Kenya's Listed Insurance Report H1'2023, & Cytonn Weekly #43/2023

By Research Team, Oct 29, 2023

Executive Summary

Fixed Income

During the week, T-bills were undersubscribed for the first time in four weeks, with the overall subscription rate coming in at 75.6%, albeit lower than the oversubscription rate of 123.4% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 10.6 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 266.0%, albeit lower than the oversubscription rate of 588.9% recorded the previous week. The subscription rate for the 182-day paper increased to 56.7%, from 37.9% recorded the previous week, while the subscription rate of the 364-day paper decreased to 18.4%, from 22.7% recorded the previous week. The government accepted a total of Kshs 15.7 bn worth of bids out of Kshs 18.2 bn of bids received, translating to an acceptance rate of 86.2%. The yields on the government papers were on an upward trajectory, with the yields on the 364-day, 182-day and 91-day papers increasing by 4.6 bps, 5.3 bps and 6.5 bps to 15.4%, 15.1% and 15.1%, respectively;

Equities

During the week, the equities market was on a downward trajectory, with NASI declining the most by 4.0%, while NSE 20, NSE 25 and NSE 10 declined by 1.9%, 2.4% and 2.6%, respectively, taking the YTD performance to losses of 29.8%, 12.7%, and 23.5% for NASI, NSE 20, and NSE 25, respectively. The equities market performance was mainly driven by losses recorded by large-cap stocks such as Safaricom, KCB and DTB-K of 9.4%, 5.3% and 3.2%, respectively. The losses were however mitigated by gains recorded by stocks such as Equity Bank and Cooperative Bank of 2.0% and 1.7% respectively;

Real Estate

During the week, Kenya’s Diamonds Resorts secured two prestigious awards at the 30th World Travel Awards 2023. Diamond Leisure Beach and Golf Resort located in Diani, and Diamond’s Dreams of Africa Resort which is located in Malindi, Kenya were crowned Africa’s Leading Resort and Africa’s Leading All-Inclusive Resort respectively;

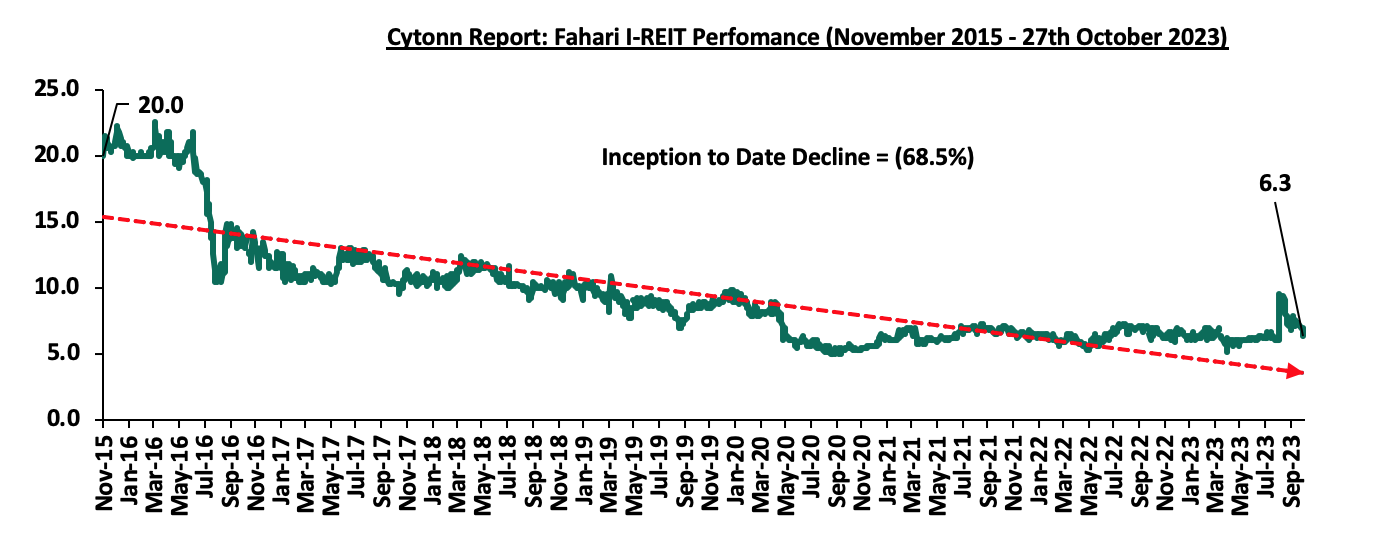

On the Nairobi Securities Exchange, LAPTrust Imara I-REIT traded for the first time on 25th October 2023 since its listing in March 2023. In two deals the Fund traded 30.0 mn shares valued at Kshs 600.0 mn. ILAM Fahari I-REIT closed the week trading at an average price of Kshs 6.3 per share after a two-weeks trading suspension from Friday 6th October 2023.

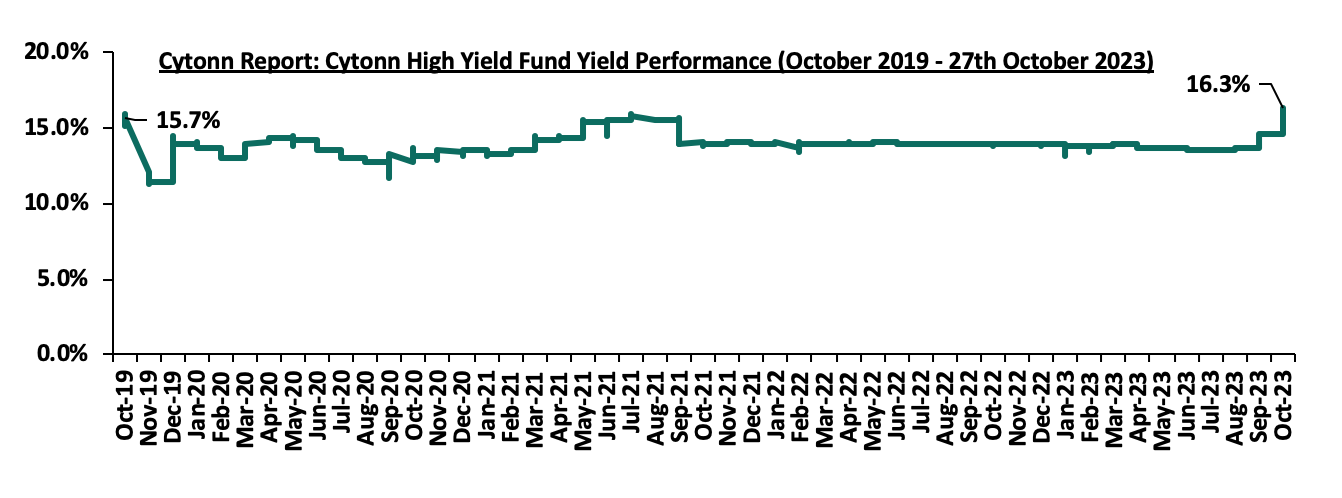

On the Unquoted Securities Platform, as at 27th October 2023, Acorn D-REIT and I-REIT closed the week trading at Kshs 25.3 and Kshs 21.7 per unit, a 26.6% and 8.2% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 listing price. In addition, Cytonn High Yield Fund (CHYF) closed the week with an annualized yield of 16.3%, a 0.2%-points increase from the 16.1% recorded the previous week;

Focus of the Week

Following the release of H1’2023 results by insurance companies, this week we analyze the performance of the 5 listed insurance companies in Kenya, identify the key factors that influenced their performance, and give our outlook for the insurance sector going forward;

Investment Updates:

- Weekly Rates:

- Cytonn Money Market Fund closed the week at a yield of 14.53% p.a. To invest, dial *809# or download the Cytonn App from Google Playstore here or from the Appstore here;

- Cytonn High Yield Fund closed the week at a yield of 16.34% p.a. To invest, email us at sales@cytonn.com and to withdraw the interest, dial *809# or download the Cytonn App from Google Play store here or from the Appstore here;

- We continue to offer Wealth Management Training every Wednesday, from 9:00 am to 11:00 am. The training aims to grow financial literacy among the general public. To register for any of our Wealth Management Trainings, click here;

- If interested in our Private Wealth Management Training for your employees or investment group, please get in touch with us through wmt@cytonn.com;

- Cytonn Insurance Agency acts as an intermediary for those looking to secure their assets and loved ones’ future through insurance namely; Motor, Medical, Life, Property, WIBA, Credit and Fire and Burglary insurance covers. For assistance, get in touch with us through insuranceagency@cytonn.com;

- Cytonn Asset Managers Limited (CAML) continues to offer pension products to meet the needs of both individual clients who want to save for their retirement during their working years and Institutional clients that want to contribute on behalf of their employees to help them build their retirement pot. To more about our pension schemes, kindly get in touch with us through pensions@cytonn.com;

Real Estate Updates:

- For more information on Cytonn’s real estate developments, email us at sales@cytonn.com;

- Phase 3 of The Alma is now ready for occupation and the show house is open daily. To join the waiting list to rent, please email properties@cytonn.com;

- For Third Party Real Estate Consultancy Services, email us at rdo@cytonn.com;

- For recent news about the group, see our news section here;

Hospitality Updates:

- We currently have promotions for Staycations. Visit cysuites.com/offers for details or email us at sales@cysuites.com;

Money Markets, T-Bills Primary Auction:

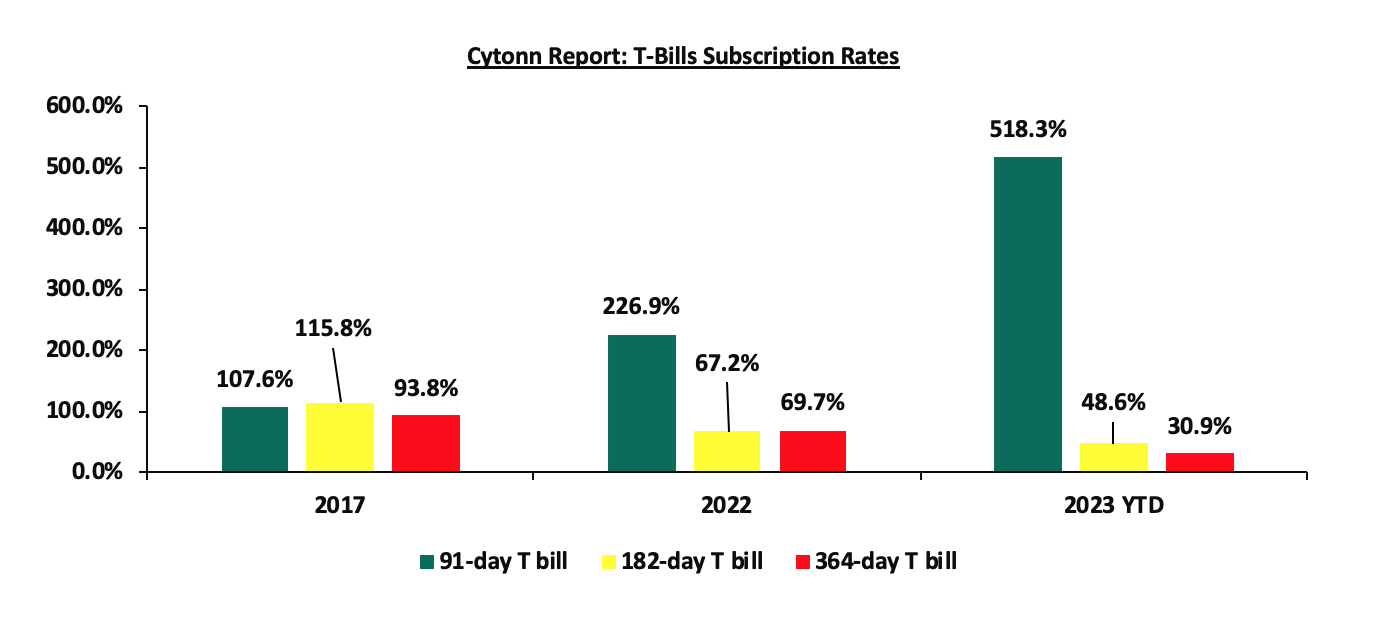

During the week, T-bills were undersubscribed for the first time in four weeks, with the overall subscription rate coming in at 75.6%, albeit lower than the oversubscription rate of 123.4% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 10.6 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 266.0%, albeit lower than the oversubscription rate of 588.9% recorded the previous week. The subscription rate for the 182-day paper increased to 56.7%, from 37.9% recorded the previous week. While, the subscription rate of the 364-day paper decreased to 18.4%, from 22.7% recorded the previous week. The government accepted a total of Kshs 15.7 bn worth of bids out of Kshs 18.2 bn of bids received, translating to an acceptance rate of 86.2%. The yields on the government papers were on an upward trajectory, with the yields on the 364-day, 182-day and 91-day papers increasing by 4.6 bps, 5.3 bps and 6.5 bps to 15.4%, 15.1% and 15.1%, respectively; The chart below compares the overall average T- bills subscription rates obtained in 2017, 2022 and 2023 Year to Date (YTD):

Money Market Performance:

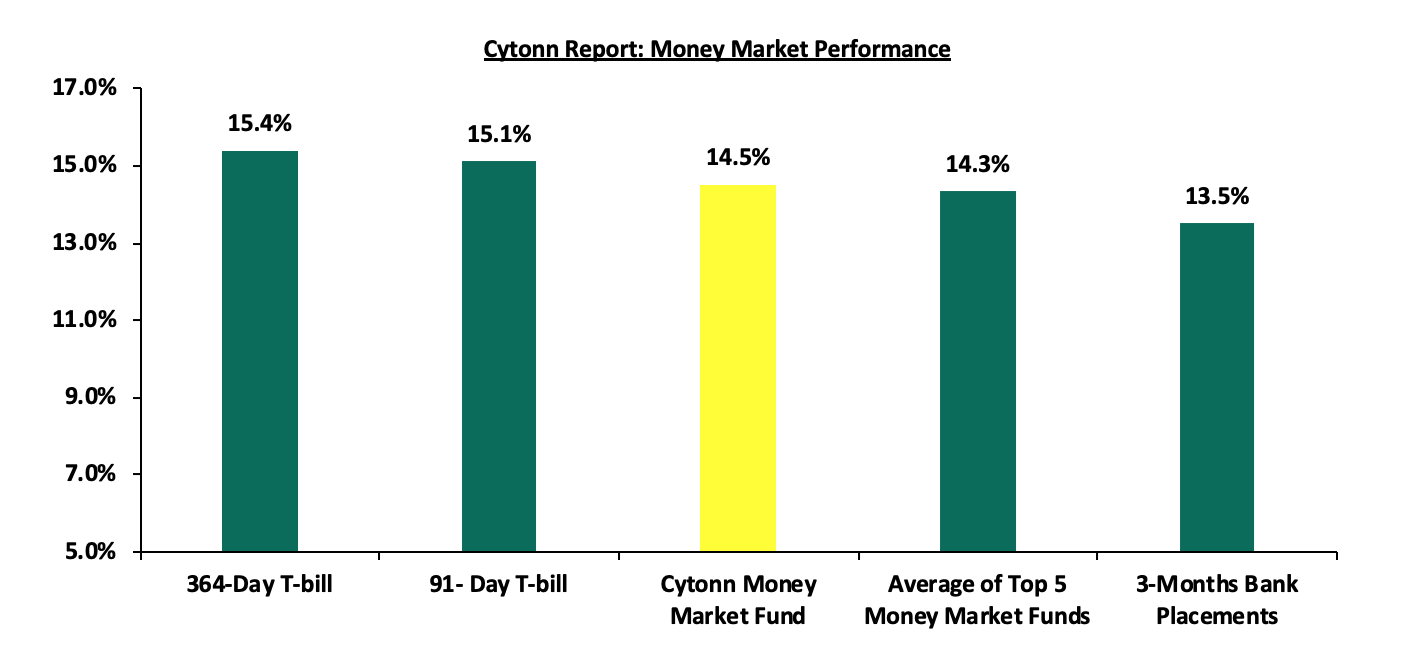

In the money markets, 3-month bank placements ended the week at 13.5% (based on what we have been offered by various banks), and the yields on the 364-day and 91-day T-bill increased by 4.6 bps and 6.5 bps to 15.4% and 15.1%, respectively. The yields of the Cytonn Money Market Fund decreased by 4.0 bps to 14.5% from 14.6% recorded the previous week, and the average yields on the Top 5 Money Market Funds increased by 20.6 bps to 14.3%, from 14.1% recorded the previous week.

The table below shows the Money Market Fund Yields for Kenyan Fund Managers as published on 27th October 2023:

|

Cytonn Report: Money Market Fund Yield for Fund Managers as published on 27th October 2023 |

||

|

Rank |

Fund Manager |

Effective Annual |

|

1 |

GenAfrica Money Market Fund |

14.9% |

|

2 |

Cytonn Money Market Fund |

14.5% |

|

3 |

Enwealth Money Market Fund |

14.4% |

|

4 |

Apollo Money Market Fund |

14.2% |

|

5 |

Lofty-Corban Money Market Fund |

13.7% |

|

6 |

Madison Money Market Fund |

13.7% |

|

7 |

Etica Money Market Fund |

13.6% |

|

8 |

AA Kenya Shillings Fund |

13.2% |

|

9 |

Jubilee Money Market Fund |

13.1% |

|

10 |

Co-op Money Market Fund |

13.1% |

|

11 |

Sanlam Money Market Fund |

12.8% |

|

12 |

GenCap Hela Imara Money Market Fund |

12.8% |

|

13 |

Kuza Money Market fund |

12.8% |

|

14 |

Old Mutual Money Market Fund |

12.5% |

|

15 |

Nabo Africa Money Market Fund |

12.4% |

|

16 |

Absa Shilling Money Market Fund |

12.2% |

|

17 |

KCB Money Market Fund |

12.0% |

|

18 |

ICEA Lion Money Market Fund |

11.6% |

|

19 |

Equity Money Market Fund |

11.5% |

|

20 |

CIC Money Market Fund |

11.4% |

|

21 |

Dry Associates Money Market Fund |

11.3% |

|

22 |

Orient Kasha Money Market Fund |

11.1% |

|

23 |

Mali Money Market Fund |

10.3% |

|

24 |

British-American Money Market Fund |

9.5% |

Source: Business Daily

Liquidity:

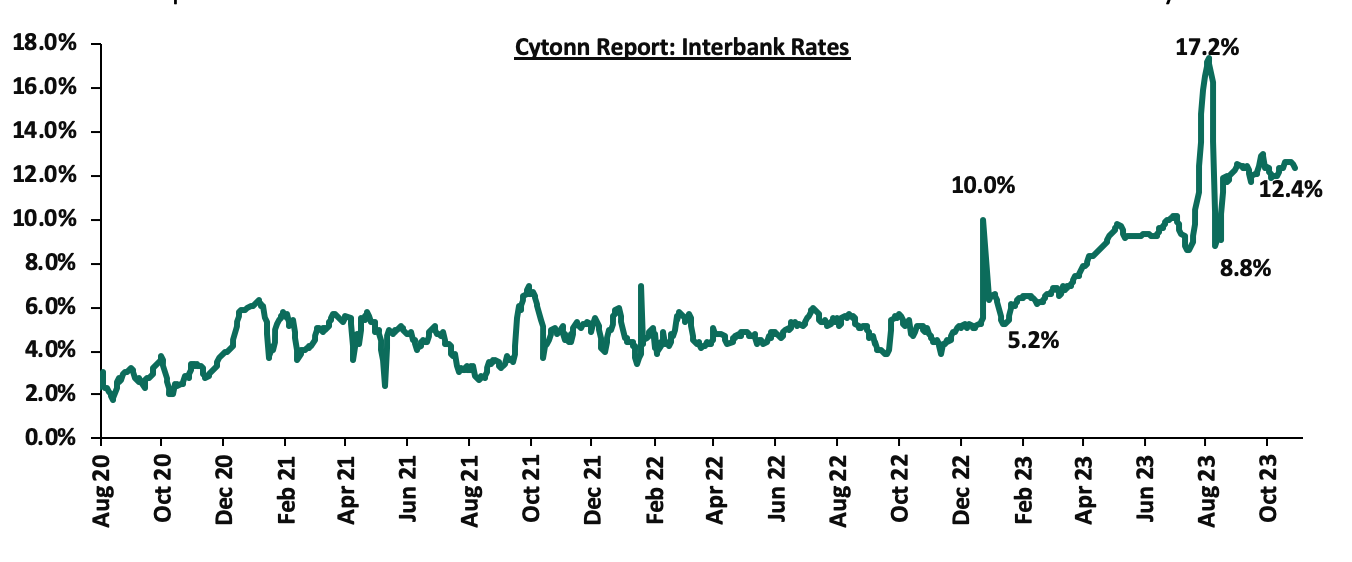

During the week, liquidity in the money markets marginally tightened, with the average interbank rate remaining relatively unchanged at 12.5%, partly attributable to tax remittances that offset government payments. The average interbank volumes traded decreased by 22.3% to Kshs 14.1 bn from Kshs 18.1 bn recorded the previous week. The chart below shows the interbank rates in the market over the years:

Kenya Eurobonds:

During the week, the yields on Eurobonds recorded mixed performance, with the yield on the 10-year Eurobond issued in 2018 increasing the most by 0.4% points to 13.6%, from 13.1% recorded the previous week. The table below shows the summary of the performance of the Kenyan Eurobonds as of 26th October 2023;

|

Cytonn Report: Kenya Eurobonds Performance |

||||||

|

|

2014 |

2018 |

2019 |

2021 |

||

|

Tenor |

10-year issue |

10-year issue |

30-year issue |

7-year issue |

12-year issue |

12-year issue |

|

Amount Issued (USD) |

2.0 bn |

1.0 bn |

1.0 bn |

0.9 bn |

1.2 bn |

1.0 bn |

|

Years to Maturity |

0.7 |

4.4 |

24.4 |

3.6 |

8.6 |

10.7 |

|

Yields at Issue |

6.6% |

7.3% |

8.3% |

7.0% |

7.9% |

6.2% |

|

02-Jan-23 |

12.9% |

10.5% |

10.9% |

10.9% |

10.8% |

9.9% |

|

02-Oct-23 |

19.0% |

13.5% |

12.6% |

14.6% |

12.9% |

12.5% |

|

18-Oct-23 |

16.5% |

13.1% |

12.8% |

15.0% |

13.3% |

12.9% |

|

19-Oct-23 |

16.7% |

14.3% |

12.8% |

15.1% |

13.4% |

13.0% |

|

23-Oct-23 |

16.1% |

14.0% |

12.7% |

14.7% |

13.2% |

12.7% |

|

24-Oct-23 |

14.8% |

13.6% |

12.4% |

14.1% |

12.9% |

12.4% |

|

25-Oct-23 |

14.9% |

13.6% |

12.4% |

14.0% |

12.8% |

12.4% |

|

Weekly Change |

(1.7%) |

0.4% |

(0.4%) |

(1.0%) |

(0.5%) |

(0.5%) |

|

MTD Change |

(4.1%) |

0.1% |

(0.2%) |

(0.6%) |

(0.0%) |

(0.1%) |

|

YTD Change |

2.0% |

3.1% |

1.5% |

3.1% |

2.1% |

2.6% |

Source: Central Bank of Kenya (CBK) and National Treasury

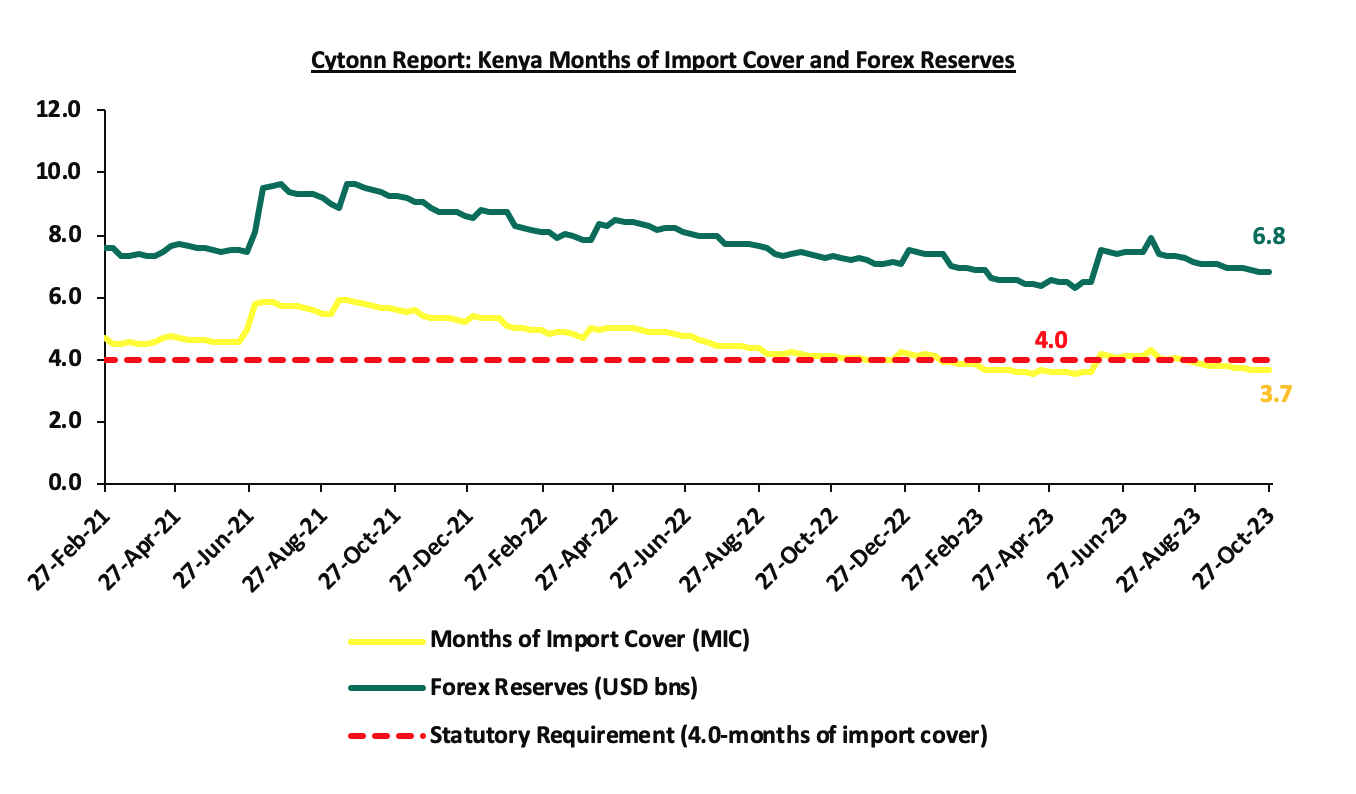

Kenya Shilling:

During the week, the Kenya Shilling depreciated against the US Dollar by 0.4% to close at Kshs 150.4, from Kshs 149.8 recorded the previous week. On a year to date basis, the shilling has depreciated by 21.8% against the dollar, adding to the 9.0% depreciation recorded in 2022. We expect the shilling to remain under pressure in 2023 as a result of:

- An ever-present current account deficit which came at 3.7% of GDP in Q2’2023 from 6.0% recorded in a similar period last year,

- The need for government debt servicing, continues to put pressure on forex reserves given that 67.1% of Kenya’s external debt was US Dollar denominated as of June 2023, and,

- Dwindling forex reserves currently at USD 6.8 bn (equivalent to 3.7-months of import cover), which is below the statutory requirement of maintaining at least 4.0-months of import cover.

The shilling is however expected to be supported by:

- Diaspora remittances standing at a cumulative USD 3,106.7 mn in 2023 as of September 2023, 3.8% higher than the USD 2,992.5 mn recorded over the same period in 2022. In the September 2023 diaspora remittances figures, North America remained the largest source of remittances to Kenya accounting for 57.0% in the period, and,

- The tourism inflow receipts which came in at USD 268.1 bn in 2022, a significant 82.9% increase from USD 146.5 bn inflow receipts recorded in 2021.

The chart below summarizes the evolution of Kenya months of import cover over the years:

Weekly Highlights:

- October 2023 Inflation Projection

We are projecting the y/y inflation rate for October 2023 to come in at the range of 6.8%-7.0% mainly on the back of:

- Increased Fuel Prices – The Energy and Petroleum Regulatory Authority (EPRA) announced a rise in the maximum retail fuel prices in Kenya, effective 15th October 2023 to 14th November 2023. Consequently, the fuel prices for super petrol, Diesel and Kerosene increased by 2.7%, 2.2% and 1.2% to Kshs 217.4, Kshs 205.5 and Kshs 205.1, respectively, up from Kshs 211.6, Kshs 201.0 and Kshs 202.6 recorded in the previous period. The Fuel prices in the country remain elevated with the average landing costs per cubic meter for super petrol and diesel increasing by 3.9% and 7.1% to USD 805.1 and USD 845.7 in September 2023, from USD 774.7 and USD 789.9, respectively, in August 2023. However, the average landing costs of kerosene decreased by 5.0% to USD 868.7 in September 2023, from USD 827.3 in August 2023. Notably, global oil prices eased up in October 2023, having decreased by 4.3% to USD 92.0 as of 27th October 2023, from USD 96.1 recorded on 29th September 2023, and,

- Increased food and commodity prices – Anticipated rises in fuel costs are predicted to drive up food prices, leading to transfer-inflation affecting both food and non-food items.

As a result, we foresee a surge in the inflation rate for October, primarily due to the escalating fuel costs, considering its crucial role in the country’s production. It’s worth noting that the ongoing depreciation of the Kenya Shilling has led to an increase in commodity prices nationwide. This depreciation has inflated the import bill, causing manufacturers to transfer the cost burden to consumers by raising commodity prices.

In the near future, we anticipate that inflationary pressures will continue, but they are expected to moderate in the medium term to the Central Bank of Kenya’s target range of 2.5% to 7.5%. This is due to the expected decrease in global oil prices and a reduction in local food prices, thanks to favorable weather conditions that will boost agricultural production and subsequently lower food prices. Additionally, we foresee that government initiatives to subsidize key agricultural inputs like fertilizers will reduce farming costs and contribute to long-term inflation relief.

Rates in the Fixed Income market have been on an upward trend given the continued high demand for cash by the government and the occasional liquidity tightness in the money market. The government is 19.4% behind of its prorated net domestic borrowing target of Kshs 91.2 bn, having a net borrowing position of Kshs 73.5 bn of the domestic net borrowing target of Kshs 316.0 bn for the FY’2023/2024. Therefore, we expect a continued upward readjustment of the yield curve in the short and medium term, with the government looking to bridge the fiscal deficit through the domestic market. Owing to this, our view is that investors should be biased towards short-term fixed-income securities to reduce duration risk.

Market Performance:

During the week, the equities market was on a downward trajectory, with NASI declining the most by 4.0%, while NSE 20, NSE 25 and NSE 10 declined by 1.9%, 2.4% and 2.6%, respectively, taking the YTD performance to losses of 29.8%, 12.7%, and 23.5% for NASI, NSE 20, and NSE 25, respectively. The equities market performance was mainly driven by losses recorded by large-cap stocks such as Safaricom, KCB and DTB-K of 9.4%, 5.3% and 3.2%, respectively. The losses were however mitigated by gains recorded by stocks such as Equity Bank and Cooperative Bank of 2.0% and 1.7% respectively.

During the week, equities turnover increased by 177.6% to USD 11.1 mn, from USD 4.0 mn recorded the previous week, taking the YTD total turnover to USD 598.5 mn. Foreign investors remained net sellers for the third consecutive week with a net selling position of USD 2.3 mn, from a net selling position of USD 0.9 mn recorded the previous week, taking the YTD foreign net selling position to USD 285.1 mn.

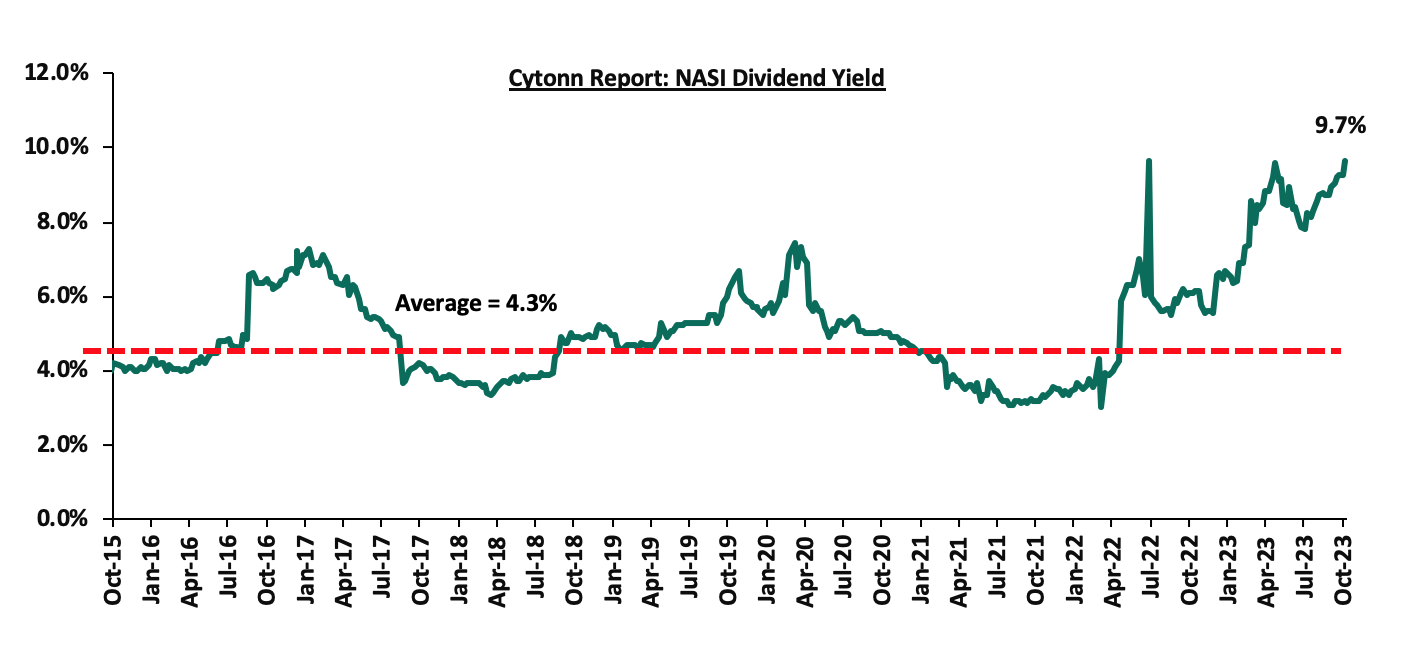

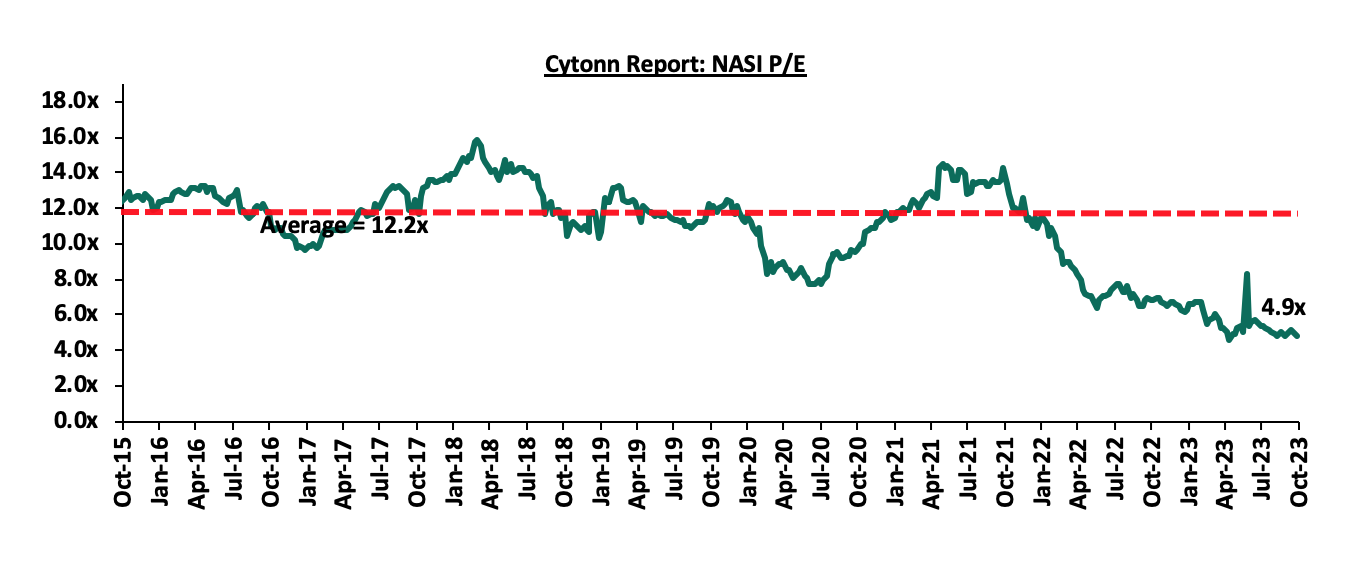

The market is currently trading at a price to earnings ratio (P/E) of 4.9x, 60.1% below the historical average of 12.2x. The dividend yield stands at 9.7%, 5.3% points above the historical average of 4.3%. Key to note, NASI’s PEG ratio currently stands at 0.6x, an indication that the market is undervalued relative to its future growth. A PEG ratio greater than 1.0x indicates the market is overvalued while a PEG ratio less than 1.0x indicates that the market is undervalued. The charts below indicate the historical P/E and dividend yields of the market;

Universe of Coverage:

|

Cytonn Report: Equities Universe of Coverage |

|||||||||

|

Company |

Price as at 19/10/2023 |

Price as at 27/10/2023 |

w/w change |

YTD Change |

Target Price* |

Dividend Yield |

Upside/ Downside** |

P/TBv Multiple |

Recommendation |

|

KCB Group*** |

19.9 |

18.9 |

(5.3%) |

(50.8%) |

30.7 |

10.6% |

73.5% |

0.3x |

Buy |

|

Kenya Reinsurance |

1.8 |

1.8 |

(1.1%) |

(6.4%) |

2.5 |

11.4% |

54.9% |

0.1x |

Buy |

|

Liberty Holdings |

3.8 |

4.0 |

5.0% |

(20.8%) |

5.9 |

0.0% |

48.4% |

0.3x |

Buy |

|

Jubilee Holdings |

186.0 |

185.0 |

(0.5%) |

(6.9%) |

260.7 |

6.5% |

47.4% |

0.3x |

Buy |

|

CIC Group |

2.0 |

1.9 |

(6.5%) |

(2.1%) |

2.5 |

7.0% |

40.6% |

0.6x |

Buy |

|

Diamond Trust Bank*** |

46.5 |

45.0 |

(3.2%) |

(9.7%) |

58.1 |

11.1% |

40.2% |

0.2x |

Buy |

|

Sanlam |

7.7 |

7.4 |

(3.9%) |

(22.8%) |

10.3 |

0.0% |

39.1% |

2.1x |

Buy |

|

I&M Group*** |

17.7 |

17.3 |

(2.3%) |

1.5% |

21.8 |

13.0% |

39.0% |

0.4x |

Buy |

|

ABSA Bank*** |

12.0 |

11.9 |

(0.8%) |

(2.9%) |

14.8 |

11.4% |

36.3% |

1.0x |

Buy |

|

Co-op Bank*** |

11.6 |

11.8 |

1.7% |

(2.5%) |

13.5 |

12.7% |

27.1% |

0.6x |

Buy |

|

Britam |

4.6 |

4.8 |

2.8% |

(8.5%) |

6.0 |

0.0% |

25.4% |

0.7x |

Buy |

|

Standard Chartered*** |

160.0 |

156.0 |

(2.5%) |

7.6% |

170.9 |

14.1% |

23.7% |

1.1x |

Buy |

|

Equity Group*** |

37.3 |

38.0 |

2.0% |

(15.6%) |

42.6 |

10.5% |

22.6% |

0.8x |

Buy |

|

NCBA*** |

39.8 |

39.0 |

(2.0%) |

0.1% |

43.2 |

10.9% |

21.7% |

0.8x |

Buy |

|

Stanbic Holdings |

109.0 |

109.0 |

0.0% |

6.9% |

118.2 |

11.6% |

20.0% |

0.8x |

Buy |

|

HF Group |

4.3 |

4.0 |

(6.3%) |

27.0% |

3.2 |

0.0% |

(20.0%) |

0.2x |

Sell |

We are “Neutral” on the Equities markets in the short term due to the current tough operating environment and huge foreign investor outflows, and, “Bullish” in the long term due to current cheap valuations and expected global and local economic recovery.

With the market currently being undervalued to its future growth (PEG Ratio at 0.6x), we believe that investors should reposition towards value stocks with strong earnings growth and that are trading at discounts to their intrinsic value. We expect the current high foreign investors sell-offs to continue weighing down the equities outlook in the short term.

- Residential Sector

During the week, Kenya’s Diamonds Resorts secured two prestigious awards at the 30th World Travel Awards 2023. Diamond Leisure Beach and Golf Resort located in Diani, and Diamond’s Dreams of Africa Resort which is located in Malindi, Kenya were crowned Africa’s Leading Resort and Africa’s Leading All-Inclusive Resort respectively. Set against a stunning costal backdrop, the hotels offer a sanctuary of unparalleled hospitality where tourists can enjoy a luxurious lifestyle, pristine beaches, top-tier amenities, and exciting experiences. Notably, a total of 13 Kenyan hotels received awards in the best African category, as highlighted below;

|

|

Cytonn Report: 30th World Travel Awards 2023 Kenya Hotels Winners in the African Category |

|

|

# |

Hotel |

Award |

|

1 |

Diamond Leisure Beach and Golf Resort |

Africa’s Leading Resort |

|

2 |

Four Points by Sheraton Nairobi Airport |

Africa’s Leading Airport Hotel |

|

3 |

Diamond’s Dreams of Africa |

Africa’s Leading All-Inclusive Resort |

|

4 |

Swahili Beach |

Africa’s Leading Beach Resort |

|

5 |

Billionaire Resort and Retreat |

Africa’s Leading Boutique Resort |

|

6 |

Fairmont The Norfolk |

Africa’s Leading City Hotel |

|

7 |

Baobab Beach Resort and Spa |

Africa’s Leading Family Resort |

|

8 |

Fairmont Mount Kenya Safari Club |

Africa’s Leading Hotel |

|

9 |

Leopard Beach Resort and Spa |

Africa’s Leading Hotel Residences |

|

10 |

Sirai House |

Africa’s Leading Private Luxury Private Villa |

|

11 |

Somerset Westview |

Africa’s Leading Serviced Apartments Hotel |

|

12 |

Finch Hattons |

Africa’s Leading Tented Safari Camp |

|

13 |

Manda Bay |

Africa’s Leading Private Island Resort |

Source: Word Travel Awards

In terms of destinations, Nairobi and Diani emerged as Africa’s top destinations in various categories. Overall, Kenya was voted as Africa’s Leading Destination 2023, marking the second consecutive win after emerging top in the 29th World Travel Awards in 2022. The table below shows the key awards for top Kenya destinations in the African category 2023;

|

Cytonn Report: Top Kenya Destinations in the African Category 2023 |

||

|

# |

Destination |

Award |

|

1 |

Diani, Kenya |

Africa’s Leading Beach Destination |

|

2 |

Nairobi, Kenya |

Africa’s Leading Business Travel Destination |

|

3 |

Kenya |

Africa’s Leading Destination |

Source: World Travel Awards

In our view, the aforementioned awards where Kenya was voted as Africa’s leading destination therefore positions the country as a vibrant tourism market. This is expected to further boost investor confidence in the hospitality market as well as lead to an increase in visitor arrivals into the country. Some of the factors that are expected to further enhance the growth of the sector include; i) concerted efforts to promote local and regional tourism, ii) aggressive marketing campaigns by the Kenya Tourism Board on the Magical Kenya platform, iii) implementation of vital government initiatives such as the New Tourism Strategy for Kenya 2021-2025, iv) continuous opening and expansions by local and international hotel brands such as JW Marriott of the Bonvoy Global and Pan Pacific Hotels Group in the country, and, v) increased visitor arrivals into the country gearing towards pre-COVID levels. However, the; i) recent austerity measures implemented by the Chief of Staff and Head of Public Service, including the indefinite suspension of non-essential local and foreign travels, ii) newly issued travel advisories by multiple governments, including those of China and the United States in light of heightened security concerns and threats, and iii) soaring operational costs exacerbated by rising inflation amidst a tough micro-economic climate are expected to weigh down the optimal performance of the hospitality sector in the country.

- Regulated Real Estate Funds

- Real Estate investment trusts (REITs)

During the week, LAPTrust Imara I-REIT traded for the first time on 25th October 2023 since its listing, with a total of 30.0 mn shares traded in two deals valued at Kshs 600.0 mn. The restricted I-REIT’s share price remained unchanged from its listing price of Kshs 20.00. The I-REIT which is structured as a close-ended fund consisting of 346.2 mn units worth Kshs 6.9 bn was initially intended to remain non-public, with no securities offered to the general market for the next three years. The decision was to provide the I-REIT sufficient time to build a performance track record, allowing investors to gain confidence in the asset class. Imara I-REIT which was listed in March 2023 is listed on the Main Investment Market – Restricted Sub-Segment of the Nairobi Securities Exchange, and its units can only be traded to persons qualifying as professional investors, confined to high net-worth individuals and institutions. For more information, please see our Cytonn Weekly # 12/2023.

In the Nairobi Securities Exchange, ILAM Fahari I-REIT closed the week trading at an average price of Kshs 6.3 per share after a two-week trading suspension from Friday 6th October 2023. Trading of Fahari I-REIT’s units had been suspended to allow for the redemption of 36.6 mn units from Non-Professional investors in order to facilitate the conversion of the I-REIT into a restricted REIT from an un-restricted REIT. The performance represents a 16.2% decline from Kshs 7.5 per share recorded on 6th October 2023, taking it to a 7.1% Year-to-Date (YTD) loss from Kshs 6.8 per share recorded on 3 January 2023. Additionally, the performance represents a 68.5% Inception-to-Date (ITD) loss from the Kshs 20.0 price. The dividend yield currently stands at 10.3%. The graph below shows Fahari I-REIT’s performance from November 2015 to 27th October 2023;

In the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 25.3 and Kshs 21.7 per unit, respectively, as of 27th October 2023. The performance represented a 26.6% and 8.2% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. The volumes traded for the D-REIT and I-REIT came in at 12.3 mn and 30.7 mn shares, respectively, with a turnover of Kshs 257.5 mn and Kshs 633.8 mn, respectively, since inception in February 2021.

REITs provide various benefits like tax exemptions, diversified portfolios, and stable long-term profits. However, the continuous deterioration in performance of the Kenyan REITs and restructuring of their business portfolio is hampering major investments that had previously been made. The other general challenges include; i) inadequate comprehension of the investment instrument among investors, ii) prolonged approval processes for REITs creation, iii) high minimum capital requirements of Kshs 100.0 mn for trustees, and, iv) minimum investment amounts set at Kshs 5.0 mn, continue to limit the performance of the Kenyan REITs market.

- Cytonn High Yield Fund (CHYF)

Cytonn High Yield Fund (CHYF) closed the week with an annualized yield of 16.3%, a 0.2%-point increase from 16.1% recorded the previous week. The performance represented a 2.4%-points Year-to-Date (YTD) increase from the 13.9% yield recorded on 1st January 2023, and 0.6%-points Inception-to-Date (ITD) increase from the 15.7% yield. The graph below shows Cytonn High Yield Fund’s performance from November 2019 to 27th October 2023;

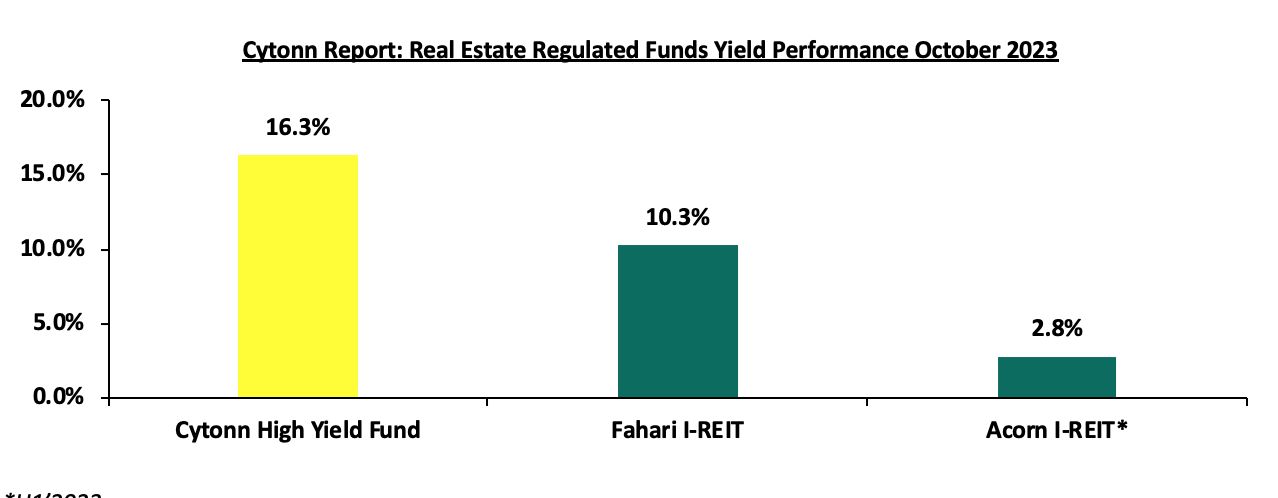

Notably, the CHYF has outperformed other regulated Real Estate funds with an annualized yield of 16.3%, as compared to Fahari I-REIT and Acorn I-REIT with yields of 10.3%, and 2.8% respectively. As such, the higher yields offered by CHYF makes the fund one of the best alternative investment resource in the Real Estate sector. The graph below shows the yield performance of the Regulated Real Estate Funds;

*H1’2023

Source: Cytonn Research

We expect the performance of Kenya’s Real Estate sector to be resilient, supported by; i) continued expansion activities and recovery of the hospitality sector, ii) strategic positioning of Kenya as a regional hub which continues to attract multi-national businesses and organizations into the country, iii) positive accolades awarded to several local and international brands in various award categories such as the World Travel Awards which will continue to boost investor confidence in the sector, iv) government’s continued emphasis on affordable housing, and, v) growing demand for Real Estate supported by positive demographics. However, the sector's optimal performance will be hampered by; i) rising construction costs as a result of inflationary pressures, ii) existing oversupply of physical space in select market segments resulting in slower uptake of new spaces, and iii) limited investor knowledge in REITs coupled with high minimum investment amounts among other factors impeding the growth of the asset class.

Following the release of the H1’2023 results by Kenyan insurance firms, the Cytonn Financial Services Research Team undertook an analysis on the financial performance of the listed insurance companies and the key factors that drove the performance of the sector. In this report, we assess the main trends in the sector and areas that will be crucial for growth and stability going forward, seeking to give a view on which insurance firms are the most attractive and stable for investment. As a result, we shall address the following:

- Insurance Penetration in Kenya,

- Key Themes that Shaped the Insurance Sector in H1’2023

- Industry Highlights and Challenges,

- Performance of The Listed Insurance Sector in H1’2023, and,

- Conclusion & Outlook of the Insurance Sector.

Section I: Insurance Penetration in Kenya

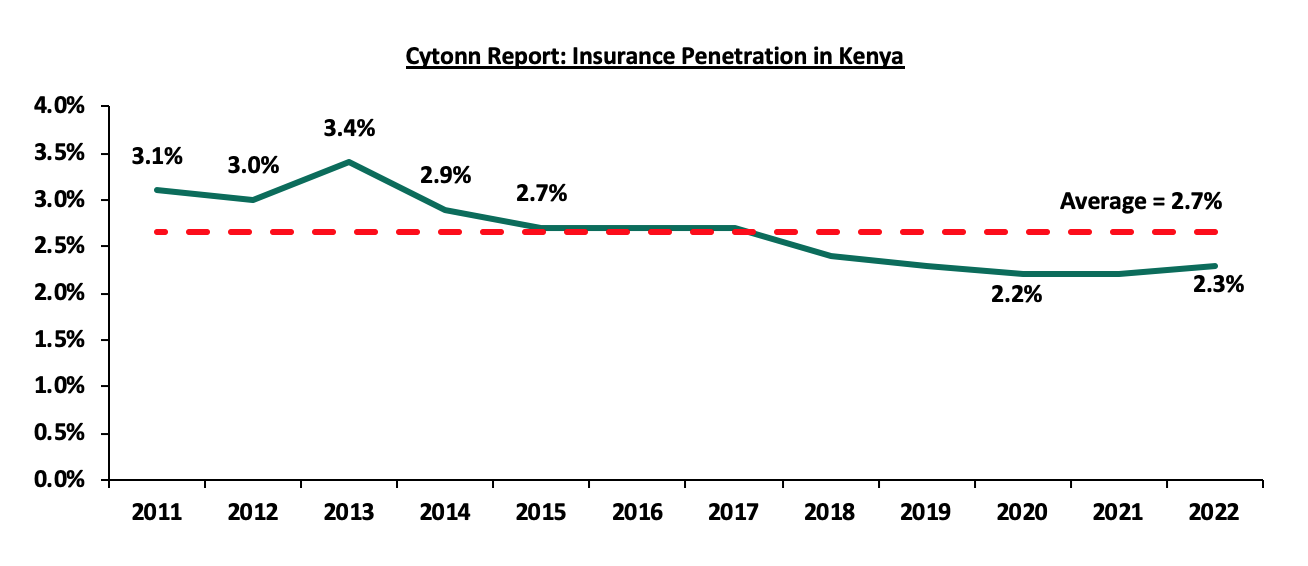

The rate of Insurance penetration in Kenya has remained historically low compared to other major economies, with the insurance penetration coming in at 2.3% as at FY’2022, according to the Kenya National Bureau of Statistics (KNBS) 2023 Economic Survey. The low penetration rate, which is below the global average of 7.0%, according to Swiss RE Institute, is attributable to the fact that insurance uptake is still seen as a luxury and mostly taken when it is necessary or is a regulatory requirement. In addition, a large portion of the Kenya’s work force is in the informal sector, making up approximately 83.0% of the total working population, where there are no strict regulations for taking up insurance plans. Notably, Insurance penetration remained unchanged at 2.3% in 2022, similar to what was recorded in 2021 and 2020, despite the economic recovery that saw an improved business environment. The chart below shows Kenya’s insurance penetration for the last 12 years:

Source: CBK Financial Stability Reports

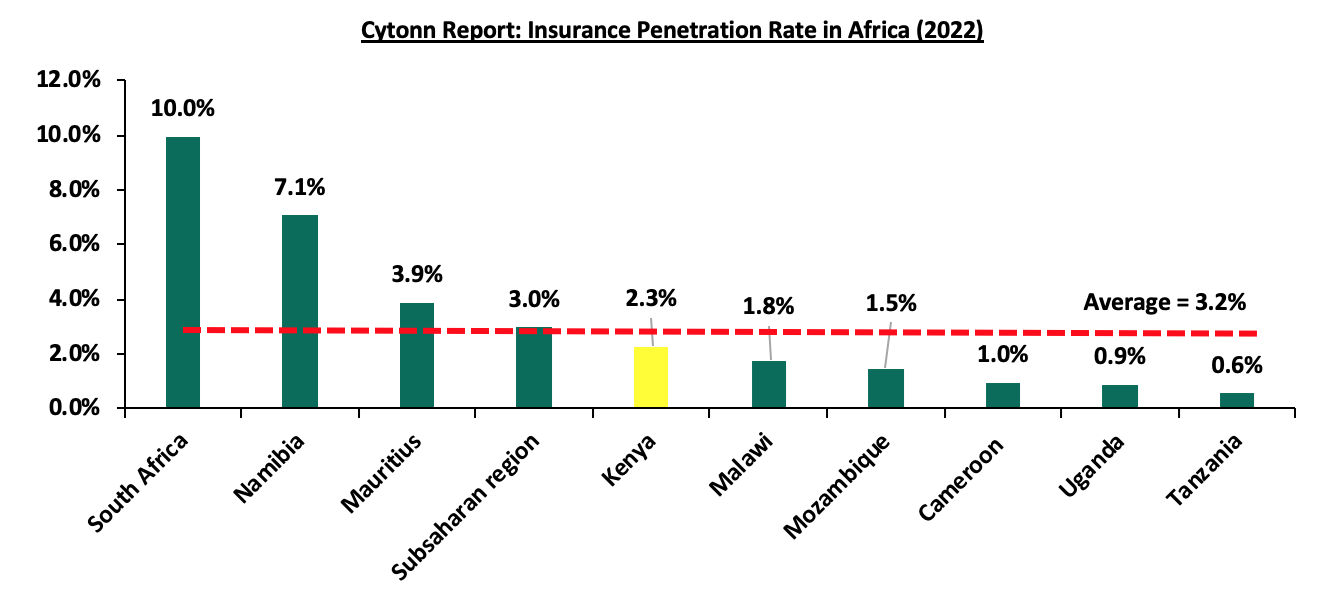

The chart below shows the insurance penetration in other economies across Africa:

Source: Swiss Re, GCR Research, KNBS

Over the period, insurance penetration in Africa has remained low compared to other developed economies, averaging 3.2% in 2022, mainly attributable to lower disposable income in the continent and slow growth of alternative distribution channels such as mobile phones to ensure a wider reach of insurance products to the masses. In addition, insurance products are often not tailored to specific needs of the local population, which can discourage uptake among the population. South Africa remains the leader in insurance penetration in the continent, with a penetration rate of 10.0% in 2022, owing to a mature and highly competitive market, coupled with strong institutions and a sound regulatory environment.

Section II: Key Themes that Shaped the Insurance Sector in H1’2023

In H1’2023, the country witnessed a tough economic environment occasioned by elevated inflationary pressures with the average inflation at 8.5% in H1’2023 compared to 6.3% over a similar period in 2022. The economic growth also slowed by 0.6% points to 5.4% in 2023, from 6.0% recorded in 2022 according to the Kenya National Bureau of Statistics (KNBS). Despite the economic Challenges facing the country, the insurance sector showed resilience registering a 14.8% growth in gross premiums to Kshs 101.5 bn in Q1’2023, from Kshs 88.4 bn in Q1’2022, outpacing the 11.3% growth in insurance claims to Kshs 42.9 bn in Q1’2023, from Kshs 38.5 bn in Q1’2022, according to the Q1’2023 Insurance Regulatory Authority Insurance Industry Report.

The general insurance business contributed 61.6% of the industry’s gross premium income compared to 38.4% contribution by long-term insurance business in Q1’2023. In Q1’2023, gross premiums from the general insurance registered a growth of 15.9% to Kshs 62.5 bn, up from Kshs 53.9 bn recorded over a similar period in 2022. Similarly, gross premiums from the long-term business increased by 12.9% to Kshs 39.0 bn, from Kshs 34.5 bn in Q1’2022. In addition, motor insurance and medical insurance classes of insurance accounted for 61.7% of the gross premium income under the general insurance business, albeit lower than 63.5% recorded in Q1’2022. On the other hand, the largest contributors of gross premiums for long-term insurance business were deposit administration and life assurance classes accounting for 52.3% of gross premiums under this class in Q1’2023, albeit lower than 59.5% recorded in Q1’2022.

Since most of the insurance companies invest in the stock market they were also affected by the 16.1% decline in the NASI in H1’2023, but this was better than the 25.2% decline recorded in H1’2022. However, the index remained in a decline position resulting in the deterioration of the insurance sector’s bottom line as a result of fair value losses in the equities investments. The sector’s allocation to quoted equities continues to reduce, with the proportion of quoted equities to total industry assets declining to 2.4% in H1’2023, from 4.0% in H1’2022.

To help with the penetration and increased efficiency the industry has adopted a number of key measures some among them being:

- Adoption of Alternative Channels: Convenience and efficiency through adoption of alternative channels for both distribution and premium collection such as Bancassurance and improved agency networks,

- Adoption of technology: Advancement in technology and innovation making it possible to make premium payments through mobile phones,

- Product innovation: Infusion of artificial intelligence into insurance client user interface and introduction of parametric insurance products such as flood insurance and livestock insurance covers has contributed to increased uptake of insurance covers, leading to growth in gross premiums which increased by 14.8% to Kshs 101.5 bn in Q1’2023, from Kshs 88.4 bn in Q1’2022, and,

- Diversification of Investments: The sector’s investments income increased significantly by 51.8% to Kshs 17.4 bn in Q1’2023, from Kshs 11.4 bn in Q1’2022, mainly attributable to the 59.9% growth in investment income from the long-term insurance business to Kshs 14.4 bn, from Kshs 9.0 bn in Q1’2022. Notably, the investment income from the general business increased by 21.9% to Kshs 3.0 bn, from Kshs 2.4 bn in Q1’2022.

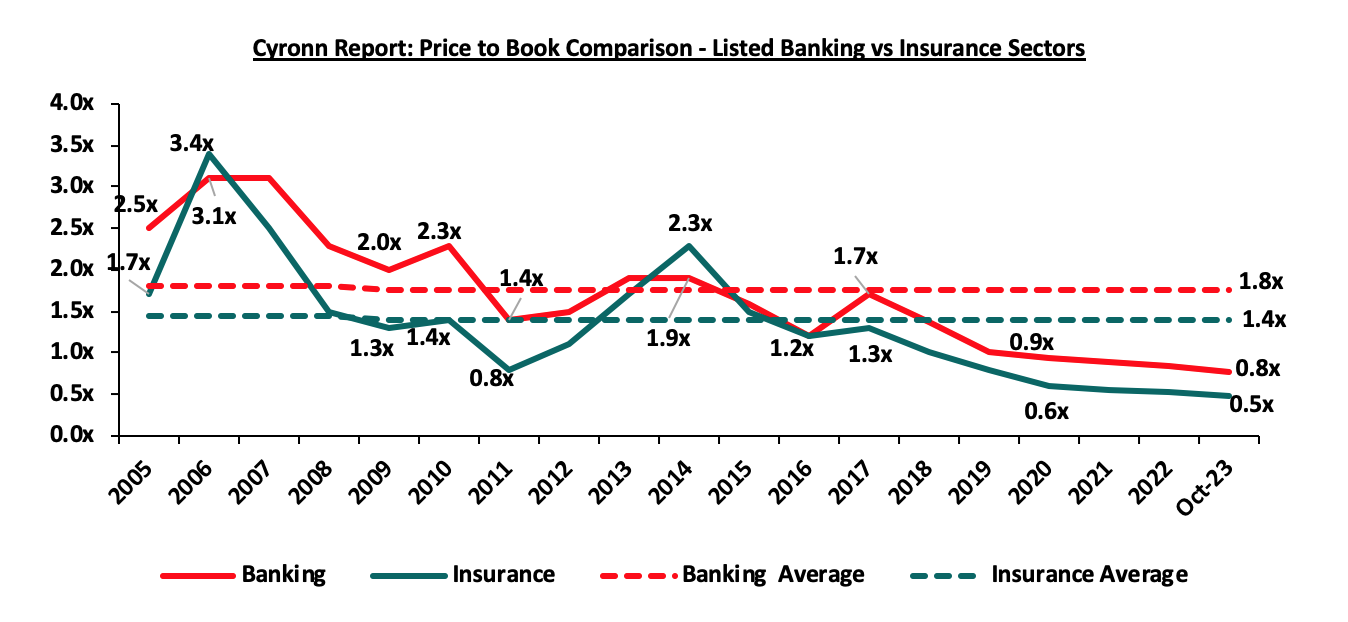

On valuations, listed insurance companies are trading at a price to book (P/Bv) of 0.5x, lower than listed banks at 0.8x, but both are lower than their 17-year historical averages of 1.4x and 1.8x, for the insurance and banking sectors respectively. These two sectors are attractive for long-term investors supported by the strong economic fundamentals. The chart below shows the price to book comparison for Listed Banking and Insurance Sectors:

- Regulation

In the pursuit of fostering a globally competitive financial services sector, the regulatory authority has been diligently implementing regulations to address both long-standing and emerging challenges within the industry. The situation became quite challenging, not only due to the impact of the COVID-19 pandemic but also due to the prevailing economic pressures. This presented a complex balancing act for insurance underwriters, as they needed to maintain prudence in their operations while simultaneously adhering to the established regulations. Regulations used for the insurance sector in Kenya include the Insurance Act Cap 487 and its accompanying schedule and regulations, Retirement Benefits Act Cap 197 and The Companies Act. In H1’2023, regulation remained a key aspect affecting the insurance sector and the key themes in the regulatory environment include;

- IFRS 17 - IFRS 17, the international accounting standard for insurance contracts, aims to establish a framework for how insurance companies should recognize, measure, present, and disclose information about their insurance contracts. The primary goal is to ensure that insurance companies provide accurate and transparent information that effectively represents the nature of these contracts. Given the disruptions caused by the COVID-19 pandemic, the International Accounting Standards Board (IASB), responsible for establishing worldwide financial reporting standards, made the decision to delay the implementation of IFRS 17. However, it's important to note that all the Kenya’s listed insurance companies have already incorporated the provisions of IFRS 17 in their recently released H1’2023 financial results. In doing so, they have also restated their financial statements for FY’2022 to align with this new standard. By replacing, IFRS 4, this new standard is anticipated to bring about significant improvements in the way insurance companies report their financial results. It is designed to provide a deeper and more insightful view of the current and future profitability of insurance contracts. One of its key features is the separation of financial and insurance results in the income statement. This separation will enable a more thorough analysis of the core performance of insurance entities and enhance the comparability of different insurance companies,

- IFRS 9 - IAS 39, Financial Instruments Recognition and Measurement was replaced with IFRS 9, Financial Instruments to address the classification and measurement of financial instruments, impairment, and hedge accounting. The guidelines introduce new classification and measurement especially for financial assets, necessitating insurers to make judgements to determine whether financial investments are measured at amortized cost or fair value, and whether gains and losses are included in the profit or loss or other comprehensive income. The new impairment model under IFRS 9 is based on expected credit losses and subsequently, all financial assets will carry a loss allowance, meaning that insurers will have to provision higher for impairment losses. Many insurance companies have opted to use the temporary exemption from implementation of IFRS 9, by continuing to apply IAS 39, but the temporary exemption expired January 2023. IFRS 9 will enable insurance companies to develop appropriate models for their customer debtors and develop plans that will help them lower their credit risk in the future, and,

- Risk Based Supervision - Risk-Based Supervision, as enforced by the Insurance Regulatory Authority (IRA), involves the implementation of guidelines that compel insurance companies to maintain a capital adequacy ratio of at least 200.0% of the minimum required capital. These regulations further stipulate that insurers should regularly monitor their capital adequacy and solvency margins on a quarterly basis. The primary objective behind this regulatory approach is to ensure that insurance companies remain financially stable, enabling them to operate as a going concern while also delivering satisfactory returns to their shareholders. We expect more mergers within the industry as smaller companies struggle to meet the minimum capital adequacy ratios. We also expect insurance companies to adopt prudential practices in managing and taking on risk and reduction of premium undercutting in the industry as insurers will now have to price risk appropriately.

- Capital Raising, Share Purchase and Consolidation

The move to a risk-based capital adequacy framework presented opportunities for capital raising initiatives mostly by the small players in the sector to shore up their capital and meet compliance measures. With the new capital adequacy assessment framework, capital is likely to be critical to ensuring stability and solvency of the sector to ensure the businesses are a going concern. In October 2022, Allianz announced that it had completed the transaction to acquire a majority stake in Jubilee Holdings Limited’s general insurance business in East Africa. The two companies announced the agreement on September 29, 2020, where Allianz had agreed to acquire the majority shareholding in the short-term general (property and casualty) insurance business operations of Jubilee Holdings. In Kenya, the former Allianz Insurance Company of Kenya and Jubilee General Insurance Company of Kenya merged to operate under the name Jubilee Allianz General Insurance Company of Kenya, with the aim to leverage on the two entities footprints in Africa and create a leading Pan-African financial services group. Consequently, US-based finance and insurance corporation American Insurance Group (AIG) announced its move to dispose of at least Kshs 2.0 bn (USD 13.5 mn) of its majority shareholding in AIG Kenya Insurance to NCBA Group.

- Technology and Innovation

One of the major drivers in the insurance sector is technology and innovation. While the insurance sector was traditionally slow to embrace digital advancements, the outbreak of the COVID-19 pandemic in 2020 compelled the industry to swiftly adopt digital channels for the distribution of insurance products. Consequently, a significant number of insurance companies have leveraged these digital avenues to stimulate growth and enhance insurance accessibility across the nation. Given that the manual handling and assessment of insurance claims is a laborious and imperfect process, the integration of Artificial Intelligence (AI) plays a crucial role in the investigation of claim legitimacy and the detection of fraudulent claims. For instance, Jubilee Holdings introduced a digital virtual assistant that enables clients to access real-time services, including end-to-end insurance product purchases and assistance, all without the need for human intervention.

Section III: Industry Highlights and Challenges

The insurance sector has seen consistent expansion in the past ten years. As a result, we expect that it will continue to achieve gradual growth due to an improving awareness as well as the increased technological advancements which have continued to shape the sector. As such, we expect a continued increase in insurance premiums, which, in turn, will bolster the industry's capacity to maintain profitability.

In H1’2023, the Insurance Regulatory Authority (IRA), in line with their mandate of regulating and promoting development of the insurance sector approved 12 new or repackaged insurance products filed by various insurance companies. In the new products, 2 or 16.7% of the 12 products were bundled products, 3 or 25.0% of the 12 products were medical plans, 1 or 8.3% of the 12 products was micro insurance, 1 or 8.3% of the 12 products was non-linked insurance, 2 or 16.7% of the 12 products were life products, while miscellaneous accounted for 3 or 25.0% of the total new/repackaged products.

Industry Challenges:

- High market competition: One of the major challenges in the insurance sector is the intense competition within the market. Despite the relatively low level of insurance adoption in the country, there are 57 insurance companies all offering similar products. Some insurers have resorted to questionable tactics in their quest for market supremacy, including the practice of premium undercutting. This strategy involves offering clients unrealistically low premiums in an effort to gain a competitive edge and safeguard their market share. Such practices have significantly contributed to underwriting losses in the industry. Although there were initial plans in March 2021 to engage a consultant to review pricing strategies in the industry, these efforts faced resistance from the regulatory authorities. However, discussions regarding pricing remain ongoing, and they take place against the backdrop of a fragile insurance market, where higher premium prices could potentially exacerbate the issue of low insurance adoption,

- Insurance fraud: Insurance Fraud is an intentional deceit performed by an applicant or policyholder for financial advantage. In recent years, there has been an upsurge in fraudulent claims, particularly in medical and motor insurance, with estimates indicating that one in every five medical claims are fraudulent. This is mainly through exaggerating medical costs and hospitals by making patients to undergo unnecessary tests. In FY’2022, 150 fraud instances were reported, with fraudulent motor accident injury claims accounting for 22.0% of the total. Fraudsters also collude with hospitals to make false claims fake surgeries and treatments, while health-care providers overcharge insured patients. The sector has been adopting the use of block chain and artificial intelligence to curb fraud within the sector. Key to note, most companies are also setting up their own assessment centres across the country so as to better determine the actual compensation,

- High loss ratios: Core insurance business performance has been dwindling, mainly attributable to the high loss ratios, which have deteriorated further, following the increase in claims outpacing the increase in premiums. As of Q1’2023, loss ratios under the general insurance business increased by 4.3% points to 72.0%, from 67.7% recorded in Q1’2022, mainly attributable to 16.8% increase in claims to Kshs 21.5 bn, from Kshs 18.4 bn in Q1’2022, that outpaced the 13.2% increase in net premiums to Kshs 42.5 bn, from Kshs 37.6 bn in Q1’2022. However, the loss ratios under the long-term insurance business eased, with the ratio declining to 62.8% as of Q1’2023, from 64.3% in Q1’2022, largely attributable to the 8.7% increase in net premiums to Kshs 34.0 bn, from Kshs 31.3 bn in Q1’2022, which outpaced the 6.3% growth in net claims to Kshs 21.4 bn, from Kshs 20.1 bn in Q1’2022. This situation has been a major concern for the industry as it affects its overall profitability and sustainability. Finding ways to address these high loss ratios is crucial to ensure the long-term health and success of the insurance sector,

- Dwindling trust from insurance consumers: One pressing issue in the insurance industry is the erosion of trust among policyholders and beneficiaries. During the H1’2023, the Insurance Regulatory Authority (IRA) registered 522 complaints in Q1’2023. General insurance business accounted for 79.1% of the complaints whereas 20.9% were made against long-term insurers. The grievances included instances where insurance companies failed to fulfill claim settlements and engaged in persistent negotiations regarding insurance terms, and,

- Regulatory compliance: Regulation on capital requirements has made it difficult for smaller insurance companies to continue operating without increasing their capital or merging in order to raise their capital base. Additionally, some of global regulatory requirements such as implementation of IFRS 17 are costly due to the need to revamping and realigning accounting and actuarial systems.

Section IV: Performance of the Listed Insurance Sector in H1’2023

The table below highlights the performance of the listed insurance sector, showing the performance using several metrics, and the key take-outs of the performance:

|

Cytonn Report: Listed Insurance Companies H1’2023 Earnings and Growth Metrics |

||||||||

|

Insurance Company |

Core EPS Growth |

Insurance Revenue Growth |

Loss ratio |

Expense Ratio |

Combined Ratio |

ROACE |

ROaA |

ROaE |

|

Britam Holdings |

334.5% |

33.8% |

66.1% |

71.4% |

137.5% |

9.7% |

1.0% |

2.0% |

|

CIC Group |

168.2% |

19.9% |

70.6% |

50.4% |

121.1% |

23.2% |

1.4% |

7.7% |

|

Jubilee Holdings |

(47.8%) |

11.4% |

114.5% |

38.5% |

153.0% |

16.5% |

1.1% |

4.3% |

|

Liberty Holdings |

(760.0%) |

(151.2%) |

61.9% |

71.2% |

133.1% |

7.5% |

0.5% |

2.4% |

|

Sanlam Kenya |

(1794.0%) |

(8.8%) |

89.2% |

40.8% |

130.0% |

60.5% |

(0.5%) |

(18.1%) |

|

H1'2023 Weighted Average |

19.8% |

9.7% |

86.6% |

54.2% |

140.8% |

15.9% |

1.0% |

3.1% |

|

H1'2022 Weighted Average |

16.0% |

1.7% |

83.4% |

43.4% |

126.8% |

10.5% |

2.2% |

2.2% |

|

*Market cap weighted as at 27/10/2023 |

||||||||

|

**Market cap weighted as at 09/06/2022 |

||||||||

The key take-outs from the above table include;

- Core EPS growth recorded a weighted growth of 19.8% in H1’2023, compared to a weighted growth of 16.0% in H1’2022. The sustained growth in earnings was attributable to the improved profitability owing to the increased insurance revenue despite the tough operating environment occasioned by the elevated inflationary pressures as well as the depreciation of the Kenyan currency against the dollar,

- The insurance revenue grew at a faster pace of 9.7% in H1’2023, compared to a growth of 1.7% in H1’2022,

- The loss ratio across the sector increased slightly to 86.6% in H1’2023 from 83.4% in H1’2022,

- The expense ratio increased to 54.2% in H1’2023, from 43.4% in H1’2022, owing to an increase in operating expenses, a sign of reduced efficiency,

- The insurance core business still remains unprofitable, with a combined ratio of 140.8% as at H1’2023, compared to 126.8% in H1’2022, and,

- On average, the insurance sector delivered a Return on Average Equity (ROaE) of 3.1%, an increase from a weighted Return on Average Equity of 2.2% in H1’2022.

Based on the Cytonn H1’2023 Insurance Report, we ranked insurance firms from a franchise value and from a future growth opportunity perspective with the former getting a weight of 40.0% and the latter a weight of 60.0%.

For the franchise value ranking, we included the earnings and growth metrics as well as the operating metrics shown in the table below in order to carry out a comprehensive review:

|

Cytonn Report: Listed Insurance Companies H1’2023 Franchise Value Score |

|||||||

|

Insurance Company |

Loss Ratio |

Expense Ratio |

Combined Ratio |

Return on Average Capital Employed |

Tangible Common Ratio |

Franchise Value Score |

Ranking |

|

CIC Group |

70.6% |

50.4% |

121.1% |

23.2% |

17.3% |

17 |

1 |

|

Sanlam |

89.2% |

40.8% |

130.0% |

60.5% |

1.4% |

19 |

2 |

|

Jubilee |

114.5% |

38.5% |

153.0% |

16.5% |

26.0% |

22 |

3 |

|

Britam |

66.1% |

71.4% |

137.5% |

9.7% |

12.9% |

23 |

4 |

|

Liberty |

61.9% |

71.2% |

133.1% |

7.5% |

100.0% |

24 |

5 |

|

*H1’2023 Weighted Average |

86.6% |

54.2% |

140.8% |

15.9% |

24.0% |

|

|

The Intrinsic Valuation is computed through a combination of valuation techniques, with a weighting of 40.0% on Discounted Cash-flow Methods, 35.0% on Residual Income and 25.0% on Relative Valuation. The overall H1’2023 ranking is as shown in the table below:

|

Cytonn Report: Listed Insurance Companies H1’2022 Comprehensive Ranking |

|||||

|

Bank |

Franchise Value Score |

Intrinsic Value Score |

Weighted Score |

H1'2023 Ranking |

H1'2022 Ranking |

|

CIC Group |

1 |

3 |

2.2 |

1 |

5 |

|

Jubilee Holdings |

3 |

2 |

2.4 |

2 |

1 |

|

Liberty Holdings |

5 |

1 |

2.6 |

3 |

2 |

|

Sanlam Kenya |

2 |

4 |

3.2 |

4 |

4 |

|

Britam |

4 |

5 |

4.6 |

5 |

3 |

Major Changes from the H1’2023 Ranking are;

- CIC Group improved to position 1 in H1’2023 from position 5 in H1’2022 driven by an improvement in both franchise and intrinsic scores, attributable to the improvement in the expense ratio to 50.4%, from 51.1%, taking the combined ratio to 121.1%, an improvement from the 122.8% recorded in H1’2022,

- Jubilee Holdings declined to position 2 in H1’2023, from position 1 in H1’2022 mainly due to the declines in both the franchise and intrinsic scores in H1’2022, driven by the deterioration in the loss ratio to 114.5%, from 99.4% in H1’2022., taking the combined ratio to 153.0%, from the 133.0% in H1’2022,

- Britam Holdings declined to position 5 in H1’2023, from position 3 in H1’2022 mainly due to declines in both the franchise and intrinsic scores in H1’2023, driven by the deterioration in the expense ratio to 71.4%, from 48.6% in H1’2022, taking the combined ratio to 137.5%, from the 122.1% in H1’2022, and,

- Liberty declined to position 3 in H1’2023 from position 2 in H1’2022 mainly due to deterioration in both the franchise score and intrinsic value score.

Section V: Conclusion & Outlook of the Insurance Sector

In H1’2023, the insurance sector continued to suffer from low penetration rates which has been worsened by deteriorated business environment emanating from rising interest rates, increased inflationary pressures as well as the persisted currency depreciation. As a result, the level of disposable income among households has decreased. However, the sector continues to undergo transition where traditional models have been disrupted, mainly on the digital transformation, innovation and regulation front, which have positively impacted the outlook. We also expect the insurance sector to maintain the culture of innovation achieved during the pandemic period while maintaining the customer-centricity as the main focus of the sector’s operating model. As a result, we believe that in order to maintain profitability, the insurance industry will need to engage in careful balancing acts. Some of these things the industry can take to grow significantly and raise penetration in the nation include:

- Enhance Operational Efficiency: Insurance companies should focus on streamlining their operations to reduce high expense ratios that have been hampering premium growth. In H1’2023, the weighted average expense ratio remained elevated at 54.2%, from 43.4% in H1’2022, owing to an increase in operating expenses, a sign of reduced efficiency. Efficiency can be achieved by optimizing operating models and leveraging digitalization to expedite processes and cut costs,

- Partnerships and alternative distribution channels: We anticipate that Underwriters will continue forming alliances and expanding their reach through various distribution channels. This may involve collaborating with other financial service providers, such as asset managers who have diversified into offering insurance-linked products. In addition to existing Bancassurance partnerships with banks, insurers can leverage the bank's product distribution network to promote their own insurance offerings. Furthermore, the integration of mobile money payment solutions is projected to remain a growing trend. This is due to the convenience it offers, along with the widespread use of mobile phones in the country,

- Optimization of A Portfolio: To maintain the sector's recovery and achieve profitability, insurance companies should optimize their portfolio by re-evaluating their goods and services. The sale of business divisions deemed to be unproductive can help insurers focus on their core and profitable products while eliminating non-core offers. For instance, in September 2023, AIG Insurance Kenya announced plans to enter into a Kshs 2.0 bn deal with NCBA Group which would see the bank acquire 100% of the issued share capital from the insurer. As insurers focus more on profitable goods, portfolio optimization will eventually include reducing holdings in unprofitable subsidiaries and affiliates and impact underwriters' products,

- Regulations: We also anticipate increased regulation in the sector from the regulatory body and other international players to ensure its solvency and sustainability. Notably, all the listed Insurers have adjusted their insurance contract recognition methods to IFRS 9 and IFRS 17 having restated their financial statements in line with these new reforms. The push by the regulator to have the desired capital adequacy levels will likely see more consolidations as insurers try to meet the capital requirements, especially for small firms. Additionally, there are increased efforts by regulators, governments and policymakers to ensure that Environmental, Social and Governance (ESG) regulations become a necessity in the insurance sector. As such, insurers will have no option but to incorporate ESG and as such, services and products offered by insurers should ensure environmental sustainability, ethics and regulatory compliance and data privacy, and ensuring social responsibility,

- Technology and innovation: The sector will continue experiencing enhanced technological tools and innovations such as Artificial Intelligence and real time data in hyper personalization of insurance marketing so as to use customer information to tailor content, products and services in line with customer preferences. With such tools, insurers will effectively respond to changes in buying behaviours and tailoring products and services to the needs of the customers to ensure their loyalty hence high retention. Firms will also adopt increased inclusion of advancements like smart contracts through block chain that would help eliminate processing costs, reduce insurance fraud and fictitious claims and improve customer satisfaction through efficient claims processing,

- Investment diversification: Insurance companies should prioritize diversifying their investments through channels like pension schemes, unit trusts, fund management, and investment advisory services to enhance their profitability and mitigate potential losses. This strategic shift is crucial, given the rising combined ratios that have led to insurers experiencing losses in their core operations, where underwriting expenses and claims have been increasing relative the realised premium increases. For instance, As of Q1’2023, loss ratios under the general insurance business increased by 4.3% points to 72.0%, from 67.7% recorded in Q1’2022, mainly attributable to 16.8% increase in claims to Kshs 21.5 bn, from Kshs 18.4 bn in Q1’2022, that outpaced the 13.2% increase in net premiums to Kshs 42.5 bn, from Kshs 37.6 bn in Q1’2022, and,

- Insurance awareness campaigns: Insufficient knowledge on insurance products and their importance continues to persist, massively contributing to the low insurance penetration. Insurance is still largely assumed as regulatory compliance, rather than a necessity. The regulators, insurers, and other stakeholders should enhance insurance awareness campaigns to increase understanding of insurance products. According to a survey commissioned by the Association of Kenya Insurers (AKI), the second largest contributor to low insurance uptake at 27.0% is a lack of knowledge of the various insurance products and their benefits. As such, there is a lot of headroom for insurers to educate, repackage, and tailor their products to different potential clients.

To read the H1’2023 Insurance Report, please download it here

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma