Sep 9, 2018

In line with Cytonn’s expansion strategy, we continue to carry out market analysis for various regions in Kenya and Sub Saharan Africa in order to identify lucrative investment opportunities for our investors.

- In 2018, we have released the Nyeri Real Estate Investment Opportunity 2017, Kisumu Real Estate Investment Opportunity , and the Nakuru Real Estate Investment Opportunity topicals in January, July and August, respectively,

- In 2017, we released the Kampala Real Estate Investment Opportunity and the Accra Real Estate Investment Opportunity, in September and November 2017, respectively,

- In 2016, we published the Kisumu Real Estate Investment Opportunity 2016.

This week, we turn our focus to the real estate investment opportunity in Mombasa County, which is an update on research conducted in 2016. As per the 2016 analysis, the market had an average rental yield of 7.0% with the residential sector recording average total returns of 7.9% p.a. (an average capital appreciation of 1.6% per annum and rental yield at 6.3%), whereas the office and retail sectors recorded average rental yields of 5.9% and 8.9%, respectively. This week, we update those findings in light of the recent developments within the county where this year, the real estate market recorded average rental yields of 6.2%, with the residential sector recording average total returns to investors of 7.2% (rental yields of 5.1% and capital appreciation of 2.1%), whereas the retail and office sectors attained yields of 8.3% and 5.1%, respectively.

In this topical, we shall look at the following:

- Overview of Mombasa,

- Factors Driving Real Estate in Mombasa,

- Challenges Facing Real Estate in Mombasa,

- Mombasa Real Estate Market Performance,

- Regional Comparative Analysis, and,

- Investment Opportunity and Outlook.

- Overview of Mombasa:

Mombasa, the 2nd largest city in Kenya after the capital city of Nairobi, is situated on the South- Eastern side of Kenya and is the smallest county in Kenya, measuring 229.9 SQKM. It is bordered by Kwale County to the West, Kilifi County to the East, and the Indian Ocean to the South. The county consists of 6 constituencies: Jomvu, Changamwe, Likoni, Nyali, Kisauni, and Mvita, but is broadly divided into Mombasa Island and the Mainland by the Indian Ocean. The county has a relatively high population growth with the County Government of Mombasa estimating the 2017 population to be 1.3 mn persons, an 8-year CAGR of 3.9% from the 0.9 mn recorded in 2009. Thus, the county currently has a relatively high population density of approximately 5,532 persons per SQKM in comparison to the national population density of 83 persons per SQKM. Economically, the county is poised as one of the regional leaders in terms of maritime trade within the continent where Mombasa Port is the largest seaport in East and Central Africa. Moreover, Mombasa is one of the leading tourist destinations in East Africa due to its location adjacent to the Indian Ocean.

- Factors Driving Real Estate in Mombasa:

The real estate sector in Mombasa has been on an upward growth trajectory in terms of supply, attracting both local and international investors in the residential, commercial office, retail and hotel sectors. The key factors that have contributed to the growth include:

- Positive Demographic Dividend: The county has a relatively high population growth with the County Government of Mombasa estimating the 2017 population to be at 1.3 mn persons, an 8-year CAGR of 3.9% from the 0.9 mn recorded in 2009. Thus, the county currently has a relatively high population density of approximately 5,532 persons per SQKM in comparison to the national population density of 83 persons per SQKM. The county also reaps from the prevalent mixture of international cultures that have boosted its middle class population portfolio,

- Housing Deficit: The rapid population growth coupled with a continuous inflow of tourists as well as rural to urban migrators in search of employment has largely contributed to demand for dwellings with the Ministry of Land, Housing, and Physical Planning estimating the housing deficit to be at 380,000 as of 2018. The rapid demographic growth has also boosted the demand for other facilities such as land and retail properties to serve the needs of the residents,

- Infrastructural Improvements: Mombasa has seen several infrastructural projects in the last few years, which has improved the ease of doing business and thus attracted investment. For example, the start of operation of the Standard Gauge Railway in June last year resulted in an increase in local tourism thus, pushing up demand for accommodation services. According to KNBS Economic Survey 2018, bed-occupancy by local tourists increased by 15.6% to 3.6 mn in 2017 from 3.1 mn in 2015. Plans are also underway to upgrade the Moi International Airport’s capacity and efficiency at a cost of Kshs 7.0 bn, alongside the Likoni Channel through construction of the Kshs 82.0 bn Mombasa Gate Bridge Project. Such developments, while also supported by the ongoing Mombasa West Integrated Urban Roads Network Project, which consists of projects such as the Port Reitz Road and the Dongo Kundu Bypass, are bound to open up new areas for investment in Mombasa County, thereby pushing property prices up, as they boost accessibility and reduce traffic snarl-ups, thus setting up the region to attract more investments, including real estate,

- Tourism Sector: Mombasa is recognized as one of the major tourist attraction areas in Kenya, partly due to its rich cultural heritage and also its proximity to the Indian Ocean. The tourist activities have resulted in a vibrant economy boosting the retail sector and the hotel industry, as well as the demand for luxury residential homes especially by long-stay visitors, and,

- Strong Economic Growth: According to a 2015 World Bank study, Mombasa ranked the 9th in Kenya in terms of GDP Per Capita among all counties, recording an average GDP Per Capita of USD 935, 34.7% higher than the national average of USD 694. This is expected to grow further given the rebound in tourism sector and the infrastructural developments that are aimed at enhancing trade in the county’s sea and airports.

Below is a table highlighting the GDP per Capita for the top 10 Kenyan Counties;

|

|

Top 10 Kenyan Counties in GDP Per Capita |

|

|

Rank |

Counties |

GDP Per Capita (USD) |

|

1 |

Kiambu |

1,785 |

|

2 |

Nyeri |

1,503 |

|

3 |

Kajiado |

1,466 |

|

4 |

Nakuru |

1,413 |

|

5 |

Kwale |

1,406 |

|

6 |

Laikipia |

1,226 |

|

7 |

Murang’a |

1,090 |

|

8 |

Nairobi |

1,081 |

|

9 |

Mombasa |

935 |

|

10 |

Machakos |

913 |

Source: World Bank (2015)

3. Challenges Facing Real Estate in Mombasa:

Mombasa County has had its fair share of challenges that have hampered the full maturity of its real estate sector, key among them being:

- Insecurity: The county has been prone to terrorist-related threats, stemming from the 2015 attacks by international terrorist groups such as Al Shabaab, which led to the number of international arrivals declining by a 6-year CAGR of 10.0% to 1.2 mn in 2015 from 1.8mn in 2011. This has resulted in potential investors holding off investment in the county - despite the rebound in the number of arrivals in 2016 and H1’2017, which should be an indicator of return to calm - and this has generally had a negative impact on the business environment. As a result, the performance of the office sector, for example, has been poor with the average occupancy as at August 2018 coming in at an average of 65.8%, compared to counties such as Nairobi with 84.6%,

- Insufficient Infrastructure: Despite the new infrastructural developments, Mombasa County still struggles with inadequate infrastructure, which inhibits the growth of the business environment. For instance, the narrow Nyali Bridge and roads have rendered the city center and its environs unattractive for commercial real estate due to the perennial traffic snarl-ups, whereas the insufficient capacity of the Likoni Ferries affects Mombasa South’s tourism industry due to the long delays caused at the crossing channel. In addition, insufficient access to water services and sewerage systems in majority of the residential estates impedes real estate investments in certain areas such as Likoni and Tudor,

- Inadequate Supply of Affordable Development Land: The county, which is the smallest county in Kenya, lacks sufficient development land to cater for the huge demand, with a population density of 5,532 persons per SQKM, in comparison to the national 83 persons per SQKM. This has resulted in the proliferation of squatter settlements in areas such as Bamburi, Kisauni, Likoni, and Jomvu. According to our research, average land prices in areas such as Nyali, Kizingo, Port Reitz, and Shanzu areas, have grown by a 2-year CAGR of 12.6% to an average of Kshs 115.4 mn as at 2018, from an average of Kshs 109.4 mn in 2016 making it more difficult to provide affordable housing for the low-income population,

- Outdated County Spatial Planning: Mombasa lacks an updated and proper spatial plan to meet the needs of the fast-growing population with the last planning policy having been drawn in 1971, and having expired in in the year 2000. This has resulted in unplanned development, transport challenges, especially within Mombasa town, with constant traffic jams, drainage issues resulting in flooding in areas such as Mzizima and Kaloleni, poor waste management practices and consequently poor living conditions especially for low income households. This has led to decline in development land available at the city centre, improper land use practices and proliferation of informal settlements, rendering such areas unattractive for investment grade commercial developments.

4. Mombasa Real Estate Market Performance:

We conducted research in Mombasa in August 2018 covering the residential, commercial office, retail and land sectors. Below is the sectoral review of performance:

- Residential Sector

The residential sector in Mombasa recorded a marginal decline in average total returns to investors to 7.2% from 7.9% recorded in 2016. This is majorly attributable to a decline in average rental yields which came in at 5.1% in 2018, 0.6% annualized drop since 2016 when the market had an average rental yield of 6.3%. This is attributable to increased vacancies as more developments are delivered to the market which are out of reach for majority of the Mombasa residents, majority of whom are low income earners, that is, below Kshs 50,000 per month (JICA 2016). Notably, capital appreciation recorded a marginal improvement of 0.3% annualized growth to a market average of 2.1% this year, from the 1.6% recorded in 2016. The best performing segment was the upper mid-end sector, which recorded the highest returns to investors of 7.9% on average, that is, average rental yields of 5.6% and a capital appreciation of 2.3%. This is on account of investors in the region purchasing apartments in order to rent them to the growing middle class as well as long-stay international visitors in the county.

The sector’s performance is detailed below:

- Lower Mid-End

The lower mid-end sector mainly comprises of developments in areas such as Tudor, Bamburi, and select parts of Nyali. The segment recorded relatively high occupancy rates with an average of 89.2%, indicating demand from the region’s lower-middle working population. Average total returns came in at 6.7%, with 2-bedroom units offering relatively higher returns of 7.4%, attributable to demand from young families and investors seeking to convert them to short and mid-term stay facilities as they are relatively affordable.

|

(all values in Kenya Shillings unless stated otherwise) |

||||||||||

|

Mombasa Residential Performance Summary August 2018 - Lower Mid-End |

||||||||||

|

Typology |

Size (SQM) |

Price (2018) |

Average Price Per SQM |

Average Rent Per SQM |

Average Occupancy Rate |

Average Annualized Uptake |

Average Rental Yield |

Average Price Appreciation |

Average Total Returns |

|

|

Studio |

42 |

2.4 mn |

57,416 |

355 |

|

8.3% |

6.2% |

0.3% |

6.5% |

|

|

1 BR |

68 |

3.6 mn |

54,312 |

279 |

|

14.6% |

4.9% |

1.4% |

6.3% |

|

|

2 BR |

88 |

7.1 mn |

89,220 |

379 |

89.6% |

26.4% |

4.8% |

2.6% |

7.4% |

|

|

3 BR |

114 |

9.7 mn |

90,348 |

409 |

92.8% |

29.5% |

5.3% |

1.9% |

7.2% |

|

|

Average |

78 |

5.7 mn |

72,824 |

355 |

91.2% |

19.7% |

5.2% |

1.5% |

6.7% |

|

|

· 2-bedroom units recorded the highest average total returns of 7.4%, compared to the market average of 6.7%. This is attributable to a high demand especially from investors seeking rental income · In terms of uptake, 2-bedroom and 3-bedroom units also recorded high average annual uptake with 26.4% and 29.5%, respectively, compared to the entire market’s average of 19.7%. |

||||||||||

Source: Cytonn Research

B. Upper Mid-End

The upper mid-end segment mainly comprises of developments in Nyali, Kizingo, and Shanzu. The upper mid-end segment registered the highest performance with average total returns of 7.9%, in comparison to the overall market’s average of 7.1%, attributable to a relatively high capital appreciation, which came in at 2.3% compared to the overall market’s average of 1.8%. This is attributable to demand for quality housing from the middle class in the region especially in areas such as Nyali and Kizingo; 3-bedroom apartments recorded the highest average annual uptake of 23.8%, indicating demand from investors.

|

(all values in Kenya Shillings unless stated otherwise) |

|||||||||

|

Mombasa Residential Performance Summary August 2018 : Upper Mid-End |

|||||||||

|

Typology |

Size (SQM) |

Price (2018) |

Average Price Per SQM |

Average Rent Per SQM |

Average Occupancy Rates |

Average Annualized Uptake |

Average Rental Yield |

Average Price Appreciation |

Total Returns |

|

1 BR |

74 |

8.1 mn |

111,310 |

658 |

76.8% |

16.0% |

5.4% |

1.3% |

6.7% |

|

2 BR |

92 |

14.3 mn |

136,324 |

679 |

92.9% |

17.8% |

5.0% |

2.3% |

7.1% |

|

3 BR |

177 |

18.8 mn |

116,071 |

598 |

77.5% |

23.8% |

5.2% |

2.6% |

7.8% |

|

4 BR |

261 |

24.3 mn |

95,232 |

547 |

83.3% |

23.3% |

6.3% |

3.5% |

9.8% |

|

Average |

151 |

16.4 mn |

114,734 |

621 |

82.6% |

19.6% |

5.6% |

2.3% |

7.9% |

|

· 4-bedroom units in the upper mid-end sector recorded the highest returns to investors with an average of 9.8%, 1.9% points higher than the market average of 7.9%. This is attributable to demand from middle-income class especially from the prevalent Asian communities who tend to live in larger groups, · 2-bedroom and 4-bedroom units registered the highest average rental yields attributable to their relatively high occupancy rates of 92.9% and 83.3%, respectively, in comparison to the market average of 82.6% · 3-Bedroom units recorded the highest annual uptake of 23.8% on average followed by 4-bedroom units as they offer better returns to investors with average capital appreciation of 2.6% and 3.5%, respectively, compared to 1-bedroom and 2-bedroom units with 1.3% and 2.3%, respectively |

|||||||||

Source: Cytonn Research

C. High-End

The high-end market comprises of developments in Nyali and Kizingo. The segment recorded the lowest returns to investors with average total returns of 4.1%, attributable to low rental yields at 2.7% as a result of relatively low occupancy rates of 62.2%, compared to lower-middle and upper-middle segments, which recorded average occupancies of 89.2% and 82.6%, respectively. This indicates that the high-end units may be out of the affordability range for majority of the Mombasa population with an average absolute price of Kshs 56.1 mn, and thus they only attract the few wealthy individuals. Generally, 4-bedroom units performed better with average total returns of 4.4%, with occupancy rates being highest in Kizingo which recorded an average of 92.9%. This is attributable to demand from wealthy investors seeking spacious beach homes

|

(All Values in Kshs Unless Stated Otherwise) |

||||||||||

|

Mombasa Residential Performance Summary August 2018: High-End |

||||||||||

|

Typology |

Size(SQM) |

Price (2018) |

Average Price Per SQM |

Average Rent Per SQM |

Average Occupancy Rates |

Average Annualized Uptake |

Average Rental Yield |

Average Price Appreciation |

Total Returns |

|

|

3 BR |

345 |

54.7 mn |

188,602 |

645 |

43.9% |

10.8% |

1.8% |

1.7% |

3.5% |

|

|

4 BR (Kizingo) |

273 |

45.7 mn |

173,504 |

757 |

92.9% |

22.8% |

4.9% |

2.4% |

7.3% |

|

|

4 BR (Nyali) |

460 |

70.0 mn |

152,952 |

371 |

50.0% |

6.3% |

1.5% |

0.0% |

1.5% |

|

|

Average |

340 |

55.1 mn |

171,686 |

591 |

62.2% |

13.3% |

2.7% |

1.4% |

4.1% |

|

|

· The high–end market recorded average total returns of 4.1%; with the average rental yields coming in at 2.7% which is relatively low compared to the overall market average of 5.3%, attributable to the high-end market’s high rental rates that dissuade occupancy · 3-bedroom units recorded returns of 3.5% with rental yield and price appreciation of 1.8% and 1.7%, respectively · 4-bedroom units in Kizingo performed better than 4-bedroom units in Nyali with average returns of 7.3% thus drawing investor demand due to their relatively low average absolute price of Kshs 45.7 mn in comparison to Nyali’s average of Kshs 70.0 mn |

||||||||||

Source: Cytonn Research

D. Mombasa Residential Performance Summary

Overall, the residential sector recorded a downward growth in returns with average total returns to investors declining by 0.7% points to an average of 7.2% in 2018 from 7.9% recorded in 2016. In terms of performance, the 4-bedroom typology recorded the highest returns to investors with an average of 8.0% and the highest price appreciation of 2.4%, indicated by the relatively high annual uptake rates of 21.3% in comparison to the market average of 18.3%. This is attributable to the low supply of 4-bedroom units, against high demand especially from upper middle income and high-income individuals. However, 2-bedroom units recorded the biggest gain with capital appreciation improving by 6.5% points to 2.4% in 2018, from a depreciation of 4.1% in 2016.

|

Mombasa Residential Performance Summary August 2018 |

|||||||||

|

Typology |

Average Rental Yields 2018 |

Average Price Appreciation 2018 |

Average Total Returns 2018 |

Average Rental Yield 2016 |

Average Price Appreciation 2016 |

Average Total Returns 2016 |

Annualized Changes Rental Yield (% Points) |

Annualized Changes Price Appreciation (% Points) |

Annualized Changes Total Returns (% Points) |

|

1 BR |

5.1% |

1.3% |

6.4% |

8.0% |

2.3% |

10.3% |

(1.5%) |

(0.5%) |

(2.0%) |

|

2 BR |

4.9% |

2.4% |

7.3% |

6.0% |

(4.1%) |

1.9% |

(0.6%) |

3.3% |

2.7% |

|

3 BR |

4.8% |

2.3% |

7.1% |

6.0% |

3.5% |

9.5% |

(0.6%) |

(0.6%) |

(1.2%) |

|

4 BR |

5.6% |

2.4% |

8.0% |

5.2% |

4.5% |

9.7% |

0.2% |

(1.1%) |

(0.8%) |

|

Average |

5.1% |

2.1% |

7.2% |

6.3% |

1.6% |

7.9% |

(0.6%) |

0.3% |

(0.3%) |

|

· The residential sector’s performance softened between 2016 and 2018, with total returns to investors declining annually by 0.3% points on average, to 7.2% in 2018 from 7.8% in 2016 · Average rental yields declined by 0.6% points, annually over the period with 2018 recording an average of 5.1%, 1.2% points lower than the 6.3% recorded in 2016, · However, capital appreciation gained marginally by 0.3% points on average annually. This was mainly due to the 2-bedroom units which recorded average capital appreciation of 2.4% in 2018, a notable gain of 6.5% points from the depreciation recorded in 2016 of 4.1% |

|||||||||

Source: Cytonn Research

II. Commercial Real Estate

A. Office Sector

The office sector in Mombasa recorded a relatively low performance with average rental yields of 5.1% in 2018, a 0.5% points decline from 5.6% recorded in 2016. This is attributable to a decline in rental rates which came in at Kshs 75.7 per SQFT in 2018, a compounded annual drop of 12.6% from the Kshs 99.0 per SQFT recorded in 2016. This is as demand increased at a slow rate by a 2-year CAGR of 0.6% - an indicator of minimal business expansion in the region, which could be attributed to insufficient infrastructure in key areas such as Mombasa Island, which has made it hard to conduct business in the region. In addition, growth in the financial services sector has been hampered due to (i) lack of legal and regulatory structures, (ii) insufficient skilled professionals in Islamic finance considering that 41.0% of Mombasa’s population is Muslim, and (iii) poor perception and lack of awareness of sharia compliant financial products.

However, the sector has a potential for growth in the future, due to the ongoing developments in the region such as infrastructural improvements, the devolved government’s emphasis on investment in sectors such as manufacturing and the maritime business, and the national economic growth which has a spill-over effect as companies expand to the nation’s largest cities such as Mombasa. This is bound to improve demand for office space.

|

(all values in Kenya Shillings unless stated otherwise) |

|||||

|

Mombasa Office Market Performance Summary August 2018 |

|||||

|

Class |

Current Price/SQFT (Kshs) |

Asking Rent Per SQFT per Month (Kshs) |

Service Charge (Kshs) |

Occupancy Rate |

Rental Yield 2018 |

|

Grade B |

15,000.0 |

79.6 |

20.0 |

71.7% |

5.9% |

|

Grade C |

|

61.3 |

19.0 |

59.1% |

3.2% |

|

MUD |

11,750.0 |

108.5 |

14.7 |

64.4% |

7.4% |

|

Average |

12,833.3 |

75.7 |

18.6 |

65.8% |

5.1% |

|

· Mixed-use developments recorded better returns with average rental yields of 7.4% compared to the market average of 5.1%, attributable to their relatively high rental rates with an average of Kshs 108 per SQFT compared to the market average of Kshs 75.7 per SQFT, as they are mostly located in exclusive high end or upper mid-end residential areas thus target high-end clientele, · Grade C offices recorded the lowest returns with average rental yields of 3.2% attributable to a low demand for such due to their tendency to lack sufficient amenities, especially parking spaces as majority of them are located within the CBD thus limiting land for parking and quality space, · Grade B offices are mostly in good locations, along major routes such as Links road, and are few in supply hence record relatively high in occupancy rates with an average of 71.7%, 5.9% points higher than the market average of 65.8%. |

|||||

Source: Cytonn Research

The average selling price for office space remained flat at Kshs 12,833 per SQFT mainly driven by the notably low uptake of 20.0% on average, as well as sluggish occupancy rates, which increased by a 2-year CAGR of 0.9% between 2016 and 2018.

(all values in Kenya Shillings unless stated otherwise)

|

Mombasa Office Sector Performance Summary 2016/2018 |

|||

|

Factor |

2018 |

2016 |

Annualized Change |

|

Average Price per SQFT (Kshs) |

12,833.3 |

12,833.3 |

0.0 Points |

|

Average Rent Per Month per SQFT (Kshs) |

75.7 |

99.0 |

(12.6%) |

|

Average Occupancy Rate |

65.8% |

64.0% |

0.9% Points |

|

Average Uptake |

20.0% |

18.0% |

1.0% Points |

|

Average Rental Yields |

5.1% |

5.9% |

(0.4%) Points |

|

· Average selling price for office space remained flat with to a slow marginal increase rate in office space uptake by 2.0% points in the last 2 years · Asking rents however declined deeply by an annualized rate of 12.6%. This is as developers sought to raise occupancy rates within the poorly performing market and also Grade C developments that are charging relatively lower rents of Kshs 61.3 per SQFT, on average |

|||

Source: Cytonn Research

B. Retail Sector

The retail sector in Mombasa recorded an improvement in performance from 2016 to 2018, in terms of occupancy rates, which increased by 7.2% points on average, annually from 82.0% to 96.3%. The demand has been spurred by a positive demographic dividend, a growing middle class, the rebound in the tourism sector, and local retailers such as Tuskys and Naivas that are keen on expanding their national footprint. Nakumatt, which was predominantly the main retailer in a majority of the malls in Mombasa has paved the way for entry of other local retail giants such as Naivas as well as international retailers such as Shoprite, through its exit from the market. Moreover, several international retailers have announced plans to expand to Mombasa including LC Waikiki, Domino’s Pizza, Coldstone, and Shoprite. Mombasa has the second largest mall space supply in Kenya with 1.4mn SQFT, after Nairobi, which has 6.5 mn SQFT. New malls in the region include the Mwembe Mall in Mwembe Tayari measuring 135,600 SQFT, which was complete in 2018, and Airport Mall in Changamwe measuring 172,000 SQFT, which is under construction and expected to be operational within 2018.

|

(all values in Kenya Shillings unless stated otherwise) |

||||

|

Mombasa Retail Sector Performance Summary August 2018 |

||||

|

Class |

Average Rent Per SQFT per Month (Kshs) |

Service Charge (Kshs) |

Occupancy Rate |

Rental Yield 2018 |

|

Community |

143.3 |

16.0 |

87.5% |

9.4% |

|

Neighborhood |

93.8 |

21.0 |

97.9% |

7.5% |

|

Average |

103.7 |

18.5 |

96.3% |

8.3% |

|

· Neighborhood malls recorded high occupancy rates of 97.9% on average, compared to the market average of 96.3%. This is attributable to their affordability with the average rents per SQFT for neighborhood malls coming at Kshs 93.8, compared to community malls’ Kshs 143.3 per SQFT while the amenities are similar. They include malls like Nyali Plaza, and City Mall · Community malls, however, recorded higher returns with average rental yields of 9.4%, 1.1% points higher than the market average of 8.3%, owing to their high rental rates which came in at an average of Kshs 143.3 per SQFT. They include malls like Nyali Centre, and the recently opened Mwembe Mall |

||||

Source: Cytonn Research

In comparison with 2016, the average asking rents for the retail sector declined by 5.5% annually between 2016 and 2018, as investors sought to attract clientele especially with the exit of various banks from the malls, and Nakumatt, which was an anchor tenant in key malls such as City Mall, Nyali Plaza and Likoni Complex. Occupancy rates increased by a cumulative of 14.3% between the 2-years from 82.0% as at 2016 to 96.3% in 2018, driven by affordable rental rates, as well as the continued expansion of local retailers such Naivas.

(all values in Kenya Shillings unless stated otherwise)

|

Mombasa 2016/2018 Retail Sector Performance Summary |

|||

|

Factor |

2018 |

2016 |

Annualized Change |

|

Average Rent Per SQFT (Kshs) |

103.7 |

116.0 |

(5.5%) |

|

Average Occupancy Rate |

96.3% |

82.0% |

7.2% points |

|

Average Rental Yields |

8.3% |

8.9% |

(0.3%) |

|

· Average asking rents for the retail sector declined by 5.5% annually between November 2016 and August 2018, as investors sought to attract clients and as various malls experienced vacancy rates with the closure of Nakumatt, as well as bank branches · As a result, average occupancy rates increased by a cumulative of 14.3% between the two years indicating a return of investor confidence. In addition, the region has attracted interest from both international retailers such as LC Waikiki and Shoprite supermarket, and local retailers seeking to expand their nationwide footprint such as Naivas and Tuskys |

|||

Source: Cytonn Research

III. Land Performance

The average price per acre in Mombasa is Kshs 115.4 mn, an average price appreciation of 12.6% from Kshs 109.4 mn per acre in 2016. Fast developing areas such as Kizingo and Nyali, recorded the highest price per acre at Kshs 244.6 mn and Kshs 134.0 mn, respectively. Areas such as Likoni Harbor and Port Reitz also exhibit high demand for land hence high prices. Ongoing infrastructural improvements such as the Mombasa West Integrated Urban Roads Network Project, the planned Mombasa Gate Bridge, and the recently launched SGR, have also contributed in boosting land prices as they open up areas for investment. Additionally, the ability to densify in areas such as Kizingo, Tudor and Nyali has led to high land prices as developers are able to maximize their investment.

(all values in Kenya Shillings unless stated otherwise)

|

Average Land Performance for Select Areas in Mombasa2016/2018 |

||||

|

Location |

Price Per SQM |

Average Price Per Acre 2016 (Kshs) |

Average Price per Acre 2018 (Kshs) |

Annualized Capital Appreciation |

|

Shanzu |

13,583 |

60.0mn |

61.3mn |

0.9% |

|

Nyali |

33,500 |

77.5mn |

134.0mn |

24.5% |

|

Bamburi |

11,475 |

|

45.9 mn |

|

|

Kizingo |

70,774 |

200.0mn |

244.6mn |

8.9% |

|

Port Reitz |

36,591 |

100.0mn |

146.4mn |

16.5% |

|

Average |

31,012 |

109.4mn |

115.4mn |

12.6% |

Source: Cytonn Research

IV. Mombasa Real Estate Performance Summary

In summary, the real estate sector in Mombasa registered average rental yields and price appreciation of 6.2% and 7.2%, respectively, with the retail sector recording the highest rental yields of 8.3% compared to other themes such residential and office, which attained yields of 5.3% and 5.1%, respectively.

|

August 2018 Mombasa Real Estate Performance |

|||

|

Sector |

Average Occupancy Rates 2018 |

Average Rental Yields 2018 |

Capital Appreciation |

|

Residential |

82.0% |

5.1% |

1.8% |

|

Office |

65.8% |

5.1% |

|

|

Retail |

96.3% |

8.3% |

|

|

Land |

|

|

12.6% |

|

Average |

81.4% |

6.2% |

7.2% |

Source: Cytonn Research

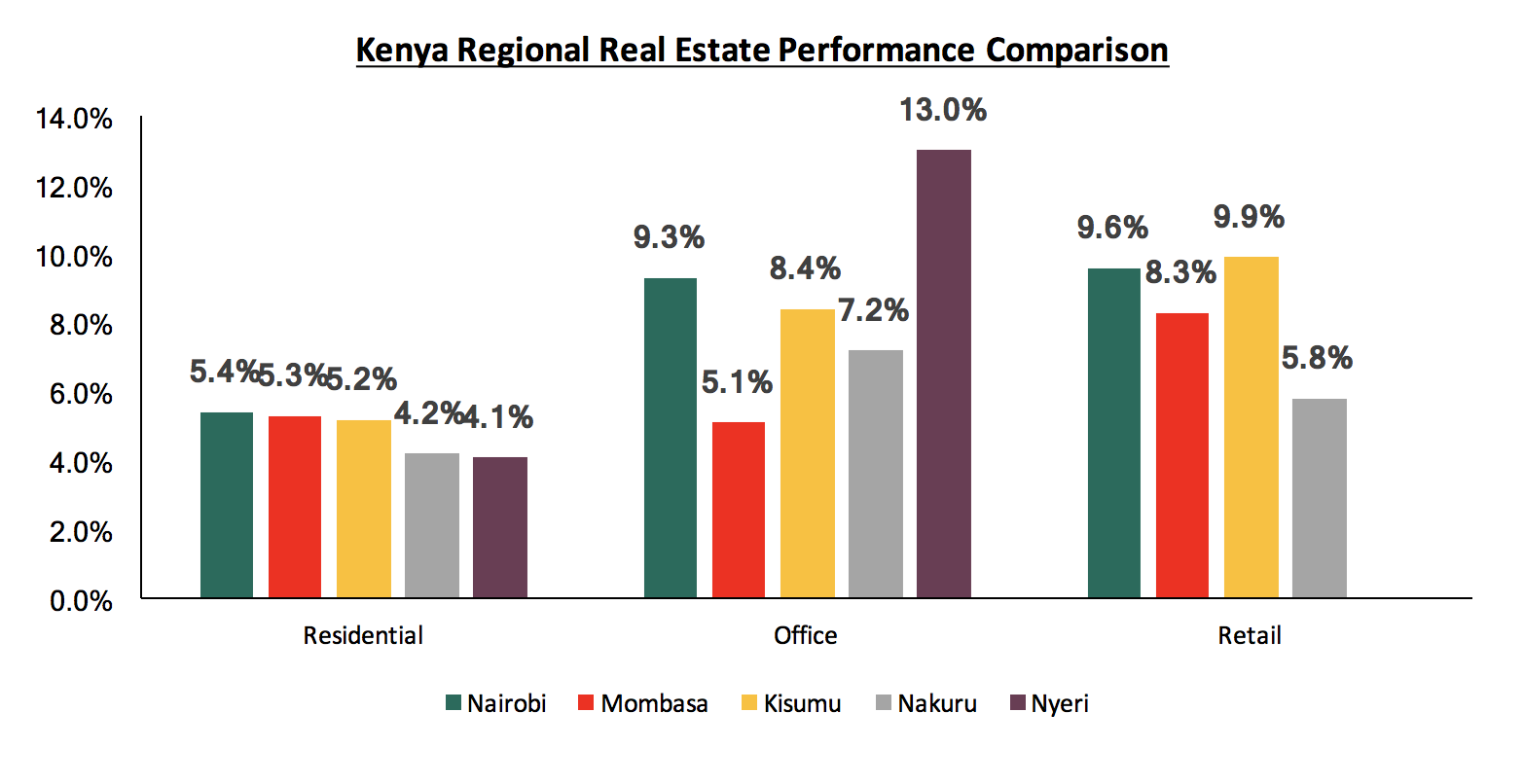

5. Regional Comparative Analysis

Comparing across the 5 counties we have tracked thus far;

- In the residential sector, Mombasa recorded average rental yields of 5.1%, higher than Nakuru’s 4.2%, Nyeri’s 4.1%, and Nairobi’s 5.4% and lower than Kisumu which recorded 5.2%

- In the office sector, Mombasa recorded the least yields of 5.1%, compared to Nakuru, Kisumu, Nyeri and Nairobi with 7.2%, 8.4%, 13.0% and 9.3%, respectively

- In the retail sector, Mombasa recorded average rental yields of 8.3%, which is higher than Nakuru’s 5.8%, albeit lower than Nairobi’s 9.6%, and Kisumu with 9.9%

Below is a graph showing the summary;

*Nyeri’s Performance is as of August 2017

Source: Cytonn Research

6. Investment Opportunity & Outlook

In conclusion, we have analyzed and identified the investment opportunity in Mombasa County based on our research then given our outlook classified as Neutral, Negative or Positive as shown below;

|

Mombasa Investment Opportunity Summary & Outlook |

||||

|

Theme |

Performance (2016) |

Performance (2018) |

Investment Opportunity |

Outlook |

|

Residential |

Average rental yields came in at 6.3%, with average capital appreciation 1.6%, thus average total returns of 7.9% |

Apartments in Mombasa attained returns of 7.2%, with average rental yields and price appreciation of 5.1% and 2.1%, respectively |

The highest returns to investors are in the upper mid-end segment especially within upcoming areas such as Kizingo and Tudor. However, investors should carry out thorough research to determine demand as some areas could be saturated

|

|

|

Commercial Office |

2016 recorded average occupancy rates of 64.0% with rental yields of 5.9% |

The occupancy rates came in at 65.8% on average, with rental yields of 5.1% |

The office sector is set to continue on a decline due to reluctance of investors to relocate business to the region, and the local population’s limited ability to occupy investment grade office developments |

|

|

Retail |

The market recorded average occupancy rates of 82.0%, with average rental yields of 8.9% |

The occupancy rates came in at 96.3% on average, with rental yields of 8.3% |

Malls in Mombasa are more concentrated in one area, i.e. Nyali and its close environs. Thus, the opportunity is in select residential areas that are have no mall space

|

|

|

Land |

Average price per acre for development land was Kshs 109.4 mn |

Average price per acre for development land is Kshs 115.4 mn, with a 2-year CAGR of 12.6%, driven by the ongoing infrastructural developments |

Site and service schemes in areas earmarked for infrastructural developments especially the Mombasa West Integrated Urban Roads Network Project

|

|

Source: Cytonn Research

Out of the four themes that we have looked at, two have a neutral outlook, i.e. residential and retail sectors, the office sector has a negative outlook, while the land sector has a positive outlook. Thus, our outlook for the region is neutral. For investors, the opportunity is in (a) retail sector in undersupplied areas such as Tudor on account of (i) increasing middle class, (ii) lack of supply to serve the upcoming middle-class residential estates such as Tudor and Kizingo, and (b) site service schemes in areas experiencing the ongoing infrastructural developments such as the Mombasa West Integrated Urban Roads Network.

For the full report, please see (link)

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma