Jun 13, 2021

Following the release of the Q1’2021 results by Kenyan listed banks, the Cytonn Financial Services Research Team undertook an analysis on the financial performance of the listed banks and identified the key factors that shaped the performance of the sector.

Core Earnings per Share recorded a weighted increase of 28.4% in Q1’2021, compared to a weighted decline of 7.3% recorded in Q1’2020. The increase in earnings was mainly attributable to the growth in Net Interest Income, which grew by 17.5% in Q1’2021, compared to a growth of 7.4% in Q1’2020, for the listed banking sector. Additionally, interest income grew by 14.7%, compared to a growth of 8.2% recorded in Q1’2020, attributable to the increased allocation to higher yielding government securities during the quarter. Investments in government securities grew by 20.3%, faster than the 11.0% loan growth recorded during the period. Consequently, the Yield on Interest Earning Assets (YIEA) increased to 10.2%, from the 9.8% recorded in Q1’2020, with Net Interest Margin (NIM) increasing to 7.4%, 0.2% points higher than the 7.2% recorded in Q1’2020 for the whole listed banking sector.

The report is themed “Recovery of the Banking Sector Amid a Tough Operating Environment” where we assess the key factors that influenced the performance of the banking sector in Q1’2021, the key trends, the challenges banks faced, and areas that will be crucial for growth and stability of the banking sector going forward. As such, we shall address the following:

- Key Themes That Shaped the Banking Sector Performance in Q1’2021,

- Summary of The Performance of the Listed Banking Sector in Q1’2021,

- The Focus Areas of the Banking Sector Players Going Forward, and,

- Brief Summary and Ranking of the Listed Banks based on the Outcome of Our Analysis.

Section I: Key Themes That Shaped the Banking Sector Performance in Q1’2021

Below, we highlight the key themes that shaped the banking sector in Q1’2021 which include regulation, regional expansion through mergers and acquisitions, asset quality deterioration and capital raising for onward lending:

1. Regulation

- Closure of Loan restructuring Window: The loan restructuring window as per the Banking Circular No 3 of 2020 by the Central Bank of Kenya provided to commercial banks and mortgage finance companies on loan restructuring came to an end on March 2nd, having seen a total of loans worth Kshs 1.7 tn restructured, representing 57.0% of the banking sector’s loan book. With this expiry the banks are now back to normal loan risk management. However, despite the expiry of the loan restructuring window, some banks still supported their borrowers during the period. Equity Group, KCB Group, Diamond Trust Bank and Cooperative Bank disclosed the cumulative amount of loans they have restructured as at Q1’2021;

|

No. |

Bank |

Cumulative Amount Restructured (Kshs bn) |

% of restructured loans to total loans |

Q1’2021 y/y Change in Loan loss provision |

|

1 |

Equity Group Holdings |

171.0 |

31.0% |

(59.3%) |

|

2 |

Kenya Commercial Bank |

102.5 |

18.8% |

(1.3%) |

|

3 |

Diamond Trust Bank |

72.0 |

33.0% |

67.7% |

|

4 |

Co-operative Bank of Kenya |

49.0 |

14.3% |

153.5% |

|

|

Total |

394.5 |

24.3% |

40.2% |

2. Regional Expansion through Mergers and Acquisitions: The Kenyan banks are looking at having an extensive regional reach and to this end the following were the major M&A’s activities announced in May 2021:

- Equity Group disclosed that it had acquired an additional 7.7% stake valued at Kshs 996.0 mn in Equity bank Congo (EBC) from the German Sovereign Wealth Fund (KfW). The acquisition raised the total ownership in EBC to 94.3%, indicating that they are currently valuing the company at Kshs 14.2 bn. This follows the recent acquisition of 66.5% stake in Banque Commerciale Du Congo (BCDC) by Equity Group at a cost of Kshs 10.2 bn in August 2020. For more information, please see Cytonn Weekly#20/2021,

- KCB Group disclosed that it had made an offer to the Banque Populaire du Rwanda Plc (BPR) shareholders to raise its acquisition stake in the bank from 62.1% to 100.0%. As highlighted in our Cytonn Weekly #48/2020, the 62.1% BPR acquisition would see KCB pay a cash consideration based on the net asset value of the BPR at completion of the transaction using a price to book multiple of 1.1x. According to the latest BPR financials, the bank had a book value of Rwf 47.3 bn (Kshs 5.1 bn), and thus at the trading multiple of 1.1x, we expect KCB Group to pay Kshs 5.6 bn. Collectively, KCB will spend a total of USD 56.9 mn (Kshs 6.1 bn) in the acquisition of Banque Populaire du Rwanda Plc (BPR) Rwanda and African Banking Corporation (ABC) Tanzania. For more information on the acquisition, see our Cytonn Weekly #19/2021, and,

- I&M Holdings Plc announced that it completed the 90.0% acquisition of Orient Bank Limited Uganda (OBL) share capital, after receiving all the required regulatory approvals. As highlighted in our Cytonn Weekly #50/2020, I&M Holdings was set to pay Kshs 3.6 bn for the deal. Additionally, I&M Holdings will take over 14 branches from OBL, taking its total branches to 80, from 66 branches as at the end of 2020. For more information, please see Cytonn Weekly #18/2021.

Below is a summary of the deals in the last 7 years that have either happened, been announced or expected to be concluded:

|

Acquirer |

Bank Acquired |

Book Value at Acquisition (Kshs bn) |

Transaction Stake |

Transaction Value (Kshs bn) |

P/Bv Multiple |

Date |

|

I&M Holdings PLC |

Orient Bank Limited Uganda |

3.3 |

90.0% |

3.6 |

1.1x |

April-21 |

|

KCB Group |

Banque Populaire du Rwanda, and, ABC Tanzania |

4.5 (Banque Populaire du Rwanda, only. ABC Tanzania financials unknown) |

100.0% |

6.1 |

N/D |

Nov-20* |

|

Co-operative Bank |

Jamii Bora Bank |

3.4 |

90.0% |

1 |

0.3x |

Aug-20 |

|

Commercial International Bank |

Mayfair Bank Limited |

1 |

51.0% |

Undisclosed |

N/D |

May-20* |

|

Access Bank PLC (Nigeria) |

Transnational Bank PLC. |

1.9 |

100.0% |

1.4 |

0.7x |

Feb-20* |

|

Equity Group ** |

Banque Commerciale Du Congo |

8.9 |

66.5% |

10.3 |

1.2x |

Nov-19* |

|

KCB Group |

National Bank of Kenya |

7 |

100.0% |

6.6 |

0.9x |

Sep-19 |

|

CBA Group |

NIC Group |

33.5 |

53%:47% |

23 |

0.7x |

Sep-19 |

|

Oiko Credit |

Credit Bank |

3 |

22.8% |

1 |

1.5x |

Aug-19 |

|

CBA Group** |

Jamii Bora Bank |

3.4 |

100.0% |

1.4 |

0.4x |

Jan-19 |

|

AfricInvest Azure |

Prime Bank |

21.2 |

24.2% |

5.1 |

1.0x |

Jan-18 |

|

KCB Group |

Imperial Bank |

Unknown |

Undisclosed |

Undisclosed |

N/A |

Dec-18 |

|

SBM Bank Kenya |

Chase Bank Ltd |

Unknown |

75.0% |

Undisclosed |

N/A |

Aug-18 |

|

DTBK |

Habib Bank Kenya |

2.4 |

100.0% |

1.8 |

0.8x |

Mar-17 |

|

SBM Holdings |

Fidelity Commercial Bank |

1.8 |

100.0% |

2.8 |

1.6x |

Nov-16 |

|

M Bank |

Oriental Commercial Bank |

1.8 |

51.0% |

1.3 |

1.4x |

Jun-16 |

|

I&M Holdings |

Giro Commercial Bank |

3 |

100.0% |

5 |

1.7x |

Jun-16 |

|

Mwalimu SACCO |

Equatorial Commercial Bank |

1.2 |

75.0% |

2.6 |

2.3x |

Mar-15 |

|

Centum |

K-Rep Bank |

2.1 |

66.0% |

2.5 |

1.8x |

Jul-14 |

|

GT Bank |

Fina Bank Group |

3.9 |

70.0% |

8.6 |

3.2x |

Nov-13 |

|

Average |

|

|

76.7% |

|

1.3x |

|

|

* Announcement Date ** Deals that were dropped |

||||||

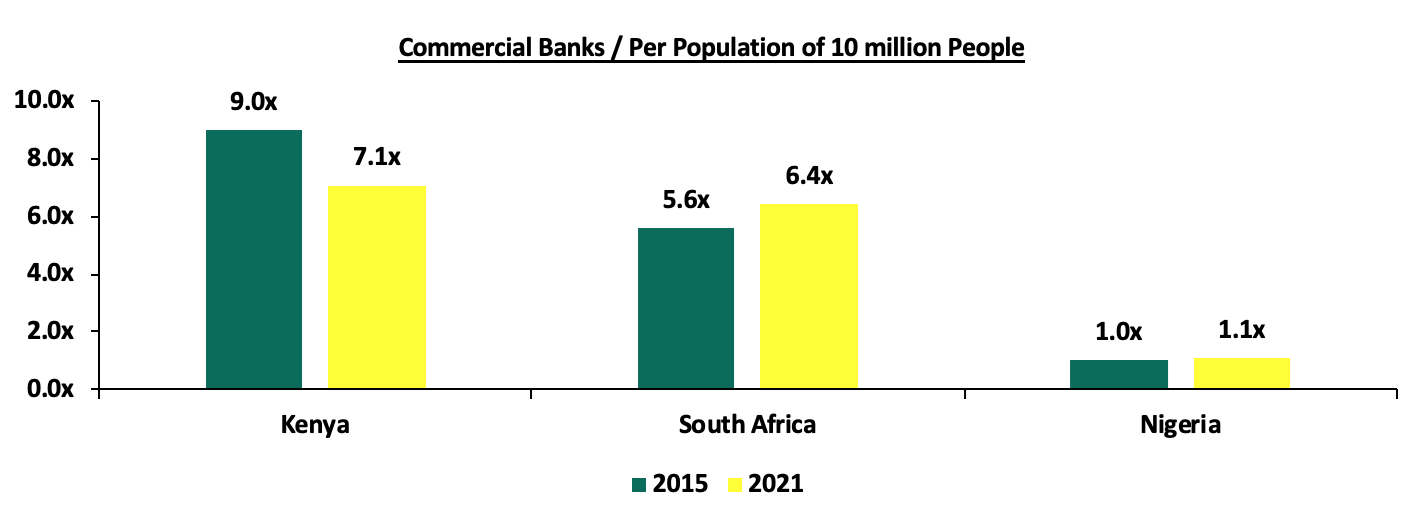

The number of commercial banks in Kenya has now reduced to 38, compared to 43 banks 6-years ago. The ratio of the number of banks per 10 million population in Kenya now stands at 7.1x, which is a reduction from 9.0x 6-years ago, demonstrating continued consolidation of the banking sector. However, despite the ratio improving, Kenya still remains overbanked as the number of banks remains relatively high compared to the population. For more on this see our topical.

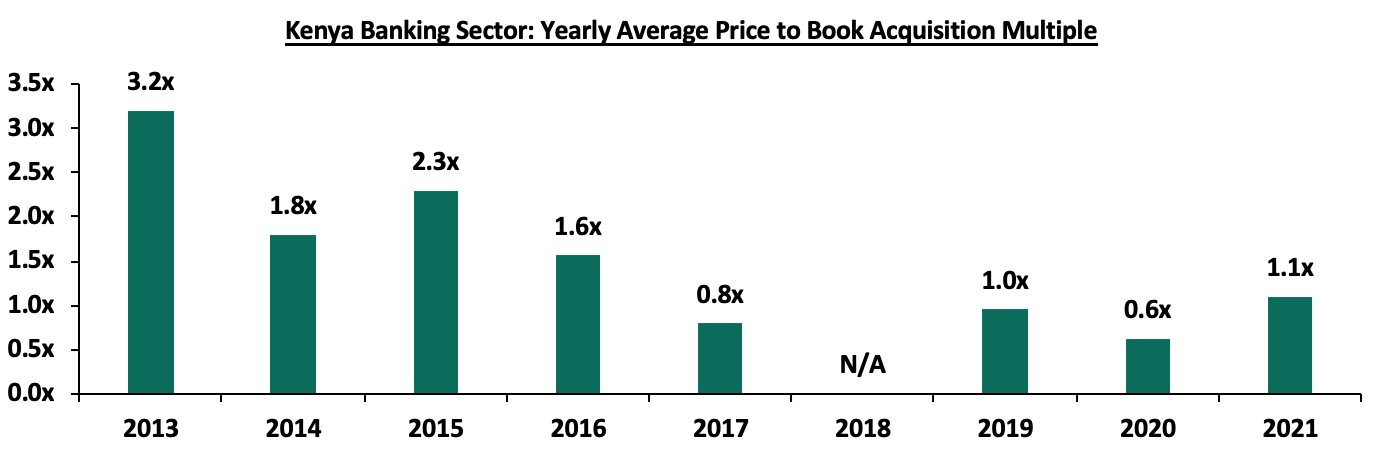

After a consistent decline in the acquisition valuation for banks, we saw an increase in the valuations from the average of 0.6x in 2020 to 1.1x so far in 2021. This however still remains low compared to historical prices paid as highlighted in the chart below;

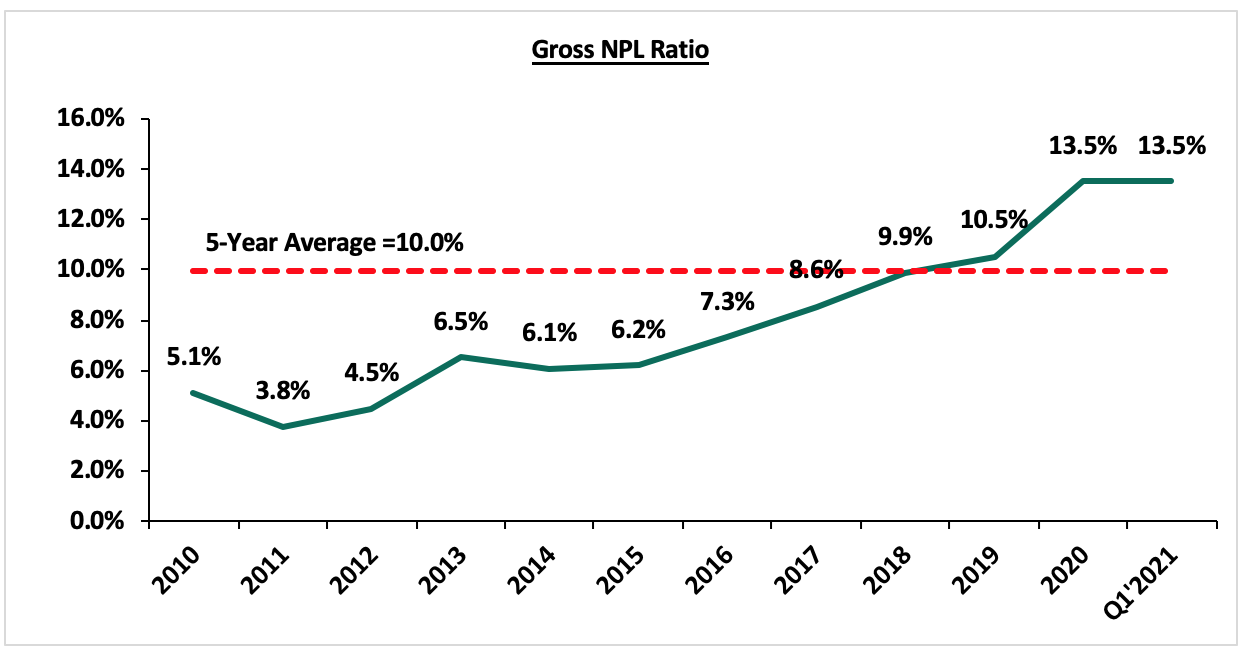

3. Asset Quality Deterioration: Asset quality for listed banks deteriorated in Q1’2021, with the Gross NPL ratio rising by 2.1% points to 13.5% from 11.4% in Q1’2020. Key to note, the listed banks’ NPL ratio of 13.5% is the highest it has ever been and is higher than the 5-year average of 10.0%. The deterioration in asset quality was due to the coronavirus-induced downturn in the economy, which led to an uptick in the non-performing loans. The NPL coverage rose to 62.0% in Q1’2021, from 57.4% recorded in Q1’2020, in accordance with IFRS 9, where banks are expected to provide both for the incurred and expected credit losses. The significantly higher provisional requirement levels coupled with the increased credit risk led to slower loan growth in Q1’2021, which came in at 11.2% compared to a growth of 14.1% in Q1’2020. According to the May 2021 MPC Press Release, the NPL ratio for the entire banking sector stood at 14.2% as at April 2021, a deterioration from 14.1% in December 2020.

The chart below highlights the asset quality trend:

https://cytonnreport.com/storage/research/60c596b1970155.92407539.png

The table below highlights the asset quality for the listed banking sector:

|

|

Q1’2020 NPL Ratio** |

Q1’2021 NPL Ratio* |

Q1’2020 NPL Coverage** |

Q1’2021 NPL Coverage* |

% point change NPL Ratio |

% point change NPL Coverage |

|

ABSA |

8.1% |

7.5% |

64.5% |

73.4% |

(0.6%) |

9.8% |

|

DTB-K |

8.0% |

10.6% |

42.4% |

46.5% |

2.6% |

4.1% |

|

I&M Holdings |

11.3% |

11.9% |

58.8% |

61.1% |

0.6% |

2.3% |

|

Equity Group |

11.2% |

12.1% |

45.8% |

55.5% |

0.9% |

9.7% |

|

NCBA Group |

14.5% |

14.7% |

54.5% |

65.0% |

0.2% |

10.5% |

|

KCB |

11.1% |

14.9% |

61.3% |

61.6% |

3.8% |

0.3% |

|

Stanbic Bank |

12.1% |

15.1% |

59.3% |

63.9% |

3.0% |

4.6% |

|

SCBK |

14.2% |

16.4% |

78.1% |

81.1% |

2.2% |

3.0% |

|

Co-op Bank |

10.8% |

16.9% |

54.8% |

58.4% |

6.1% |

3.6% |

|

HF Group |

27.3% |

24.7% |

52.2% |

64.7% |

(2.6%) |

12.5% |

|

Mkt Weighted Average |

11.4% |

13.5% |

57.4% |

62.0% |

2.1% |

4.7% |

|

*Market cap weighted as at 08/06/2021 |

||||||

|

**Market cap weighted as at 02/06/2020 |

||||||

Key take-outs from the table include;

- Asset quality for the listed banks deteriorated during the period of review, with the weighted average NPL ratio rising by 2.1% points to a market cap weighted average of 13.5%, from an average of 11.4% in Q1’2020. The deterioration in asset quality was as a result of increased non-performing loans due to the increased credit risk as the economy slowed down due the Covid-19 pandemic, and,

- NPL Coverage for the listed banks increased to a market cap weighted average of 62.0% in Q1’2021, from 57.4% recorded in Q1’2020, as the banks increased their provisioning levels to proactively manage risks given the tough economic conditions occasioned by the pandemic. We expect banks to continue over-provisioning, albeit at a slower rate than in 2020.

4. Capital Raising : In Q1’2021, listed banks’ turned to borrowing from international institutions to not only strengthen their capital position but also boost their ability to lend to the perceived riskier Micro Small and Medium Sized Enterprises (MSMEs) segment in order to support the small businesses in the tough operating environment occasioned by the COVID-19 pandemic. Some of the loans taken up for onward lending to MSMEs include:

- In January 2021, Cooperative Bank announced it had received a USD 75.0 mn (Kshs 8.3 bn) loan from the International Finance Corporation (IFC) to facilitate lending to MSMEs and businesses undertaking climate-friendly projects. The loan, which has a 7-year repayment period will also help match the bank’s assets-liabilities match, with long term loans being financed by long term debt. Cooperative Bank also received a USD 15.0 mn (Kshs 1.6 bn) loan from Swedfund in February 2021 to enhance the bank’s ability to lend to SMEs and increase their access to funding particularly in the midst of a pandemic,

- In January 2021, Equity Bank obtained a USD 50.0 mn (Kshs 5.9 bn) loan from Dutch Development Bank (FMO) to enable the bank to lend to perceived riskier small enterprises who have been hard hit by the pandemic. Additionally, Equity received a €0 mn (Kshs 15.8 bn) facility from the European Union and the European Investment Bank (EIB) in March 2021 to support access to finance MSMEs including in the agricultural sector and help entrepreneurs and small businesses better withstand the economic challenges and uncertainties caused by COVID-19,

- KCB Bank received a USD 150.0 mn (Kshs 16.4 bn) loan from the IFC, The SANAD Fund for MSMEs (SANAD), the Belgium Investment Company for Developing Countries (BIO) and Symbiotics in March 2021 to help the bank increase lending for climate-friendly projects and smaller businesses especially those owned by women, and,

- I&M Bank received a USD 50.0 mn (Kshs 5.4 bn) from IFC in May 2021 to expand lending to MSMEs. The loan, with a five year grace period and maturity of 7 years will also serve as an additional capital buffer for the bank.

The table below highlights the disclosed loan facilities that banks have secured for capital injection and lending to the MSMEs in Q1’2021:

|

Bank |

Amount Borrowed For Onward Lending (Kshs bn) |

Purpose |

|

Equity Bank |

21.7 |

MSME lending |

|

KCB Bank |

16.4 |

MSME lending |

|

Cooperative Bank |

9.9 |

*MSME lending and Tier II Capital |

|

I&M Bank |

5.4 |

*MSME lending and Tier II Capital |

|

Total |

53.4 |

*Tier II Capital refers to a bank’s supplementary capital which includes senior debt (debt that a company must repay first before going out of business) with a tenure of not less than five years

Section II: Summary of the Performance of the Listed Banking Sector in Q1’2021:

The table below highlights the performance of the banking sector, showing the performance using several metrics, and the key take-outs of the performance;

|

Bank |

Core EPS Growth |

Interest Income Growth |

Interest Expense Growth |

Net Interest Income Growth |

Net Interest Margin |

Non-Funded Income Growth |

NFI to Total Operating Income |

Growth in Total Fees & Commissions |

Deposit Growth |

Growth in Government Securities |

Loan to Deposit Ratio |

Loan Growth |

Return on Average Equity |

|

NCBA |

73.8% |

8.1% |

(5.7%) |

19.9% |

5.9% |

(3.3%) |

44.3% |

(8.1%) |

11.2% |

15.1% |

56.0% |

(1.1%) |

8.1% |

|

Equity |

63.8% |

31.9% |

42.4% |

28.4% |

7.6% |

30.7% |

42.3% |

21.5% |

58.2% |

16.1% |

61.7% |

28.6% |

18.9% |

|

ABSA |

23.7% |

(0.3%) |

17.6% |

5.9% |

7.0% |

(3.9%) |

32.0% |

7.4% |

7.7% |

1.1% |

84.9% |

7.5% |

13.6% |

|

Stanbic |

23.1% |

0.5% |

(7.3%) |

5.0% |

6.1% |

19.3% |

46.7% |

(8.5%) |

10.6% |

42.3% |

69.5% |

(2.4%) |

13.2% |

|

SCBK |

18.9% |

(9.0%) |

(30.2%) |

(2.8%) |

6.7% |

11.1% |

35.1% |

11.7% |

8.9% |

7.8% |

44.4% |

(6.1%) |

11.3% |

|

I&M |

13.5% |

10.2% |

(5.2%) |

23.4% |

5.4% |

(17.7%) |

29.7% |

(5.3%) |

9.3% |

89.5% |

73.4% |

5.6% |

13.3% |

|

KCB |

1.8% |

8.7% |

1.8% |

11.1% |

8.4% |

(20.0%) |

27.4% |

(26.5%) |

1.2% |

4.7% |

79.7% |

7.8% |

13.9% |

|

DTB-K |

0.5% |

4.8% |

2.9% |

6.2% |

5.3% |

(1.9%) |

23.9% |

(20.5%) |

10.6% |

7.9% |

68.2% |

2.3% |

5.7% |

|

COOP |

(3.7%) |

27.6% |

19.8% |

30.7% |

8.6% |

(9.2%) |

32.0% |

(15.7%) |

16.0% |

43.4% |

75.7% |

8.0% |

12.3% |

|

HF |

N/A |

(18.7%) |

(19.0%) |

(18.3%) |

4.1% |

(46.7%) |

22.0% |

(36.2%) |

(2.1%) |

13.4% |

96.2% |

(6.9%) |

(20.4%) |

|

Q1'21 Mkt Weighted Average* |

28.4% |

14.7% |

12.7% |

17.5% |

7.4% |

2.9% |

35.3% |

(2.4%) |

21.8% |

20.3% |

69.2% |

11.0% |

13.8% |

|

Q1'20 Mkt Weighted Average** |

(7.3%) |

8.2% |

11.4% |

7.4% |

7.2% |

15.9% |

22.7% |

24.5% |

14.3% |

14.9% |

74.1% |

14.1% |

17.2% |

|

*Market cap weighted as at 08/06/2021 |

|||||||||||||

|

**Market cap weighted as at 02/06/2020 |

|||||||||||||

Key takeaways from the table above include:

- The listed banks recorded a 28.4% weighted average growth in core Earnings per Share (EPS), compared to a weighted average decline of 7.3% in Q1’2020 for the entire listed banking sector. The performance is largely skewed by the strong performance from NCBA and Equity Group,

- The Banks have recorded a weighted average deposit growth of 21.8%, faster than the 14.3% growth recorded in Q1’2020,

- Interest expense grew at a faster pace, by 12.7%, compared to the 11.4% growth in Q1’2020 while cost of funds declined, coming in at a weighted average of 2.5% in Q1’2021, from 3.0% in Q1’2020, owing to the faster growth in average interest-bearing liabilities, an indication that the listed banks were able to mobilize cheaper deposits,

- Average loan growth came in at 11.0%, lower than the 14.1% growth recorded in Q1’2020. The loan growth was also slower than the 20.3% growth in government securities, an indication of the banks’ preference of investing in Government securities as opposed to lending due to the elevated credit risk occasioned with the pandemic. The faster growth in government securities could also be attributed to cautious lending by banks in a bid to reduce cost of risk as well as mitigate further deterioration of the asset quality,

- Interest income grew by 14.7%, compared to a growth of 8.2% recorded in Q1’2020. Notably, the Yield on Interest Earning Assets (YIEA) increased to 10.2%, from the 9.8% recorded in Q1’2020, an indication of the increased allocation to higher-yielding government securities by the sector during the period. Consequently, the Net Interest Margin (NIM) now stands at 7.4%, 0.2% points higher than the 7.2% recorded in Q1’2020 for the whole listed banking sector, and,

- Non-Funded Income grew by 2.9%, compared to the 15.9% growth recorded in Q1’2020. This can be attributable to a slower growth in the fees and commission which declined by 2.4% compared to a growth of 24.5% in Q1’2020.

Section III: Outlook of the banking sector:

The banking sector remained resilient during the quarter, as evidenced by the increase in profitability, with the Core Earnings Per Share (EPS) growing by 28.4%, despite the tough prevailing operating environment occasioned by the COVID-19 pandemic. The increase in EPS is mainly attributable to the 17.5% growth in Net Interest Income (NII) compared to the 7.4% growth recorded in Q1’2020. Provisioning levels for most listed banks also declined, pointing to reduced credit risk during the period and in turn boosting the sector’s bottom line. We expect the reduction in provisioning levels to be a recurrent theme in 2021. However, the banking sector’s Loan Loss Provisions are expected to remain higher than the pre-COVID period and historic average and as such, banks will continue to overprovision during the period. The waiver of charges on transactions weighed down the Non-Funded Income (NFI) performance, with the listed banks recording a slower 2.9% weighted growth in NFI, from the 15.9% growth recorded in Q1’2020. Following the expiry of the waiver on fees and commissions on loans and the loan restructuring window having closed in March 2021, we expect the banking sector’s performance to improve in the medium to long term. Based on the current operating environment, we believe the future performance in the banking sector will be shaped by the following key factors:

- Growth in Interest income: With interest income growth at 14.7% in Q1’2021 outpacing the 8.2% growth recorded in Q1’2020, we believe that interest income growth will remain a key industry driver going forward. The continued allocation to government securities which witnessed slight increases in yields in Q1’2021 will also lead to an increase in the overall interest income. The expiry of the restructuring and moratorium window given to borrowers will also enable banks to further increase interest income growth which will lead to increased profitability. Key to note, some banks are still supporting borrowers after the expiry of the loan restructuring window and this could slow down the recovery of interest income in the medium term,

- Revenue Diversification: In Q1’2021, Non-Funded Income recorded a 2.9% weighted average growth, slower than the 15.9% recorded in Q1’2020, attributable to the waiver on fees and commissions on loans and advances issued by the CBK on March 2020. The banking sector’s Non-Funded Income to Operating Income however improved, coming in at 35.3% in Q1’2021, compared to 22.7% of Operating Income in Q1’2020. Given that Non-Funded Income contributes less than 50.0% of listed banks’ operating income, there exists an opportunity for the sector to increase NFI contribution to revenue going forward. With the expiry of the waiver on bank charges on 2nd March 2021, we expect NFI growth to recover in the medium-long term due to the increased adoption of digital channels. According to Central Bank Annual Report 2019/2020, 67.0% of banking transactions were conducted on mobile phones after the onset of the pandemic, compared to 55.0% of transactions before the pandemic. Moreover, more than 1.6 mn additional customers are now using mobile-money channels compared to the period before the pandemic began. The increased uptake of digital channels will enable banks to leverage on these platforms and generate Non-Funded Income from transactions. This presents an ideal opportunity for the banking sector to diversify away from their reliance on interest income in the long term and boost revenue growth,

- Provisioning: Loan Loss Provisions recorded a slower growth of 5.5% in Q1’2021 compared to a growth of 233.2% in FY’2020, signifying improving business conditions and reduction of credit risk. However, given that the duration of the pandemic remains unknown, coupled with the emergence of new variants of COVID-19 in the country, we believe that the normalization of the sector’s provisioning levels to pre-pandemic levels will take longer than expected. The proactive stance taken by the banks in monitoring their loan books will however continue to support the sector’s growth,

- Cost Rationalization: Given the low revenues and increased automation, banks are expected to continue pursuing their cost rationalization strategies. Majority of banks have been riding on the digital revolution wave to improve their operational efficiency. Increased adoption of alternative channels of transactions such as mobile, internet, and agency banking has led to increased transactions carried out via alternative channels and out of bank branches, which have been reduced to handling high-value transactions and other services such as advisory. ABSA Bank, for example, succeeded in moving 87.0% of transactions outside the branch as at FY’2020. With the COVID-19 pandemic necessitating contactless transactions, banks reduced front-office operations, thereby cutting the number of staff required and by extension, reducing operating expenses and hence, improving operational efficiency, and,

- Expansion and Further Consolidation: With consolidation remaining a key theme going forward, the current environment could provide opportunities for bigger banks with an adequate capital base to expand and take advantage of the low valuations in the market to further consolidate and buy out smaller banks. Consolidation will be key for most of the smaller banks that suffered losses during the pandemic, and would also benefit larger banks with the opportunity to improve their asset base. We believe that consolidation could also increase post-COVID as tier one banks resume their expansion strategies both locally and regionally as the economy improves.

Section IV: Brief Summary and Ranking of the Listed Banks:

As per our analysis on the banking sector from a franchise value and a future growth opportunity perspective, we carried out a comprehensive ranking of the listed banks. For the franchise value ranking, we included the earnings and growth metrics as well as the operating metrics shown in the table below in order to carry out a comprehensive review of the banks:

|

Bank |

Loan to Deposit Ratio |

Cost to Income (with LLP) |

Return On Average Capital Employed |

Deposits/Branch |

Gross NPL Ratio |

NPL Coverage |

Tangible Common Ratio |

Non Funded Income /Revenue |

|

SCBK |

44.4% |

52.0% |

11.3% |

7.4 |

16.4% |

81.1% |

14.7% |

35.1% |

|

NCBA Group |

56.0% |

65.6% |

8.1% |

6.2 |

14.7% |

65.0% |

12.8% |

44.3% |

|

Equity Bank |

61.7% |

54.4% |

18.9% |

2.4 |

12.1% |

55.5% |

11.8% |

42.3% |

|

DTBK |

68.2% |

54.0% |

5.7% |

2.3 |

10.6% |

46.5% |

15.2% |

23.9% |

|

Stanbic Bank |

69.7% |

56.9% |

13.2% |

9.1 |

15.1% |

63.9% |

13.5% |

46.3% |

|

I&M Holdings |

73.4% |

58.0% |

13.3% |

4.0 |

11.9% |

61.1% |

16.7% |

29.7% |

|

Coop Bank |

75.7% |

64.5% |

12.3% |

2.2 |

15.8% |

58.4% |

15.9% |

31.5% |

|

KCB Group |

79.7% |

60.4% |

13.9% |

2.1 |

14.9% |

61.6% |

14.6% |

27.4% |

|

Absa Bank |

84.9% |

61.3% |

10.2% |

3.1 |

7.5% |

73.4% |

12.6% |

32.3% |

|

HF Group |

96.2% |

129.3% |

(20.4%) |

1.7 |

24.7% |

64.7% |

14.3% |

22.2% |

|

Weighted Average Q1'2021 |

69.2% |

58.7% |

13.8% |

3.4 |

13.5% |

62.0% |

13.8% |

35.4% |

The overall ranking was based on a weighted average ranking of Franchise value (accounting for 60.0%) and intrinsic value (accounting for 40.0%). The Intrinsic Valuation is computed through a combination of valuation techniques, with a weighting of 40.0% on Discounted Cash-flow Methods, 35.0% on Residual Income and 25.0% on Relative Valuation, while the Franchise ranking is based on banks operating metrics, meant to assess efficiency, asset quality, diversification, and profitability, among other metrics. The overall Q1’2021 ranking is as shown in the table below:

|

Bank |

Franchise Value Rank |

Intrinsic Value Rank |

Weighted Rank |

FY'2020 |

Q1'2021 |

|

I&M Holdings |

1 |

1 |

1.0 |

1 |

1 |

|

KCB Group Plc |

2 |

3 |

2.6 |

3 |

2 |

|

Equity Group |

6 |

2 |

3.6 |

2 |

3 |

|

Stanbic Bank/Holdings |

4 |

7 |

5.8 |

6 |

4 |

|

ABSA |

3 |

8 |

6.0 |

4 |

5 |

|

NCBA Group Plc |

9 |

4 |

6.0 |

9 |

5 |

|

DTBK |

8 |

5 |

6.2 |

5 |

7 |

|

Co-operative Bank of Kenya |

7 |

6 |

6.4 |

7 |

8 |

|

SCBK |

5 |

9 |

7.4 |

8 |

9 |

|

HF Group Plc |

10 |

10 |

10.0 |

10 |

10 |

Major Changes from the FY’2020 Ranking are:

- Stanbic Holdings recorded an improvement in the overall ranking, coming in at position 4 from position 6 in FY’2020 attributable to a 19.3% increase in the group’s Non-Funded Income which contributed to an increase in the bank’s franchise value score, coupled with an improvement in the group’s NPL coverage which recorded a 3.3% points increase to 63.9% from 60.6% recorded in FY’2020,

- NCBA’s rank improved to position 5 from position 9 in FY’2020 attributable to a 30.1% decline in Loan Loss Provision, which contributed to an increase in the bank’s franchise value score, coupled with an Improvement in the bank’s NPL coverage, which recorded a 4.1% points increase to 65.0% from 60.9% in FY’2020, and,

- Diamond Trust Bank Kenya’s (DTB-K) rank declined to Position 7 from Position 5 in FY’2020, mainly due to the bank having the lowest NPL coverage of the listed banks at 46.5% despite the deterioration of asset quality, which saw the bank’s NPL ratio increase by 2.6% points to 10.6% from 8.0% recorded in FY’2020.

For more information, see our Cytonn Q1'2021 Listed Banking Sector Review

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma