Apr 20, 2019

Following the release of FY’2018 results by Kenyan banks, the Cytonn Financial Services Research Team undertook an analysis on the financial performance of the listed banks and identified the key factors that shaped the performance of the sector, and our expectations for the banking sector in 2019.

The report is themed “Growth and Recovery in a tough operating environment”, as we assess the key factors that influenced the improved performance of the banking sector in 2018, the key challenges, and also areas that will be crucial for growth of banking sector going forward. As a result, we seek to answer the questions, (i) “what influenced the banking sector’s performance?”, and (ii) “what should be the focus areas for the banking sector going forward?” as the sector navigates the relatively tough operating environment. As such, we shall address the following:

- Key Themes that Shaped the Banking Sector in FY’2018;

- Performance of the Banking Sector in FY’2018; and,

- Outlook and Focus Areas of the Banking Sector Players Going Forward.

Section I: Key Themes that Shaped the Banking Sector in FY’2018:

Below, we highlight the key themes that shaped the banking sector in FY’2018, which include consolidation, regulation, asset quality and improved earnings:

- Consolidation – The banking sector has continued to witness consolidation activity, as players in the sector are either acquired or merged leading to formation of relatively larger and possibly more stable entities. Consolidations that took place in 2018 include:

- In August 2018, State Bank of Mauritius (SBM) Bank Kenya completed the acquisition of select assets and liabilities of Chase Bank Limited, which was under receivership. Following the agreement between the Central Bank of Kenya (CBK), Kenya Deposit Insurance Corporation (KDIC), and SBM Bank Kenya, 75.0% of the value of all moratorium deposits at Chase Bank were be transferred to SBM Bank Kenya. The remaining 25.0% remained with Chase Bank. This was a major milestone in Kenya’s banking sector as it the first successful instance, in the history of Kenya, of a bank being successfully brought out of receivership. We note that the deal highlighted the continued attractiveness of the Kenyan banking sector, as banks, both local and foreign, drive their growth inorganically through mergers and acquisitions. This is especially evident with Morocco-based bank, Attijariwafa Bank highlighting its plans for several acquisitions in Africa in the coming year, with Kenya being one of its key focus areas. The bank, which has an asset base of USD 51.0 bn, indicated it was looking to make an acquisition in Kenya, targeting one of the 5 largest banks in Kenya, meaning that one of KCB Group, Equity Group, Co-operative Bank, Standard Chartered Bank Kenya and Diamond Trust Bank Kenya, would be the bank’s targets,

- The Central Bank of Kenya (CBK) and Kenya Deposit Insurance Corporation (KDIC) announced the acceptance of a binding offer from KCB Group, to acquire certain assets and liabilities of Imperial Bank Limited under Receivership (IBLR). The transaction will see an additional 19.7% of deposits availed to depositors, an addition to the 35.0% availed, on the acceptance of the binding offer by KDIC and CBK in December 2018. The remaining deposit balances will be availed to depositors in three tranches, (i) 12.5% after the official signing of the agreement, a further 12.5% one-year after the signing of the agreement, and (ii) 25.0% balance on the second, third and fourth anniversaries of the signing of the agreement. The split of the 25.0% deposits in the second, third and fourth anniversaries is however yet to be disclosed. The deposits will continue to earn interest in line with KCB’s prevailing deposit rates on its products. However, the recovery does not include the realization of approximately Kshs 36.0 bn of loans, translating to 50.0% of the current loan balances, linked to ongoing litigation. KCB confirmed that it would take over five branches of IBLR, out of the 26 that IBLR had prior to going under receivership. The completion of the transaction, in our view, will continue to instill confidence in the banking sector’s stability, as it provides a remediation route for banks that have encountered turbulence in their operations, as well as safeguarding of depositors’ interests. We also are of the view that there should be no recourse for failures induced by lax corporate governance, and that the enforcement of strict regulations, operating procedures and corporate governance principles is key to avoid similar occurrences in the future. KCB Group also issued its proposal to acquire 100.0% of all the ordinary shares of National Bank of Kenya on 18th April 2019, through a share swap of 1 ordinary share of KCB for every 10 NBK shares. The swap will be after the conversion of 1.135 bn preference shares in NBK, to ordinary shares. The transaction, is subject to ratification by the shareholders and the regulatory authorities,

- In January 2019, the directors of NIC Group and Commercial Bank of Africa (CBA) announced their agreement to a proposed merger between the two banks that was first announced on 6th December 2018, with the shareholders of NIC Group accepting the merger proposition during the Annual General Meeting (AGM) on 17th April 2019. The proposed merger is expected to be completed upon fulfilment of a certain set of conditions, with the merged entity expected to commence its operations at the onset of Q3’2019. The proposed transaction will be executed through a share swap in the ratio of 53:47 between CBA and NIC, implying that shareholders of CBA Group will be entitled to own 53.0% of the merged entity’s issued shares while shareholders of NIC Group will be allotted 47.0% of the combined entity. Given that NIC Group has 703.9 mn issued shares, it will have to issue 793.8 mn new shares to CBA shareholders, in order to adhere to the 53:47 share swap ratio. The merged company, NIC Group, is set to remain listed on the Nairobi Securities Exchange (NSE).

The increased consolidation activity continued into 2019, as CBA Group issued Jamii Bora owners with a buyout offer of Kshs 1.4 bn, to acquire a 100.0% stake in the bank. With Jamii Bora’s equity position of Kshs 3.4 bn as at Q1’2018, without further injection, it would imply the transaction would happen at a P/Bv ratio of 0.4x. We note that the huge discount to equity was largely due to Jamii Bora’s deteriorating financial performance, whose genesis can be traced to the enactment of the Banking (Amendment) Act 2015 that capped interest chargeable on loans, as shown by the steep 21.0% decline in the loan book in the first full year of implementation of the Banking (Amendment) Act 2015. This consequently led to the decline in interest income, which declined by 36.2% to Kshs 1.4 bn in FY’2017, from Kshs 2.2 as at FY’2016. Consequently, operating income declined 57.8% to Kshs 0.5 bn from Kshs 1.3 bn in FY’2016. Since decline in income was faster than the 28.0% decline in total operating expenses to Kshs 1.3 bn from Kshs 1.8 bn, the bank consequently begun its loss making trend. The declining performance impacted its liquidity, with its liquidity position declining to (11.1%) as at Q1’2017, indicating its inability to meet any short-term obligations. The performance consequently enables CBA to offer a buyout at the huge discount to the book.

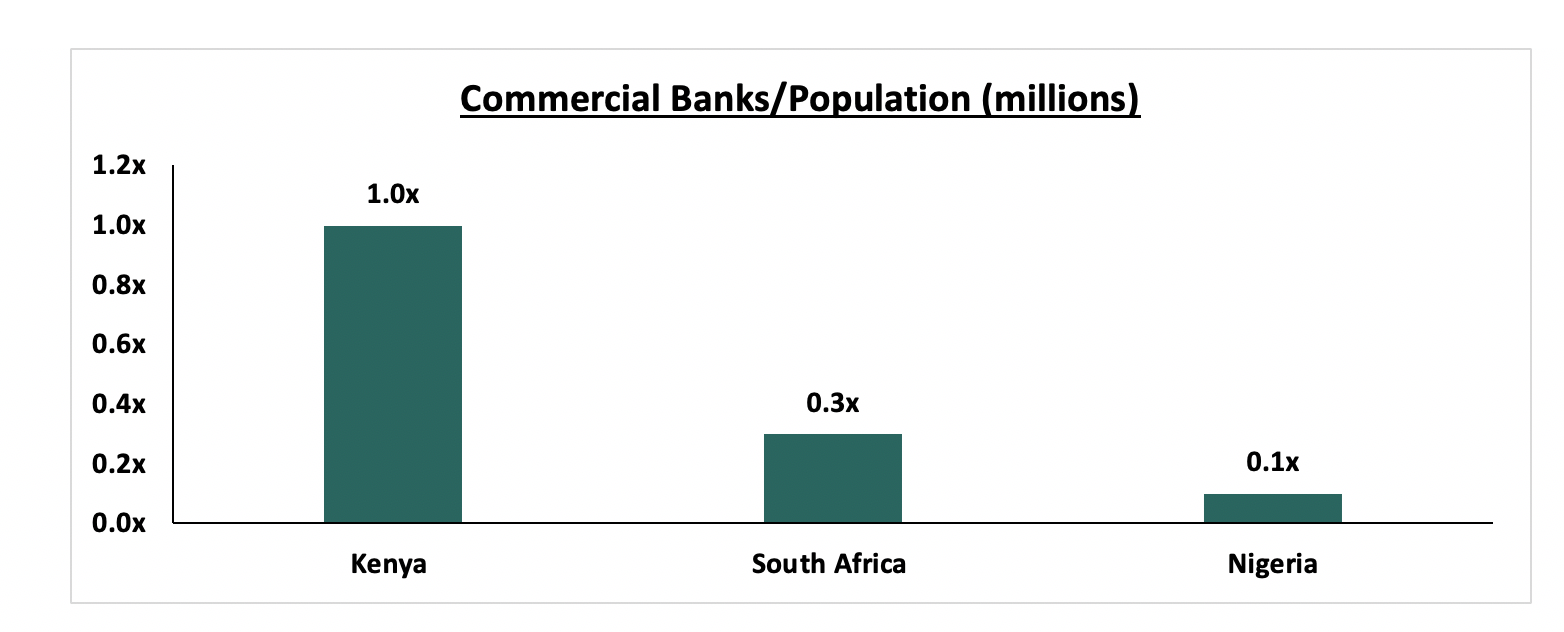

As noted in our focus note titled Consolidation in Kenya’s Banking Sector to Continue, we expect more consolidation in the banking sector, as the relatively weaker banks that probably do not serve a niche become acquired by the larger counterparts who have expertise in deposit gathering, or serve a niche in the market. Consolidation will also likely happen, as entities form strategic partnerships, as they navigate the relatively tougher operating environment that is exacerbated by the stiff competition among the various players in the banking sector. We maintain our view that Kenya continues to be overbanked when compared to other countries as shown in the chart below, necessitating a reduction in the number of players in the sector.

The table below summarizes the deals that have either happened or announced and expected to be concluded;

Acquirer

Bank Acquired

Book Value at Acquisition (Kshs bns)

Transaction Stake

Transaction Value (Kshs bns)

P/Bv Multiple

Date

KCB Group

National Bank of Kenya

7.0

100.0%

6.6

0.9x

19-Apr*

CBA Group

Jamii Bora Bank

3.4

100.0%

1.4

0.4x

19-Jan*

AfricInvest Azure

Prime Bank

21.2

24.2%

5.1

1.0x

19-Jan

NIC Group

CBA Group

30.5**

47:53***

18.0

0.6x

19-Jan*

KCB Group

Imperial Bank

Unknown

Undisclosed

Undisclosed

N/A

18-Dec

SBM Bank Kenya

Chase Bank ltd

Unknown

75.0%

Undisclosed

N/A

18-Aug

DTBK

Habib Bank Kenya

2.4

100.0%

1.8

0.8x

17-Mar

SBM Holdings

Fidelity Commercial Bank

1.8

100.0%

2.8

1.6x

16-Nov

M Bank

Oriental Commercial Bank

1.8

51.0%

1.3

1.4x

16-Jun

I&M Holdings

Giro Commercial Bank

3

100.0%

5

1.7x

16-Jun

Mwalimu SACCO

Equatorial Commercial Bank

1.2

75.0%

2.6

2.3x

15-Mar

Centum

K-Rep Bank

2.1

66.0%

2.5

1.8x

14-Jul

GT Bank

Fina Bank Group

3.9

70.0%

8.6

3.2x

13-Nov

Average

78.3%

1.4x

* Announcement date

** Book Value as of the announcement date

*** Shareholder swap ratio between NIC and CBA, respectively

- Regulation - Regulation remained a key aspect that affected the banking sector, with the regulatory environment evolving and becoming increasingly stringent. Key changes in the regulatory environment in 2018 include:

- IFRS 9 Implementation: The implementation of the standard took effect from 1st January 2018, and banks were expected to provision for both the incurred and expected credit losses, a deviation from the previous IAS 39, which required provisioning for only the incurred credit losses. As allowed for in the initial year of implementation, most banks charged the one-off impairments on their equity, hence the decline in the impairment charges, despite a deterioration in asset quality. To avoid the high provisioning levels that would be required, whilst earning higher risk-adjusted returns, banks became unwilling to lend to the private sector largely comprised of SMEs. Due to the adoption of more stringent lending policies, lending was largely skewed towards collateral based lending as opposed to unsecured lending. The IFRS 9 standard also requires the implementation of the Effective Interest Rate (EIR) Model, which required the amortization of the fees and commission received from loans, over the tenor of the loan. Thus on implementation of the standard, some banks recorded declines in the fees and commissions segment of Non-Funded Income (NFI),

- Draft Financial Markets Conduct Bill 2018: The National Treasury completed the Draft Financial Markets Conduct Bill, which seeks to create an effective financial consumer protection, make credit more accessible and consequently support financial innovation and competition. The bill’s main objectives thus are:

- Ensure better conduct by banks and other lenders in terms of extending credit to retail financial customers. By categorically not defining lenders as banks, this, in our view, might be the introduction of licensing for credit companies that are not banks, mainly the non-deposit taking Microfinance Institutions (MFIs),

- Provide consumer protection, mainly for retail customers by ensuring their credit contracts are clear and well understood in terms of interest, fees, charges and costs on credit facilities, thereby removing the opacity that has been existent in loan pricing. With consumer protection a key facet of the law, the law seeks to cast a wider net on financial services institutions that fall under the ambit of the proposed financial markets conduct authority, which, presumably, should rope in mobile lending institutions into this bracket,

- Banking Sector Charter: The Central Bank of Kenya proposed to introduce a Banking Sector Charter that will guide service provision in the sector. The Charter aims to instill discipline in the banking sector in order to make it responsive to the needs of the banked population. It is expected to facilitate a market-driven transformation of the Kenyan banking sector, thereby considerably improving the quality of service provided, and increasing access to affordable financial services for the unbanked and under-served population. The impending implementation of the charter possibly in 2019, will likely introduce risk-based credit scoring, which requires banks to extend credit on the basis of their credit scores, as determined by licensed credit reference bureaus, and,

- Removal of the 70.0% of the CBR interest on deposits: The National Assembly voted to retain the cap on loans in the Finance Act 2018, effectively retaining the 4.0% cap above the Central Bank Rate (CBR) on interest chargeable on loans. However, the 70.0% of the CBR floor on interest payable on deposits was removed, effectively enabling banks to pay lower interest on their deposits. With the removal of the same, banks have adjusted accordingly, with various players indicating a lowering of their interest expense requirements, and a possible improvement in the Net Interest Margin, whose benefits will be fully realized in 2019. We however do not expect a significant adjustment in the aggregate cost of funds, given that most banks had already commenced re-adjustments and reclassification of accounts to transactional and non-interest bearing accounts.

- Asset Quality – The banking sector continued to record a deterioration in its asset quality in 2018, as indicated by the rise in the Gross Non-Performing Loans (NPLs) ratio to 9.7%, from 8.5% in FY’2017, much higher than the 5-year average of 8.4%. The effects of the harsh operating environment experienced in 2017 spilled over to 2018, with the economic recovery from the previous year being slower than anticipated, which resulted in an increase in the number and value of bad loans. The major sectors touted by banks as leading in asset quality deterioration include trade, retail, manufacturing and real estate, all of which were affected by the tough operating environment experienced in 2017, which was occasioned by a volatile political environment due to the prolonged electioneering period, and a severe prolonged drought that affected the agriculture sector, which remains the largest GDP contributor. Delayed payments by the government was also identified as a contributing factor, which affected various sectors, with small to mid-sized entities affected the most. Owing to the deteriorating asset quality, banks continued to implement their stringent lending policies in a bid to curb the relatively rising NPLs, and consequently the associated impairment charges. In addition to this, the 100 bps decline in the Central Bank Rate (CBR) resulted in reduced margins, and risk-adjusted returns for banks. Consequently, listed banks, on average, slowed their pace of credit extension to the economy, as shown in the chart below, with the listed banking sector’s net loan growth coming in at 4.3%, slower than the 6.1% growth experienced in FY’2017. With reduced credit extension to the private sector, largely the Micro, Small and Medium Enterprises (MSME) who make up approximately 80.0% of the private sector, the country’s economic growth will likely be affected in the long-run, due to reduced availability of capital for the acquisition and creation of capital goods.

- Improved Earnings Growth: Listed banks, on aggregate, recorded an improved profitability in 2018 compared to 2017, as evidenced by the 13.8% rise in the core Earnings per Share (EPS), from a 1.0% decline in FY’2017. The performance highlights the banking sector’s resilience, even in the face of the relatively tougher operating environment. The improved performance was largely driven by an improvement in the total operating income, coupled with an improvement in the operating expenses. The Net Interest Income (NII) improved to record a 2.6% growth, compared to the 3.8% decline recorded in FY’2017. The improvement in NII was largely due to the improvement in interest income, as most banks earned higher interest income from government securities, benefitting from the re-allocations to government securities in 2017, as they yielded relatively higher risk-adjusted returns compared to loans. Focus on NFI also helped grow the bottom line, albeit banks registered a mixed performance in NFI growth, with 6 banks recording growths in NFI while 5 banks recorded declines in NFI. For banks that recorded declines in NFI, the declines were largely on the fees and commission income, with the decline in fees and commissions on loans attributed to reduced lending and consequently the fee income, and the implementation of the EIR model under IFRS 9. Banks have however continued to exploit this space, with some forays being made into bancassurance, transactional income and brokerage. Examples of ventures undertaken in 2018 include:

- I&M Holdings completing a full buyout of Youjays Insurance Brokers for an undisclosed amount on 5thApril 2018,

- KCB Group partnering with Liberty Holdings for the education savings plan dubbed Elimisha in 5th June 2018;

Banks have also been promoting the usage of alternative channels of transactions such as mobile banking, internet banking, and agency banking as they seek to grow transactional income. Notable moves towards the alternative transaction channels segment in 2018 include:

- Housing Finance launching their own mobile banking app dubbed HF Whizz. The app aims to change the way consumers open and access their bank accounts. Users of the app will be able to open an account, access loans, and deposit and transfer cash via their mobile phones,

- Barclays Bank launched its own digital platform, dubbed Timiza, which allows customers to send money to their respective accounts, pay for utilities such as water and electricity, procure micro insurance, and pay for online taxi hailing services. In addition to this, the app grants customers with the access to micro loans of between Kshs 100 and Kshs 150,000 from the platform at interest rates of 1.2% monthly, and a one-off facilitation fee of 5.0%, with the loan repayable after 30-days,

- Equity Group launched its FinTech subsidiary, Finserve, a technological service company, tasked to drive disruptive technology innovation in the financial services segment. Finserve will operate as an autonomous commercial enterprise, delivering technological solutions not just for Equity Group, but also to the entire economy. Finserve houses products like Equitel, Equity Eazzy app, EazzyBiz and EazzyNet. Through Finserve, Equity Group aims to provide an edge in terms of integration with all major global card associations including American Express, Mastercard, Visa, JCB, Dinners, and Union Pay, becoming the single largest aggregator of card payments in the region.

Section II: Performance of the Banking Sector in FY’2018:

The table below highlights the performance of the banking sector, showing the performance using several metrics, and the key take-outs of the performance.

|

Bank |

Core EPS Growth |

Interest Income Growth |

Interest Expense Growth |

Net Interest Income Growth |

Net Interest Margin |

Non-funded income Growth |

NFI to Total Operating Income |

Growth in Total Fee and Commissions |

Deposit Growth |

Growth in Govt Securities |

Cost to Income |

Loan to Deposit ratio |

Loan Growth |

Cost of Funds |

Return on average equity |

|

Stanbic |

45.7% |

13.8% |

19.2% |

14.0% |

5.0% |

18.3% |

45.1% |

15.5% |

13.5% |

3.7% |

59.5% |

79.7% |

22.1% |

3.5% |

14.3% |

|

NBK |

33.5% |

(10.5%) |

(10.9%) |

(22.6%) |

6.5% |

(30.3%) |

24.8% |

(72.5%) |

4.9% |

29.7% |

94.3% |

66.9% |

(3.0%) |

2.8% |

0.1% |

|

KCB |

21.8% |

4.1% |

14.1% |

0.9% |

8.2% |

(0.1%) |

32.0% |

(25.3%) |

7.6% |

9.1% |

52.8% |

84.8% |

7.9% |

3.2% |

21.9% |

|

SCBK |

17.1% |

2.3% |

(3.0%) |

4.5% |

7.5% |

4.9% |

32.2% |

19.7% |

5.1% |

(10.7%) |

58.6% |

52.9% |

(6.1%) |

3.3% |

17.5% |

|

I&M |

17.1% |

6.4% |

17.3% |

0.3% |

6.7% |

32.8% |

32.8% |

59.1% |

25.9% |

0.9% |

53.0% |

78.2% |

9.0% |

4.9% |

17.2% |

|

Co-op |

11.6% |

6.6% |

(0.2%) |

9.5% |

9.5% |

(4.4%) |

29.5% |

(3.0%) |

6.5% |

10.4% |

58.8% |

80.2% |

(3.3%) |

3.8% |

18.3% |

|

Barclays |

7.1% |

7.0% |

31.6% |

0.9% |

8.6% |

14.7% |

30.6% |

6.7% |

11.5% |

58.9% |

66.4% |

85.5% |

5.3% |

3.5% |

16.8% |

|

Equity |

4.8% |

10.0% |

8.9% |

(0.9%) |

8.5% |

(6.3%) |

38.4% |

(16.6%) |

13.3% |

1.9% |

57.7% |

70.3% |

6.5% |

2.7% |

22.5% |

|

DTBK |

2.3% |

1.8% |

2.0% |

1.8% |

6.2% |

3.0% |

21.3% |

5.7% |

6.2% |

2.6% |

56.9% |

68.3% |

(1.5%) |

4.9% |

13.9% |

|

NIC |

2.0% |

4.8% |

14.1% |

(1.8%) |

5.7% |

11.4% |

30.5% |

9.2% |

4.0% |

12.9% |

61.7% |

81.7% |

(1.4%) |

5.2% |

12.1% |

|

HF |

N/A |

(15.2%) |

(9.1%) |

(23.9%) |

4.2% |

(2.0%) |

36.8% |

23.3% |

(5.3%) |

75.0% |

(118.2%) |

89.1%* |

(12.5%) |

7.4% |

(5.5%) |

|

2018 Mkt cap Weighted Average* |

13.8% |

6.5% |

10.6% |

2.6% |

7.9% |

3.8% |

33.2% |

(1.0%) |

10.3% |

9.1% |

57.8% |

75.5% |

4.3% |

3.5% |

19.0% |

|

2017 Mkt cap Weighted Average* |

(1.0%) |

(2.4%) |

2.6% |

(3.8%) |

8.4% |

9.1% |

33.6% |

13.4% |

12.5% |

22.2% |

61.1% |

80.0% |

6.1% |

3.6% |

17.6% |

|

*Market cap weighted as at 30th December 2018/2017 respectively |

|||||||||||||||

Key takeaways from the table above include:

- Listed Kenyan banks recorded a 13.8% average increase in core Earnings Per Share (EPS), compared to a decline of 1.0% in FY’2017, and consequently, the Return on Average Equity (RoAE) increased to 19.0%, from 17.6% in FY’2017. All banks apart from HF Group recorded growths in their core EPS, with Stanbic Holdings recording the highest growth of 45.7%, and the lowest being HF Group, which recording a loss per share of Kshs 1.7,

- The sector recorded weaker deposit growth, which came in at 10.3%, slower than the 12.5% growth recorded in FY’2017. Despite the slower deposit growth, interest expenses increased by 10.6%, indicating banks have been mobilizing expensive deposits. However, with the removal of the limit of interest payable on deposits, the associated interest expenses on deposits is expected to improve in 2019, and possibly improve the cost of funds,

- Average loan growth came in at 4.3%, which was lower than the 6.1% recorded in FY’2017, indicating that there was an even slower credit extension to the economy, due to sustained effects of the interest rate cap and the relatively tougher operating environment that saw banks tighten their credit standards. Government securities on the other hand recorded a growth of 9.1% y/y, which was faster compared to the loans, albeit slower than 22.2% recorded in FY’2017. This highlights banks’ continued preference towards investing in government securities, which offer better risk-adjusted returns. Interest income increased by 6.4%, compared to a decline of 2.4% recorded in FY’2017, as increased allocations to government securities bore fruit. The Net Interest Income (NII) thus grew by 2.5% compared to a decline of 3.8% in FY’2017,

- The average Net Interest Margin in the banking sector currently stands at 7.9%, down from the 8.4% recorded in FY’2017, despite the Net Interest Income increasing by 2.6% y/y. The decline was mainly due to the faster 9.1% increase in allocation to relatively lower yielding government securities, coupled with the decline in yields on loans due to the 100 bps decline in the Central Bank Rate (CBR), and,

- Non Funded Income grew by 3.8% y/y, slower than 9.1% recorded in FY’2017. The growth in NFI was weighed down as total fee and commission declined by 1.0%, compared to the 13.4% growth recorded in FY’2017. The fee and commission income continued to be subdued by the slow loan growth, coupled with the implementation of the Effective Interest Rate (EIR) model under IFRS 9, which requires banks to amortize the fees and commissions on loans, over the tenor of the loan.

Section III: Outlook and Focus Areas of the Banking Sector Going Forward:

In summary, the banking sector had an improved performance, largely aided by the relatively better operating environment compared to 2017, however, the banking sector has been fraught by two main challenges:

- Deteriorating asset quality brought about by the spillover effects of the challenging operating environment experienced in 2017, and the delayed payments by the Government, and

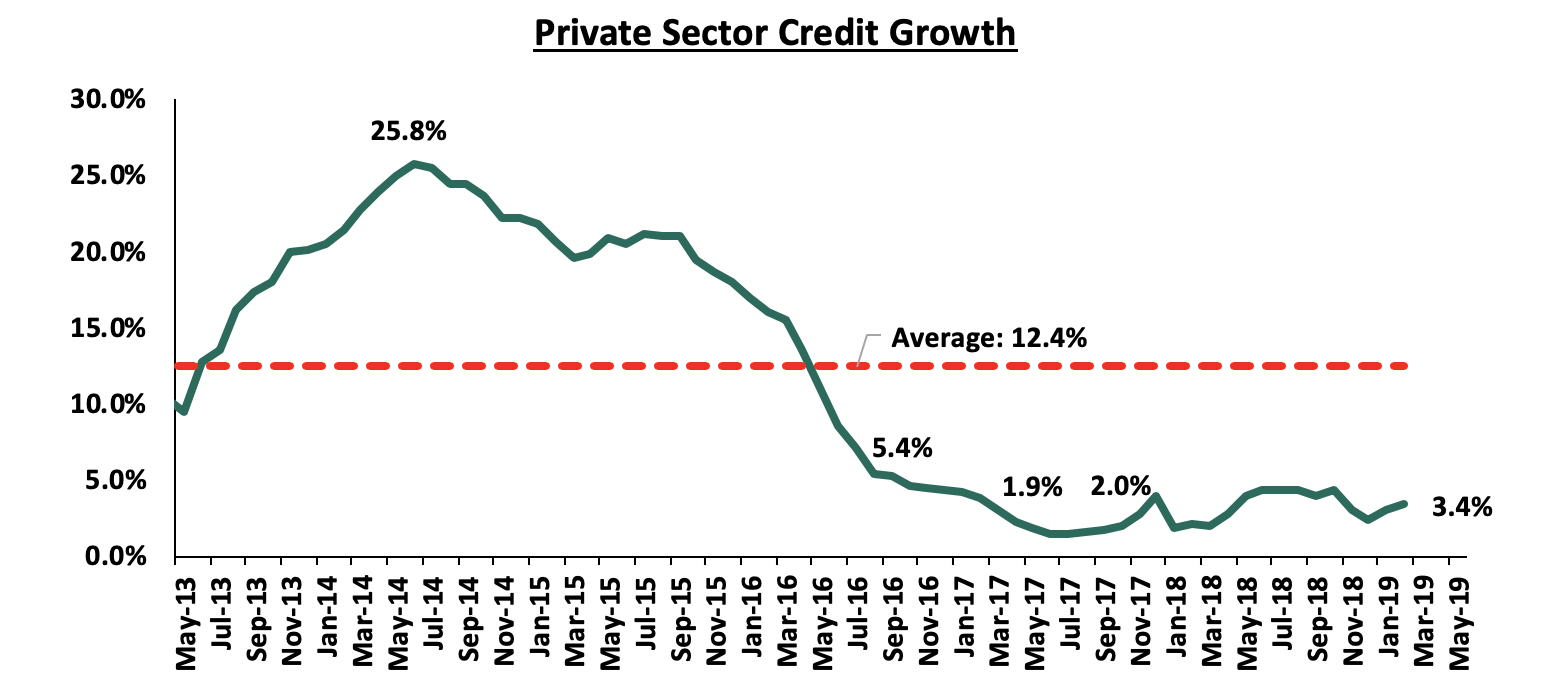

- The capping of interest rates, which has continued to subdue credit extension to the private sector. Instead, banks have been allocating even more of their deposits into government securities. The increased allocation to relatively lower yielding assets has consequently reduced the Net Interest Margin (NIM). Private sector credit growth has remained subdued, coming in at 2.4% in December 2018, and 3.4% as at February 2019, way below the 5-year average of 12.4%.

We maintain our view that the interest rate cap has not achieved its intended objectives of easing the access to credit and reducing the cost of credit. International Institutions such as the International Monetary Fund (IMF) have advocated for a repeal of the law, as it constricts credit extension to the economy, making it even harder for the MSMEs to conduct their business. We continue to be proponents of promoting competing sources of financing, which should reduce the overreliance on bank funding in the economy that is currently between 90.0% to 95.0% of all funding. By having various competing sources of financing, this would trigger a self- regulated pricing structure, in the event of a repeal of the law.

Thus, for 2019, we expect:

- A review of the Banking (Amendment) Act 2015, with the high court having suspended the law terming it as illegal, and a Member of Parliament proposing a revision of the law to include a ceiling of 6.0% above the limit set by the Banking (Amendment) Act, 2015 for the high risk borrowers, and 4.0% above the CBR for low risk borrowers,

- Relatively low credit extension. With the interest rate cap law remaining in place, we expect private sector credit growth to remain below 5.0%, as banks continue to skew their asset allocation to government securities that yield higher risk-adjusted returns,

- We also expect consolidation activity in the banking sector to continue, as the relatively tougher operating conditions make it even harder for the smaller undercapitalized banks to operate, especially those that do not serve a niche, which may see them getting acquired by the larger players who seek to grow their market share and product offerings.

We expect banks to focus on the following business aspects in 2019:

- Asset quality management: Banks will look to manage the deteriorating asset quality, which will lead to further tightening of credit standards as banks cherry pick low risk credit consumers and increase focus on secured, collateral-based lending,

- Revenue diversification: In the current regime of compressed interest margins, focus on Non-Funded Income (NFI) is likely to continue, as banks aim to grow transactional income via alternative channels such as agency banking, internet and mobile technologies,

- Operational efficiency: Cost containment is likely to continue being a focus area. We thus expect continued restructuring, possibly leading to staff layoffs, as banks take advantage of efficient alternative channels of distributions, and,

- Downside regulatory compliance risk management: With increased emphasis on anti-money laundering and fraudulent transactions, we expect banks to be keener on streamlining their operational processes and procedures in line with global standards and regulatory requirements.

For more information, see our Cytonn FY’2018 Banking Sector Review

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma