Feb 12, 2023

The Kenya Mortgage Refinance Company (KMRC) is as a non-deposit taking, public-private partnership (PPP) firm formed by the Government of Kenya and regulated by the Central Bank of Kenya (CBK). The primary mandate of KMRC is to ensure sustainable home financing in the country, by providing long-term funds to primary mortgage lenders (PMLs) such as; banks, microfinance institutions, and SACCOs at low and fixed interest rates. KMRC was incorporated in April 2018 under the Companies Act 2015, and authorized by the CBK to begin lending operations in September 2020. During 2021, the company received 12 applications and disbursed funds worth Kshs 1.3 bn to 7 PMLs. KMRC currently has 23 shareholders which include; the Kenyan government through the National Treasury (25.3%), 8 commercial banks and one microfinance bank (44.3%), 11 SACCOs (7.5%), with the remainder, 22.9%, being owned by 2 development finance institutions; Shelter Afrique and the International Finance Corporation.

As a wholesale financial institution, KMRC does not take deposits nor lend directly to individuals. This enables KMRC to focus on increasing liquidity to PMLs and developing standardized lending practices through working with the government and other stakeholders. This is geared to enable the mortgage lending institutions to continue lending to home buyers without worrying about a lack of long-term funding, by gaining ability to cover any unexpected short-term deposit outflows. In addition to providing long-term funding, KMRC also plays a key role in promoting the development of the economy in Kenya by expanding the capital markets through the issuance of corporate bonds for long-term financing. The Capital Markets Authority of Kenya (CMA) supervises KMRC's bond issuance activities. We have previously covered five topicals on KMRC namely;

- Kenya Mortgage Refinance Company (KMRC) Progress, in May 2022 where we analyzed the performance of KMRC since the company commenced its lending operations,

- Kenya Mortgage Refinance Company Update in August 2021, where we benchmarked with the Jordan Mortgage Refinance Company,

- Kenya Mortgage Refinance Company Recap in November 2020, where we drew lessons from Saudi Real Estate Refinance Company,

- Kenya Mortgage Refinance Company Update in April 2019, where we reintroduced what mortgage refinance companies are, why they are needed, how they operate, what benefits they give, and,

- Kenya Mortgage Refinance Company in April 2018, where we introduced KMRC as a mortgage liquidity facility and demystified the conditions necessary for the KMRC to thrive.

This week, we update on the progress of KMRC by highlighting the key developments, challenges and milestones the company has achieved towards the goal of sustainable home financing in the country. In addition, we shall provide our expectations for KMRC and give recommendations regarding how to boost mortgage financing in Kenya by looking towards similar companies in other countries. This we shall cover through the following;

- Overview of the Housing Sector in Kenya,

- Home Financing in Kenya,

- Kenya Mortgage Refinance Company (KMRC) Update,

- Case Studies and Lessons Learnt, and,

- Conclusion.

Section I: Overview of the Housing Sector in Kenya

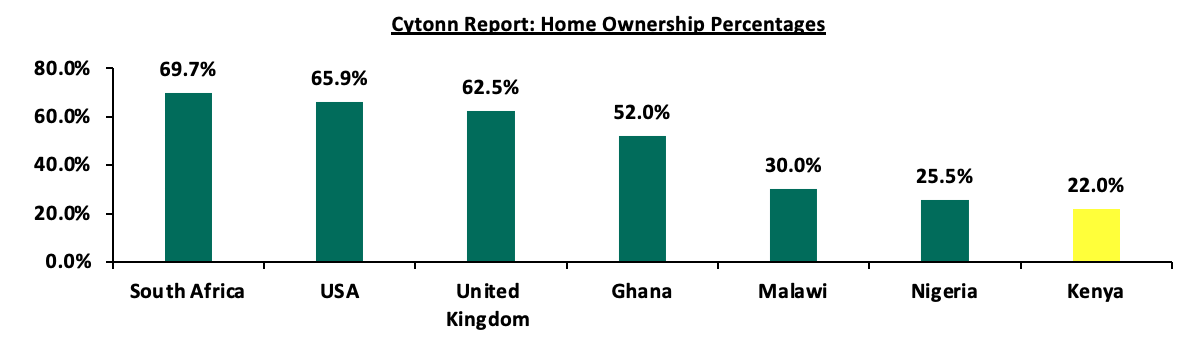

The housing situation in Kenya is characterized by a high demand for dwellings, driven by the relatively high urbanization and population growth rates averaging 3.7% and 1.9%, compared to the global averages of 1.6% and 0.9%, respectively, according to the World Bank as of 2021. The Centre for Affordable Housing Finance Africa (CAHF) estimates that Kenya has an 80.0% annual housing deficit, as only about 50,000 new houses are delivered each year against a demand for 250,000 units per year hence the demand outstripping supply at an average of 200,000 houses every year. The prevailing tough economic environment in the country has continually led to gradual increase in the costs of construction and building materials such as cement and steel on the back of elevated inflation, which in turn necessitates higher financing costs for developers, that they pass on to the market. This has led to a high cost of housing, with many people being unable to afford to buy or rent homes in the country. As a consequence, the percentage of Kenyans who own homes is relatively low, coming in at 22.0% in urban areas, with the majority of the population, 78.0%, being property renters. This is in contrast to other Sub-Saharan African countries such as South Africa and Ghana with home-ownership rates of 69.7% and 52.0%, respectively, as shown below;

Source: Centre for Affordable Housing Africa, US Census Bureau, UK Office for National Statistics

In response to this challenge, the Government of Kenya launched the Affordable Housing Programme (AHP), with two key components of delivery housing units, the supply side, and enabling purchasing of housing units, the demand side.

On the supply side, the government has set a goal of delivering 200,000 affordable housing units on an annual basis. To supply the required units, the government has been on a robust drive to launch affordable housing projects, with the AHP pipeline currently boasting about 30 projects being undertaken by both the government and private developers. This is through various incentives such as; i) exemption of VAT on importation and local purchase of goods for the construction of houses under the AHP, ii) lower corporate tax rate at 15.0% for AHP developers of over 100 units, iii) exemption from 4.0% (urban areas) and 2.0% (rural areas) stamp duty for first time buyers of houses under the AHP, iv) tax relief of 15.0% of savings to drive contributions towards home ownership, v) exemption from restrictions in interest expense deduction for foreign controlled companies undertaking AHP projects, and, vi) availing State land to County governments for the construction of affordable housing units.

On the supply side of the AHP is to increase access to mortgage financing for low and middle-income households in Kenya. To achieve this, the government aims to restructure the housing finance scheme in the country, by instituting a National Housing Fund and Cooperative Social Housing Scheme, which will guarantee uptake of houses that are developed under the AHP. This is envisioned to increase the number of mortgage accounts from the current 26,723 to a target of 1,000,000 by enabling affordable mortgages at monthly repayments of Kshs 10,000 and below. This is from the current average repayment amounts of Kshs 96,847 per month, given an average mortgage size of Kshs 9.2 mn repaid at an annual interest rate of 11.3% over 20 years. As such, the KMRC plays a vital role in supporting the ongoing AHP, through its objectives which include;

- Providing sustainable, long-term funding at attractive rates to participating financing institutions which will enable them to scale up their mortgage lending operations,

- Boosting the growth of the capital markets in the country through the issuance of corporate bonds as a source of sustainable long-term funding,

- Standardization of mortgage practices in Kenya which is geared to enable efficiency of lending processes by working together with the government and stakeholders,

- Facilitating the entry of new mortgage lenders in the market in a bid to increase competition among PMLs in order to lead to a wider range of high-quality mortgage products,

- Ensuring lower overall transaction costs to PMLs through pooling issuance, as compared to accessing the markets individually, that will in turn enable them to offer lower rates to homebuyers, and,

- Facilitating participating institutions to extend the mortgage maturity durations in line with the goal of achieving long-term housing finance.

Section II: Home Financing in Kenya

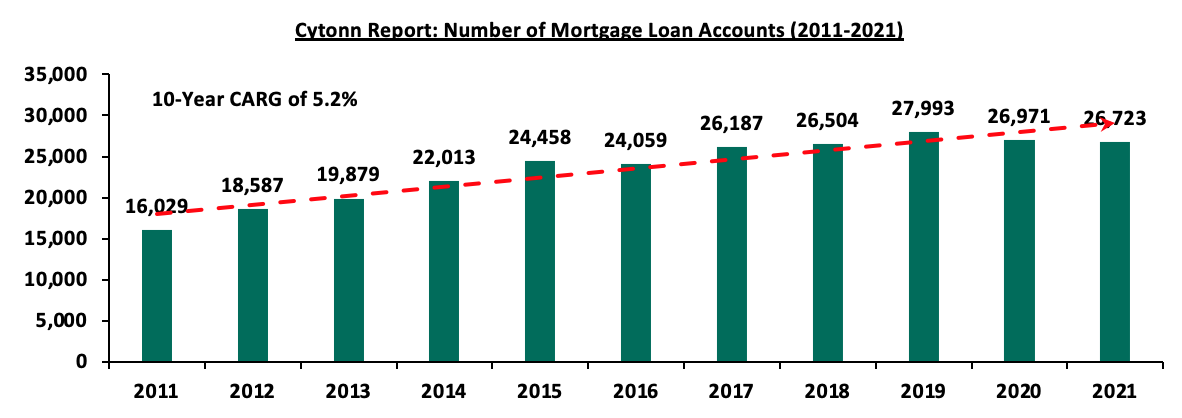

The housing finance industry plays a crucial role in Kenya's Real Estate sector. Despite its potential for growth, the mortgage sector, in particular, has not fully developed, as evidenced by recent declines in the number of mortgage accounts. In 2021, the number of mortgage accounts declined by 0.9% to 26,723 from 26,971 in 2020 which also represented a 3.7% decline from 27,993 accounts in 2019. The few number of mortgage accounts, even with the entrance of KMRC in the sector in 2021, still represents a relatively smaller portion of the overall financial landscape, contributing only 1.9% to the country's GDP as at 2021.

However, the average number of loan accounts has recorded a 10-year Compounded Annual Growth Rate (CARG) of 5.2%, showcased by a growing demand for homeownership among Kenyans, driven by steady economic growth and a subsequent increase in disposable income to invest in property especially during the pre-COVID-19 period. The recent decline in the number of mortgage accounts suggests that there are still challenges to overcome to sustain this growth in the future. Despite these challenges, there is significant room for growth in the Kenyan housing finance industry, as more Kenyans look for ways to invest in the real estate sector such as personal savings, sale of other assets, SACCO loans, inheritance/gift, investment groups, and a blend of several financing. The graph below shows the average mortgage loan accounts from 2011 to 2021;

Source: Central Bank of Kenya

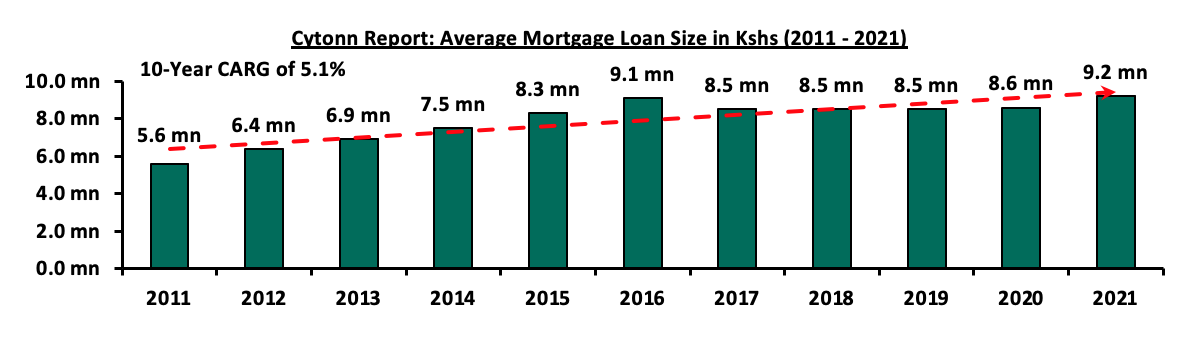

In line with the growth of mortgage loan accounts, the trend of average mortgage loan size has also been upward in the recent past, realizing a 10-year CAGR of 5.1% to Kshs 9.2 mn from Kshs 5.6 mn as shown in the graph below;

Source: Central Bank of Kenya

This growth can be attributed to the joint efforts of the government and private financial institutions in enhancing financial accessibility and providing more reasonable and flexible mortgage options which accommodate the general public.

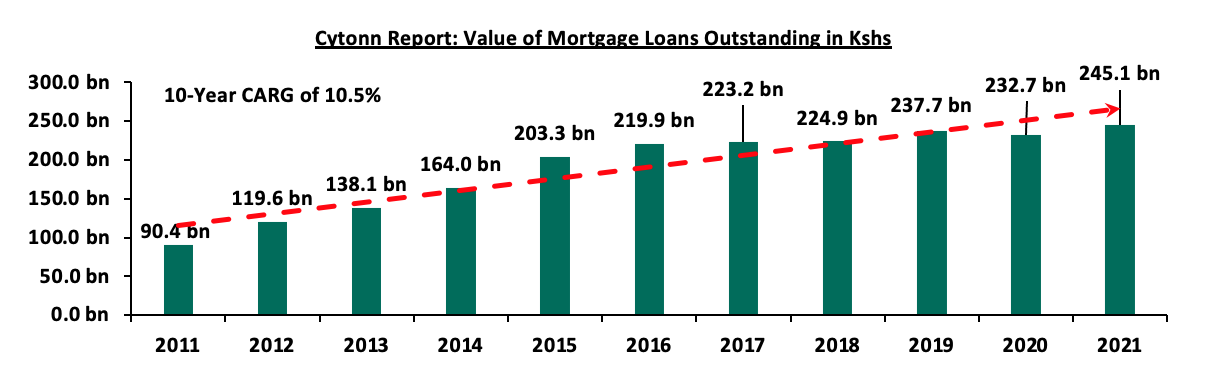

According to Bank Supervision Annual Report 2021, the value of mortgage loans outstanding increased by Kshs 12.4 bn, representing 5.3% increase to Kshs 245.1 bn in 2021 from Kshs 232.7 bn in 2020. The upward trajectory of the loans which also represented a positive 10-year CARG of 10.5% was attributed to increase in the value of mortgages granted by banks, with the average loan size significantly adjusted to Kshs 9.2 mn from Kshs 8.6 mn in 2020 and Kshs 8.5 mn in 2019. This was at the back of recovery of the economy from a depressed 2020, where the mortgage sector was negatively affected by the COVID-19 pandemic. The graph below illustrates the trend of value of mortgage loans outstanding from 2011 to 2021;

Source: Central Bank of Kenya (CBK)

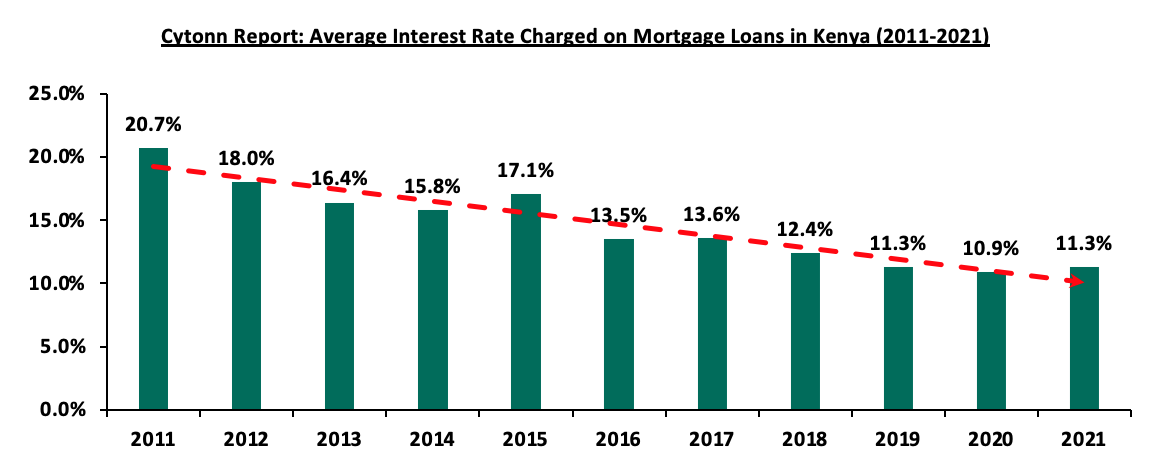

Additionally, the industry recorded an average interest rate charged on mortgages of 11.3% which was 0.4% points increase from 10.9% recorded in 2020. The interest rates majorly ranged from 7.1% to 15.0% in 2021 compared to a range from 7.0% to 15.0% charged in 2020. The increase in the interest rates was attributed to the consistency of increasing interest rates in the economy during 2021. However, for the past decade, the interest rate charged on mortgage loans has been on a downward trajectory mainly attributed by the introduction of the interest rate cap imposed by the Central Bank of Kenya (CBK) in September 2016 and later removed in November 2019. This resulted to significant drop in interest rates offered by banks during the period as shown in the graph below;

Source: Central Bank of Kenya (CBK)

Nevertheless, this rate is still considered unaffordable for most low-income and low-middle income earners. Assuming a low-middle income earner applies for a mortgage size of Kshs 9.2 mn, at an interest rate of 11.3%, and a maximum repayment term of 20 years, the client would need to pay approximately Kshs 96,847 per month, given that the average median household income in Kenya is Kshs 50,000 per month. Additionally, we expect that the continued adoption of risk based pricing models by commercial banks will drive interest rates further upwards, given that banks will be able to adequately price their risks.

The maximum loan that an average median household income of Kshs. 50,000 can afford, assuming 30% of the income, Kshs. 15,000, goes into mortgage payment is 2.5 mn (assuming interest rate of 11.3%, 20 years payment, and 15,000 per month payment.)

On the other hand, the maximum loan as a percentage of property value, also known as Loan to Value Ratio stabilized at 90.0% since 2014, whereas the average maturity of the loans was 12 years. Loan maturity ranged from 5 years as the minimum and 25 years as the maximum number of years. This was a one-year increase of 11 years recorded in 2020 ranging from a minimum of 4 years to a maximum of 20 years.

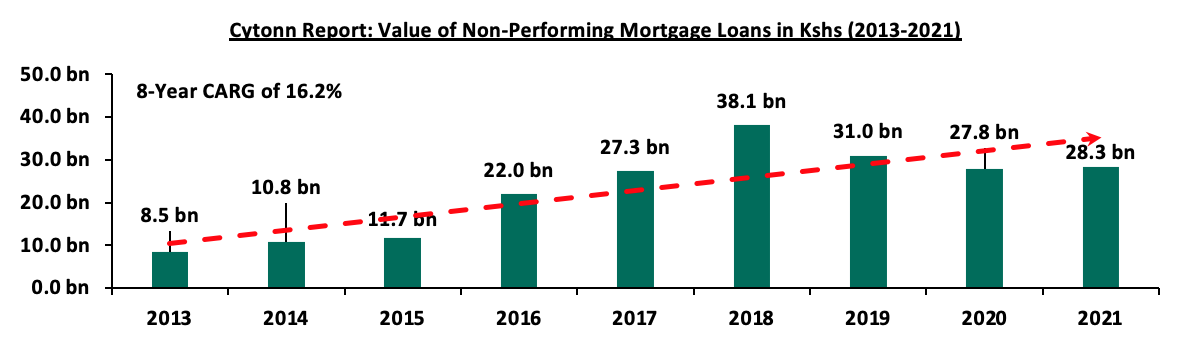

The outstanding value of Non-Performing Mortgage Loans increased by 1.8% to Kshs 28.3 bn in 2021 from Kshs 27.8 bn in 2020. This was attributed to ripple effect of COVID-19 pandemic which caused widespread economic disruption in 2020, leading to widespread job loss and reduction in income for many individuals. As a result, a significant number of housing investors found it difficult to service their mortgage loans. The pandemic also disrupted housing market activity, leading to a slowdown in Real Estate sales and making it more difficult for investors to sell their homes and refinance their mortgages during the period. However, the Non-Performing Mortgage Loans to Gross Mortgage Loans ratio was at 11.6%, 2.5% points lower compared to industry gross non-performing loans to gross loans ratio of 14.1%. The graph below shows the performance of non-performing mortgage loans from 2013 to 2021;

Source: Central Bank of Kenya (CBK)

On the other hand, the value of Non-Performing Mortgage Loans recorded an 8-year CARG of 16.2% between 2013 and 2021, which was majorly attributed by a significant increase of 88.0% in the value of Non-Performing Mortgage Loans to Kshs 22.0 bn in 2016 from Kshs 11.7 bn in 2015. Additionally, the political instability caused by the August 2017 general elections and the repeat elections in October 2017 likely had a negative impact on the housing market in Kenya, contributing to the 39.7% increase in the value Non-Performing Mortgage Loans between 2017 and 2018. This instability majorly caused a slowdown in Real Estate sales and made it more difficult for individuals finance their mortgages, leading to an increase in non-performing loans.

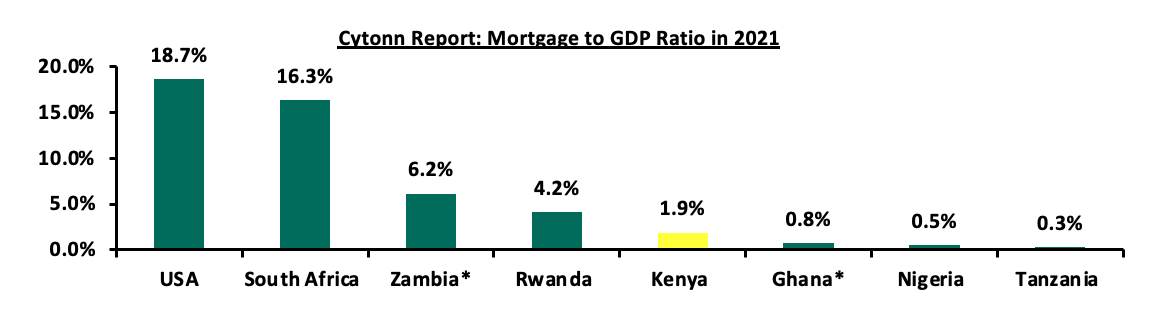

Subsequently, Kenya’s mortgage to GDP continues to underperform at approximately 1.9%, compared to countries such as South Africa and Rwanda which are at approximately 16.3% and 4.2% as at 2021, respectively, as shown below;

*(2020)

Source: Centre for Affordable Housing Africa

Currently, Kenya has 26,723 mortgage loan accounts with an average size of Kshs 9.2 mn bringing the total value of mortgages to Kshs 245.1 bn, which translates to a 1.9% mortgage-to-GDP ratio. To match South Africa's 16.3% mortgage to GDP ratio, the Kenyan mortgage market needs a Kshs 2,121.9 bn expansion. This means we require an additional 230,646 mortgages given the same average mortgage size to achieve that target.

However, several challenges have contributed to the underperformance of the Kenyan mortgage market such as;

- Ripple negative impact of COVID-19 in 2021 which continued to cause economic downturns and uncertainty regarding investing in Real Estate hence most borrowers struggled to repay the loans or take more mortgages,

- Low level of income among most consumers which reduces their ability to qualify for and make mortgage repayments, increasing the risk of default, and consequently putting pressure on banks to manage their risks and comply with the sustained new financial regulations,

- High cost of property purchase making it difficult for the consumers to afford high monthly repayments hence slowing down the mortgage process. On the other hand, the value of collateral used to secure the mortgage loans has also been on the rise, making it more difficult for banks to recover their losses in an event of default,

- Limited access to affordable long-term finance as most consumers struggle to access credit from banks and financial institutions due to strict lending criteria imposed especially during the COVID-19 period,

- Weak property rights regarding disputes over the ownership of a property undermine most consumers to secure mortgages and making it difficult for a bank to recover its funds in case of defaults,

- KMRC, which officially began its lending in 2021, is yet to stamp its dominance in the market and increase its attractiveness to more stakeholders in the sector, and

- Political and economic instabilities such as general elections and elevated inflationary pressures has made banks become more cautious about granting mortgages, as they are concerned about the risk of default and the potential loss of their funds, hence discouraging investments and limiting the growth of the mortgage market.

Section IV: Kenya Mortgage Refinance Company (KMRC) Progress Update

- Overview of the Kenya Mortgage Refinance Company

The Kenya Mortgage Refinance Company (KMRC) is a treasury backed non-deposit taking financial institution established in 2018 under the Companies Act 2015, and was licensed by the Central Bank of Kenya (CBK) to commence core business operations in September 2020. KMRC is the sole institution licensed to carry out Mortgage Liquidity Facility (MLF) activities in Kenya, which include provision of long-term funds to Primary Mortgage Lenders (PMLs) such as banks, microfinance institutions and SACCOS for purposes of increasing availability of affordable home loans to Kenyans. Typical of all MLFs, the KMRC acts as an intermediary between PMLs and the capital markets through issuance of bonds subject to regulation and supervision of the CBK and Capital Markets Authority (CMA), with the objective of providing long term funds at better rates. As such, KMRC does not lend directly to individual borrowers. The issuer was established as a crucial component in the implementation of the Affordable Housing Plan aimed at increasing the low rates of home ownership, particularly in urban areas coming in at 22.0%, resulting from limited and inaccessible housing financing as well as high housing costs. In support of this, KMRC was purposely established through a public private partnership arrangement between the Government of Kenya, and World Bank with majority ownership being by the private sector at 75.0%. Currently, KMRC has 23 shareholders which include;

|

Cytonn Report: KMRC Shareholders |

|||

|

# |

Umbrella Body |

Individual Shareholders |

Estimated Stake (%) |

|

1 |

The Government of Kenya |

The National Treasury and Economic Planning |

25.3% |

|

2 |

Development Finance Institutions |

International Finance Corporation (IFC), Shelter Afrique |

22.9% |

|

3 |

Commercial Banks |

KCB Bank, Co-operative Bank, Stanbic Bank, NCBA, Credit Bank, DTB, Absa Bank Kenya, HFC Limited |

44.3% |

|

4 |

Microfinance Bank |

Kenya Women Microfinance Bank (KWFT) |

|

|

5 |

Savings and Credit Cooperatives (SACCOs) |

Stima, Imarisha, Ukulima, Tower, Mwalimu, Unaitas, Harambee, Bingwa, Kenya Police, Safaricom & Imarika SACCOs |

7.5% |

Source: Kenya Mortgage Refinance Company (KMRC)

KMRC, through the provision of low-interest, fixed, long-term financing to participating primary lenders at 5.0% with a repayment period of up to 25 years, has boosted the funds available for subsequent lending to borrowers at single-digit rates. Correspondingly, KMRC has increased the supply of housing finance in Kenya’s housing market by refinancing mortgage loans of its member PMLs. To this end, KMRC has been fundamental in the push to increase homeownership in Kenya. In terms of products, KMRC’s offers two key refinance loan products categorized as either:

- Affordable Housing Loans: These are loans extended to Primary Mortgage Lenders to refinance mortgage portfolios defined as “Affordable” by the Government capped at Kshs 8.0 mn in Nairobi Metropolitan Area (Nairobi, Kiambu, Machakos & Kajiado) and Kshs 6.0 mn in other parts of the country to individual borrowers whose monthly household income is not more than Kshs 150,000. These mortgages are predominantly refinanced through the concessional funding provided by the World Bank (up to 80.0% of portfolios presented to KMRC by PMLs) and AfDB funding (up to 40.0% of portfolios presented to KMRC by PMLs), and,

- Market-Rate Housing Loan: These are PML loans for mortgages with a value of more than Kshs 8.0 mn. These mortgages are partially refinanced through the concessional funding provided by the World Bank (up to 20.0% of the portfolio presented to KMRC by PMLs), the AfDB financing (up to 60.0% of the portfolio presented to KMRC by PMLs) and future bond issuances.

- KMRC Progress and Key Milestones Achieved

KMRC was incorporated in April 2018 in accordance with the requirements of the Companies Act 2015. In 2019, KMRC completed a successful capital mobilization drive resulting in the Government of Kenya, eight commercial banks, one microfinance bank and eleven SACCOs becoming shareholders of the Company. In June 2020, KMRC held its first Annual General Meeting and was later issued with its license in September 2020. Following its licensing by the CBK to begin core business operations, KMRC in December 2020 approved loans for disbursement of cumulative value Kshs 2.8 bn to participating PMLs. They included; KCB Bank Kenya Limited, Housing Finance Company Limited, Stima Sacco Society Limited, and Tower Sacco Society Limited. These approvals for disbursement were to be funded from the World Bank line of credit. It is worth noting however, that despite most of KMRC’s business operations beginning in 2020, actual lending operations to PML began in 2021. In 2021, KMRC disbursed Kshs 1.3 bn to seven PMLs out of the twelve received applications closing the year on a high note, and reported a Profit After Tax (PAT) of Ksh 0.2 bn for the year, a 154.6% increase from Kshs 0.1 bn in 2020. This improvement in performance was attributed to growth in investment income and disbursements to the primary mortgage lenders. The table below shows a summary of KMRC’s income statement for FY’2020 and FY’2021;

|

Cytonn Report: Summary of KMRC Statement of Comprehensive Income |

|||

|

|

FY’2020 |

FY’2021 |

y/y Change |

|

Interest Income: |

|

|

|

|

Interest on Loans and Advances |

- |

24,419,799 |

100.0% |

|

Other Interest Income |

221,094,696 |

686,526,589 |

210.5% |

|

Total Interest Income |

221,094,696 |

710,946,388 |

221.6% |

|

Interest Expenses |

(25,389,655) |

(246,873,372) |

872.3% |

|

Net Interest Income |

195,705,041 |

464,073,016 |

137.1% |

|

Impairment Provision |

- |

(440,814) |

100.0% |

|

Other expenses |

(78,474,909) |

(178,353,474) |

127.3% |

|

Total expenses |

(78,474,909) |

(178,794,288) |

127.8% |

|

Profit Before Tax (PBT) |

101,615,001 |

285,278,728 |

180.7% |

|

Income Tax Expense |

(24,397,662) |

(88,667,655) |

263.4% |

|

Profit After Tax (PAT) |

77,217,339 |

196,611,073 |

154.6% |

Source: Kenya Mortgage Refinance Company (KMRC)

The table below shows a summary of KMRC’s balance sheet for FY’2020 and FY’2021;

|

Cytonn Report: Summary of KMRC Statement of Financial Position |

|||

|

|

FY’2020 |

FY’2021 |

y/y Change |

|

Assets |

|||

|

Loans and Advances |

- |

1,286,717,998 |

0.0% |

|

Cash and Cash equivalents |

6,062,907,771 |

6,684,792,247 |

10.3% |

|

Total Assets |

6,309,802,091 |

9,823,579,908 |

55.7% |

|

Liabilities |

|||

|

Borrowings |

3,725,173,478 |

6,771,588,698 |

81.8% |

|

Total Liabilities |

3,793,113,568 |

7,456,134,267 |

96.6% |

|

Equity |

|||

|

Share Capital |

1,291,000,100 |

1,808,375,125 |

40.1% |

|

Total Equity |

2,516,688,523 |

2,367,445,641 |

(5.9%) |

Source: Kenya Mortgage Refinance Company (KMRC)

Other key milestones achieved by KMRC during 2021 and 2022 include;

- Blue Company Certification – KMRC become a certified blue company, an initiative that is geared towards helping to create a corruption-free business environment in East Africa,

- Standardization of mortgage origination practices – KMRC successfully managed to standardize mortgage origination practices for participating SACCOs. This was in turn expected to revolutionize mortgage lending to SACCOs and increase loan processing efficiency, and,

- Convened the first Affordable Housing Conference – In December 2021, KMRC convened its first Affordable Housing Conference geared towards enhancing demand and supply sides linkages, and discussing issues affecting the delivery of affordable housing and how to resolve them.

In January 2022, KMRC received approval from the CMA to issue a Medium-Term Note (MTN) under its inaugural bond program. The table below shows the particulars of the MTN;

|

Cytonn Report: Summary of KMRC Medium-Term Note |

|

|

Issuer |

Kenya Mortgage Refinance Company (KMRC) |

|

Trustee |

Ropat Trust Company Ltd |

|

Aggregate Nominal Amount |

Kshs 10.5 bn |

|

Issue Date |

4th March 2022 |

|

Listing Date |

14th March 2022 |

|

Nairobi Securities Exchange (NSE) Market Segment |

Fixed Income Securities Market Segment (FISMS) |

|

Tranche 1 |

Kshs 1.4 bn |

|

Oversubscription Rate |

478.6% |

|

Expected Date Tranche 2 |

June 2023 |

|

Interest Rates |

12.5% p.a., payable semi-annually in arrears |

|

Placing Agent |

NCBA Investment Bank Ltd. |

|

Receiving Bank |

KCB Bank Kenya Ltd. |

|

Specified Denomination |

Kshs 100,000 with integral multiples of Kshs 100,000 thereof |

|

Tenor |

7 years amortizing, with a Weighted Average Life of 4.5 years |

|

Interest on Late Payments |

Initial Interest Rate plus a margin of 2.0% p.a. to trade creditors |

|

Credit Rating |

GCR-AA+AA- (Highest certainty of timely payment of obligations) |

|

Default |

In case of default, issuer commences negotiations with any one or more of its creditors with a view to the general readjustment or rescheduling of its indebtedness. N/B; Trade creditors not mentioned |

Source: Kenya Mortgage Refinance Company (KMRC), Cytonn Research

The high oversubscription rates were attributable to the attractive returns to investors of 12.5%, and was partly on the back of the increased optimism on the firm having raised funds from the World Bank and African Development Bank. Following the MTN’s listing, KMRC’s subsequent bond issuing will most likely face competition from government instruments offering higher rates. To put this into context, 10-year government bonds currently offer coupon rates of up to 14.2% and would seem more attractive to investors. Notably, KMRC bond was assigned a national credit rating of AA- and AA+ in the long term and short term respectively, with an average risk score of 9.75 by the Global Credit Rating (CGR). The table below summarizes the rating particulars;

|

Cytonn Report: KMRC Global Credit Rating Scorecard |

|||||

|

Rated Entity |

Rating Class |

Rating Scale |

Rating |

Rating Description |

Outlook |

|

Kenya Mortgage Refinance Company Plc |

Long Term Issuer |

National |

AA-(KE) |

Very high credit quality relative to other issuers or obligations in the same country |

Stable Outlook |

|

Short Term Issuer |

National |

AA+(KE) |

Highest certainty of timely payment of Short term obligations relative to other issuers or obligations in the same country |

||

Source: Global Credit Rating (CGR)

Furthermore, during the year, KMRC disbursed an additional Kshs 5.7 bn, bringing the total number of funds disbursed to Kshs 7.0 bn as at September 2022, out of the Kshs 8.1 bn approved for refinancing to eight PMLs out of the 20 PMLs members. The disbursed amount represented 2,475 mortgages out of the total 2,781 mortgages approved for refinancing. KMRC refinancing activities are estimated to have created 9,900 jobs directly and indirectly and benefitted approximately 11,124 assuming an average household size of 4, with an estimated 30.0% of supported jobs benefitting females. Evidently, KMRC has made immense progress since it began operations two years ago and continues to deploy refinancing loans to support PMLs access long term liquidity and originate new affordable housing mortgages for the target income groups. African Development Bank (AfDB) latest September Implementation Progress and Results Report on KMRC reiterates the mortgage refinancing company’s positive progress in achieving its targets and objectives as being on track and has deemed it satisfactory.

- Recent Developments

Some of the recent developments by the KMRC aimed at improving the Kenyan mortgage market in 2023 include;

- In January, KMRC announced an increase in the limit or size of maximum mortgage in Kenya to be issued to its clients. The table below highlights the adjustments made;

|

Cytonn Report: Kenya Mortgage Refinancing Company (KMRC) limit of maximum mortgage in Kshs |

||

|

Region |

Previous limit of maximum mortgage in Kshs |

New limit of maximum mortgage in Kshs |

|

Nairobi Metropolitan Area- Nairobi County - Kiambu County - Kajiado County - Machakos County |

4.0 mn |

8.0 mn |

|

The rest of the 43 counties |

3.0 mn |

6.0 mn |

Source: Kenya Mortgage Refinance Company (KMRC)

Multiple factors served as impetus for the decision to revise the limit upwards including; i) renewed demand from buyers who previously postponed acquisitions during the height of the COVID-19 economic downturn, ii) hike in the prices of key construction materials such as steel, paint, and cement occasioned by supply chain bottlenecks resulting from the Russia-Ukraine war, ii) global and domestic inflationary pressures affecting the overall cost of goods and services, and iv) the continuing depreciation of the Kenyan Shilling against the US dollar. However, the Kshs 8.0 mn KMRC-backed mortgage is still relatively lower than the average maximum home loan amount, offered by other financial institutions averaging at Kshs 9.2 mn as at 2021, and,

- Moreover, KMRC raised the Loan to Value Ratio (LTV) to 105.0% from 90.0%, eliminating the need for a home-buyer to pay a 10.0% deposit prior to obtaining the mortgage plus another 5% needed for transaction costs. KMRC highlighted that the extra 5.0% above the value of the house under purchase was facilitated to cover incidental costs such as legal and appraisal fees. This move will greatly reduce the obstacles facing buyers in acquiring homes, thereby making the state-backed mortgage more attractive and affordable, particularly for first-time buyers in the low to middle-income bracket. As an illustration, to buy a house of Kshs. 8 mn, a buyer needed to come up with a 10% deposit of Kshs. 800k plus another Kshs. 400k for transaction costs, hence an upfront cost totaling Kshs. 1.2 mn. As of today, the buyer will no longer need to come up with the 1.2 mn, as they will only need to demonstrate an ability to service a loan of Kshs. 8.4 mn.

It is anticipated that KMRC's policy changes will enhance its competitiveness in providing affordable mortgages, thereby drawing more financial sector partners to expand loan opportunities. As a result, the move is expected to: i) increase homeownership for Kenyans, particularly in urban areas which currently stands at 22.0%, ii) drive growth in mortgage uptake, and iii) help address some of the major obstacles hindering mortgage uptake in the country. For more information regarding these recent developments, please see our Cytonn Monthly-January 2023.

- KMRC Achievements

The following are key achievements by KMRC;

- Increased liquidity to Primary Mortgage Lenders: KMRC's long-term funding has helped increase the liquidity of the mortgage market, making it easier for lenders to access the funding they need to provide mortgages to borrowers. In 2021, KMRC closed the year having disbursed Kshs 1.3 bn to seven PMLs. In 2022, as at September, KMRC had disbursed an additional Kshs 5.7 bn, bringing the total amounts disbursed to Kshs 7.0 bn, from the Kshs 8.1 bn available for refinancing. Notably, KMRC has continued to grow its affordable mortgage refinancing portfolio and as such has increased funding available to PMLs for onward lending to borrowers,

- Increased Mortgage Uptake in the country: The wholesale lender to PMLs cumulatively refinanced 2,475 mortgages out of the available 2,781 mortgages available for refinancing at a low interest rate of 5.0%. Consequently, this has enabled banks and SACCOs in partnership with KMRC to lend at a single digit rate of 9.5%, which is comparatively lower than market rates of between of 11.5% and 18.8%. This has made mortgages affordable and within the reach of many clients thereby increasing mortgage uptake,

- Promoted Financial Sector Inclusion: KMRC successfully managed to standardize mortgage origination practices for participating SACCOs in 2021. SACCOs play a vital role in Kenya’s finance and housing finance sector by bridging the gap in the housing finance market experienced in the lower income brackets, through the provision of unsecured, medium-term loans to their members. In support of this, the integration of the SACCO sector, which has demonstrated resilience and durability, could be a potential solution for providing mortgage loans to low- and informal-income earners in the near future, thereby boosting home ownership rates in the lower market segment,

- Improved Standards of Living: KMRC has improved the lives and living standards of many through job creation and employment. It is estimated that KMRC has benefitted approximately 11,124 persons, created and sustained 9,900 jobs in the mortgage industry and related sector. This number is expected to increase as the number of refinanced mortgages by the company increases,

- Promoting homeownership in Kenya: KMRC has helped improve the overall availability of housing funding in Kenya’s housing sector by providing long term funds and liquidity to PMLs. In this regard, KMRC has been instrumental in the push to increase homeownership in Kenya and in supporting the government’s Affordable Housing Plan,

- Successful issuance of its inaugural bond: KMRC got a nod from the CMA to roll out its Kshs 10.5 bn Medium Term Note programme in January 2022. In the first tranche of the issuance, the firm aimed to raise Kshs 1.4 bn and recorded an over subscription of 478.6%. Additionally, through its issuance of bonds, KMRC is contributing towards the development and advancement of the capital market in Kenya which remains severely under developed,

- Strengthened mortgage market infrastructure: KMRC has helped build and strengthen the infrastructure needed to support a thriving mortgage market in Kenya by establishing standard procedures and practices, and supporting capacity building initiatives for mortgage lenders. These efforts have helped increase the overall stability, efficiency, and quality of the mortgage market, making it easier for borrowers to access financing and become homeowners.

- KMRC Challenges

Despite the above achievements, KMRC has faced numerous challenges which include;

- High Property Prices: Rapidly rising residential property prices are increasingly making it difficult for low-income earners to access mortgages. This is attributable to land high costs especially in urban areas, rising construction costs, and costly land registration processes for multi-unit developments resulting in mortgaged purchases being priced higher by as much as 10% or more to cover developer’s carrying costs. During FY’2022, prices for detached units averaged at Kshs 12.4 mn while that of apartments averaged at Kshs 9.1 mn which are both higher than the KMRC affordable housing loan limits of Kshs 8.0 mn in the NMA region and Kshs 6.0 mn elsewhere. The table below shows the performance of both apartments and detached units in the Nairobi Metropolitan Area (NMA) in FY’2022 assuming an average size of 90-SQM unit;

|

Average Property Prices |

||||||

|

Segment |

Average Unit Size (SQM) |

Average Price per SQM FY'2022 |

Price FY'2022 |

Average Rental Yield FY'2022 |

Average Price Appreciation FY'2022 |

Total Returns |

|

Detached Units |

||||||

|

High End |

90 |

193,036 |

17.4 mn |

4.4% |

1.4% |

5.8% |

|

Upper Mid-End |

90 |

147,178 |

13.2 mn |

4.5% |

1.1% |

5.6% |

|

Satellite Towns |

90 |

73,696 |

6.6 mn |

5.0% |

1.0% |

6.0% |

|

Detached Units Average |

90 |

137,970 |

12.4 mn |

4.7% |

1.1% |

5.8% |

|

Apartments |

||||||

|

Upper Mid-End |

90 |

126,751 |

11.4 mn |

5.4% |

0.5% |

5.9% |

|

Lower Mid-End |

90 |

94,406 |

8.5 mn |

5.5% |

1.1% |

6.6% |

|

Satellite Towns |

90 |

82,586 |

7.4 mn |

5.5% |

1.4% |

6.9% |

|

Apartments Average |

90 |

101,248 |

9.1 mn |

5.5% |

1.0% |

6.5% |

Source: Cytonn Research

- Inability to Meet Criteria Threshold for Mortgage Products: The primary lending institutions have a set of eligibility criteria to meet before they can receive funding from KMRC, mostly set under the World Bank and African Development Bank (AfDB) standards. Most of these requirements have not been met thus limiting the number of primary mortgage lenders for the loans. For instance, in 2021, KMRC disbursed funds to only 7 PMLs out of the 12 applications received,

- Competition from other sources of financing: KMRC recently doubled its maximum loan limit to 8.0 mn however, it remains lower than the average maximum home loan amount, offered by other financial institutions averaging at Kshs 9.2 mn. Due to the low qualifying amounts, KMRC faces competition from other sources of financing, such as commercial banks, microfinance banks, and other financial institutions which offer higher maximum loan sizes or limits. This essentially means that absorption rates for KMRC backed mortgages will continue to be low,

- Elevated Credit Risk owing to a High Number of Non-Performing Loans (NPLs): According to Quarterly Economic Review July-September 2022 by the Central Bank of Kenya (CBK), Gross Non Performing Loans (NPLs) in the Real Estate sector increased to Kshs 75.6 bn in Q3’2022 from Kshs 69.2 bn recorded in Q3’2021, representing a 9.2% Year-on-Year (y/y) increase attributable to increased Real Estate loan default rates. An increase in NPLs in the Real Estate sector, indicates a higher risk for lenders and can indicate a downturn in the market. This can make it more difficult for KMRC to attract funding from its capital markets, as investors may become more cautious about lending money to the company. Additionally, if the Real Estate market continues to decline and more loans become NPLs, KMRC may face increased pressure to write off bad loans. This can impact the company's bottom line and reduce its ability to provide new loans to other borrowers, and,

- Cost of capital: KMRC’s current funding model is unclear and unsustainable, owing to the large negative spread between its cost of capital and lending rate. Based on KMRC’s latest issuance, its 7 year tenor bond raised in the market cost 12.5%. It is therefore not clear how the firm will maintain lending at a 5.0% rate while its borrowing costs are high hence deeming clarity on how KMRC will sustainably fund mortgages using its current financing model, once it exhausts the funding that was contributed by the original shareholders.

Section V: Case Studies and Lessons Learnt

In our previous topicals, Kenya Mortgage Refinance Company Progress 2022, Kenya Mortgage Refinance Company Update 2021, Kenya Mortgage Refinance Company Recap 2020, we provided case studies of Tanzania Mortgage Refinance Company, Jordan Mortgage Refinance Company and the Saudi Real Estate Refinancing company, respectively. In this topical, we now look at the lessons and key takeout’s that we can derive from the aforementioned mortgage refinancing companies alongside France's Caisse de Refinancement de l’Habitat (CRH), and Nigeria Mortgage Refinancing Company (NMRC);

|

Cytonn Report: Summary of Mortgage Refinance Companies in Various Countries |

|

|

Institution |

Key Takeouts/Achievements |

|

Jordan Mortgage Refinancing Company |

|

|

Saudi Real Estate Refinance Company |

|

|

Tanzania Mortgage Refinance Company |

|

|

France's Caisse de Refinancement de l’Habitat (CRH) |

|

|

Nigeria Mortgage Refinance Company |

|

Based on the aforementioned case studies, the following measures can be put in place to speed up funding for KMRC, and enhance its operations;

- Diversify funding sources: CRH has a diversified funding base, which includes both long-term and short-term bonds, which helps ensure sustainability of funding. KMRC can diversify its funding sources by issuing bonds with both longer and shorter tenors. Longer term bonds can provide a stable and predictable source of funding for KMRC over the long term whereas, short-term bonds can be used to meet immediate financing needs, as they can be issued and redeemed quickly. By issuing both, KMRC can attract a wider range of investors and increase its access to capital, helping to diversify its funding sources. Currently, KMRC only one 7-year tenor MTN issued under its inaugural bond program,

- Innovative Products and Services: NMRC has established a secondary market for mortgage-backed securities, which allows mortgage lenders to sell their existing mortgages to other investors in the secondary capital market. This has provided mortgage lenders with much-needed liquidity and helped to deepen the Nigerian mortgage market. Securitization presents a plausible channel to raise capital for KMRC. However, the lack of standardization of lending terms in Kenya has been a hindrance to the development of mortgage backed securities market. KMRC had back in 2021 initiated harmonization of the same, however that is yet to materialize. KMRC would benefit from an additional avenue to raise funding and should therefore see to having it implemented,

- Foster partnerships and collaboration with member PMLs: Support provided by members of the CRH is a key component of the MLFs business model that have contributed to its success. KMRC should prioritize the establishment of a solid solidarity mechanism and foster partnerships and collaborations among its shareholders. This will ensure that all stakeholders have a vested interest in the success of the company and are obligated to regularly contribute to meet its liquidity,

- Increased Transparency: Many market participants have questions about KMRC’s funding model and the sustainability of its lending rate considering its high cost of capital. As such, it would be constructive for KMRC’s board and management to come out and address this market concern,

- Low Qualifying Amounts: The low qualifying amounts of up to Kshs 8.0 mn fall below the average mortgage size of Kshs 9.2 mn offered by other financial institutions as at 2021, implying that the uptake of mortgages backed by KMRC will remain low due to this mismatch. KMRC should consider revising the limits regularly to be in tandem with other financial institutions so as to remain competitive,

- Further develop its Legal and Regulatory Framework: KMRC has failed to accommodate financing of rental development in its mandate despite its significant role in achieving affordable housing. Rental housing is an important component of the affordable housing ecosystem, as it provides a more flexible and accessible option for those who cannot afford to buy a home. Incorporating financing of rental development into KMRC's mandate could play a crucial role in achieving the affordable housing agenda in Kenya by increasing the supply of affordable rental housing, thereby improving living standards,

- Public Education and Increased Awareness: KMRC should work towards increasing awareness of its existence and its mortgage products to potential home owners through awareness campaigns. Public education is critical in creating awareness of available mortgage products and their demystification. This is likely help in increasing mortgage uptake in Kenya which has remained relatively low partially due to limited knowledge of affordable home financing options,

- Tax exemptions: Interest earned and profits realized from bonds issued by the JRC are exempted from tax. KMRC should incentivize investors by doing away with tax on the interests and profits realized by their investors. Currently, investors are charged a 15.0% withholding tax, and,

- Green Shoe Option in Bonds: Lastly, KMRC should consider incorporating the green shoe option, which is an overallotment provision in its subsequent bond issuances. This would allow for the issuer to capitalize on oversubscription rates over and above issued bond amounts if demand by investors is higher than expected, thus allowing the lender to raise more capital.

Section VI: Conclusion

The Kenya Mortgage Refinance Company (KMRC) has made considerable strides towards its goal of enhancing the flow of long-term funds in the Kenyan mortgage industry, and offering affordable financing options to mortgage lenders. The company's efforts to offer mortgages to clients at low interest rates will continue to spur mortgage uptake, leading to an increase in home ownership rates. However, the sustainability of KMRC’s funding model remains our primary concern, which we fathom requires attention due to the negative spread between the cost of capital and its lending rate. However, we expect the integration of the SACCO sector will be a vital contributor and key lever in originating and distributing mortgage loans to low-income and informal-income earners in the near future. Moreover, we expect to see KMRC issue more bonds, with a particular emphasis on environmentally friendly green bonds that are gaining widespread popularity globally. This is on the back of the issuer’s expressed interest to tap into the Green Market in July 2022, in line with the Kenya Green Bonds Program aimed at encouraging development of affordable green housing in Kenya. Overall, we are of the view that KMRC's role as a refinancing service provider, its ability to provide mortgages at lower borrowing costs, and its support in the growth of the mortgage industry make it a pivotal player in achieving Kenya's affordable housing plan.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma