. However, careful planning will be needed to mitigate potential social challenges, including the displacement of current residents. Overall, the project is poised to serve as a catalyst for urban renewal and sustainable development in one of Nairobi’s most dynamic areas.

- Infrastructure Sector

During the week, the cabinet approved the construction of the Rironi-Mau Summit road project. This development is set to transform a critical transportation corridor in Kenya by upgrading the existing road from Rironi near Nairobi to Mau Summit in Nakuru County into a modern four-lane dual carriageway. The project, with an estimated cost of Kshs 175.0 bn, is scheduled to begin in June 2025 and conclude in June 2027, aligning with strategic government infrastructure plans ahead of the 2027 general elections.

Covering a primary stretch of approximately 181 kilometers—supplemented by an additional 62 kilometers along the Rironi–Mai Mahiu–Naivasha Road—the project will address chronic congestion on one of Kenya’s busiest routes. Improved road quality is expected to reduce travel times and lower transportation costs, thereby boosting trade and tourism across key regions like Naivasha and Nakuru. This enhanced connectivity is anticipated to stimulate local economies by creating thousands of jobs during the construction phase and by attracting further investments in regional development.

A significant shift in the project’s contractual dynamics has taken place as well. Initially awarded to a French consortium, the contract was later transferred to a Chinese contractor following discussions between Presidents Ruto and Xi Jinping. This change, implemented within a public-private partnership framework, is designed to manage risks more effectively, with the contractor set to recover investments through toll fees over a 30-year period.

We expect that the improved road will have a transformative impact on the real estate sector along the corridor. Enhanced accessibility and reduced travel times will likely drive up property values in previously underdeveloped areas. Investors are expected to seize new opportunities for both residential and commercial developments, particularly in towns such as Naivasha, Gilgil, and Nakuru. This influx of development is anticipated to spur further urbanization, reshape local real estate markets, and create vibrant communities, thereby contributing to sustained economic growth in the region.

- Real Estate Investments Trusts (REITs)

On the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 25.4 and Kshs 22.2 per unit, respectively, as per the last updated data on 7th March 2025. The performance represented a 27.0% and 11.0% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. The volumes traded for the D-REIT and I-REIT came in at Kshs 12.8 mn and Kshs 35.6 mn shares, respectively, with a turnover of Kshs 323.5 mn and Kshs 791.5 mn, respectively, since inception in February 2021. Additionally, ILAM Fahari I-REIT traded at Kshs 11.0 per share as of 7th March 2025, representing a 45.0% loss from the Kshs 20.0 inception price. The volume traded to date came in at 138,600 shares for the I-REIT, with a turnover of Kshs 1.5 mn since inception in November 2015.

REITs offer various benefits, such as tax exemptions, diversified portfolios, and stable long-term profits. However, the ongoing decline in the performance of Kenyan REITs and the restructuring of their business portfolios are hindering significant previous investments. Additional general challenges include:

- Insufficient understanding of the investment instrument among investors leading to a slower uptake of REIT products,

- Lengthy approval processes for REIT creation,

- High minimum capital requirements of Kshs 100.0 mn for REIT trustees compared to Kshs 10.0 mn for pension funds Trustees, essentially limiting the licensed REIT Trustee to banks only

- The rigidity of choice between either a D-REIT or and I-REIT forces managers to form two REITs, rather than having one Hybrid REIT that can allocate between development and income earning properties

- Limiting the type of legal entity that can form a REIT to only a trust company, as opposed to allowing other entities such as partnerships, and companies,

- We need to give time before REITS are required to list – they would be allowed to stay private for a few years before the requirement to list given that not all companies maybe comfortable with listing on day one, and,

- Minimum subscription amounts or offer parcels set at Kshs 0.1 mn for D-REITs and Kshs 5.0 mn for restricted I-REITs. The significant capital requirements still make REITs relatively inaccessible to smaller retail investors compared to other investment vehicles like unit trusts or government bonds, all of which continue to limit the performance of Kenyan REITs.

We expect Kenya’s Real Estate sector to remain on a growth trend, supported by: i) demand for housing sustained by positive demographics, such as urbanization and population growth rates of 3.8% p.a and 2.0% p.a, respectively, against the global average of 1.7% p.a and 0.9% p.a, respectively, as at 2023,, ii) activities by the government under the Affordable Housing Program (AHP) iii) heightened activities by private players in the residential sector iv) increased investment by local and international investors in the retail sector,v) improved infrastructure throughout the country. However, challenges such as rising construction costs, strain on infrastructure development (including drainage systems), high capital requirements for REITs, and existing oversupply in select Real Estate sectors will continue to hinder the sector’s optimal performance by limiting developments and investments.

According to the ACTSERV Q4’2024 Pension Schemes Investments Performance Survey, the five-year average return for segregated schemes over the period 2020 to 2024 was 4.5% with the performance fluctuating over the years to a high of 13.2% in Q4’2024 and a low of 0.7% in Q4’2021 reflective of the markets performance. Notably, segregated retirement benefits scheme q/q returns increased to a 13.2% return in Q4’2024, up from the 3.1% gain recorded in Q4’2023. The y/y growth in overall returns was largely driven by the 18.7% points increase in returns from Equities to 15.7% from a loss of 3.0% in Q4’2023 attributable to the increased corporate earnings and attractive valuations as well as the 13.3% gain from fixed income. The performance was however weighed down by the 17.2% points decline in the Offshore returns to 0.8%, from 18.0% in Q4’2023 majorly attributable to the uncertainty about the US general election, China’s weak economic data and the strengthening of the Kenyan Shilling. This week, we shall focus on understanding Retirement Benefits Schemes and look into the quarterly performance and current state of retirement benefits schemes in Kenya with a key focus on Q4’2024;

We have been tracking the performance of Kenya’s Pension schemes with the most recent topical being, Retirement Benefits Schemes Q3’2024 Performance Report, done in December 2024. This week, we shall focus on understanding Retirement Benefits Schemes and looking into the historical and current state of retirement benefits schemes in Kenya with a key focus on 2024 (latest official data) and what can be done going forward. We shall also analyze other asset classes that the schemes can tap into to achieve higher returns. Additionally, we shall look into factors and challenges influencing the growth of the RBSs in Kenya as well as the actionable steps that can be taken to improve the pension industry. We shall do this by looking into the following:

- Introduction to Retirement Benefits Schemes in Kenya,

- Historical and Current State of Retirement Benefits Schemes in Kenya,

- Factors Influencing the Growth of Retirement Benefits Scheme in Kenya,

- Challenges that Have Hindered the Growth of Retirement Benefit Schemes, and,

- Recommendations on Enhancing the Performance of Retirement Benefits Schemes in Kenya;

Section I: Introduction to Retirement Benefits Schemes in Kenya

A retirement benefits scheme is a savings avenue that allows contributing individuals to make regular contributions during their productive years into the scheme and thereafter get income from the scheme upon retirement. There are a number of benefits that accrue to retirement benefits scheme members, including:

- Income Replacement – Retirement savings ensure that your income stream does not stop even when you stop working. After retirement, many people experience a decline in the amount and stability of income relative to their productive years. Retirement savings ensure that this decline is manageable or non-existent and enables you to be able to live the lifestyle you desire even after retirement,

- Compounded and Tax-free interest – Savings in a pension scheme earn compounded interest which means that your money grows faster as the interest earned is reinvested. Additionally, retirement schemes’ investments are tax-exempt meaning that the schemes have more to reinvest,

- Tax-exempt contributions – Pension contributions enjoy a monthly tax relief of up to Kshs 30,000.0 – this lessens the total PAYE deducted from your earnings,

- Avoid old age poverty – By providing an income in retirement, pension schemes ensure that the scheme members do not experience old age poverty where they have to rely on their family, relatives, and friends for survival, and,

- Home Ownership - Savings in a pension scheme can help you achieve your dream of owning a home. This can be done through a mortgage or a direct residential house purchase using your pension savings. A member may assign up to 60.0% of their pension benefits or the market value of the property, whichever is less, to provide a mortgage guarantee. The guarantee may enable the member to acquire immovable property on which a house has been erected, erect a house, add, or carry out repairs to a house, secure financing or waiver, as the case may be, for deposits, stamp duty, valuation fees and legal fees and any other transaction costs required. On the other hand, a pension scheme member may utilize up to 40.0% of their benefits to purchase a residential house directly subject to a maximum allowable amount of Kshs 7.0 mn and the amount they use should not exceed the buying price of the house.

Section II: Historical and the Current State of Retirement Benefits Schemes in Kenya

- Growth of Retirement Benefits Schemes

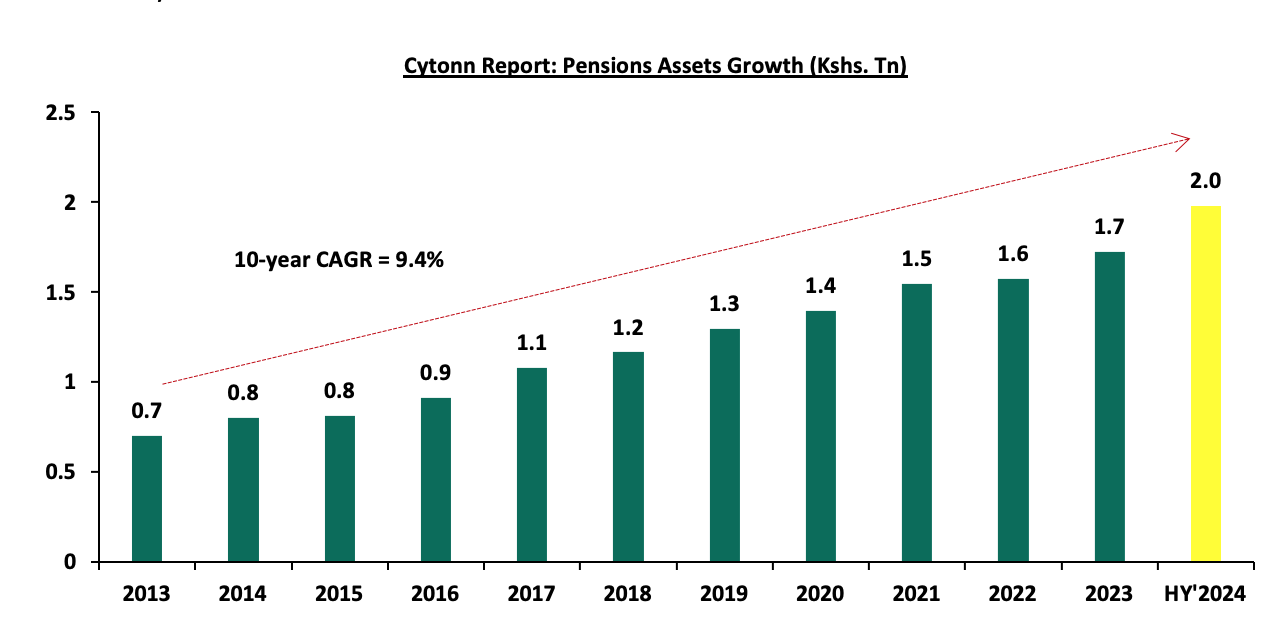

According to the latest Retirement Benefits Authority (RBA) Industry Report for June 2024, assets under management for retirement benefits schemes increased by 14.7% to Kshs 2.0 tn in June 2024 from the Kshs 1.7 tn recorded in December 2023. The growth of the assets is attributed to the improved market and economic conditions during the period as evidenced by improved business conditions, eased inflationary pressures and stability of the exchange rate. Notably, on a year-on -year basis, assets under management increased by 16.1% from the Kshs 1.7 tn recorded in June 2023, partly attributable to the enhanced contributions to the mandatory scheme, NSSF, which began in earnest in February 2023 following the court of appeal ruling. The increase in NSSF contribution limits from February 2025, marking the third phase of implementation under the NSSF Act of 2013, is expected to boost the overall pension sector's assets under management (AUM) by increasing retirement savings.

The graph below shows the growth of Assets under Management of the retirement benefits schemes over the last 10 years:

Pensions AUM increased by 14.7% to Kshs 2.0 tn in June 2024 from the Kshs 1.7 tn recorded in December 2023 and by 16.1% on a y/y basis to Kshs 2.0 mn in HY’2024 from Kshs 1.7 mn in HY’2023, which is 6.7% points increase from the 9.4% growth between 2023 and 2022. Additionally, the 9.4% increase in Assets Under Management is 7.5% points increase in growth from the 1.9% growth that was recorded in 2022, demonstrating the significant role that the enhanced NSSF contributions made to the recovery of the industry’s performance following a difficult period in 2022 due to the court ruling that declared revival of NSSF Act No.45 of 2013 unconstitutional. The primary goal of the act was to broaden the NSSF’s benefit coverage, range, and scope as well as improve the adequacy of benefits paid out of the scheme by the Fund amongst others.

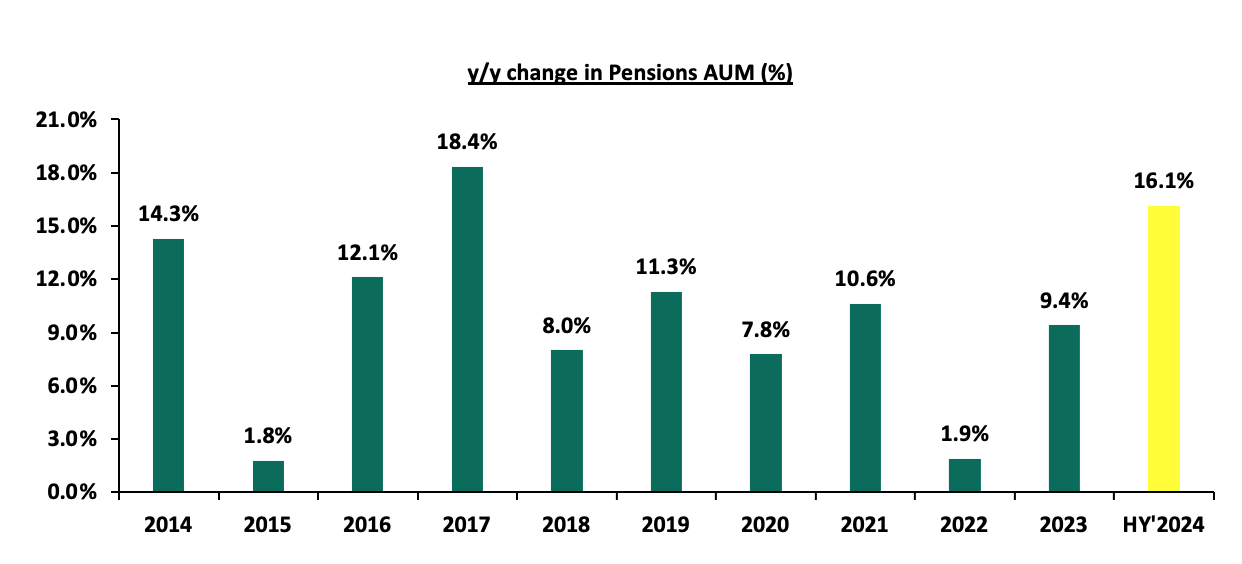

The chart below shows the y/y changes in the assets under management for the schemes over the years.

Despite the continued growth, Kenya is characterized by a low saving culture with research by the Federal Reserve Bank indicating that only 14.2% of the adult population in the labor force save for their retirement in Retirement Benefits Schemes (RBSs).

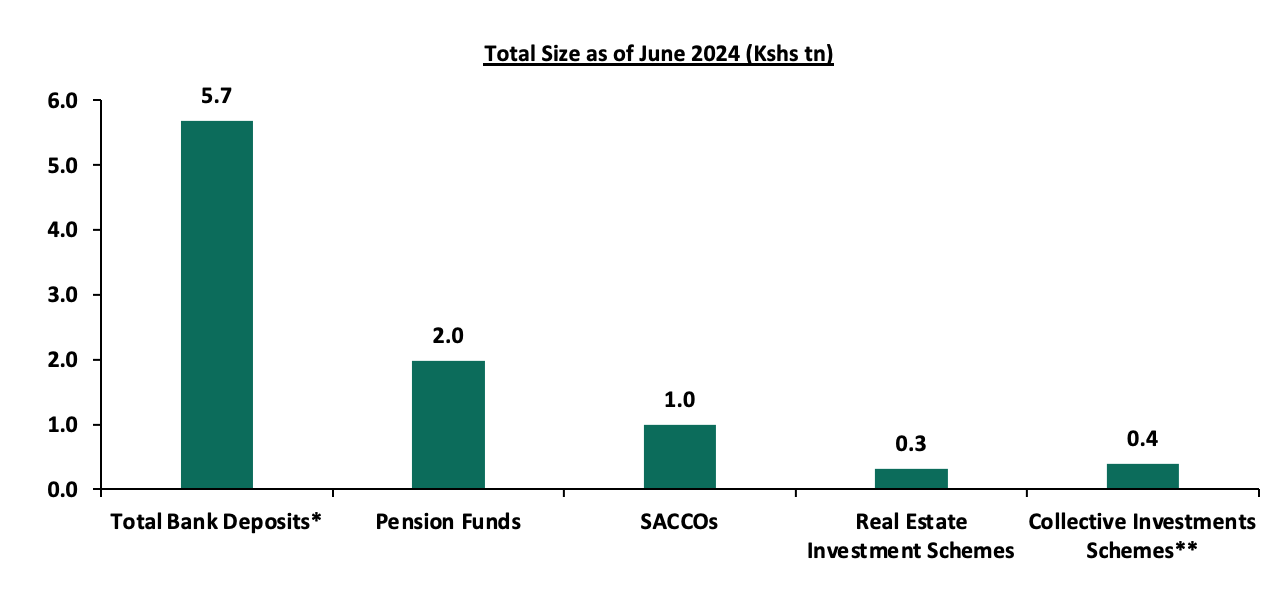

In Kenya, pension funds hold a substantial share of financial assets, consistently growing due to mandatory and voluntary contributions under the National Social Security Fund (NSSF) Act of 2013 regulations. In comparison, bank deposits remain the largest financial pool, reflecting their role as the primary savings vehicle driven by their liquidity, security, and accessibility, though they offer lower returns. Capital markets products, including unit trusts, REITs, are relatively smaller highlighting the nascent stage of capital markets in Kenya, but expanding as investors seek diversification and higher yields. SACCOs play a crucial role in cooperative-based savings and credit access, especially for middle-income earners.

The graph below shows the Assets under Management of Pensions against other Capital Markets products and bank deposits:

Sources: CMA, RBA, SASRA and REIT Financial Statements, *as of Sept 2024, **as of Dec 2024

- Retirement Benefits Schemes Allocations and Various Investment Opportunities

Retirement Benefits Schemes strategically allocate funds across various asset classes available in the market to safeguard members' contributions while striving to generate attractive returns. These schemes have access to a diverse range of investment opportunities, including traditional asset classes such as equities and fixed income securities. Additionally, they can explore alternative investments such as real estate, private equity, infrastructure, and other non-traditional assets, which may offer higher returns and diversification benefits. The choice of investments is guided by the scheme's Investment Policy Statement (IPS), regulatory guidelines, and the need to align with the risk tolerance and long-term goals of the members. As such, the performance of Retirement Benefits Schemes in Kenya depends on a number of factors such as;

- Asset allocation,

- Selection of the best-performing security within a particular asset class,

- Size of the scheme,

- Risk appetite of members and investors, and,

- Investment horizon.

The Retirement Benefits (Forms and Fees) Regulations, 2000 offers investment guidelines for retirement benefit schemes in Kenya in terms of the asset classes to invest in and the limits of exposure to ensure good returns and that members’ funds are hedged against losses. According to RBA’s Regulations, the various schemes through their Trustees should formulate their own Investment Policy Statements (IPS) to Act as a guideline on how much to invest in the asset option and assist the trustees in monitoring and evaluating the performance of the Fund. However, the Investment Policy Statements often vary depending on risk-return profile and expectations mainly determined by factors such as the scheme’s demography and the economic outlook.

The Retirement Benefits Authority (RBA) regulations also emphasize the importance of diversification as a key principle in managing pension funds. By setting limits on exposure to specific asset classes, the regulations mitigate the risks associated with market volatility, ensuring that no single investment disproportionately affects the scheme's overall performance. Trustees are required to regularly review and update their Investment Policy Statements (IPS) to reflect changes in market conditions, economic dynamics, and the evolving needs of the scheme's members. This proactive approach not only aligns the investment strategy with the scheme’s objectives but also enhances accountability and transparency in fund management, safeguarding members’ retirement savings. The table below represents how the retirement benefits schemes have invested their funds in the past:

|

Cytonn Report: Kenyan Pension Funds’ Assets Allocation |

|||||||||||||

|

Asset Class |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

HY’2024 |

Average |

Limit |

|

Government Securities |

31.0% |

29.8% |

38.3% |

36.5% |

39.4% |

42.0% |

44.7% |

45.7% |

45.8% |

47.5% |

51.1% |

41.1% |

90.0% |

|

Immovable Property |

17.0% |

18.5% |

19.5% |

21.0% |

19.7% |

18.5% |

18.0% |

16.4% |

15.8% |

14.0% |

11.9% |

17.3% |

30.0% |

|

Quoted Equities |

26.0% |

23.0% |

17.4% |

19.5% |

17.3% |

17.6% |

15.6% |

16.5% |

13.7% |

8.4% |

8.8% |

16.7% |

70.0% |

|

Guaranteed Funds |

11.0% |

12.2% |

14.2% |

13.2% |

14.4% |

15.5% |

16.5% |

16.8% |

18.9% |

20.8% |

20.5% |

15.8% |

100.0% |

|

Fixed Deposits |

5.0% |

6.8% |

2.7% |

3.0% |

3.1% |

3.0% |

2.8% |

1.8% |

2.7% |

4.8% |

2.7% |

3.5% |

30.0% |

|

Listed Corporate Bonds |

6.0% |

5.9% |

5.1% |

3.9% |

3.5% |

1.4% |

0.4% |

0.4% |

0.5% |

0.4% |

0.4% |

2.5% |

20.0% |

|

Offshore |

2.0% |

0.9% |

0.8% |

1.2% |

1.1% |

0.5% |

0.8% |

1.3% |

0.9% |

1.6% |

2.0% |

1.2% |

15.0% |

|

Cash |

1.0% |

1.4% |

1.4% |

1.2% |

1.1% |

1.2% |

0.9% |

0.6% |

1.1% |

1.5% |

1.2% |

1.1% |

5.0% |

|

Unquoted Equities |

1.0% |

0.4% |

0.4% |

0.4% |

0.3% |

0.3% |

0.2% |

0.2% |

0.3% |

0.2% |

0.2% |

0.4% |

5.0% |

|

REITs |

0.0% |

0.0% |

0.1% |

0.1% |

0.1% |

0.0% |

0.0% |

0.0% |

0.0% |

0.6% |

0.6% |

0.1% |

30.0% |

|

Private Equity |

0.0% |

0.0% |

0.0% |

0.0% |

0.1% |

0.1% |

0.1% |

0.2% |

0.2% |

0.3% |

0.4% |

0.1% |

10.0% |

|

Others e.g. unlisted commercial papers |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.1% |

0.2% |

- |

0.0% |

0.0% |

10.0% |

|

Commercial Paper, non-listed bonds by private companies |

- |

- |

- |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.0% |

0.2% |

0.0% |

10.0% |

|

Total |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

Source: Retirement Benefits Authority

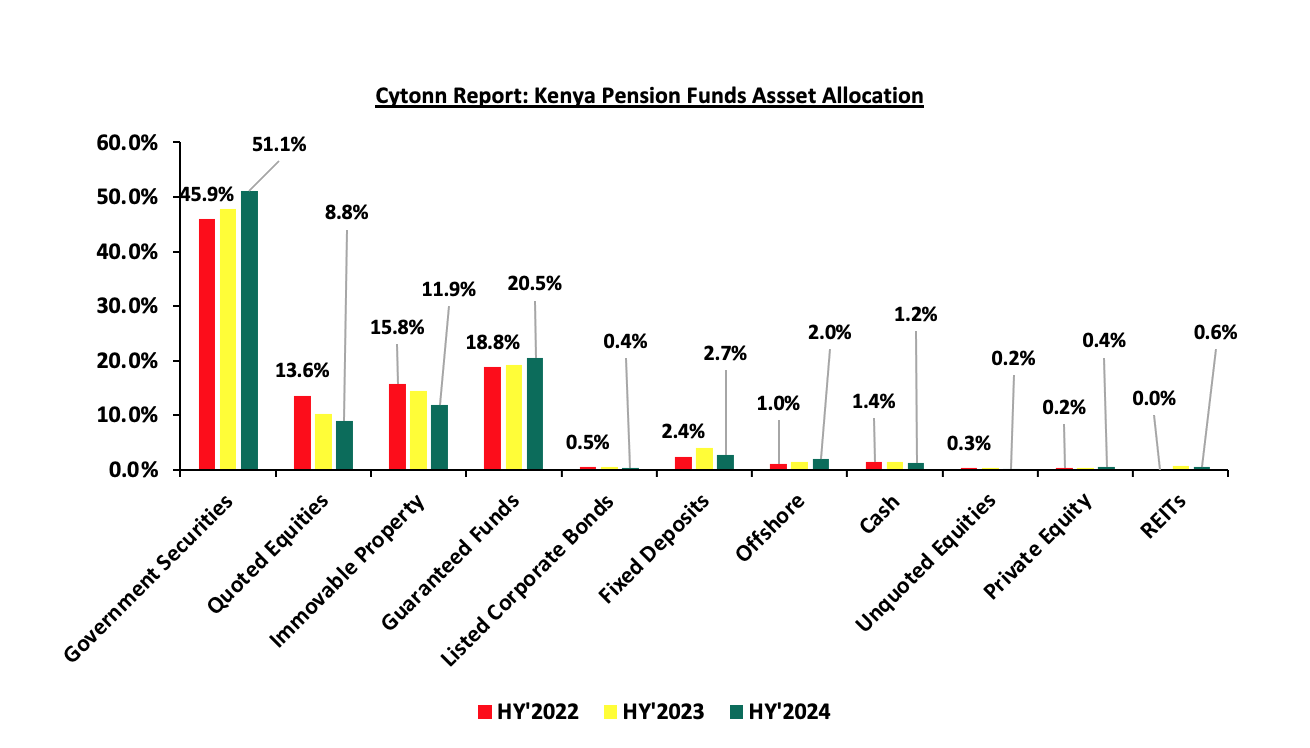

Retirement benefits schemes have for a long time skewed their investments towards traditional assets, mostly, government securities and the equities market, averaging 57.8% as of 30th June 2024 for the two asset classes, leaving only 42.2% for the other asset classes. However, as pension schemes seek higher returns, diversification, and inflation hedging, there has been a growing shift towards alternative investments that include immovable property, private equity as well as Real Estate Investments Trusts (REITs). It is vital to note, that in HY’2024 the second largest increase in allocation was recorded in investments in private equity by 63.3% to Kshs 8.8 bn from Kshs 5.4 bn recorded in HY’2023 and investments in Real Estate Investments Trusts increased by 4.5% to Kshs 11.1 bn in HY’2024 from Kshs 10.6 bn in HY’2023. However, allocation to immovable property decreased by 4.1% to Kshs 236.3 bn in HY’2024 from Kshs 246.3 bn in HY’2023.

Key Take-outs from the table above are;

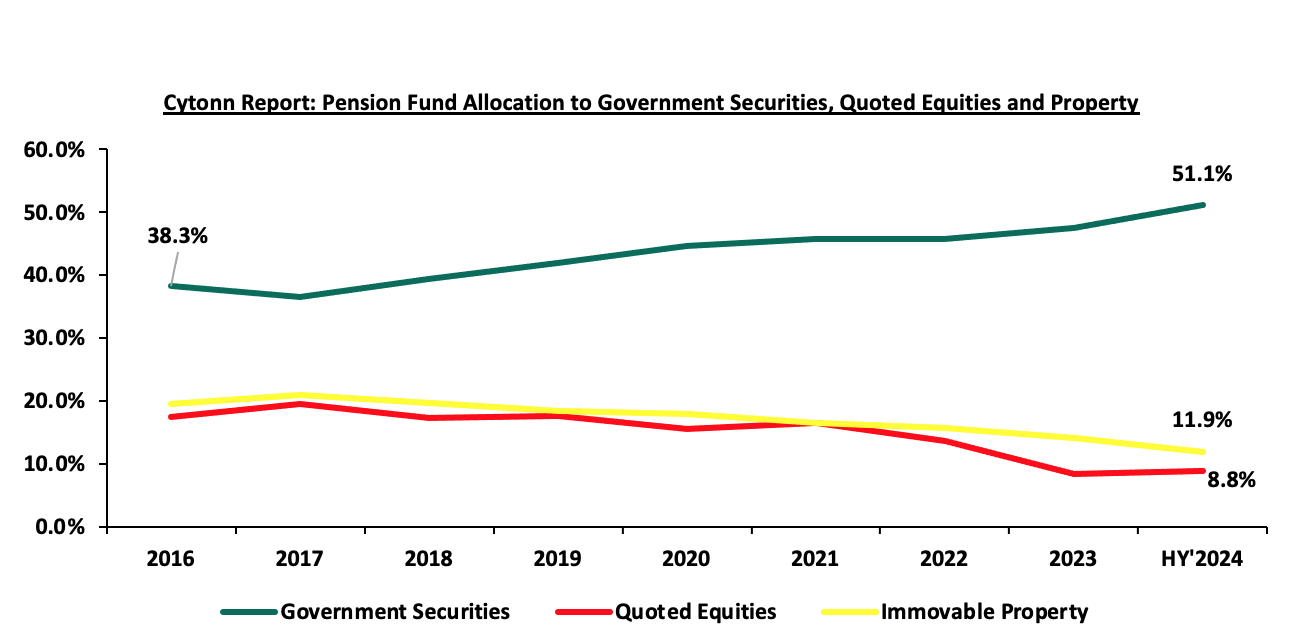

- Schemes in Kenya allocated an average of 57.8% of their members’ funds towards government securities and Quoted Equities between the period of 2013 and end of June 2024. The 41.1% average allocation to government securities is the highest among the asset classes attributable to safety assurances of members’ funds because of low-risk associated with government securities. Notably, allocation towards government securities increased by 3.6% points to 51.1% in HY’2024 from 47.5% in FY’2023 attributable to high yields by the government papers and increased issuance of treasury bonds to finance fiscal deficits as well as increase domestic borrowing during the period,

- The allocation towards quoted equities increased to 8.8% as of June 2024, from 8.4% in December 2023 on the back of improved performance in the Kenyan equities market as evidenced by 19.0% of the NASI index in H1’2024, driven by a recovery in corporate earnings and increased investor confidence. Favourable macroeconomic conditions, such as easing inflation and a strengthened shilling, boosted market sentiment, have encouraged trustees to allocate more funds to equities during the period,

- Retirement Benefits Schemes investments in offshore markets increased by 0.4% points to 2.0% as of June 2024, from 1.6% in December 2023 as a result of the opportunities in developed and emerging markets, and currency hedging strategies that allowed schemes to benefit from foreign exchange gains, and,

- The 0.2% points increase in investment in commercial paper, non-listed bonds issued by private companies was due to an investment of Kshs 3.0 bn in Linzi sukuk bond by one of the schemes during the period.

The chart below shows the allocation by pension schemes on the three major asset classes over the years:

Source: RBA Industry report

- Performance of the Retirement Benefit Schemes

According to the ACTSERV Q4’2024 Pension Schemes Investments Performance Survey, the five-year average return for segregated schemes over the period 2020 to 2024 was 4.5% with the performance fluctuating over the years to a high of 13.2% in 2024 and a low of 0.7% in 2021 reflective of the markets performance. Notably, segregated retirement benefits scheme returns increased to a 13.2% return in Q4’2024, up from the 3.1% gain recorded in Q4’2023. The y/y growth in overall returns was largely driven by the 18.7% points increase in returns from Equities to 15.7% from a loss of 3.0% in Q4’2023 attributable to the increased corporate earnings and attractive valuations as well as the 13.3% gain from fixed income. The performance was however weighed down by the 17.2% points decline in the Offshore returns to 0.8%, from 18.0% in Q4’2023 majorly attributable to the uncertainty about the US general election and China’s weak economic data. The chart below shows the performance of segregated pension schemes since 2015:

Source: ACTSERV Survey Reports (Segregated Schemes), computed for quarters ending 31st December

The key take-outs from the graph include:

- Schemes recorded a 13.2% gain in Q4’2024, representing 12.8% points increase from the 0.4% gain recorded in Q3’2024. The performance was largely driven by the 15.7% returns from Equities attributable to the increased corporate earnings and attractive valuations as well as the 13.3% gain from fixed income. The performance was however weighed down by the 3.9% points decline in the Offshore returns to 0.8%, from 4.7% in Q3’2024 majorly attributable to the uncertainty about the US general election and China’s weak economic data, and,

- Returns from segregated retirement funds have exhibited significant fluctuations, ranging from a high of 13.2% recorded in Q4’2024 to a low of 0.7% in Q4’2021, highlighting the sensitivity of fund performance to market and economic conditions.

The survey covered the performance of asset classes in three broad categories: Fixed Income, Equity, Offshore, and Overall Return.

Below is a table showing the fourth quarter performances over the period 2020-2024:

|

Cytonn Report: Quarterly Performance of Asset Classes (2020 – 2024) |

|||||||

|

|

Q4'2020 |

Q4'2021 |

Q4'2022 |

Q4’2023 (a) |

Q4'2024 (b) |

Average (2020-2024) |

% points change (b-a) |

|

Equity |

5.9% |

(4.4%) |

(0.2%) |

(3.0%) |

15.7% |

2.8% |

18.7% |

|

Fixed Income |

2.0% |

2.2% |

2.9% |

4.0% |

13.3% |

4.9% |

9.3% |

|

Offshore |

8.5% |

7.2% |

7.4% |

18.0% |

0.8% |

8.4% |

(17.2%) |

|

Overall Return |

3.0% |

0.7% |

2.3% |

3.1% |

13.2% |

4.5% |

|

Source: ACTSERV Surveys

Key take-outs from the table above include;

- Returns from Equity investments recorded a significant increase by 18.7% points to a 15.7% gain in Q4’2024, from the 3.0% loss recorded in Q4’2023, driven by strong corporate earnings, attractive stock valuations and the the performance of the Kenyan currency in 2024, having gained by 17.4%, to close the year at Kshs 129.3 from the Kshs 157.0 recorded at the beginning of 2024, which boosted investor confidence. Additionally, declining bond yields made bonds less appealing, prompting investors to shift their focus to equities, further supporting market gains,

- Returns from Fixed Income also recorded an increase of 9.3% points to 13.3% in Q4’2024 from 4.0% recorded in Q4’2023. This performance in Q4’2024 is partially attributable to improved market conditions compared to a similar period in 2023, as evidenced by the higher yields on government securities and improved investor sentiment towards government debt instruments as well as an ease in inflationary pressures with the average inflation rate for Q4’2024 coming in at 2.8% from in 6.8% Q4’2023, and,

- Returns from the Offshore investments recorded a significant decrease to a 0.8% return in Q4’2024 from the 18.0% recorded in Q4’2023. The performance was partly attributable to the uncertainty surrounding the US general election introducing market volatility, limiting the gains that segregated schemes could achieve from their offshore allocations.

Other Asset Classes that Retirement Benefit Schemes Can Leverage on

- Alternative Investments (Immovable Property, Private Equity and REITs)

Retirement benefits schemes have for a long time skewed their investments towards traditional assets, mostly, government securities and the equities market, averaging at 57.8% in 10 years, as of 30th June 2024, leaving only 42.2% for all the other asset classes. In the asset allocation, alternative investments that include immovable property, private equity as well as Real Estate Investments Trusts (REITs) account for an average of only 17.5% against the total allowable limit of 70.0%. In terms of overall asset allocation, alternative investments still lagged way behind the other asset classes, as demonstrated in the graph below;

Source: RBA Industry Report

Alternative Investments refers to investments that are supplemental strategies to traditional long-only positions in equities, bonds, and cash. They differ from traditional investments on the basis of complexity, liquidity, and regulations and can invest in immovable property, private equity, and Real Estate Investment Trusts (REITs) to a limit of 70.0% exposure. We believe that Alternative Investments, including REITs, would play a significant role in improving the performance of retirement benefits schemes by providing opportunities for higher returns and enhanced portfolio resilience.

Alternative Investments, such as immovable property, private equity, and REITs, offer not only diversification and competitive long-term returns but also the potential to hedge against inflation. Investments in real assets like immovable property and REITs often benefit from inflationary environments, as property values and rental incomes tend to rise with inflation. Additionally, private equity provides access to high-growth sectors, such as technology and renewable energy, which are less correlated to traditional market movements, offering an attractive risk-adjusted return profile.

Furthermore, REITs in Kenya, particularly Development and Income REITs, present unique opportunities for retirement schemes. They provide exposure to the real estate sector without the liquidity constraints and management challenges associated with direct property ownership. As the Kenyan real estate market continues to mature and regulatory frameworks for REITs improve, these instruments are becoming more viable for retirement funds seeking stable, inflation-protected income streams and long-term growth. By strategically allocating a portion of their portfolio to alternative investments, retirement schemes can enhance overall returns while safeguarding members' contributions against market volatility.

- Public Private Partnerships

According to the Retirement Benefits Authority Investment Regulations and Policies, pension schemes can invest up to 10.0% of their total assets under management in debt instruments for the financing of infrastructure or affordable housing projects approved under the Public Private Partnerships Act. Kenya's pension schemes are increasingly investing in infrastructure projects to diversify their portfolios, achieve stable long-term returns, and contribute to national development. A significant initiative in this direction is the Kenya Pension Funds Investment Consortium (KEPFIC), established in 2018. KEPFIC is a collective of prominent Kenyan retirement benefit funds that have united to make long-term investments in infrastructure and alternative assets within the region. As of the latest report, KEPFIC has mobilized over USD 113.0 mn into projects such as roads, student housing, and affordable housing, involving 88 local pension funds.

Despite there being 1,075 registered pension schemes in Kenya, only 88 have actively participated in infrastructure investments through KEPFIC, highlighting a significant untapped opportunity. With the Retirement Benefits Authority allowing schemes to allocate up to 10.0% of their assets into such projects, there remains substantial room for more pension funds to diversify into infrastructure and affordable housing. A prime example of this opportunity is the Usahihi Expressway, a 440-kilometer dual carriageway connecting Nairobi and Mombasa, which seeks to raise approximately USD 1.0 bn from local pension funds and financial institutions as part of its estimated USD 3.5 bn cost. The Usahihi Expressway is expected to generate revenue primarily through toll collections over the 30-year concession period. Toll roads historically provide stable, inflation-hedged cash flows, making them attractive to long-term institutional investors like pension funds. Toll roads generate cash flows that grow over time, as toll rates can be adjusted for inflation and traffic volumes are expected to increase. By participating in this Public-Private Partnership, pension schemes can not only enhance portfolio returns and manage long-term risks but also play a crucial role in national development by financing transformative projects that spur economic growth.

Section III: Factors Influencing the Growth of Retirement Benefit Schemes

The retirement benefit scheme industry in Kenya has registered significant growth in the past 10 years with assets under management growing at a CAGR of 9.4% to Kshs 1.7 tn in FY’2023, from Kshs 0.7 tn in FY’2013. The growth is attributable to:

- Legislation – The National Assembly, on 26th December 2024, assented to the Tax Laws (Amendment) Bill 2024. The Bill amended the Income Tax Act by increasing the deductible amount for contributions to registered pension, provident, and individual retirement funds or public pension schemes to Kshs 360,000 annually from Kshs 240,000 and introduced provisions that allow contributions to post-retirement medical funds up to Kshs 15,000 per month—to be tax-deductible. Additionally, income from registered retirement benefits schemes is now tax-exempt for individuals who have reached the retirement age set by their scheme, those withdrawing benefits early due to ill health, or those exiting a registered scheme after at least 20 years of membership. These changes aim to adjust for inflation and modernize deductions that have remained unchanged for over a decade. The revisions are expected to reduce individual taxable income and enhance retirement benefits. In addition, the implementation of the National Social Security Fund Act, 2013 is entering its third year and is expected to foster the growth of the pension industry by allowing both the employees in the formal and informal sector to save towards their retirement. The upward revision of the NSSF Tier 1 and Tier 2 contribution limits effective from February 2025, to Kshs 8,000 and 72,000 respectively from Kshs 7,000 and Kshs 36,000 respectively is expected to enhance retirement savings, improving pension adequacy for retirees,