Jun 30, 2019

During the first half of 2019, we tracked Kenya GDP growth projections for 2019 released by 16 organizations, that comprised of research houses, global agencies, and government organizations. The average GDP growth, including Cytonn’s 2019 growth estimate of 5.8%, came in at 5.8%, unchanged from average projections released in Q1’2019. The common view is that GDP growth will remain stable in 2019, from a growth of 6.3% in 2018, the fastest economic growth since the 8.4% recorded in 2010. Economic growth is expected to be driven by:

- Stable growth in the agriculture sector on the back of favorable weather conditions despite delayed onset of the long rains in most parts of the country,

- Implementation of the Big 4 Agenda projects by the Kenyan Government, and,

- Recovery in the business environment as evidenced by the Stanbic Bank Monthly Purchasing Manager’s Index (PMI), which rose to 51.3 in May from 49.3 recorded in April, an indication of improving business conditions.

Below is a table showing average projected GDP growth for Kenya in 2019; noteworthy being that the highest projection is by the Central Bank of Kenya at 6.3%. We shall be updating this table should projections change and shall highlight who had the most accurate projection at the end of the year.

|

Kenya 2019 Annual GDP Growth Outlook |

|||

|

No. |

|

Q1'2019 |

Q2'2019 |

|

1. |

Central Bank of Kenya |

6.3% |

6.3% |

|

2. |

Citigroup Global Markets |

6.1% |

6.1% |

|

3. |

African Development Bank (AfDB) |

6.0% |

6.0% |

|

4. |

PNB Paribas |

6.0% |

6.0% |

|

5. |

UK HSBC |

6.0% |

6.0% |

|

6. |

Euromonitor International |

5.9% |

5.9% |

|

7. |

International Monetary Fund (IMF) |

6.1% |

5.8% |

|

8. |

Cytonn Investments Management Plc |

5.8% |

5.8% |

|

9. |

FocusEconomics |

5.8% |

5.8% |

|

10. |

World Bank |

5.8% |

5.7% |

|

11. |

JPMorgan |

5.7% |

5.7% |

|

12. |

Euler Hermes |

5.7% |

5.7% |

|

13. |

Oxford Economics |

5.6% |

5.6% |

|

14. |

Standard Chartered |

5.6% |

5.6% |

|

15. |

Capital Economics |

5.5% |

5.5% |

|

16. |

Fitch Solutions |

5.2% |

5.2% |

|

|

Average |

5.8% |

5.8% |

The Kenya Shilling:

The Kenya Shilling has depreciated marginally against the US Dollar by 0.5% in H1’2019, to close at Kshs 102.3, from Kshs 101.8 at the end of December 2018, mainly driven by increased dollar demand from oil importers. This week, the Kenya Shilling depreciated marginally by 0.4% against the dollar to close at Kshs 102.3, from Kshs 101.9 the previous week, due to end-month demand from the energy and manufacturing sector exceeding dollar inflows from remittances. In our view, the shilling should remain relatively stable to the dollar in the short term, supported by:

- The narrowing of the current account deficit with data on balance of payments indicating continued narrowing to 4.5% of GDP in the 12-months to April 2019, from 5.5% recorded in April 2018. The decline has been attributed to the resilient performance of exports particularly horticulture and coffee, strong diaspora remittances, and higher receipts from tourism and transport services. Growth of imports also slowed mainly due to lower imports of food and SGR construction equipment,

- Improving diaspora remittances, which have increased cumulatively by 3.8% in May 2019 to USD 1.2 bn, from USD 1.1 bn recorded in a similar period of review in 2018. The rise is due to:

- Increased uptake of financial products by the diaspora due to financial services firms, particularly banks, targeting the diaspora, and,

- New partnerships between international money remittance providers and local commercial banks making the process more convenient,

- CBK’s supportive activities in the money market, such as repurchase agreements and selling of dollars, and,

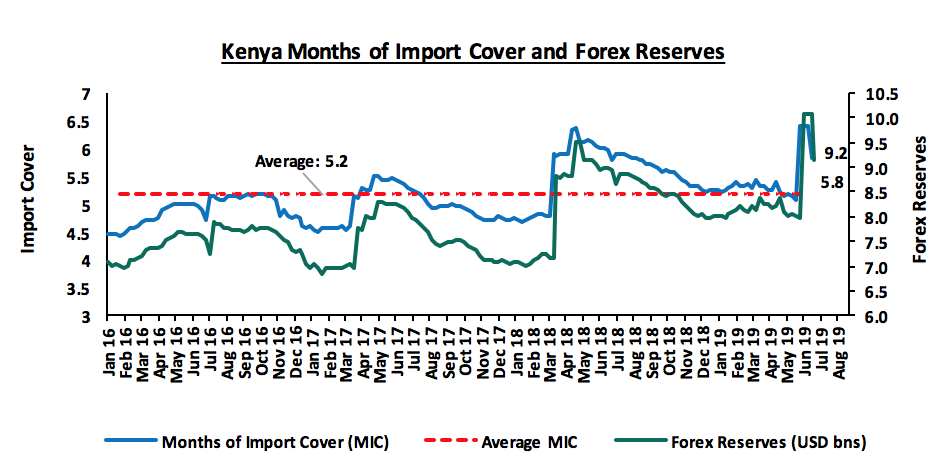

- High levels of forex reserves, currently at USD 9.2 bn (equivalent to 5.8-months of import cover), above the statutory requirement of maintaining at least 4-months of import cover, and the EAC region’s convergence criteria of 4.5-months of import cover.

Inflation:

Inflation:

The average inflation rate increased to an average of 5.2% in H1’2019, as compared to 4.3% in H1’2018. June’s inflation rate rose to 5.7% from 5.5% in May. Y/Y inflation in June 2019 rose mainly due to the base effect and a rise in the transport index, which has a weight of 8.7%, with petrol prices having increased by 5.6% to Kshs 115.8 in June 2019, from Kshs 109.7 per litre in June 2018, while diesel recorded a 1.0% rise to Kshs 105.6, from Kshs 104.6 per litre in the same period. M/M inflation in June declined mainly due to a 1.6% decline in the food and non-alcoholic beverage index owing to favorable weather conditions that led to increased food production and subsequently reduced food prices for various commodities. The inflation rate in June was slightly below our expectations of between 5.8% - 6.2%, which we expected to be driven by a base effect, as well as increases in the transport index, as highlighted in our Cytonn Weekly #25/2019.

|

Broad Commodity Group |

Price change m/m (June-19/May-19) |

Price change y/y (June-19/June-18) |

Reason |

|

Food & Non-Alcoholic Beverages |

(1.6%) |

7.0% |

The m/m decline was due to favorable weather conditions, which led to lower prices for some commodities. |

|

Transport Cost |

0.3% |

11.0% |

The m/m rise was mainly on account of increase in pump prices of petrol and diesel. |

|

Housing, Water, Electricity, Gas and other Fuels |

0.1% |

4.1% |

The m/m rise was as a result of higher costs of house rents which outweighed drops the cost of electricity and cooking fuels. |

|

Overall Inflation |

(0.7%) |

1.4% |

The m/m decline was due to a 1.6% decline in the food index which has a CPI weight of 36.0% |

Monetary Policy:

The Monetary Policy Committee (MPC) met three times in H1’2019, on 28th January 2019, 27th March 2019 and 27th May 2019. In the three meetings, the MPC retained the prevailing monetary policy stance leaving the Central Bank Rate (CBR) unchanged at 9.0%, which was in line with our expectations, citing that inflation expectations remained well anchored within the target range and that the economy was operating close to its potential as evidenced by (i) inflation remained within the 2.5% - 7.5%, target during the review period, (ii) stability in the foreign exchange market and, and (iii) improving private sector credit growth, coming in at 4.9% in the 12-months to April, compared to 4.3% in the 12-months to March, with strong growth being observed in the manufacturing sector (7.9%); trade (8.4%); finance and insurance (13.3%); and consumer durables (16.4%).

As such, the MPC concluded that the current policy stance was still appropriate, but noted that there was a need to remain vigilant on possible spillovers of recent food and fuel price increases. We expect monetary policy to remain relatively stable in 2019, as the CBK monitors Kenya’s inflation rate and the currency.

Half-Year Highlights:

- The Kenya National Bureau of Statistics (KNBS) released the Economic Survey 2019 indicating that the economy had expanded by 6.3% in 2018 from 4.9% recorded in 2017. This was the fastest economic growth since the 8.4% recorded in 2010, and above the 5-year average GDP growth rate of 5.6%. The key drivers of this growth included; (i) A rebound recorded in the agriculture sector, which recorded a growth of 6.4% in 2018 from a revised growth of 1.9% in 2017, with growth mainly driven by marked improvement in crops and animal production anchored by favorable weather conditions, and (ii) Growth in the manufacturing sector was robust in 2018 recording a 4.2% growth, up from the 0.5% growth recorded in 2017. Contribution of the manufacturing sector to total GDP however declined slightly to 9.6% from 9.8% in 2017. For more information, see our Cytonn Weekly #17/2019 and our Kenya 2018 GDP Growth and Outlook Note,

- The Kenya National Bureau of Statistics (KNBS) released the Gross County Product (GCP), which includes a geographic breakdown of Kenya’s Gross Domestic Product (GDP), giving an estimate of the size and structure of county economies. According to the report, the average contribution per county to gross value added over the period 2013-2017 was approximately 2.1%, with Nairobi having the highest contribution at 21.7%, followed by Nakuru and Kiambu at 6.1% and 5.5%, respectively. Isiolo had the lowest contribution coming in at 0.2%, for the same period under review. For more information, see our Cytonn Weekly #07/2019,

- The National Treasury released the 2019/2020 fiscal year (FY) budget on 13th June 2019. According to the budget summary, total revenue collected is expected to increase by 14.2% to Kshs 2.1 tn from the Kshs 1.9 tn as per the revised FY’2018/2019 revised Budget, mainly driven by a 12.2% rise in ordinary revenue to Kshs 1.9 tn from an estimated Kshs 1.7 tn in the revised FY’2018/2019 budget. Total expenditure is set to increase by 10.1% to Kshs 2.8 tn from Kshs 2.5 tn as per the revised FY’2018/19 Budget. The fiscal deficit is projected at Kshs 607.8 bn (5.6% GDP), which will be financed through Kshs 324.3 bn in terms of external financing, domestic borrowing of Kshs 289.2 bn and other domestic receipts worth Kshs 5.7 bn. For more information see Cytonn Weekly #24/2019 and our FY 2019/20 Pre-Budget Discussion Note, and,

- Kenya issued its 3rd Eurobond, raising USD 2.1 bn (Kshs 210.0 bn) through a dual-tranche Eurobond of 7-year and 12-year tenors, value dated 15th May 2019. A longer-term issuance would have been more preferable, though it comes at a trade-off on the yields as investors would demand a higher risk premium to compensate for the risk in tandem with the repayment period of the loan. The Eurobond will be listed on the London Stock Exchange (LSE). The issue was 4.5x oversubscribed attracting orders worth USD 9.5 bn. The Eurobond was priced at 7.0% for the 7-year tenor and 8.0% for the 12-year tenor. For more information, see our Cytonn Weekly #20/2019.

Macroeconomic Indicators Table:

The table below summarizes the various macroeconomic indicators, the actual H1’2019 experience, the impact of the same, and our expectations going forward

|

Macro-Economic & Business Environment Outlook |

|||

|

Macro-Economic Indicators |

YTD 2019 Experience and Outlook Going Forward |

Outlook at the Beginning of the Year |

Current outlook |

|

Government Borrowing |

• We still maintain our expectations of KRA not achieving their revenue targets having been raised by 14.2% in the FY’2019/2020 budget to Kshs 2.1 tn from the Kshs 1.9 tn. As per the Q3’2018/2019 Budget outturn, the Kenya Revenue Authority (KRA) had only managed to raise Kshs 1.2 tn against a target of Kshs 1.3 tn representing 91.5% of the targeted revenue collection and it is doubtful that it will meet its target. This is expected to result in further borrowing from the domestic market to plug in the deficit, which coupled with heavy maturities might lead to pressure on domestic borrowing • We also remain negative due to the ballooning public debt, as well as the maturity profile of the newly acquired foreign debt as it is relatively short, which raises maturity concentration risk as the country will be in a continuous state of maturing obligations between 2024 and 2028 |

Negative |

Negative |

|

Exchange Rate |

• The Kenya Shilling is expected to remain stable against the US Dollar in the range Kshs 101.0-Kshs 104.0 against the USD in 2019, with continued support from the CBK in the short term through its sufficient reserves currently at an all-time high of USD 10.1 bn (equivalent to 6.4-months of import cover) |

Neutral |

Neutral |

|

Interest Rates |

• The interest rate environment has remained stable in 2019, with the CBR having been retained at 9.0% in the 3 MPC meetings held in 2019. With the heavy domestic maturities in 2019, we expect slight upward pressure on interest rates going forward, as the government tries to meet its domestic borrowing targets for the 2019/2020 fiscal year |

Neutral |

Neutral |

|

Inflation |

• Inflation is expected to remain within the government target range of 2.5% - 7.5%. Risks are however abound in the near-term, arising from the late onset of the traditionally long rains season which has disrupted food supply leading to a flare in food inflation, coupled with the continued rise in global fuel prices |

Positive |

Positive |

|

GDP |

• The country's Gross Domestic Product (GDP), adjusted for inflation, rebounded in 2018 having expanded by 6.3% in 2018 from 4.9% recorded in 2017. This was the fastest economic growth since the 8.4% recorded in 2010, and above the 5-year average GDP growth rate of 5.4% • GDP growth is projected to range between 5.7%-5.9% in 2019, lower than the 6.3% growth in 2018, but higher than the 5-year historical average of 5.4% |

Positive |

Positive |

|

Investor Sentiment |

• Eurobond yields have been on a declining trend YTD. An improvement was also recorded in foreign inflows in the capital market to a net buying position of USD 17.7 mn in H1’2019 from a net selling position of USD 93.4 mn in Q4’2018, an indication of improved investor sentiments • We expect improved foreign inflows from the negative position in 2018, mainly supported by long term investors who enter the market looking to take advantage of the current cheap valuations in select sections of the market |

Neutral |

Neutral |

|

Security |

• Security is expected to be upheld in 2019, given that the political climate in the country has eased. Despite the recent terror attack experienced during the first half of 2019, Kenya was spared from travel advisories, evidence of the international community’s confidence in the country’s security position. |

Positive |

Positive |

Of the 7 indicators we track, 3 are positive, 3 are neutral and 1 is negative. The outlook of the 7 indicators has remained unchanged from the beginning of the year. From this, we maintain our positive outlook on the 2019 macroeconomic environment supported by expectations for strong economic growth at between 5.7%-5.9%, a stable currency, inflation rates within the government’s target, and stable interest rates in 2019.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma