Sep 29, 2019

Following the release of H1’2019 results by Kenyan banks, the Cytonn Financial Services Research Team undertook an analysis on the financial performance of the listed banks and identified the key factors that drove the performance of the sector. In this report, we assess the key factors that influenced the performance of the banking sector in the first half of 2019, the key trends in the sector, the challenges banks faced, and areas that will be crucial for growth and stability of the banking sector going forward. As a result, we shall address the following:

- Key Themes that Shaped the Banking Sector in H1’2019;

- Performance of the Banking Sector in H1’2019; and,

- Outlook and Focus Areas of the Banking Sector Players Going Forward.

Section I: Key Themes that Shaped the Banking Sector in H1’2019:

The first half of 2019 has been characterized by consolidation activity in the banking sector involving some of the major players in the industry, among them KCB Group which acquired National Bank, NIC Group which merged with CBA Group and Equity Group which is set to acquire a controlling equity stake in Commercial Bank of Congo (BCDC) with the aim of merging the business with its existing subsidiary in DRC and is currently rumoured to be looking at acquiring HF Group. We also saw banks continue to diversify their revenue sources through venturing into fee businesses like bancassurance, brokerage, and fleet management, coupled with increased transactional income as customers adopt alternative channels of transactions. Thus, our report is themed “Consolidation and Revenue Diversification to Drive Growth in the Kenyan Banking Sector”.

Below, we highlight the key themes that shaped the banking sector in H1’2019, which include consolidation, regulation, asset quality, demonetization and revenue diversification:

- Consolidation – Consolidation activity remained one of the key highlights witnessed in Kenya’s banking sector, as players in the sector are either acquired or merge leading to formation of relatively larger, well capitalized and possibly more stable entities. Ongoing consolidation transactions include:

-

- KCB Group finalized the take-over of 100.0% of all the ordinary shares of National Bank of Kenya (NBK) on 6th September 2019 after the Capital Markets Authority approved the acquisition. The transaction will enable KCB to increase its customer base and product offerings, which should result in a steady growth in profitability, after addressing the current challenges facing NBK of inadequate capitalization and high levels of Non-Performing Loans. For more information on the transaction, kindly see our Kenya Listed Banks Q1’2019 Report,

- On 27th September 2019, the Central Bank of Kenya announced the merger of Commercial Bank of Africa Limited and NIC Group PLC, effective 30th September 2019, following attainment of all regulatory approvals. The merged company is set to remain listed on the Nairobi Securities Exchange (NSE). Mr. John Gachora, who is currently the Group Managing Director of NIC Group will become the Group Managing Director and Chief Executive Officer of the combined entity, while Mr. Isaac Awuondo who is currently the Group Managing Director of CBA will become Chairman of the Kenyan banking subsidiary, and will maintain direct oversight over the Digital Business. The appointments are in line with our expectations, which we highlighted in our Cytonn January 2019 Monthly Report. With digital banking being a core aspect in the merger, a separate digital banking unit will be created, and it will be overseen by its own distinct board. In terms of preparation, both entities are ready to integrate their spaces, core systems, branding and even staff having received the final go ahead from the CBK. For more information on the merger, kindly see our Kenya Listed Banks Q1’2019 Report,

- Kenyan banks continued to pursue their inorganic growth strategies beyond Kenya, with a key example being Equity Group Holdings, who entered into a binding term sheet with Atlas Mara Limited to acquire certain banking assets in 4 countries in exchange for shares in Equity Group. These include:

-

-

- 62.0% of the share capital of Banque Populaire du Rwanda (BPR);

- 100.0% of the share capital of Africa Banking Corporation Zambia (ABCZam) Ltd.;

- 100.0% of the share capital of Africa Banking Corporation Tanzania (ABCTz); and,

- 100.0% of the share capital of Africa Banking Corporation Mozambique Ltd (ABCMoz).

-

More information on the details of the transaction are highlighted in our Kenya Listed Banks Q1’2019 Report. Aside from the Atlas Mara Limited transaction, Equity have entered into a binding Term Sheet with the shareholders of Banque Commerciale du Congo (BCDC), for the purchase of a controlling stake in the Congo-based lender, as discussed in our Cytonn Weekly #37/2019. Successful completion of the above transactions will likely see Equity expand its regional footprint, aiding the bank’s performance, which has in the recent past been constrained by thin margins due to the existent caps on loans. By expanding into markets where credit pricing is unrestricted, Equity would be able to leverage on its strong retail banking expertise as well as its strong digital banking capability via its subsidiary Finserve. This would enable Equity to expand both its funded and Non-Funded Income (NFI) revenue streams.

As noted in our focus note titled Consolidation in Kenya’s Banking Sector to Continue, we expect more consolidation in the banking sector, as the relatively weaker banks that probably do not serve a niche become acquired by the larger counterparts who have expertise in deposit mobilization, or serve a niche in the market. Consolidation will also likely happen, as entities form strategic partnerships, as they navigate the relatively tougher operating environment that is exacerbated by the stiff competition among the various players in the banking sector.

The table below summarizes the deals that have either happened or announced and expected to be concluded:

|

Acquirer |

Bank Acquired |

Book Value at Acquisition (Kshs bns) |

Transaction Stake |

Transaction Value (Kshs bns) |

P/Bv Multiple |

Date |

||

|

Oiko Credit |

Credit Bank |

3 |

22.8% |

1 |

1.5x |

Aug 2019 |

||

|

KCB Group |

National Bank of Kenya |

7 |

100.0% |

6.6 |

0.9x |

Apr 2019* |

||

|

CBA Group |

Jamii Bora Bank |

3.4 |

100.0% |

1.4 |

0.4x |

Jan 2019* |

||

|

AfricInvest Azure |

Prime Bank |

21.2 |

24.2% |

5.1 |

1.0x |

Jan 2019 |

||

|

CBA Group |

NIC Group |

33.5 |

53:47*** |

23.0 |

0.7x |

Jan 2019* |

||

|

KCB Group |

Imperial Bank** |

Unknown |

Undisclosed |

Undisclosed |

N/A |

Dec 2018 |

||

|

SBM Bank Kenya |

Chase Bank ltd |

Unknown |

75.0% |

Undisclosed |

N/A |

Aug 2018 |

||

|

DTBK |

Habib Bank Kenya |

2.4 |

100.0% |

1.8 |

0.8x |

Mar 2017 |

||

|

SBM Holdings |

Fidelity Commercial Bank |

1.8 |

100.0% |

2.8 |

1.6x |

Nov 2016 |

||

|

M Bank |

Oriental Commercial Bank |

1.8 |

51.0% |

1.3 |

1.4x |

Jun 2016 |

||

|

I&M Holdings |

Giro Commercial Bank |

3 |

100.0% |

5 |

1.7x |

Jun 2016 |

||

|

Mwalimu SACCO |

Equatorial Commercial Bank |

1.2 |

75.0% |

2.6 |

2.3x |

Mar 2015 |

||

|

Centum |

K-Rep Bank |

2.1 |

66.0% |

2.5 |

1.8x |

Jul 2014 |

||

|

GT Bank |

Fina Bank Group |

3.9 |

70.0% |

8.6 |

3.2x |

Nov 2013 |

||

|

Average |

|

|

73.7% |

|

1.4x |

|

||

|

* Announcement date ** Refers to certain Assets & Liabilities of Imperial Bank, which is under receivership *** Shareholder swap ratio between CBA and NIC, respectively |

||||||||

- Regulation - Regulation remained a key aspect that affected the banking sector in H1’2019, with the regulatory environment evolving and becoming increasingly stringent. Key changes in the regulatory environment in H1’2019 include:

-

- Banking Sector Charter: The Central Bank of Kenya proposed to introduce a Banking Sector Charter in 2018, which will guide service provision in the sector. The Charter, which came into effect in March 2019, aims to instill discipline in the banking sector in order to make it responsive to the needs of the banked population. It is expected to facilitate a market-driven transformation of the Kenyan banking sector, thereby considerably improving the quality of service provided, as well as increase the access to affordable financial services for the unbanked and under-served population. The implementation of the charter will likely hasten the implementation of risk-based credit scoring, which requires banks to extend credit on the basis of their credit scores, as determined by licensed credit reference bureaus. The charter is largely centered on consumer protection, by requiring banks to make full disclosure on the terms of the issuance of credit. In a bid to improve credit extension to Micro, Small and Medium Enterprises (MSMEs), the Banking Sector Charter prescribes that banks should have at least 20.0% of the loans extended to MSMEs. The CBK requires strict compliance with the charter, as banks may be imposed with administrative sanctions should they fail to comply with the charter,

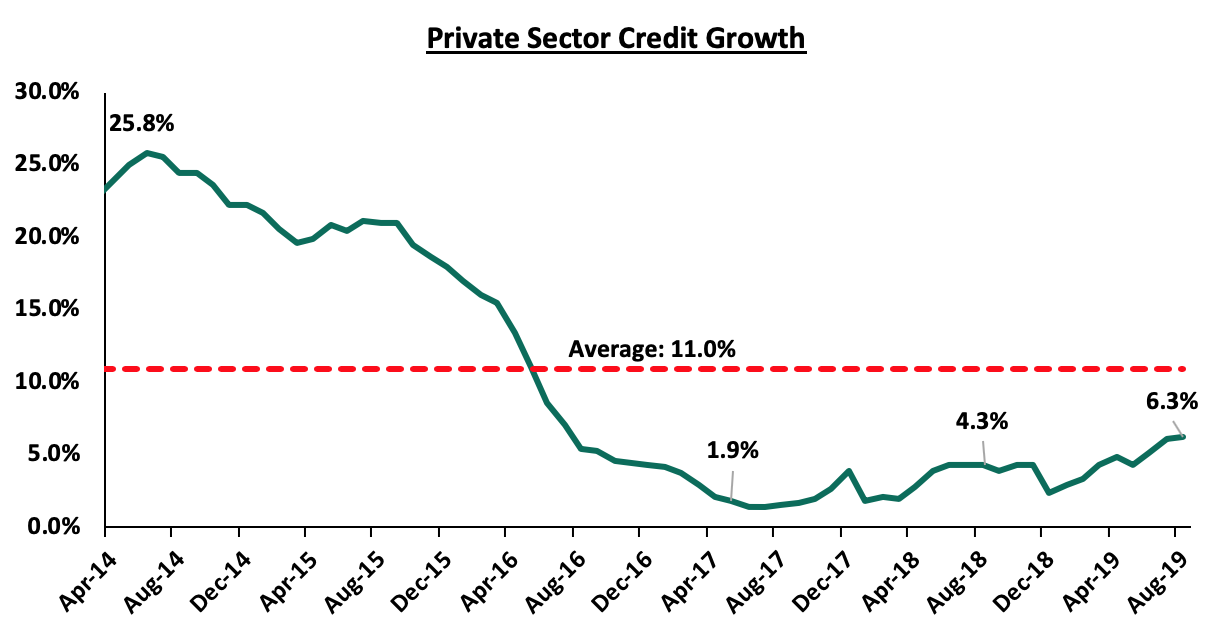

- Banking (Amendment) Act 2015: During the first half of the year, the High Court suspended the Banking (Amendment) Act 2015 for 1-year, terming it as unconstitutional. The court found the provisions of sections 33 b (1) and (2) of the Banking Act, which capped interest at 4.0% above the Central Bank Rate (CBR) to be vague, imprecise and ambiguous. To address this, the proposed Banking (Amendment) Bill 2019 was introduced in Parliament as it aims to seal the loopholes highlighted by the High Court in March 2019. Included in the Finance Bill 2019, there is the proposition by the Cabinet Secretary of the National Treasury to repeal the Act, citing that since its enactment, the law has failed to meet its objective of improved credit access, especially to MSMEs. During the week, discussions of the repeal propositions were concluded, with lawmakers voting to reject the propositions and retain the rate caps. With banks cognisant of Parliament’s relentlessness regarding the law, the push has since shifted towards increasing the 4.0% margin set. The same was proposed earlier in January 2019 by a member of parliament, proposing to increase the margin from 4.0% above the CBR, to 6.0% above the current ceiling, implying that the new cap would be at 19%, under the current CBR of 9%. With private sector credit growth remaining below the 5-year average as shown in the graph below, we retain our view as highlighted in our focus note, Review of the Interest Rate Cap that a repeal stands as the best course of action. We note that the CBK has been proactive in implementing policies aimed at consumer protection and increased credit access, with the policies yielding minimal results, as shown by the improvement in the private sector credit growth to 6.3% in August, compared to 4.3% in a similar period in 2018. We thus maintain our view that a repeal of the law remains the best course of action to spur credit extension to MSMEs, which should consequently spur economic growth.

-

- Demonetization: In an effort to track illicit financial flows, the Central Bank of Kenya, on 31st May 2019, announced the introduction of new generation notes of denominations Kshs 1,000, Kshs 500, Kshs 200, Kshs 100 and Kshs 50. Further to this, they highlighted that the old Kshs 1,000 notes will cease to be a legal tender and will be withdrawn from the market by 1st October 2019. In some cases, this exercise has brought cash shortages in the market that prompts people to seek alternatives on digital platforms. Aside from tracking illegal financial flows, demonetization is expected to enhance financial inclusion of the informal sector, in addition to helping the country transition to a more cash-less economy. For more information on demonetization, kindly see our topical on the Effects of the Issuance of the New Generation Banknotes.

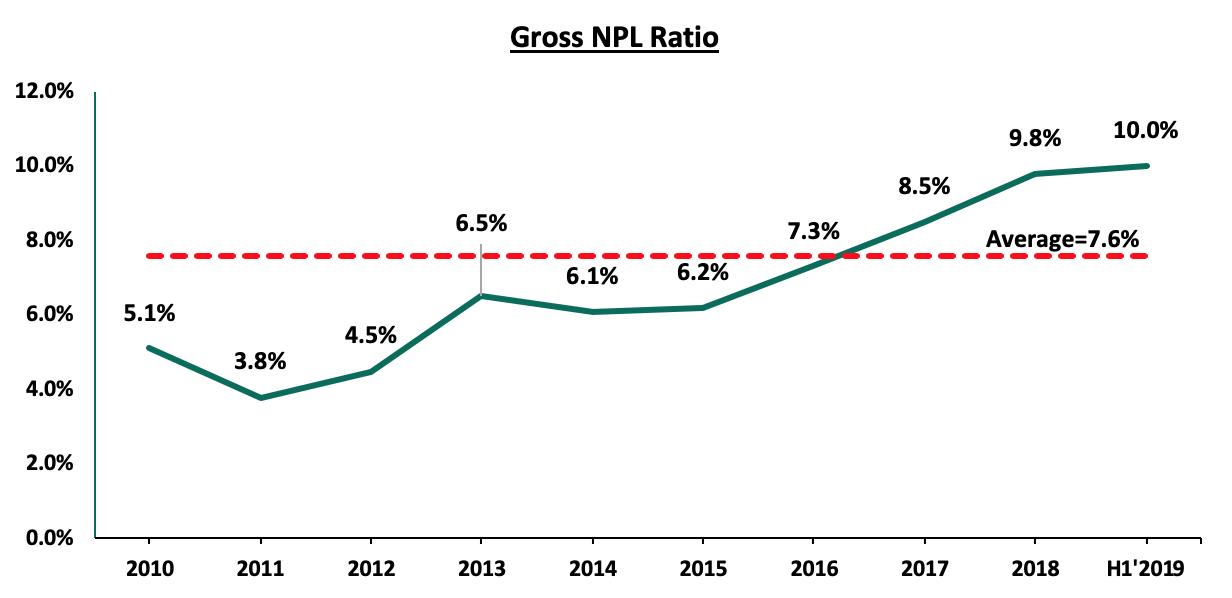

- Asset Quality – The listed banking sector continued to record a deterioration in its asset quality in H1’2019, as indicated by the rise in the Gross Non-Performing Loans (NPLs) ratio to 10.0%, from 9.8% in H1’2018, much higher than the 5-year average of 7.6%. The chart below highlights the asset quality trend:

Economic recovery from the harsh operating environment experienced in 2017 and the first quarter of 2018 has been slower than anticipated, which resulted in an increase in the number and value of bad loans. In addition, the denominator effect has been at play as the slow growth in loans has contributed to the increasing Gross NPL ratio in the sector. The major sectors touted by banks as leading in asset quality deterioration include trade, retail, manufacturing and real estate. Delayed payments by the government was also identified as a contributing factor, which affected various sectors, with small to mid-sized companies affected the most. Owing to the deteriorating asset quality, banks continued to implement their stringent lending policies in a bid to curb the rising NPLs, and consequently the associated impairment charges. Furthermore, banks have been investing heavily in adopting the use of advanced credit scoring method to identify delinquencies before they occur. In addition, several banks have set up remediation teams that help distressed clients to restructure, and consequently regain their debt-servicing capability. We however expect the industry’s asset quality to deteriorate in the near-term as businesses continue to cite a relatively tougher environment. Banks will thus continue to focus largely on (i) lending to relatively larger corporate entities, (ii) secured lending, and (iii) working capital financing to financially sound businesses.

- Revenue Diversification: Listed banks continued their revenue diversification drive by growing the Non-Funded Income (NFI) segment, with various banks launching several initiatives as highlighted below:

-

- Co-operative Bank of Kenya launched the Co-op Bank Property Hub under its mortgage division, which will offer property sales and mortgage origination to its clients. The Property Hub intends to serve the clients who have property to sell and connect them to the Co-operative Bank clients who want to buy property. The bank will also offer mortgages to the buyers of the property as it expects to leverage on its contacts with key institutions and the cooperative movements that largely own the bank to boost the property sales for its clients. For more information, please see our Kenya Mortgage Refinancing Company Update & Cytonn Weekly #17/2019,

- Co-operative Bank also highlighted its plan of growing the business of its leasing-focused subsidiary Co-op Bank Fleet, which intends to leverage on the synergies created by Co-operative Bank’s client base to grow its business, with the main business case of the subsidiary being the easing of the cash flow constraints of acquisitions of fleets, repair and maintenance, thus allowing businesses to focus on their core business. For more information, please see our our report here,

- Diamond Trust Bank Kenya (DTBK) announced that it has partnered with SWIFT, a leading provider of secure financial messaging services, in order to provide real time cross border payments to its clients. DTBK will be the first East African Bank to go live on the SWIFT global payment innovation service, a service that is carrying out over USD 30.0 bn worth of transactions a day, in over 148 currencies. For more information, please see our Kenya Mortgage Refinancing Company Update & Cytonn Weekly #17/2019,

- Standard Chartered Bank Kenya (SCBK) launched an innovation hub lab in Nairobi dubbed Xcelerator in a bid to boost its revenue streams and diversify by riding on financial technology. SCBK plans to allocate Kshs 10.0 bn into supporting Financial Technology (FinTech) startups to scale up and generate innovative solutions to problems in the banking sector. StanChart views FinTech firms as partners amid their growing disruption of the local financial sector, a move likely to aid the bank in generating additional revenue. For additional information, please see our Cytonn Weekly #15/2019, and,

- Housing Finance recently launched a WhatsApp banking solution that offers clients customized mobile services, making it the second company in the continent after First Bank of Nigeria, who launched the service in October 2018. To subscribe, one only needs to save the bank’s WhatsApp phone number and get access to services such as account opening, funds transfer bill payments and loans. This move by Housing Finance is mainly driven by the increased use of mobile phones and the internet.

We expect more forays by banks into the NFI segment, as players seek to alleviate the effects of the compressed funded income regime. We note that the average NFI for H1’2019 has grown by 16.5% compared to 6.9% seen in H1’2018 showing the shifted focus towards the segment has borne fruit for the sector.

Section II: Performance of the Banking Sector in H1’2019:

The table below highlights the performance of the banking sector, showing the performance using several metrics, and the key take-outs of the performance.

|

Bank |

Core EPS Growth |

Interest Income Growth |

Interest Expense Growth |

Net Interest Income Growth |

Net Interest Margin |

Non-Funded Income Growth |

NFI to Total Operating Income |

Growth in Total Fees & Commissions |

Deposit Growth |

Growth in Government Securities |

Loan to Deposit Ratio |

Loan Growth |

Return on Average Equity |

|

Barclays Bank Kenya |

18.0% |

7.4% |

30.8% |

0.6% |

8.4% |

12.6% |

32.4% |

11.1% |

5.9% |

15.4% |

81.3% |

6.0% |

18.1% |

|

I&M Bank |

17.0% |

8.8% |

18.3% |

2.2% |

6.0% |

21.9% |

39.3% |

6.0% |

12.5% |

28.5% |

72.6% |

5.7% |

17.7% |

|

Stanbic Holdings |

14.4% |

10.5% |

5.2% |

19.5% |

5.1% |

10.1% |

47.8% |

53.2% |

10.3% |

8.1% |

74.4% |

15.0% |

15.3% |

|

Diamond Trust Bank |

11.0% |

(6.6%) |

(5.5%) |

(7.5%) |

6.0% |

8.5% |

24.5% |

(15.6%) |

0.5% |

14.4% |

67.4% |

(3.8%) |

13.9% |

|

Equity Group |

9.1% |

9.2% |

14.3% |

7.6% |

8.5% |

25.6% |

44.0% |

16.1% |

16.5% |

13.0% |

70.0% |

16.7% |

22.1% |

|

NIC Group |

8.6% |

0.9% |

(7.0%) |

7.7% |

6.0% |

23.9% |

32.5% |

29.3% |

3.5% |

8.1% |

77.8% |

3.1% |

12.0% |

|

SCBK |

5.4% |

(7.3%) |

(26.0%) |

0.0% |

7.6% |

(2.2%) |

32.4% |

(12.8%) |

(1.0%) |

(15.2%) |

52.5% |

7.4% |

18.2% |

|

KCB Group |

5.0% |

4.3% |

1.6% |

5.2% |

8.2% |

14.7% |

34.1% |

3.5% |

7.3% |

20.3% |

85.0% |

13.6% |

22.7% |

|

Co-operative Bank |

4.6% |

(1.7%) |

3.5% |

(3.8%) |

8.4% |

25.1% |

38.0% |

38.1% |

9.0% |

14.2% |

79.6% |

2.6% |

18.8% |

|

National Bank of Kenya |

(40.1%) |

7.3% |

(14.4%) |

20.0% |

8.2% |

(28.7%) |

19.4% |

(4.6%) |

(4.9%) |

(17.5%) |

51.8% |

(1.0%) |

6.7% |

|

HF Group |

N/A |

(15.6%) |

(9.8%) |

(23.5%) |

4.0% |

55.8% |

47.1% |

44.4% |

(6.6%) |

5.4% |

91.0% |

(14.8%) |

(6.5%) |

|

H1'2019 Mkt Weighted Average* |

9.0% |

3.7% |

5.3% |

3.8% |

7.7% |

16.5% |

37.2% |

12.7% |

8.6% |

12.1% |

73.8% |

9.8% |

19.3% |

|

H1'2018 Mkt Weighted Average** |

19.0% |

7.9% |

12.0% |

6.4% |

8.1% |

6.9% |

34.3% |

4.6% |

10.0% |

14.9% |

73.8% |

3.8% |

19.5% |

|

*Market cap weighted as at 6/09/2019 **Market cap weighted as at 31/08/2018 |

|||||||||||||

Key takeaways from the table above include:

- Kenya Listed Banks recorded a 9.0% average increase in core Earnings per Share (EPS), compared to a growth of 19.0% in H1’2018. As a result, the Return on Average Equity decreased marginally to 19.3% compared to 19.5% recorded a similar period in 2018,

- Deposit growth came in at 8.6%, slower than the 10.0% growth recorded in H1’2018. On the other hand, interest expense increased at a slower pace of 5.3%, compared to 12.0% in H1’2018, indicating that banks have been able to mobilize relatively cheaper deposits. In addition, the removal of the 70.0% minimum deposit payable on deposits in the Finance Act 2018 reduced the cost of deposit funding,

- Average loan growth came in at 9.8%, which was faster than the 3.8% recorded in H1’2018, indicating that there was an improvement in credit extension to the economy. Government Securities on the other hand recorded growth of 12.1%, which was a slower growth rate compared to the 14.9% in H1’2018. This shows that banks have begun to adjust their business models, focusing more on private sector lending as opposed to investing in government securities, whose yields declined during the year. Interest income increased by 3.7%, slower than the 7.9% recorded in H1’2018. Consequently, the Net Interest Income grew by 3.8%, slower than the 6.4% recorded in H1’2018,

- The average Net Interest Margin in the sector came in at 7.7%, lower than the 8.1% in H1’2018. The decline was mainly due to a decline in yields recorded in government securities, coupled with the decline in yields on loans due to the 100-bps decline in the Central Bank Rate, and,

- Non-Funded Income grew by 16.5% y/y, faster than the 6.9% recorded in H1’2018. The growth in NFI was boosted by the total fee and commission income which improved by 12.7%, compared to the 4.6% growth recorded in H1’2018, owing to the faster loan growth.

Section III: Outlook and Focus Areas of the Banking Sector Going Forward:

The banking sector had a slower growth compared to the performance recorded in a similar period last year, largely due to the slower expansion of funded income segment, as NII grew by 3.8% in H1’2019, slower than 6.4% in H1’2018. Funded income continues to record relatively slower growth, affected by the declining yields in both loans and government securities. We maintain our view that the interest rate cap has not achieved its intended objectives of easing the access to credit and reducing the cost of credit, and thus needs to be repealed, so as to spur economic growth, as MSMEs have continued to struggle in accessing the much-needed credit. It would be helpful for the MSMEs to form a lobby group to engage directly with policy makers and legislators. We also continue to be proponents of promoting competing sources of financing, which should reduce the overreliance on bank funding in the economy, currently 90.0% to 95.0% of all funding. By having various competing sources of financing, this would trigger a self- regulated pricing structure, in the event of a repeal of the law.

Thus, we expect the following:

- A review of the Banking (Amendment) Act 2015, given the proposition to repeal the law that was included in the Finance Bill 2019 was voted down by lawmakers. Given that a Member of Parliament proposed a revision of the law to include a ceiling of 6.0% above the limit set by the Banking (Amendment) Act, 2015 for the high risk borrowers, we expect parliament to maintain their stance of a no repeal of the interest rate cap, and instead opt for an amendment of the margins, as pressure from various institutions such as the National Treasury and the CBK increases. The National Assembly approved the Finance Bill 2019 earlier this week and the same is at the Presidential accent stage where it should be signed into law, and,

- The demonetization exercise will likely result in a possibly stronger deposit growth for banks especially in H2’2019, as money flows into banks, especially in the run up to the 1st October deadline. So far, approximately 100.0 mn out of the 217.0 mn one-thousand notes have been converted, and within the first month of the June announcement, deposits in banks grew by Kshs 22.3 bn, while currency outside banks fell by Kshs 25.1 bn. Furthermore, during the current transition period, we expect an increase in the number and value of transactions, as demand for digital transactions rises, with a majority of people prioritizing digital transactions to avoid handling the old currency as well as fake currency. This should presumably lead to a relatively better performance of the Non-Funded Income (NFI) segment.

We expect banks to continue focusing on the following:

- Asset Quality Management: Banks will look to manage the industry-wide deteriorating asset quality, which can be seen in the current Gross NPL Ratio that came in a 10.0%, higher than the 5-year average of 7.6%. This may involve further tightening of credit standards as banks cherry pick low risk credit consumers and increase focus on secured, collateral-based lending,

- Revenue Diversification: In the current regime of compressed interest margins, focus on Non-Funded Income (NFI) is likely to continue, as banks aim to grow transactional income via alternative channels such as agency banking, internet and mobile technologies. The average growth in NFI for H1’2019 came in at 16.5%, compared to 6.9% recorded in H1’2018,

- Operational Efficiency: Cost containment is likely to continue being a focus area as can be seen in the H1’2019 figures, where the average cost-to-income ratio was 55.1%, lower than the 5 year average of 58.0%. Banks such as National Bank of Kenya, Standard Chartered and Stanbic Bank have had to lay off staff in H1’2019 in an effort to cut costs. We expect continued restructuring, possibly leading to staff layoffs, as staff headcount demands reduce, on increased usage of mobile and internet channels,

- Downside Regulatory Compliance Risk Management: With increased emphasis on anti-money laundering and fraudulent transactions, we expect banks to be keener on streamlining their operational processes and procedures in line with global standards and regulatory requirements, and

- Consolidation: Banks will continue to form strategic partnerships in an effort to increase market share for the strong players in the market and struggling banks that don’t have a niche market will get acquired. We expect well capitalized players to take advantage of this, which should see several deals completed.

For more information, see our Cytonn H1’2019 Banking Sector Review

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma