Jan 6, 2019

Economic Growth:

The country's Gross Domestic Product (GDP), adjusted for inflation, increased in 2018 having expanded by 5.7% in Q1’2018, 6.3% in Q2’2018 and 6.0% in Q3’2018 to record an average growth of 6.0% for the 3 quarters compared to an average growth of 4.7% over the same period in 2017. The improved growth has been against a backdrop of a stable macroeconomic environment, driven by:

- A recovery in agriculture, which saw the sector record an average growth of 5.3% for the first 3 quarters of 2018, due to improved weather conditions. In terms of sectoral contribution, agriculture remained the highest contributor averaging 22.4% over the same period,

- Improved business and consumer confidence, evidenced by the Stanbic Bank’s Monthly Purchasing Managers Index (PMI), which averaged 54.3 in the 11-months to November 2018, a rise from 46.0, recorded in a similar period in 2017. Key to note, a PMI reading of above 50 indicates improvements in the business environment, while a reading below 50 indicates a worsening outlook. The improvement in the business environment has also been facilitated by the improved ease of doing business, which saw Kenya’s rank improve by 19 positions to #61 from #80 as per the World Bank Doing Business Report 2019 as highlighted in our Analysis of Kenya’s Doing Business Environment. This was mainly driven by improvements in protection of minority investors, access to credit, improved property registration and insolvency resolution, and,

- Increased output in the real estate, manufacturing, and wholesale & retail trade sectors, which grew by 5.8%, 3.2% and 6.8%, respectively, and favorable weather conditions that positively affected output from agricultural and hydroelectricity activities.

Analysis by sector showed that there was accelerated growth in the manufacturing sector, though its contribution to GDP recorded an average of 10.0% in the first 3 quarters of 2018. This is despite the Kenyan Government singling it out as one of the key pillars to drive the economy in the Big 4 Agenda. The sector’s contribution is still way below the government’s target of increasing it to 15.0% of GDP by 2022, which is expected to increase manufacturing sector jobs by more than 800,000 per annum over the next four years.

Kenya Shilling:

The Kenya Shilling gained 1.4% against the US Dollar to close at 101.8 in 2018 compared to 103.2 at the end of 2017; the Kenya Shilling was the only major African currency, which appreciated against the dollar. In our view, the shilling should remain relatively stable to the dollar in the short term, supported by:

- The narrowing in the current account deficit to 5.3% in the 12 months to September 2018, compared to 6.5% in September 2017. The narrowing of the current account deficit is largely due to increased exports of tea and horticulture, increased diaspora remittances, strong receipts from tourism, and lower imports of food and SGR-related equipment relative to 2017.

- Inflows from principal exports, which include coffee, tea, and horticulture, which increased by 5.2% for the first 9 months of 2018 to Kshs. 209.0 bn from Kshs. 199.0 bn over the same period in 2017,

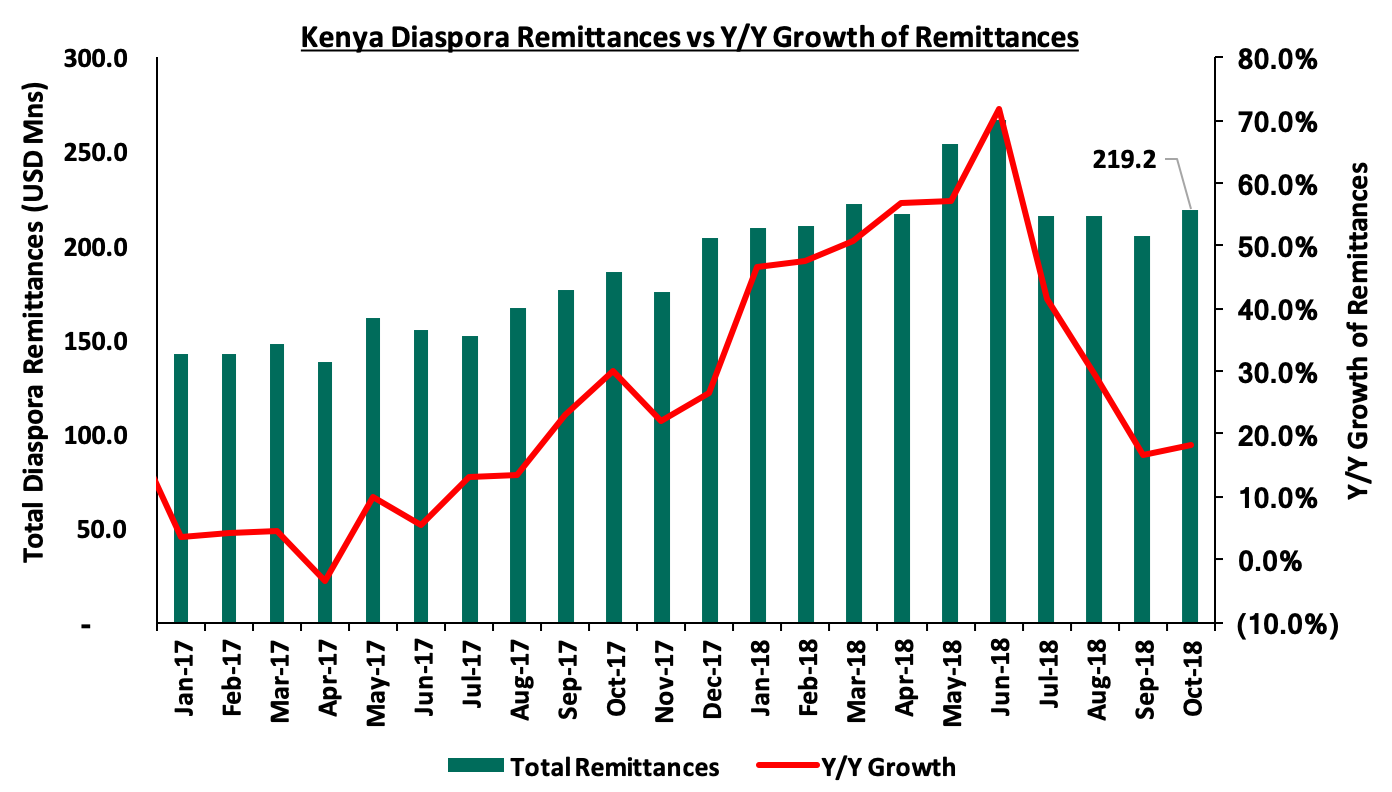

- Improving diaspora remittances, which increased by 42.5% to USD 2.2 bn during the first 10 months of 2018 from USD 1.6 bn during the same period in 2017, with the largest contributor being North America at USD 1.2 bn attributed to; (a) recovery of the global economy, (b) increased uptake of financial products by the diaspora due to financial services firms, particularly banks, targeting the diaspora, and (c) new partnerships between international money remittance providers and local commercial banks making the process more convenient, and,

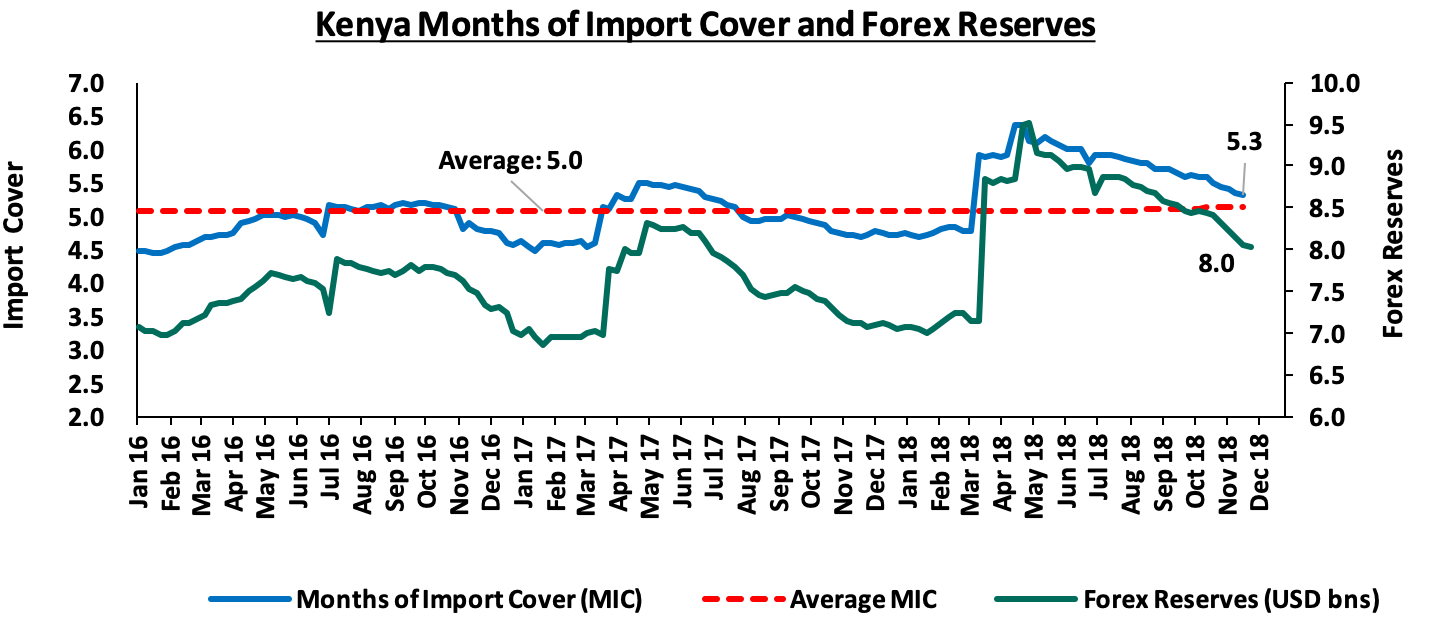

- High forex reserves, which currently stand at USD 8.0 bn (5.3 months of import cover) continue to provide adequate cover, and a buffer against short-term shocks in the foreign exchange market.

Inflation:

The inflation rate for the month of December 2018 rose to 5.7% from 5.6% recorded in November bringing the 2018 average to 4.7% compared to the 2017 average of 8.0%. Going forward, overall inflation is expected to remain within the target range (of 2.5%- 7.5%) in the near term, mainly due to expected lower food prices as a result of favorable weather conditions, the decline in international oil prices, and the recent downward revision in electricity tariffs. The recent excise tax adjustment on voice calls and internet services is expected to have a marginal impact on inflation.

Monetary Policy:

The Monetary Policy Committee lowered the Central Bank Rate (CBR) twice, in the 6 meetings held in 2018 in order to support economic activity, citing that economic output was below its potential level, and there was room for further accommodative monetary policy. During their meeting in March 2018, the MPC lowered the CBR to 9.5% from the earlier 10.0% that had been set in September 2016. The MPC later lowered the CBR by another 50 bps during their July 2018 meeting to 9.0%, from the 9.5% set in March 2018.

2018 Highlights:

- The Kenyan National Treasury released the fiscal year 2018/19 national budget in June 2018. Below were some of the key highlights

Amounts in Kshs trillions unless stated otherwise

|

Comparison of 2017/18 and 2018/19 Fiscal Year Budgets |

|||||

|

|

2018/19 |

% change 2017/18 to 2018/19 |

2017/18 |

% change 2016/17 to 2017/18 |

2016/17 |

|

Revenue |

1.9 |

14.5% |

1.7 |

9.6% |

1.5 |

|

Recurrent expenditure |

1.5 |

7.7% |

1.4 |

13.3% |

1.2 |

|

Development expenditure |

0.6 |

7.8% |

0.6 |

(27.3%) |

0.8 |

|

County governments |

0.4 |

7.3% |

0.4 |

16.4% |

0.3 |

|

Total expenditure |

2.5 |

7.7% |

2.3 |

(0.2%) |

2.3 |

|

Deficit as % of GDP |

(5.7%) |

1.5% |

(7.2%) |

1.9% |

(9.1%) |

|

Net foreign borrowing |

0.3 |

(11.2%) |

0.3 |

(30.3%) |

0.5 |

|

Net domestic borrowing |

0.3 |

(8.6%) |

0.3 |

(14.7%) |

0.3 |

|

Total borrowing |

0.6 |

10.0% |

0.6 |

(23.6%) |

0.8 |

Key take-outs from the table:

- Total expenditure in the fiscal year 2018/2019 was set to increase by 7.7%, to Kshs 2.5 tn from Kshs 2.3 tn in the fiscal year 2017/18,

- Development expenditure was set to increase at a slightly faster rate than recurrent expenditure; with the latter increasing by 7.8% to Kshs 1.5 tn from Kshs 1.4 tn, while development expenditure increased by 7.8% to Kshs 625.0 bn from Kshs 579.6 bn in FY 2017/18,

- The budget deficit was projected to decline to 5.7% of GDP from an estimated 7.2% of GDP in the FY 2017/18; this in line with the International Monetary Fund’s (IMF’s) recommendation, in a bid to reduce Kenya’s public debt requirements,

- The total borrowing requirement to plug in the deficit declined to Kshs 558.9 bn from Kshs 620.8 bn, in a bid to reduce Kenya’s public debt burden which was estimated at 55.6% of GDP as at 2017 by the IMF, 5.6% above the East African Community (EAC) Monetary Union Protocol, the World Bank Country Policy and Institutional Assessment Index, and the IMF threshold of 50.0%, but well below the 74.0% mark considered a signal for debt unsustainability, and,

- Debt financing of the 2018/19 budget was split 51:49 between foreign and domestic borrowing, with the foreign and domestic debt being estimated at Kshs 287.0 billion (equivalent to 3.0% of GDP) and Kshs 271.9 billion (equivalent to 2.8% of GDP), respectively.

- The National Assembly convened for special parliamentary sittings held on 18th September and 20th September to discuss the President’s reservations against the Finance Bill through his memorandum. All the proposals as per the President’s memorandum were tabled in parliament and passed despite a chaotic sitting, after which the president assented to the Finance Bill 2018 on 21st September 2018. We covered a detailed analysis of this in our Cytonn Weekly #36/2018,

- The International Monetary Fund (IMF) paid a visit to Kenya where discussions were held with the Kenyan Government on the second review under a precautionary Stand-By Arrangement (SBA), which was extended to Kenya on 14th March 2016. For more information, see our Cytonn Weekly #30/2018. The second review however was not completed, leading to the expiry of the precautionary stand-by facility granted to Kenya on 14th September 2018,

- According to the Stanbic Bank’s Monthly Purchasing Manager’s Index (PMI), the business environment in the country slowed to a year low in November 2018. The seasonally adjusted PMI dropped to 53.1 in November from 54.0 in October. The index score has however improved generally during the year to average at 54.3 in the 11-months to November 2018, a rise from 46.0, recorded in a similar period in 2017. A PMI reading of above 50 indicates improvements in the business environment, while a reading below 50 indicates a worsening outlook. Firms reported growth in value of outputs due to the continued rise in new orders, which rose for the 9th consecutive month. This was despite high input costs attributed to raw material shortages. In response to increased output requirements, firms also raised their staffing levels during the month though at a modest rate. The private sector has remained resilient as the PMI is still above 50.

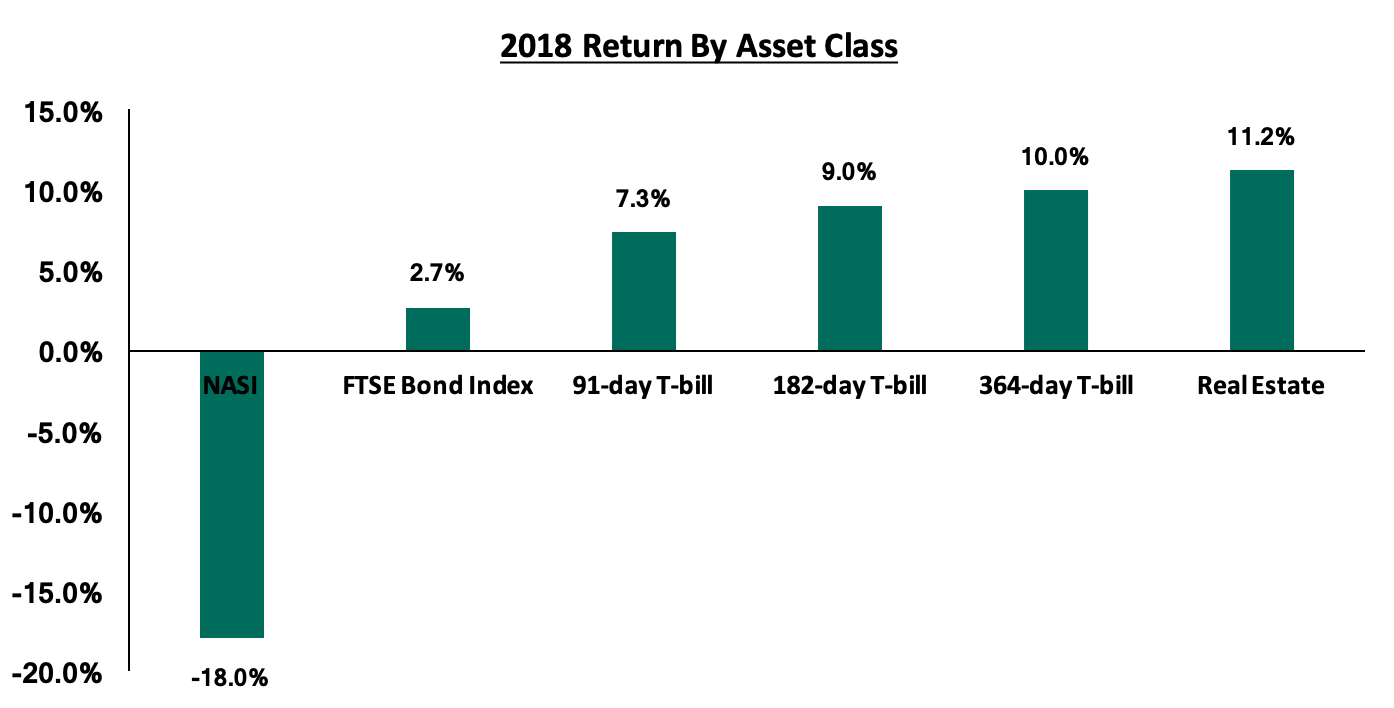

The graph below shows the summary of returns by asset class in 2018 (T- Bonds, T-Bills and Equities). The best performing asset in 2018 was Real Estate with returns of 11.2% followed by government bills with the 364-day, 182-day, and 91-day T-bills recording yields of 10.0%, 9.0% and 7.0% respectively. Investors continue to diversify their portfolio following the poor performance in the equities market as evidenced by the decline in NASI of 18%;

The table below shows the macro-economic indicators that we track, indicating our expectations for each variable at the beginning of 2018 versus the actual experience

|

Macro-Economic Indicators |

2018 Expectations at Beginning of Year |

Outlook - Beginning of Year |

2018 Experience |

Effect |

|

Government Borrowing |

We expected the government to come under pressure to borrow as it was well behind both domestic and foreign borrowing targets for FY 2017/18, and KRA was unlikely to meet its collection target due to expected suppressed corporate earnings in 2017 |

Negative |

i. The government surpassed its domestic borrowing target for the 2017/18 fiscal year, having borrowed Kshs 390.2 bn against a target of 297.6 bn |

Positive |

|

Exchange Rate |

Currency was projected to range between Kshs 102.0 and Kshs 107.0 against the USD in 2018. With the possible widening of the current account deficit being a possible point of concern, we expected the CBK to continue to support the Shilling in the short term through its sufficient reserves of USD 8.1 bn (equivalent to 5.3-months of import cover) |

Neutral |

The Kenya Shilling gained 1.4% against the US Dollar to close at 101.8 in 2018 compared to 103.2 at the end of 2017, and ranging between 100.0 and 103.4. |

Positive |

|

Interest Rates |

We expected upward pressure on interest rates, especially in the first half of the year, as the government fell behind its borrowing targets for the fiscal year. However, with the Banking (Amendment) Act, 2015, we did not expect much action by MPC with the CBR which had remained at 10.0% throughout 2017 |

Neutral |

The Monetary Policy Committee lowered the Central Bank Rate (CBR) twice, in the 6 meetings held in order to support economic activity; During their meeting in March 2018, the MPC lowered the CBR to 9.5% from the earlier 10.0% that had been set in September 2016. The MPC later lowered the CBR by another 50 bps during their July 2018 meeting to 9.0%, from the 9.5% set in March 2018 In their last meeting on 27th November 2018 they retained the CBR at 9.0 citing that inflation expectations remained well anchored within the target range, and that the economy was operating close to its potential |

Neutral |

|

Inflation |

Inflation was expected to average 7.5% compared to 8.0% last year |

Positive |

The inflation rate for the month of December 2018 rose to 5.7% from 5.6% recorded in November bringing the 2018 average to 4.7% (in line with the government’s target of 2.5% to 7.5%) compared to the 2017 average of 8.0%. |

Positive |

|

GDP |

GDP growth was projected to come in at between 5.4% - 5.6% |

Positive |

Kenya’s economy expanded in 2018 by 5.7% in Q1’2018, 6.3% in Q2’2018 and 6.0% in Q3’2018 to record an average growth of 6.0% for the 3 quarters compared to an average growth of 4.7% over the same period in 2017 |

Positive |

|

Investor Sentiment |

Investor sentiment expected to improve in 2018 given the now settling operating environment after conclusion of the 2017 elections |

Positive |

The Kenya Eurobond yields have been increasing, with the yields on the 2014 Eurobond issue rising by 220 bps and 230 bps YTD for the 5-year and 10-year Eurobonds, while the yields on the 10-year and 30-year Eurobonds issued in 2018 have risen by 170 bps and 150 bps, respectively, since the issue date. There has also been increased sell-offs by foreign equity investors amid fears of global economic slowdown, coupled with rising US Treasury yields. |

Neutral |

|

Security |

Security was expected to be maintained in 2018, especially given that the elections were concluded and the USA lifted its travel warning for Kenya, placing it in the 2nd highest tier of its new 4-level advisory program, indicating positive sentiments on security from the international community |

Positive |

The political climate in the country has eased, compared to 2017 with security maintained and business picking up. Kenya now has direct flights to and from the USA, a signal of improving security in the country |

Positive |

Out of the seven metrics that we track, five had a positive effect while two had a neutral effect, compared to the beginning of the year where four had a positive outlook, two had a neutral outlook and one factor had a negative outlook. In conclusion, macroeconomic fundamentals remained positive during the year because of an improved business environment created through political goodwill and improved security in the country.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma