Kenya’s Public Debt Review 2023, & Cytonn Weekly #42/2023

By Research Team, Oct 22, 2023

Executive Summary

Fixed Income

During the week, T-bills were oversubscribed for the third consecutive week, with the overall subscription rate coming in at 123.4%, albeit lower than the oversubscription rate of 180.2% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 23.6 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 588.9%, albeit lower than the oversubscription rate of 937.4% recorded the previous week. The subscription rate for the 364-day paper decreased to 22.7%, from 29.6% recorded the previous week while the subscription rate for the 182- day paper increased to 37.9%, from 27.8% recorded the previous week. The government accepted a total of Kshs 27.4 bn worth of bids out of Kshs 29.6 bn of bids received, translating to an acceptance rate of 92.7%. The yields on the government papers continued to rise, with the yields on the 364-day, 182-day and 91-day papers increasing by 0.4 bps, 5.3 bps and 8.5 bps to 15.3%, 15.1% and 15.0%, respectively;

In the primary market, the Central Bank of Kenya released a prospectus inviting bids for the newly issued infrastructure bond IFB1/2023/6.5 with a tenor of 6.5 years. Through the new issue, the government seeks to raise Kshs 50.0 bn to fund infrastructure projects in the FY 2023/24 budget estimates. The bidding process opened on 20th October 2023 and will close on 8th November 2023, with the coupon rate to be determined by the market. The bonds value date will be 13th November 2023, with a maturity date of 6th May 2030 and will be tax free as is the case for infrastructure bonds as provided for under the Income Tax Act. We anticipate the bond to be oversubscribed given its tax-free nature, however we expect investors to bid at higher rates given the country’s debt sustainability concerns. Notably, the last infrastructure bond to be issued was the 7-year IFB1/2023/07 in June 2023 which sought to raise Kshs 60.0 bn. The bond registered an oversubscription rate of 367.5%, at a yield of 15.8%. Based on trading of bonds of similar tenor we expect the IFB1/2023/6.5 to price at 16.3%-16.7%;

Equities

During the week, the equities market recorded mixed performance, with NSE 10 gaining the most by 0.9%, and NSE 25 gaining by 0.3%, while NASI and NSE 20 declined by 0.2% and 0.1% respectively, taking the YTD performance to losses of 26.8%, 11.1%, and 21.6% for NASI, NSE 20, and NSE 25, respectively. The equities market performance was mainly weighed down by losses recorded by large-cap stocks such as Stanbic, KCB Group and Diamond Trust Bank of 5.2%, 4.8% and 2.2% respectively. The losses were however mitigated by gains recorded by stocks such as EABL, Equity Group and NCBA Group of 5.0%, 2.2% and 2.2% respectively;

Real Estate

During the week, the State Department for Housing and Urban Development unveiled details of President William Ruto’s affordable housing programme that will allow salaried workers earning Kshs 150,000 and above per month to acquire homes through the State-funded programme. In the hospitality sector, Miftah Concierge, a leading provider of tailored lifestyle management and luxury travel services based in Dubai expanded its operations into Kenya;

In regulated Real Estate Funds, under the Real Estate Investment Trusts (REITs) segment, ILAM Fahari I-REIT released results for the redemption offer of 36,585,134 units from Non-Professional investors following the conclusion and subsequent lapsing of the conversation offer period by ICEA Lion Asset Managers on Friday 6th October. In the Nairobi Securities Exchange, the trading of ILAM Fahari I-REIT units will remain suspended until Wednesday, 25th October 2023. On the Unquoted Securities Platform, as at 29 September 2023, Acorn D-REIT and I-REIT closed the week trading at Kshs 25.3 and Kshs 21.7 per unit, a 26.6% and 8.3% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 listing price. In addition, Cytonn High Yield Fund (CHYF) closed the week with an annualized yield of 16.1%, remaining relatively unchanged from the previous week;

Focus of the Week

Many countries in the Sub-Saharan Africa region are struggling with debt sustainability as they face a high risk of defaulting on their loans, with countries such as Zambia and Ghana resorting to restructure their debt to avoid complete default. Despite being one of the fastest growing economies in Sub-Saharan Africa with a projected economic growth rate of 5.0%, above the region’s average of 3.6%, Kenya has a high debt burden, facing elevated risk of debt distress with concerns over the repayment of the 10-year 2014 Eurobond issue which is due in June 2024. The debt sustainability concerns have seen credit rating agencies such as Fitch, Moody’s and S&P Global downgrade Kenya’s credit outlook from stable to negative, resulting in higher borrowing costs in the international market. Notably, as of June 2023, Kenya’s total public debt stood at Kshs 10.2 tn with the debt to GDP ratio coming in at 70.2%, 20.2% points above IMF’s recommended threshold of 50.0% for developing countries. Additionally, debt service to revenue ratio stood at 64.3% as of September 2023, 34.3% points above IMF’s recommended threshold of 30.0%, highlighting the stress public debt servicing places on the country’s expenditure. The debt servicing cost has been on the rise given the continued aggressive depreciation of the Kenya shilling, with the shilling having depreciated by 21.4% against the USD on a year to date basis, given that 67.1% of Kenya’s external debt is USD denominated. Consequently, in this week’s topical, we shall focus on the current status of Kenya’s public debt as at the end of the first quarter of the FY’2023/2024. We shall also give our outlook on the country’s debt sustainability given the upcoming USD 2.0 bn Eurobond maturity in June 2024;

Investment Updates:

- Weekly Rates:

- Cytonn Money Market Fund closed the week at a yield of 14.55% p.a To invest, dial *809# or download the Cytonn App from Google Playstore here or from the Appstore here;

- Cytonn High Yield Fund closed the week at a yield of 16.09% p.a. To invest, email us at sales@cytonn.com and to withdraw the interest, dial *809# or download the Cytonn App from Google Playstore here or from the Appstore here;

- We continue to offer Wealth Management Training every Wednesday, from 9:00 am to 11:00 am. The training aims to grow financial literacy among the general public. To register for any of our Wealth Management Trainings, click here;

- If interested in our Private Wealth Management Training for your employees or investment group, please get in touch with us through wmt@cytonn.com;

- Cytonn Insurance Agency acts as an intermediary for those looking to secure their assets and loved ones’ future through insurance namely; Motor, Medical, Life, Property, WIBA, Credit and Fire and Burglary insurance covers. For assistance, get in touch with us through insuranceagency@cytonn.com;

- Cytonn Asset Managers Limited (CAML) continues to offer pension products to meet the needs of both individual clients who want to save for their retirement during their working years and Institutional clients that want to contribute on behalf of their employees to help them build their retirement pot. To more about our pension schemes, kindly get in touch with us through pensions@cytonn.com;

Real Estate Updates:

- For more information on Cytonn’s real estate developments, email us at sales@cytonn.com;

- Phase 3 of The Alma is now ready for occupation and the show house is open daily. To join the waiting list to rent, please email properties@cytonn.com;

- For Third Party Real Estate Consultancy Services, email us at rdo@cytonn.com;

- For recent news about the group, see our news section here;

Hospitality Updates:

- We currently have promotions for Staycations. Visit cysuites.com/offers for details or email us at sales@cysuites.com;

Money Markets, T-Bills Primary Auction:

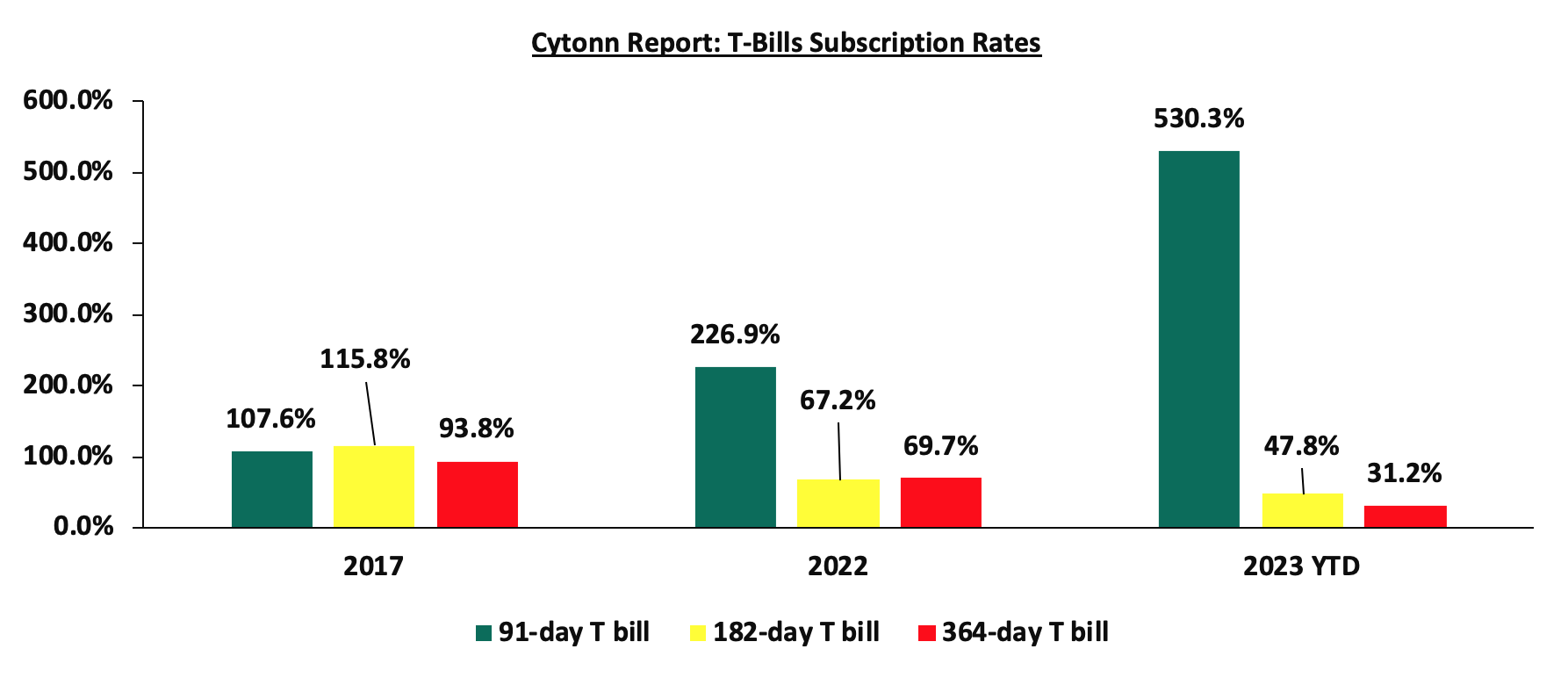

During the week, T-bills were oversubscribed for the third consecutive week, with the overall subscription rate coming in at 123.4%, albeit lower than the oversubscription rate of 180.2% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 23.6 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 588.9%, albeit lower than the oversubscription rate of 937.4% recorded the previous week. The subscription rate for the 364-day paper decreased to 22.7%, from 29.6% recorded the previous week while the subscription rate for the 182- day paper increased to 37.9%, from 27.8% recorded the previous week. The government accepted a total of Kshs 27.4 bn worth of bids out of Kshs 29.6 bn of bids received, translating to an acceptance rate of 92.7%. The yields on the government papers continued to rise, with the yields on the 364-day, 182-day and 91-day papers increasing by 0.4 bps, 5.3 bps and 8.5 bps to 15.3%, 15.1% and 15.0%, respectively; The chart below compares the overall average T- bills subscription rates obtained in 2017, 2022 and 2023 Year to Date (YTD):

In the primary market, the Central Bank of Kenya released a prospectus inviting bids for the newly issued infrastructure bond IFB1/2023/6.5 with a tenor of 6.5 years. Through the new issue, the government seeks to raise Kshs 50.0 bn to fund infrastructure projects in the FY’2023/24 budget estimates. The bidding process opened on 20th October 2023 and will close on 8th November 2023, with the coupon rate to be determined by the market. The bonds value date will be 13th November 2023, with a maturity date of 6th May 2030 and will be tax free as is the case for infrastructure bonds as provided for under the Income Tax Act. We anticipate the bond to be oversubscribed given its tax-free nature, however we expect investors to bid at higher rates given the country’s debt sustainability concerns. Notably, the last infrastructure bond to be issued was the 7-year IFB1/2023/07 in June 2023 which sought to raise Kshs 60.0 bn. The bond registered an oversubscription rate of 367.5%, at a yield of 15.8%. Based on trading of bonds of similar tenor we expect the IFB1/2023/6.5 to price at 16.3%-16.7%.

Money Market Performance:

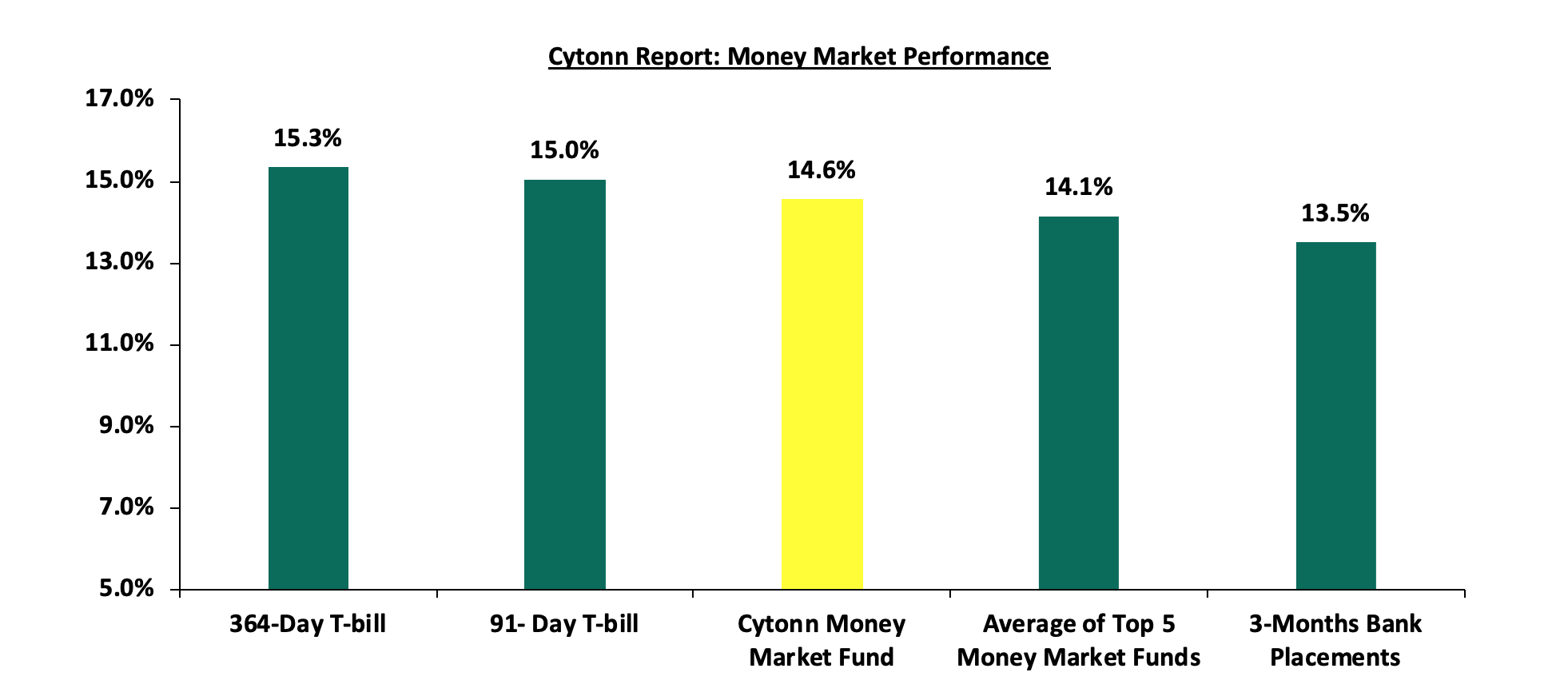

In the money markets, 3-month bank placements ended the week at 13.5% (based on what we have been offered by various banks), and the yields on the 364-day and 91-day T-bill increased by 0.4 bps and 8.5 bps to 15.3% and 15.0%, respectively. The yields of the Cytonn Money Market Fund increased by 6.0 bps to 14.6% from 14.5% recorded the previous week, and the average yields on the Top 5 Money Market Funds increased by 11.8 bps to 14.1%, from 14.0% recorded the previous week.

The table below shows the Money Market Fund Yields for Kenyan Fund Managers as published on 20th October 2023:

|

Cytonn Report: Money Market Fund Yield for Fund Managers as published on 20th October 2023 |

||

|

Rank |

Fund Manager |

Effective Annual |

|

1 |

GenAfrica Money Market Fund |

14.7% |

|

2 |

Cytonn Money Market Fund |

14.6% |

|

3 |

Enwealth Money Market Fund |

14.0% |

|

4 |

Apollo Money Market Fund |

13.7% |

|

5 |

Etica Money Market Fund |

13.7% |

|

6 |

Lofty-Corban Money Market Fund |

13.5% |

|

7 |

Madison Money Market Fund |

13.4% |

|

8 |

Jubilee Money Market Fund |

13.1% |

|

9 |

AA Kenya Shillings Fund |

13.0% |

|

10 |

Co-op Money Market Fund |

13.0% |

|

11 |

GenCap Hela Imara Money Market Fund |

12.9% |

|

12 |

Kuza Money Market fund |

12.7% |

|

13 |

Nabo Africa Money Market Fund |

12.7% |

|

14 |

Sanlam Money Market Fund |

12.6% |

|

15 |

Old Mutual Money Market Fund |

12.4% |

|

16 |

KCB Money Market Fund |

11.9% |

|

17 |

Absa Shilling Money Market Fund |

11.6% |

|

18 |

ICEA Lion Money Market Fund |

11.5% |

|

19 |

Equity Money Market Fund |

11.5% |

|

20 |

Dry Associates Money Market Fund |

11.4% |

|

21 |

CIC Money Market Fund |

11.0% |

|

22 |

Orient Kasha Money Market Fund |

11.0% |

|

23 |

Mali Money Market Fund |

10.3% |

|

24 |

British-American Money Market Fund |

9.4% |

Source: Business Daily

Liquidity:

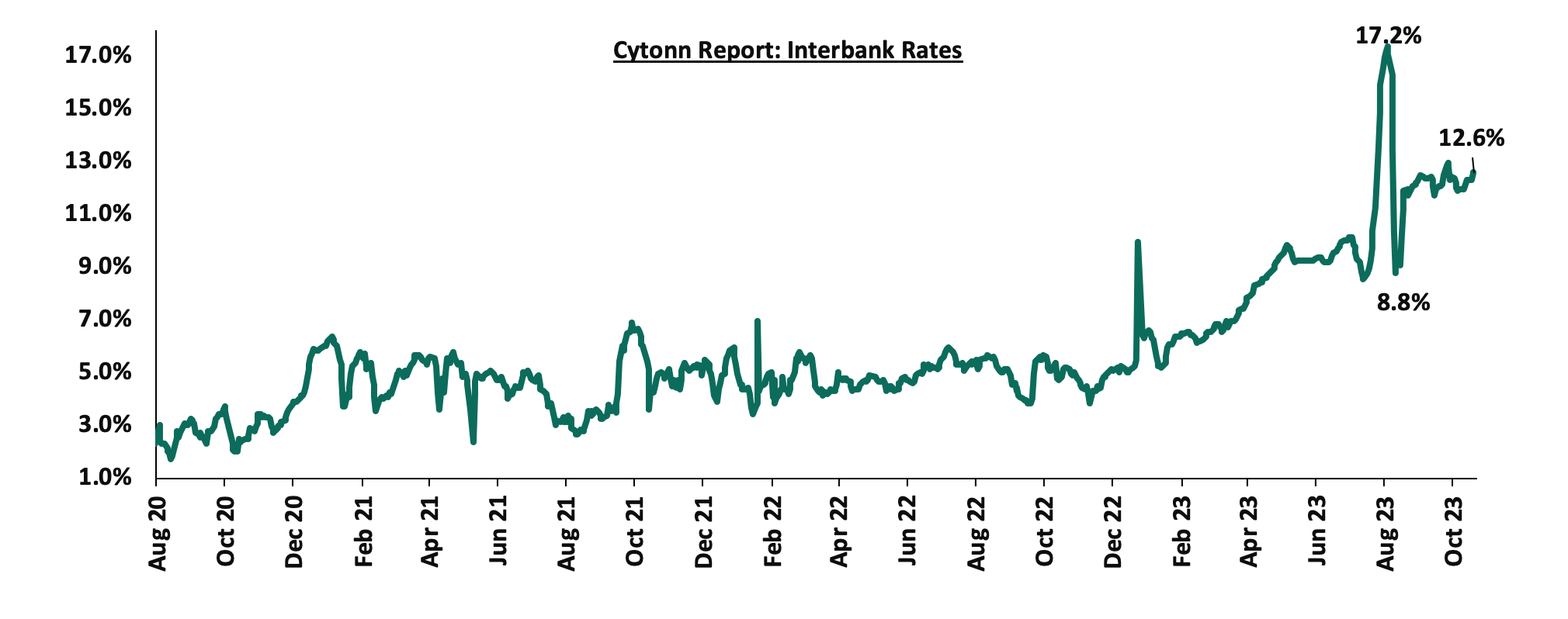

During the week, liquidity in the money markets tightened, with the average interbank rate increasing to 12.5%, from the 12.1% recorded the previous week, partly attributable to tax remittances that offset government payments. The average interbank volumes traded decreased by 33.2% to Kshs 18.1 bn from Kshs 27.1 bn recorded the previous week. The chart below shows the interbank rates in the market over the years:

Kenya Eurobonds:

During the week, the yields on Eurobonds recorded mixed performance, with the yield on the 10-year Eurobond issued in 2014 increasing the most by 1.6% points to 16.5%, from 14.9% recorded the previous week. The table below shows the summary of the performance of the Kenyan Eurobonds as of 18th October 2023;

|

Cytonn Report: Kenya Eurobonds Performance |

||||||

|

|

2014 |

2018 |

2019 |

2021 |

||

|

Tenor |

10-year issue |

10-year issue |

30-year issue |

7-year issue |

12-year issue |

12-year issue |

|

Amount Issued (USD) |

2.0 bn |

1.0 bn |

1.0 bn |

0.9 bn |

1.2 bn |

1.0 bn |

|

Years to Maturity |

0.7 |

4.4 |

24.4 |

3.6 |

8.6 |

10.7 |

|

Yields at Issue |

6.6% |

7.3% |

8.3% |

7.0% |

7.9% |

6.2% |

|

02-Jan-23 |

12.9% |

10.5% |

10.9% |

10.9% |

10.8% |

9.9% |

|

02-Oct-23 |

19.0% |

13.5% |

12.6% |

14.6% |

12.9% |

12.5% |

|

12-Oct-23 |

14.9% |

13.5% |

12.5% |

14.1% |

12.8% |

12.4% |

|

13-Oct-23 |

15.0% |

13.5% |

12.4% |

14.1% |

12.8% |

12.4% |

|

16-Oct-23 |

15.0% |

13.5% |

12.4% |

14.1% |

12.8% |

12.4% |

|

17-Oct-23 |

15.9% |

13.8% |

12.6% |

14.6% |

13.0% |

12.6% |

|

18-Oct-23 |

16.5% |

13.1% |

12.8% |

15.0% |

13.3% |

12.9% |

|

Weekly Change |

1.6% |

(0.4%) |

0.4% |

0.9% |

0.5% |

0.5% |

|

MTD Change |

(2.5%) |

(0.3%) |

0.2% |

0.5% |

0.5% |

0.4% |

|

YTD Change |

3.6% |

2.7% |

2.0% |

4.1% |

2.6% |

3.1% |

Source: Central Bank of Kenya (CBK) and National Treasury

Kenya Shilling:

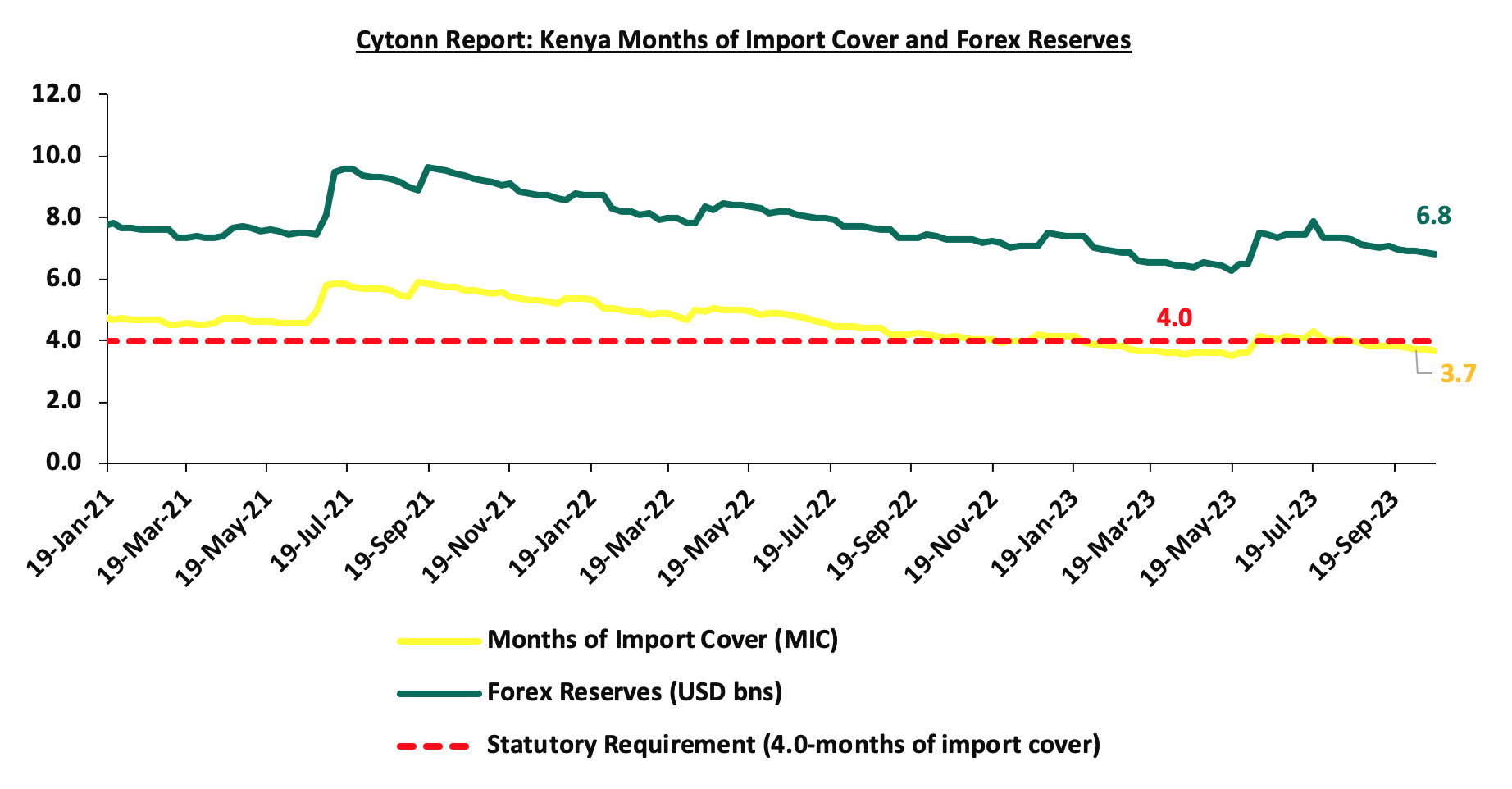

During the week, the Kenya Shilling depreciated against the US Dollar by 0.4% to close at Kshs 149.8, from Kshs 149.1 recorded the previous week. On a year to date basis, the shilling has depreciated by 21.4% against the dollar, adding to the 9.0% depreciation recorded in 2022. We expect the shilling to remain under pressure in 2023 as a result of:

- An ever-present current account deficit which came at 3.7% of GDP in Q2’2023 from 6.0% recorded in a similar period last year,

- The need for government debt servicing, continues to put pressure on forex reserves given that 67.1% of Kenya’s external debt was US Dollar denominated as of June 2023, and,

- Dwindling forex reserves currently at USD 6.8 bn (equivalent to 3.7-months of import cover), which is below the statutory requirement of maintaining at least 4.0-months of import cover.

The shilling is however expected to be supported by:

- Diaspora remittances standing at a cumulative USD 3,106.7 mn in 2023 as of September 2023, 3.8% higher than the USD 2,992.5 mn recorded over the same period in 2022, which has continued to cushion the shilling against further depreciation. In the September 2023 diaspora remittances figures, North America remained the largest source of remittances to Kenya accounting for 57.0% in the period, and,

- The tourism inflow receipts which came in at USD 268.1 bn in 2022, a significant 82.9% increase from USD 146.5 bn inflow receipts recorded in 2021.

The chart below summarizes the evolution of Kenya months of import cover over the years:

Rates in the Fixed Income market have been on an upward trend given the continued high demand for cash by the government and the occasional liquidity tightness in the money market. The government is 24.7% behind of its prorated net domestic borrowing target of Kshs 91.2 bn, having a net borrowing position of Kshs 68.6 bn of the domestic net borrowing target of Kshs 316.0 bn for the FY’2023/2024. Therefore, we expect a continued upward readjustment of the yield curve in the short and medium term, with the government looking to bridge the fiscal deficit through the domestic market. Owing to this, our view is that investors should be biased towards short-term fixed-income securities to reduce duration risk

Market Performance:

During the week, the equities market recorded mixed performance, with NSE 10 gaining the most by 0.9%, and NSE 25 gaining by 0.3%, while NASI and NSE 20 declined by 0.2% and 0.1% respectively, taking the YTD performance to losses of 26.8%, 11.1%, and 21.6% for NASI, NSE 20, and NSE 25, respectively. The equities market performance was mainly weighed down by losses recorded by large-cap stocks such as Stanbic, KCB Group and Diamond Trust Bank of 5.2%, 4.8% and 2.2% respectively. The losses were however mitigated by gains recorded by stocks such as EABL, Equity Group and NCBA Group of 5.0%, 2.2% and 2.2% respectively;

During the week, equities turnover increased by 27.3% to USD 4.0 mn, from USD 3.1 mn recorded the previous week, taking the YTD total turnover to USD 587.3 mn. Foreign investors remained net sellers for the second consecutive week with a net selling position of USD 0.9 mn, from a net selling position of USD 0.1 mn recorded the previous week, taking the YTD foreign net selling position to USD 282.8 mn.

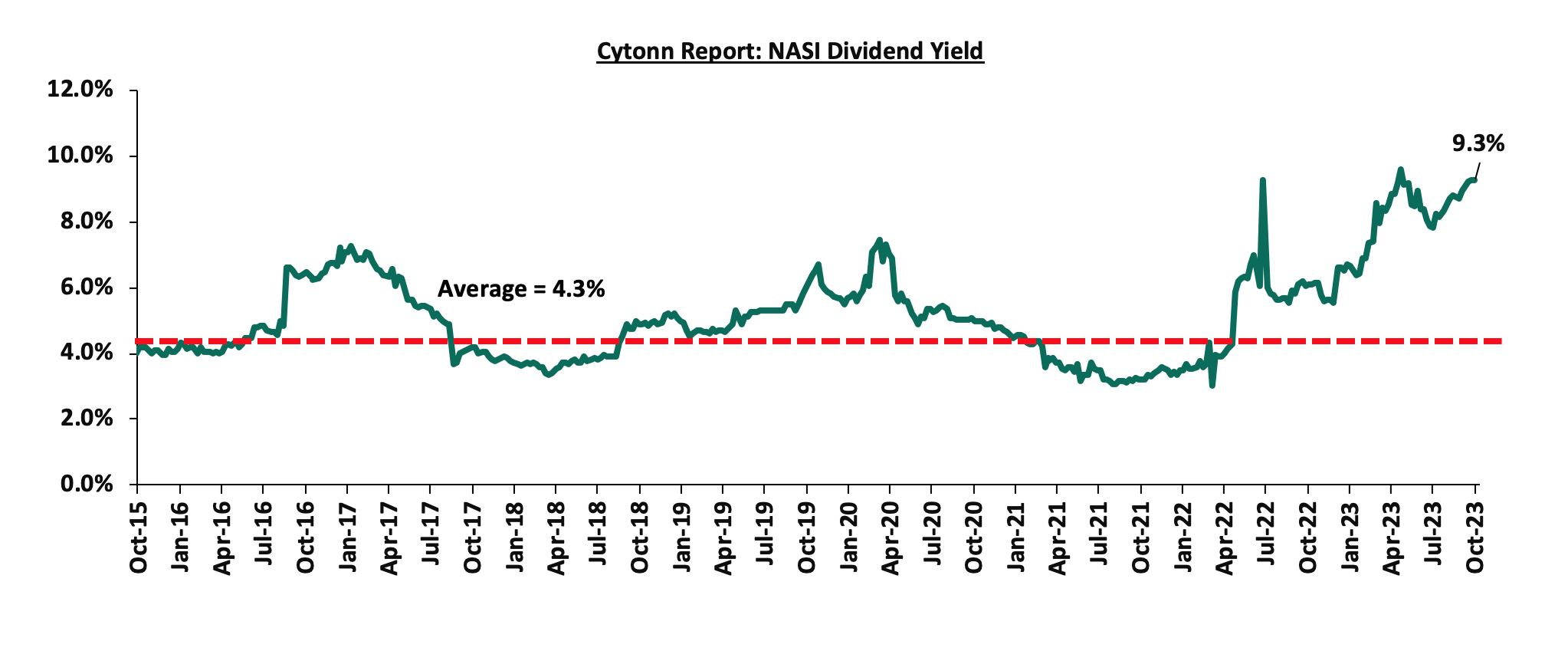

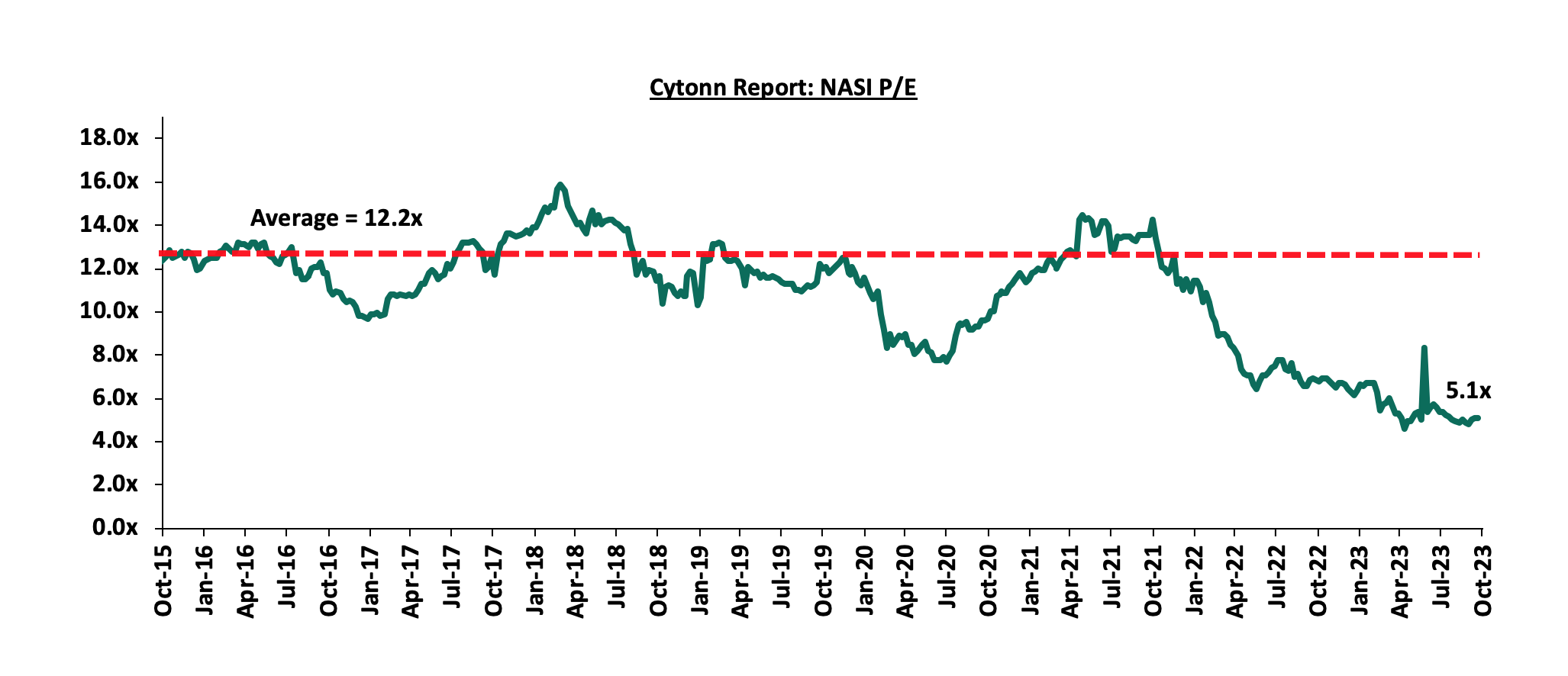

The market is currently trading at a price to earnings ratio (P/E) of 5.1x, 58.4% below the historical average of 12.2x. The dividend yield stands at 9.3%, 5.0% points above the historical average of 4.3%. Key to note, NASI’s PEG ratio currently stands at 0.7x, an indication that the market is undervalued relative to its future growth. A PEG ratio greater than 1.0x indicates the market is overvalued while a PEG ratio less than 1.0x indicates that the market is undervalued. The charts below indicate the historical P/E and dividend yields of the market;

Universe of Coverage:

|

Cytonn Report: Equities Universe of Coverage |

|||||||||

|

Company |

Price as at 13/10/2023 |

Price as at 19/10/2023 |

w/w change |

YTD Change |

Target Price* |

Dividend Yield |

Upside/ Downside** |

P/TBv Multiple |

Recommendation |

|

KCB Group*** |

20.9 |

19.9 |

(4.8%) |

(48.1%) |

30.7 |

10.1% |

64.3% |

0.3x |

Buy |

|

Liberty Holdings |

4.0 |

3.8 |

(5.0%) |

(24.6%) |

5.9 |

0.0% |

55.8% |

0.3x |

Buy |

|

Kenya Reinsurance |

1.8 |

1.8 |

(0.6%) |

(5.3%) |

2.5 |

11.3% |

53.1% |

0.1x |

Buy |

|

Jubilee Holdings |

193.5 |

186.0 |

(3.9%) |

(6.4%) |

260.7 |

6.5% |

46.6% |

0.3x |

Buy |

|

I&M Group*** |

17.6 |

17.7 |

0.9% |

3.8% |

21.8 |

12.7% |

35.9% |

0.4x |

Buy |

|

Diamond Trust Bank*** |

47.6 |

46.5 |

(2.2%) |

(6.7%) |

58.1 |

10.8% |

35.7% |

0.2x |

Buy |

|

ABSA Bank*** |

11.9 |

12.0 |

0.4% |

(2.0%) |

14.8 |

11.3% |

35.1% |

1.0x |

Buy |

|

Sanlam |

7.7 |

7.7 |

0.0% |

(19.6%) |

10.3 |

0.0% |

33.6% |

2.2x |

Buy |

|

CIC Group |

2.1 |

2.0 |

(5.7%) |

4.7% |

2.5 |

6.5% |

31.5% |

0.6x |

Buy |

|

Co-op Bank*** |

11.6 |

11.6 |

0.0% |

(4.1%) |

13.5 |

12.9% |

29.3% |

0.5x |

Buy |

|

Britam |

4.5 |

4.6 |

3.6% |

(11.0%) |

6.0 |

0.0% |

28.9% |

0.6x |

Buy |

|

Equity Group*** |

36.5 |

37.3 |

2.2% |

(17.3%) |

42.6 |

10.7% |

25.1% |

0.8x |

Buy |

|

Standard Chartered*** |

163.5 |

160.0 |

(2.1%) |

10.3% |

170.9 |

13.8% |

20.6% |

1.1x |

Buy |

|

Stanbic Holdings |

115.0 |

109.0 |

(5.2%) |

6.9% |

118.2 |

11.6% |

20.0% |

0.8x |

Buy |

|

NCBA*** |

39.0 |

39.8 |

2.2% |

2.2% |

43.2 |

10.7% |

19.2% |

0.8x |

Accumulate |

|

HF Group |

4.2 |

4.3 |

0.7% |

35.6% |

3.2 |

0.0% |

(25.1%) |

0.2x |

Sell |

We are “Neutral” on the Equities markets in the short term due to the current tough operating environment and huge foreign investor outflows, and, “Bullish” in the long term due to current cheap valuations and expected global and local economic recovery.

With the market currently being undervalued to its future growth (PEG Ratio at 0.7x), we believe that investors should reposition towards value stocks with strong earnings growth and that are trading at discounts to their intrinsic value. We expect the current high foreign investors sell-offs to continue weighing down the equities outlook in the short term.

- Residential Sector

During the week, the State Department for Housing and Urban Development unveiled details of President William Ruto’s affordable housing plan that will allow salaried workers earning Kshs 150,000 and above per month to acquire homes through the State-funded program. Under the plan which will be spearheaded by the State Department of Housing and Urban Development, units will be classed under three main categories namely; i) Social Housing targeting residents in informal settlements, ii) Affordable Housing Plan (AHP), and, iii) Market-Driven units which will be priced based on prevailing market rates of similar units. The table below summarizes the details of the various housing categories;

|

Cytonn Report: Details of Various Housing Categories under President Ruto’s Housing Program |

|||||||

|

# |

Category |

Typology |

Size (SQM) |

Price (Kshs) |

Interest Rate |

Price Per SQM (Kshs) |

Set Monthly Payments (Kshs) |

|

1 |

Social Housing |

1-Bedroom |

20 |

0.8 mn |

3% |

42,000 |

3,200 |

|

2-Bedroom |

30 |

1.3 mn |

3% |

42,000 |

4,800 |

||

|

3-Bedroom |

40 |

1.7 mn |

3% |

42,000 |

6,400 |

||

|

2 |

Affordable Housing Plan (AHP) |

Studio |

20 |

1.0 mn |

6% |

48,000 |

5,200 |

|

2-Bedroom |

40 |

1.9 mn |

6% |

48,000 |

10,400 |

||

|

3-Bedroom |

60 |

2.9 mn |

6% |

48,000 |

15,600 |

||

|

3 |

Market- Driven Units |

2-Bedroom |

60 |

4.3 mn |

9% |

72,000 |

31,300 |

|

3-Bedroom |

80 |

5.8 mn |

9% |

72,000 |

41,800 |

||

|

|

Average |

|

|

2.5 mn |

|

51,750 |

|

Source: State Department for Housing and Urban Development (SDHUD)

Units categorized as affordable housing will constitute 50.0% of total housing units to be constructed under the program, whereas market rate apartments and social housing units will take up 30.0% and 20.0% respectively. Notably, the re-classification differs from the previous regime’s, replacing one-bedroom units under the AHP with studios, and aims to deliver 250,000 units annually. This is in contrast to an initial target of 500,00 units in 5 years from 2017 to 2022 by the previous government.

The prices of units which will be sold under the Tenant Purchase Scheme (TPS) will be based upon costs of construction, plus 20.0% financing costs and a varying markup depending on the housing category. The markup or profit for the different category units has been set at; 9.4% for social housing, 14.3% for AHP and 20.0% for market rate apartments. Under the scheme, purchasers will be required to pay a 10.0% deposit, and clear the remaining balance with monthly payments ranging from Kshs 3,200 to 41,800 over a period of 30 years to eventually become homeowners. Units under the market rate segment will attract the highest interest rate of 9.0%, while units under the social housing and AHP categories will each attract interest rates of 3.0% and 6.0% respectively, on a reducing balance.

For purposes of assessing monthly repayments, assuming a 3.0% interest rate and a 30-year tenor, to purchase a home under the social housing category, individuals will pay Kshs 3,188, Kshs 4,781 and Kshs 6,375 monthly to acquire a one bedroom, two bedroom and three-bedroom house respectively. To acquire a house under the AHP category, assuming an interest rate of 6.0%, buyers will pay monthly payments of Kshs 5,181, Kshs 10,361 and Kshs 15,541 for a studio, two bedroom and three bedrooms unit respectively over a period of 30 years. For market rate apartments units, attracting a 9.0% interest rate, purchasers will pay monthly payments of Kshs 31,284 and Kshs 41,712 for two bedroom and three bedrooms respectively to become eventual homeowners of the units over a duration of 30 years. However, notwithstanding, individuals earning salaries above Kshs 150,000 will be subject to higher interest and financing rates.

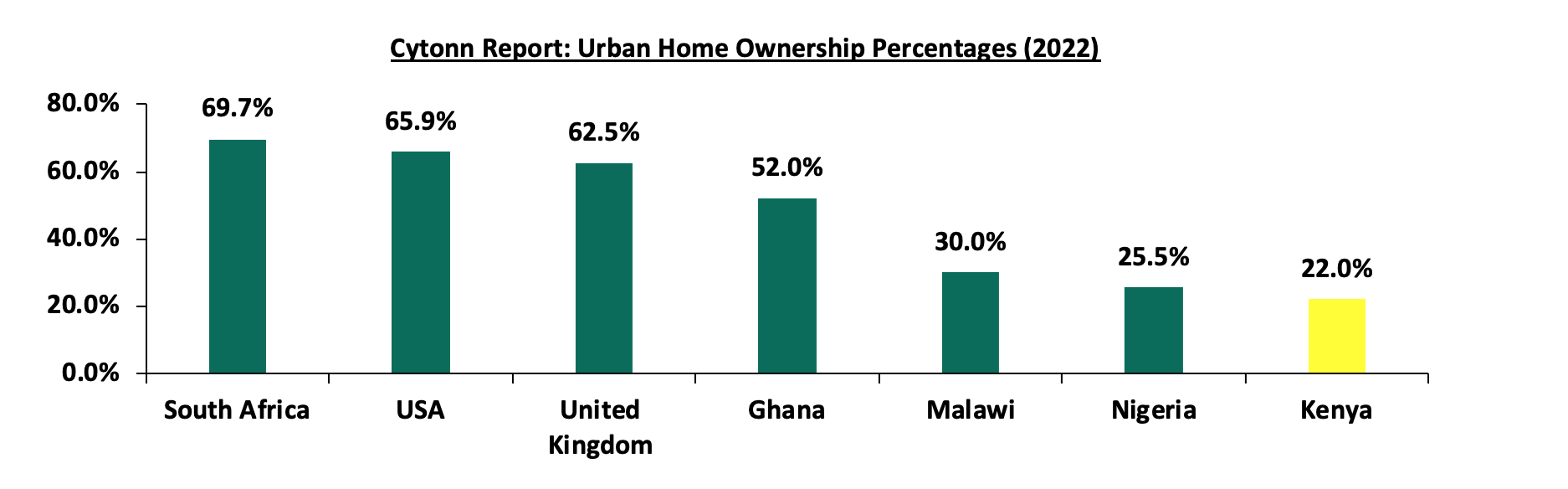

We expect that the program will; i) contribute towards bridging the housing deficit which stands at 80.0%, according to the Center for Affordable Housing Finance Africa (CAHF), ii) promote home ownership rates in the country, particularly in urban areas which have remained low at 22.0% compared to other African countries, iii) improve the living standards of residents especially in informal settlements by delivering high quality affordable homes, and, iv) contribute towards the reduction of unemployment rates in the country, by creating both direct and indirect jobs. The graph below shows urban homeownership percentage for different countries in comparison to Kenya;

- Hospitality Sector

During the week, Miftah Concierge, a leading provider of tailored lifestyle management and luxury travel services based in Dubai expanded its operations into Kenya. The move is part of the firm’s ambitious expansion strategy into Africa, using Kenya as a strategic base to initiate growth and operations across the continent. Miftah Concierge is set to inject an initial capital investment of USD 2.0 mn (Kshs 299.2 mn) into its operations in Kenya to ensure a strong and seamless launch for its Kenyan office. Miftah’s decision is driven by its desire to capitalize on the growing demand for luxury services on the continent, aiming to serve a sophisticated and selective luxury travel clientele throughout the African continent. The expansion comes at a time when the Kenyan hospitality sector is increasingly witnessing continuous openings and expansions by local and international hotel chains brands such as such as JW Marriott of the Bonvoy Global and Pan Pacific Hotels Group, and an increase in the number of developments in the pipeline by international hotel chains, according to the Hotel Chains Development Pipelines in Africa 2023 Report.

We expect the expansion will boost performance of Kenya’s hospitality industry by; i) enhancing the country’s tourism offerings potentially attracting high-end travelers into the country, ii) increase Kenya’s attractiveness as a luxury destination for high-net worth individuals and luxury travelers, iii) creating job opportunities in the sector, and, iv) promote economic growth as increased luxury tourism will result in higher average spending per visitor, leading to a boost in revenue for businesses in the hospitality industry.

- Real Estate Regulated Funds

- Real Estate Investments Trusts (REITs)

During the week, ILAM Fahari I-REIT released results for the redemption offer of 36,585,134 units from Non-Professional investors following the conclusion and subsequent lapsing of the conversion offer period by ICEA Lion Asset Managers (ILAM) on Friday 6th October. The following were the key take-outs;

- ILAM Fahari I-REIT received applications for redemption of 41,371,604 units from Non-Professional investors. This represented an overall subscription rate of 113.1% against the 36,585,134 units offered for redemption at an offer price of Kshs 11.0 by ILAM,

- ILAM Fahari will redeem a total of 36,161,059 units, against the total 36,583,004 units set to be redeemed, representing a redemption rate of 88.4%. The additional 421,945 units will be allocated to Non-Professional investors for purposes of topping up their holdings to the Professional investor threshold,

- The remaining 4,788,600 units out of the 41,371,604 units submitted for redemption were not redeemed as they constituted units held by Professional investors whose names appeared on the register at record date of Friday 1st September 2023. According to the Conversion Offering Memorandum, only Non-Professional Investors can participate in the conversion and redeem their units. Thus, in order to ensure compliance with the REIT Regulations, the redemption offer is only open to Non-Professional investors who were part of the Register as of the Record Date, and,

- The transaction will result in ICEA LION Asset Management increasing its unitholding to 22.7% post redemption, purchasing an additional 19.9% of units valued at Kshs 397.8 mn. This will significantly increase ILAM’s holding from its initial of 2.8%.

In the Nairobi Securities Exchange, the trading of ILAM Fahari I-REIT units remained suspended, with effect from Friday 6th October upon the conclusion and subsequent lapsing of the conversion offer period by ILAM. The trading of ILAM Fahari I-REIT units will remain suspended until 25th October 2023 to facilitate for reconciliation after which the suspension will be lifted. This comes a month after the Capital Markets Authority (CMA) gave its approval for the conversion of ILAM Fahari Income Real Estate Investment Trust (REIT) from the Unrestricted Main Market segment of the Nairobi Securities Exchange (NSE) into the Restricted Market Segment through a Conversion Offering Memorandum. Following this and approval of the results from the redemption process by the CMA, the I-REIT will be delisted from the Unrestricted Main Investment Market Segment (UMIMS) of the Nairobi Securities Exchange (NSE) on 4th December 2023 and subsequently, ILAM Fahari I-REIT units will be quoted on the Unquoted Securities Platform (USP) on 22nd January 2024. For more information, please see our Cytonn Monthly – August 2023, and Cytonn Weekly #36/2023.

In the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 25.3 and Kshs 21.7 per unit, respectively, as at 29th September 2023. The performance represented a 26.6% and 8.3% gain for the D-REIT and I-REIT, respectively, from the Kshs 20.0 inception price. The volumes traded for the D-REIT and I-REIT came in at 12.3 mn and 30.6 mn shares, respectively, with a turnover of Kshs 257.5 mn and Kshs 632.1 mn, respectively, since inception in February 2021.

REITs provide various benefits like tax exemptions, diversified portfolios, and stable long-term profits. However the continuous deterioration in performance of the Kenyan REITs and restructuring of their business portfolio hampering major investment they had previously made are on top of other general challenges such as; i) inadequate comprehension of the investment instrument among investors, ii) prolonged approval processes for REITs creation, iii) high minimum capital requirements of Kshs 100.0 mn for trustees, and, iv) minimum investment amounts set at Kshs 5.0 mn, continue to limit the performance of the Kenyan REITs market.

- Cytonn High Yield Fund (CHYF)

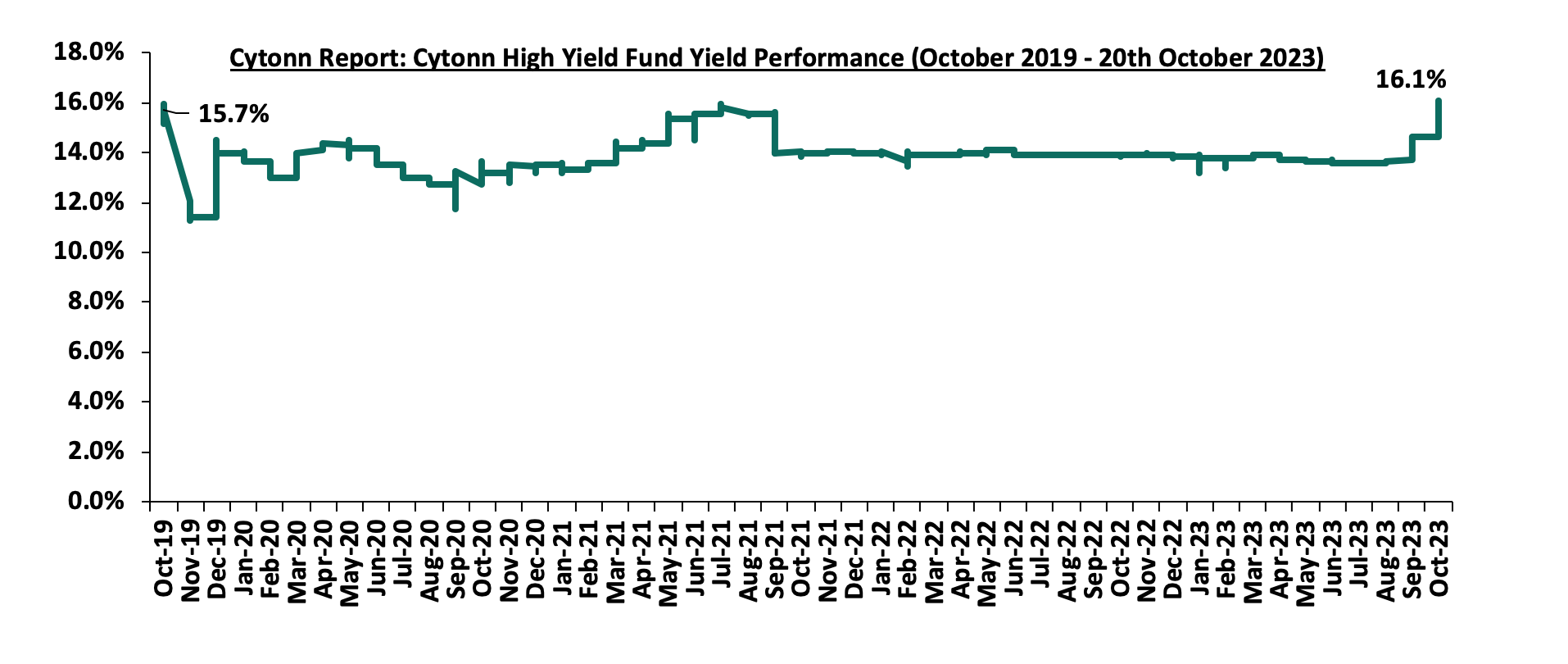

Cytonn High Yield Fund (CHYF) closed the week with an annualized yield of 16.1% remaining relatively unchanged from the previous week. The performance represented a 2.2%-points Year-to-Date (YTD) increase from 13.9% yield recorded on 1st January 2023, and 0.4%-points Inception-to-Date (ITD) increase from the 15.7% yield. The graph below shows Cytonn High Yield Fund’s performance from November 2019 to 20th October 2023;

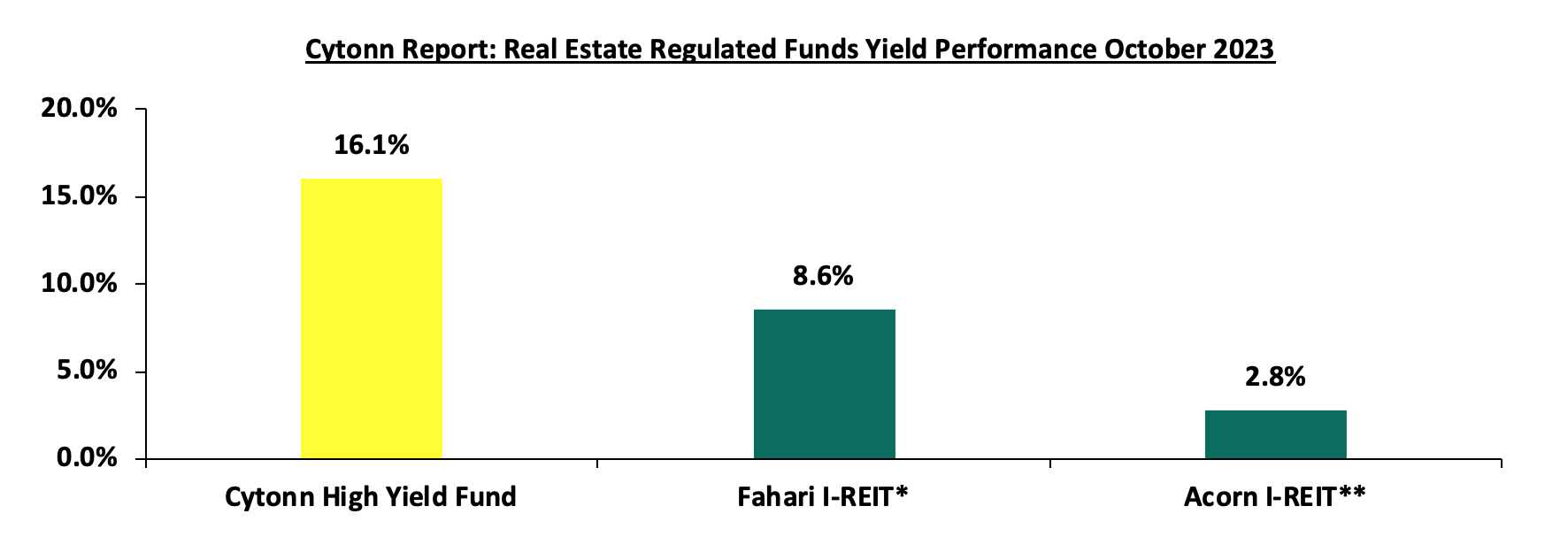

Notably, the CHYF has outperformed other regulated Real Estate funds with an annualized yield of 16.1%, as compared to Fahari I-REIT and Acorn I-REIT with yields of 8.6%, and 2.8% respectively. As such, the higher yields offered by CHYF makes the fund one of the best alternative investment resource in the Real Estate sector. The graph below shows the yield performance of the Regulated Real Estate Funds;

* As at Friday October 6th 2023

**H1’2023

Source: Cytonn Research

We expect the performance of Kenya’s Real Estate sector to be supported by; i) the government’s continued focus and emphasis on the Affordable Housing initiative, ii) continued demand for housing and Real Estate facilitated by the positive demographics which are above global averages, iii) continued expansion activities and recovery of the hospitality sector, and, iv) the strategic positioning of Kenya as a regional hub which continues to attract multi-national businesses and organizations into the country. However, we expect the sector's optimal performance will be hampered by; i) rising construction costs as a result of inflationary pressures, ii) existing oversupply of physical space in select market segments resulting in slower uptake of new spaces, and iii) limited investor knowledge in REITs coupled with high minimum investment amounts among other factors impeding the growth of the asset class.

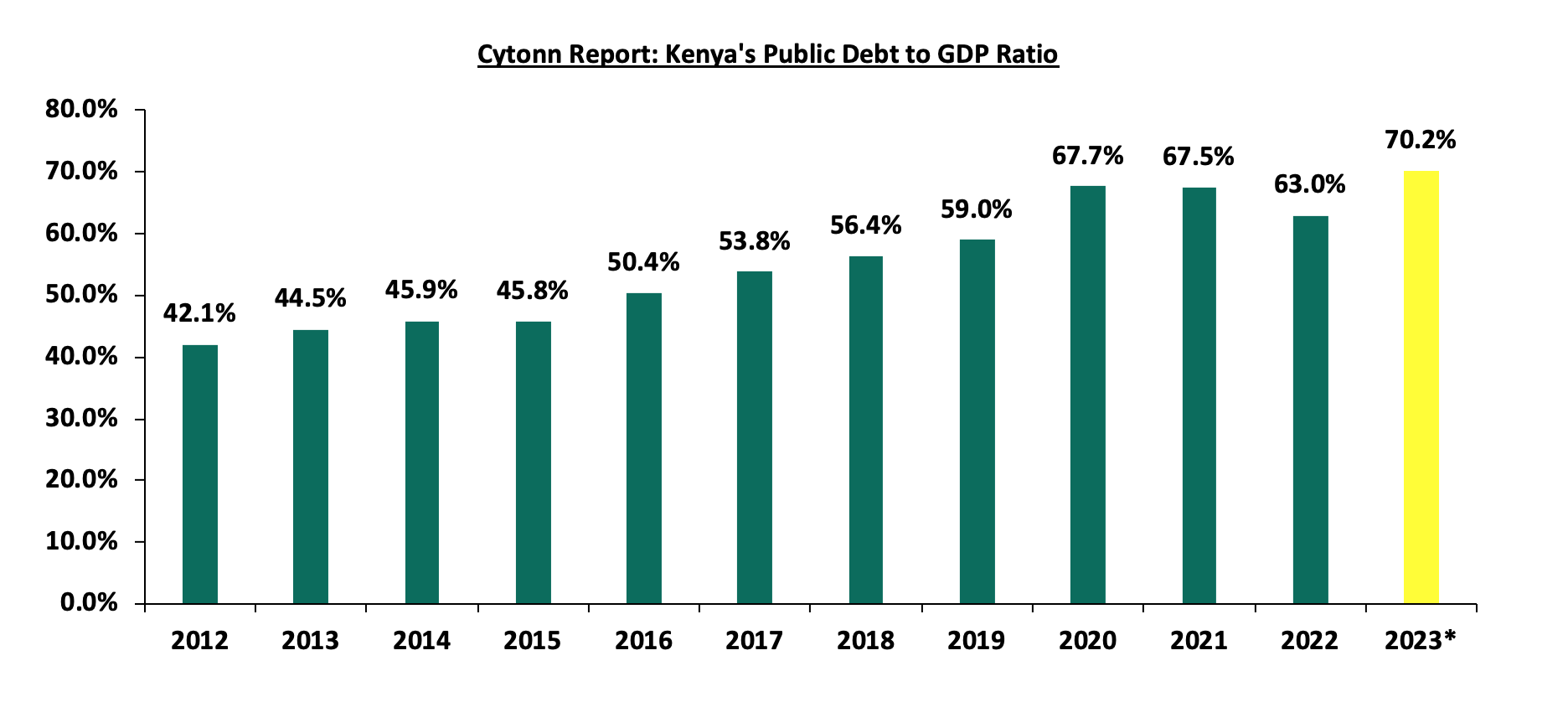

Kenya is one of the fastest growing economies in Sub-Saharan Africa, having registered a growth rate of 5.4% in the second quarter of 2023. However, the country also faces significant challenges in managing its public debt, which has increased rapidly in recent years. According to the latest data from the Central Bank of Kenya (CBK), the total public debt stood at Kshs 10.2 tn as of June 2023, compared to Kshs 8.6 tn recorded in June 2022. This has in turn increased the debt to GDP ratio to 70.2% as of June 2023, 20.1% points higher than the International Monetary Fund (IMF) threshold of 50.0% for developing countries, up from the 66.7% recorded in June 2022. The public debt comprises both external and domestic debt, where the ratio of the external debt to domestic debt remains high at 54.3% to 45.7% as of September 2023. The government has been working on trimming the domestic borrowing so as to ease the pressure on interest rates, with the short-day papers all crossing the 15.0% mark in the current auction results. The reduction in local borrowing is also meant to address the private sector crowding out. The main sources of external debt are multilateral and bilateral creditors, while the main instruments of domestic debt are Treasury bonds and Treasury bills. Likewise, the debt service to revenue ratio has increased over the period to 64.3% as of September 2023, 34.3% points higher than the IMF threshold of 30.0%. Notably, the debt service to revenue ratio hit an all-time high of 101.4% as of July 2023, indicating how debt servicing continues to weigh on the government’s expenditure.

The rising public debt has raised concerns about its sustainability and implications for fiscal and macroeconomic stability. With the upcoming maturity of the USD 2.0 bn Eurobond in June 2024, there are concerns whether the government will meet the debt repayment. This is as the public debt situation continues to deteriorate on the back of high fiscal deficits, and the depreciation of the Kenyan Shilling, which has depreciated by 21.4% on a year to date basis, given that 67.1% of Kenya’s external debt is USD denominated, thus putting more pressure on debt servicing. This has been worsened by the conflict in Eastern Europe, which has raised the expenditure on imports; and the adverse effects of climate change have worsened the fiscal position and debt vulnerability of Kenya.

We have been tracking the evolution of the public debt and below are the most recent topicals we have done on Kenya’s debt:

- Kenya's Public Debt Review 2023: Is Kenya's Public Debt Level Sustainable- In April 2023, we highlighted the state of affairs concerning the country’s public debt and concluded by discussing strategies that the government could implement in order to reduce the economic consequences of high debt levels as well as mitigate the high risk of debt distress,

- Kenya’s Public Debt 2022; Debt Service Coverage- In July 2022, In December 2016, we wrote about Kenya’s debt level, questioning its sustainability, and concluded that the government needed to reduce the amount of public debt, giving suggestions as to how this could be achieved, and,

- Kenya’s Public Debt: On a path to Distress?- In October 2021, we highlighted the state of affairs concerning the country’s public debt profile and levels and concluded that Kenya’s risk of debt distress remained elevated.

In this week’s topical, we shall focus on the current status of Kenya’s public debt as at the end of the first quarter of the FY’2023/2024. We shall look at what are the economic consequences resulting from high debt levels. We shall also give our outlook on the country’s debt sustainability given upcoming USD 2.0 bn Eurobond maturing in June 2024. The report also compares Kenya’s public debt situation with other sub-Saharan countries, using various indicators such as the debt-to-GDP ratio, and the debt service-to-revenue ratio.

This we shall cover as follows;

- The Current State of Kenya’s Public Debt,

- Kenya’s Debt Servicing Cost,

- Economic Consequences of high Debt levels,

- Kenya’s Debt sustainability analysis and projection, and,

- Conclusion and Recommendations.

Section 1: The Current State of Kenya’s Public Debt

According to the Central Bank’s Quarterly Economic Review Report for Q2’2023, Kenya’s public debt stood at Kshs 10.2 tn, (equivalent to 70.2% of GDP) as of June 2023, an 18.8% increase from the Kshs 8.6 tn (66.2% of GDP) recorded in June 2022. Amidst the government’s fiscal consolidation efforts by broadening the tax revenue base and minimizing non-priority expenditures, the public debt to GDP ratio is projected to slightly decline to 60.0% in 2023. However, we expect the government efforts to be impeded by the deteriorated macroeconomic environment as evidenced by the decline in Purchasing Manager’s index to 47.8 in September 2023, down from 50.6 in August 2023, resulting from the high inflationary pressures following a hike in fuel prices, aggressive currency depreciation, and slower economic growth which is expected to stifle revenue collection. Below is a graph highlighting the trend in the Kenya’s debt to GDP ratio over the last 10 years:

Source: National Treasury, *Data as of June 2023

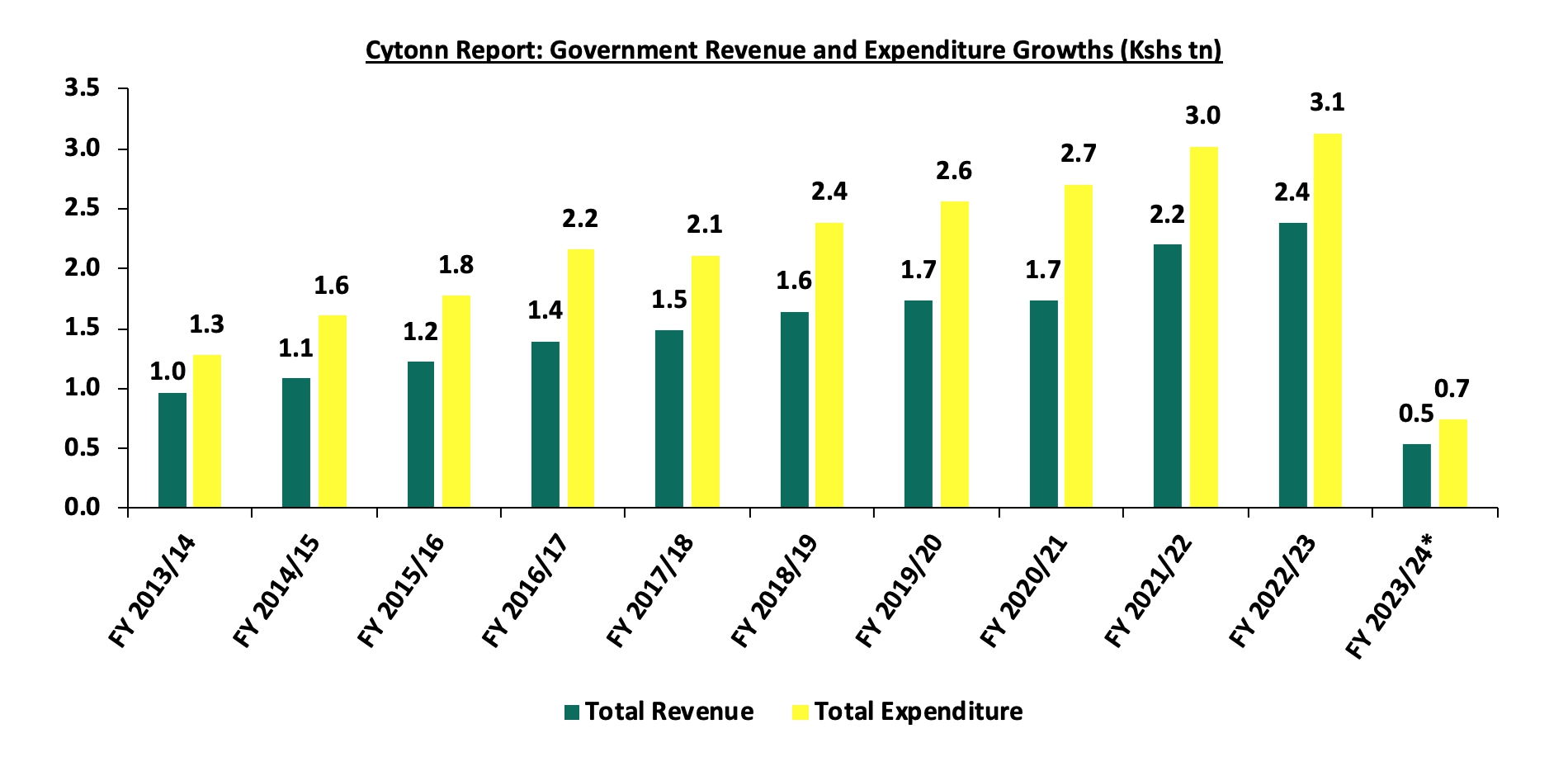

Kenya’s debt level has been on the rise due to the continued growth in fiscal deficits over the years, averaging 7.6% of the GDP for the last 9 financial years, driven by the sustained recurrent expenditure and a focus on development projects. Over a ten-year period, the growth in government revenue registered a 10-year CAGR of 11.2% to Kshs 2.4 tn as at the end of FY’2022/23, from Kshs 0.8 tn at the end of FY’2012/13. This outpaced the growth of government expenditure at a 10-year CAGR of 9.5% to Kshs 3.1 tn at the end of FY’2022/23, from Kshs 1.3 tn at the end of FY’2012/13. The chart below shows the growth in Kenya’s total revenue and expenditure in the last 10 fiscal years:

Source: Central Bank of Kenya, *Data as of September 2023

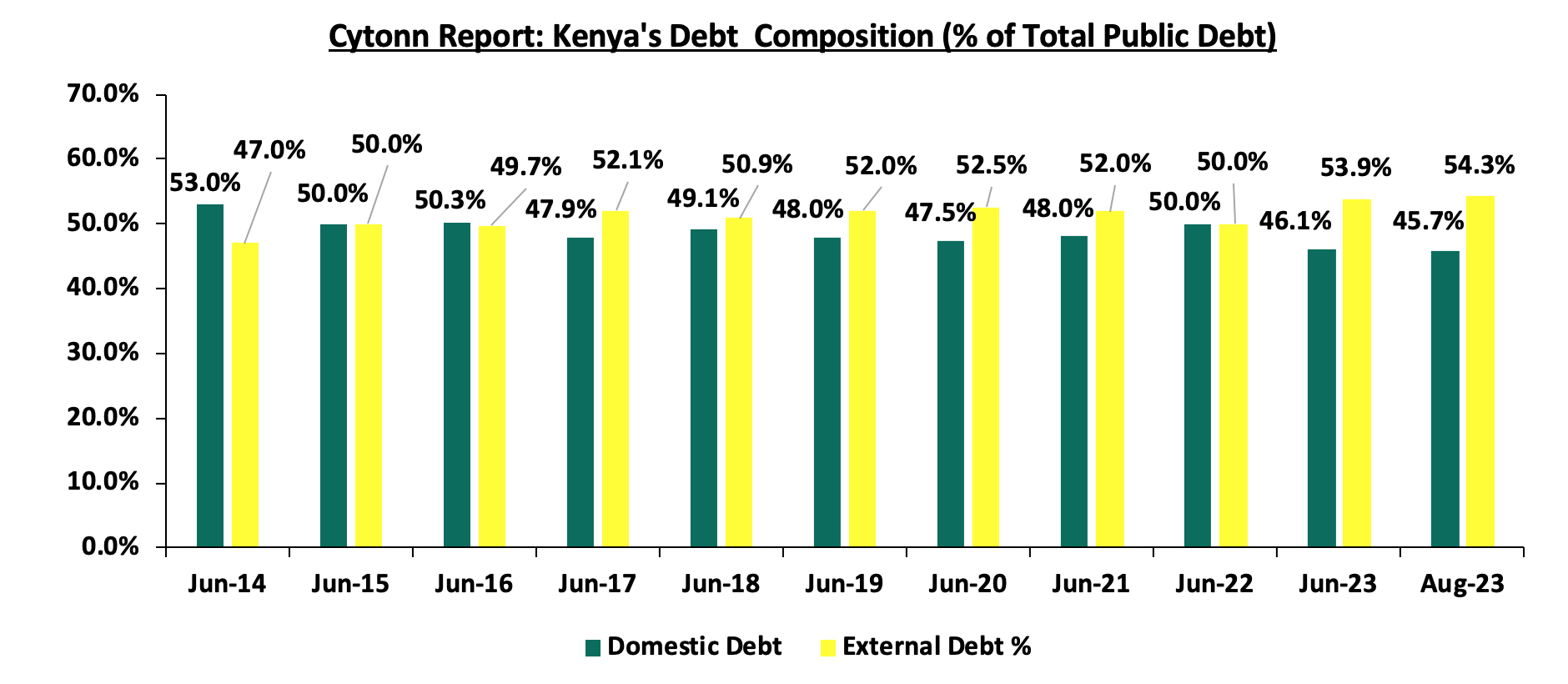

- The Nature of Kenya’s Debt Composition (Domestic vs External)

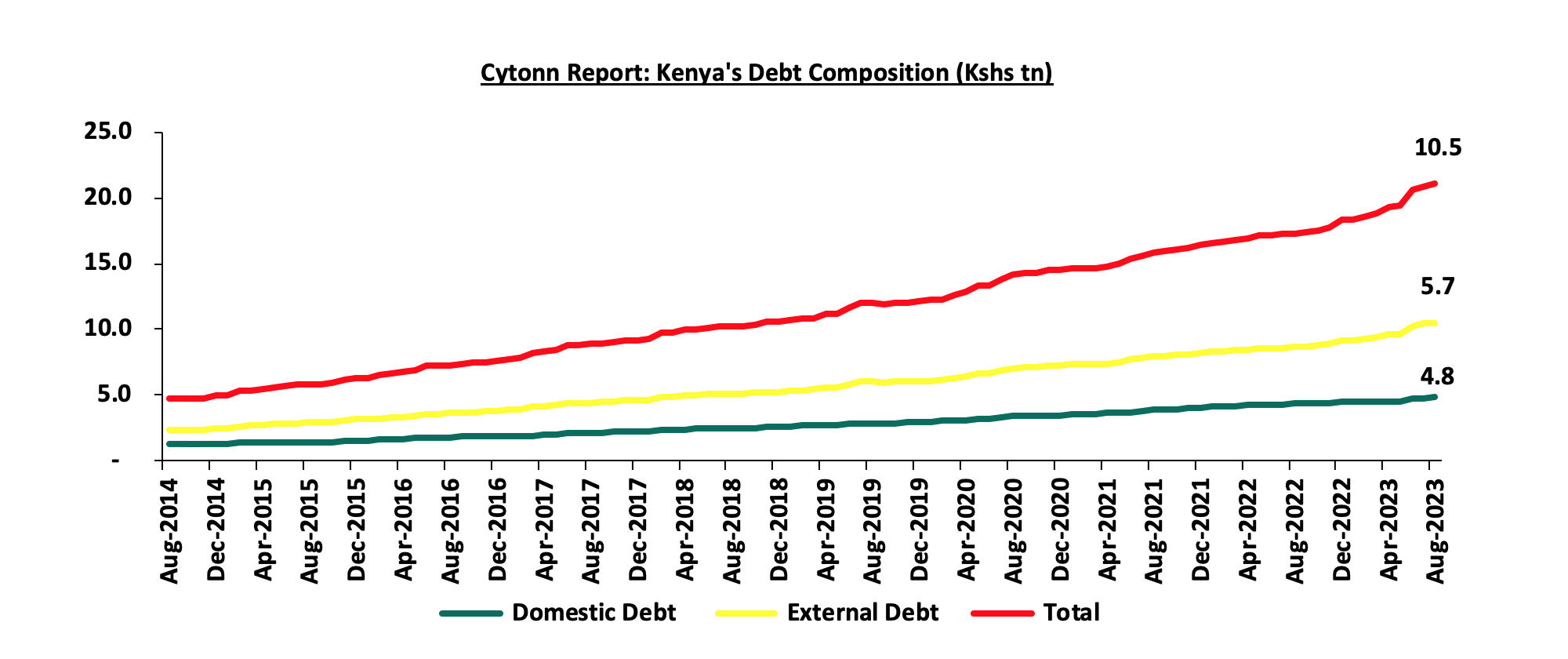

Over the years, Kenya’s debt composition has been evenly distributed between domestic and external borrowing. However, since the beginning of 2023, there has been a shift towards external borrowing with the proportion of external debt against domestic debt standing at 54.3% to 45.7% in September 2023, compared with 49.8% to 50.2% observed over a similar period in 2022. The shift has been brought about by the government’s revision of its domestic borrowing target for the FY202/24 from the initial Kshs 586.5 bn to Kshs 316.0 bn, a move aimed at mitigating the upward pressure on the domestic borrowing rates while at the same time bolstering foreign reserves by increasing the government’s efforts on sourcing for bilateral and multilateral funding. Notably, external debt increased at a 10-year CAGR of 20.5% to Kshs 5.7 tn as at August 2023, from Kshs 0.9 tn in August 2013, higher than the 15.7% CAGR recorded by domestic debt to Kshs 4.8 tn as at August 2023 from Kshs 1.1 tn in August 2013. Below is a graph highlighting the trend in the external and domestic debt composition over the last 10 years;

Source: National Treasury and Central Bank of Kenya

Below is a graph highlighting the composition of domestic and external debt as a percentage of total public debt over the last 10 years:

Source: National Treasury and Central Bank of Kenya

- Public Debt Mix by Holders

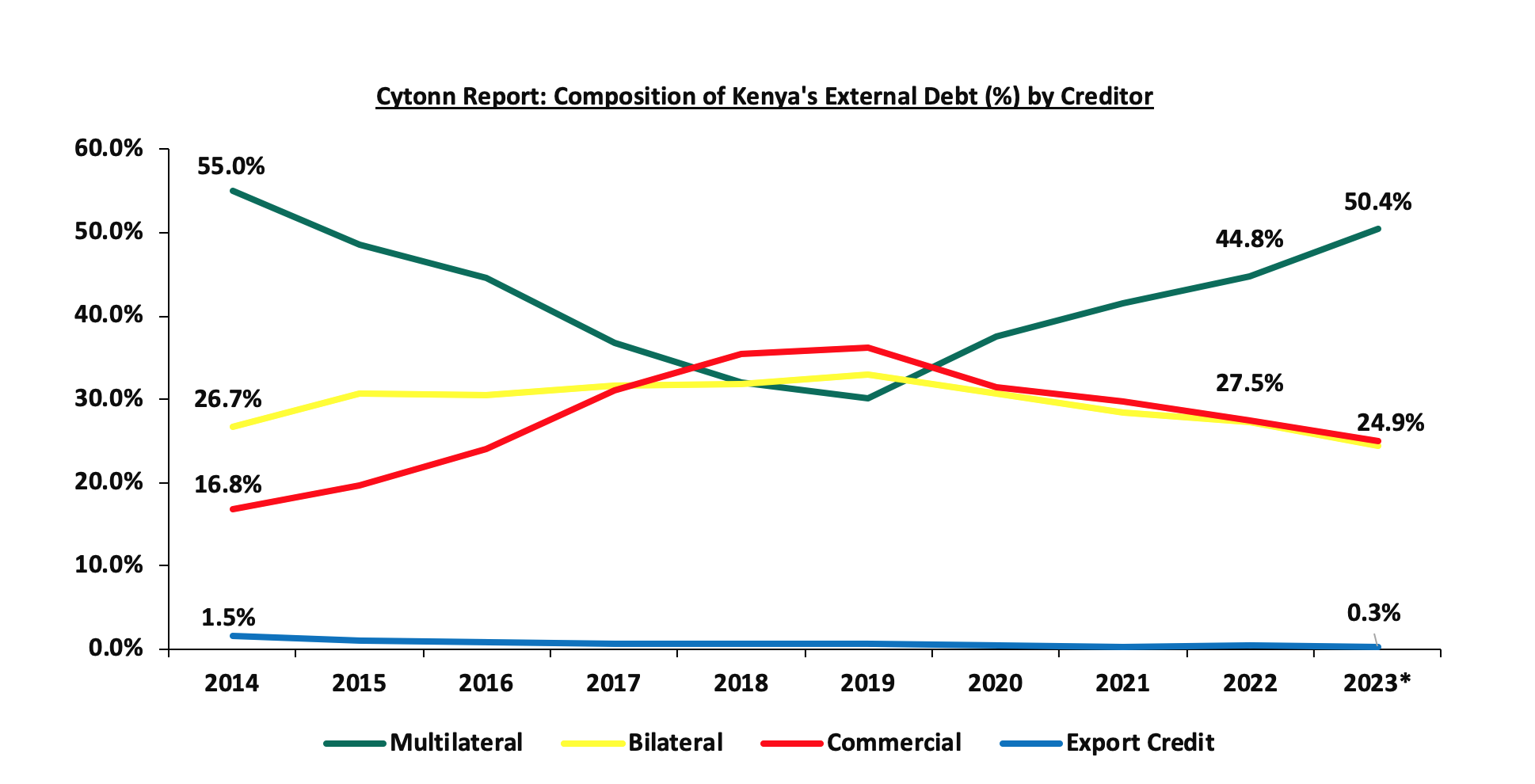

- External Debt Composition by Holders (Bilateral, Multilateral, and Commercial Banks)

Kenya’s external debt stock is mainly composed of multilateral loans, bilateral loans and commercial loans. In FY’2022/23, Kenya’s exposure to multilateral loans recorded a significant growth, attributable to favourable terms offered in terms of low interest rates and longer repayment periods, when compared to bilateral loans and commercial loans. Notably, during the FY’2022/23, Kenya has been unable to issue new Eurobonds due to the increased interest rates making borrowing expensive in the international finance market. The rising Eurobond yields are a result of the heightened perceived risk stemming from economic uncertainties and debt sustainability concerns especially in the Sub-Saharan Africa region with Kenya and Ethiopia facing Eurobond maturities in 2024. The chart below shows external debt composition by Creditors:

Source: National Treasury, *Provisional value as at June 2023

It is key to note that:

- The portion of multilateral debt increased by 5.6% points to 50.4% in June 2023, from 44.8% recorded over a similar period in 2022, due to loans worth USD 1.0 bn (Kshs 138.6 bn) under the Development Policy Operation (DPO) from the World Bank and a total of USD 415.4 mn (Kshs 58.9 bn) from the IMF under the Extended Credit Facility arrangement (EFF/ECF) for budgetary support during the period. This was in addition to the USD 551.4 mn (Kshs 78.1 bn) approved under the Resilience and Sustainability Facility (RSF), following the completion of IMF’s fifth review of the 38-months Extended Fund Facility (EFF) and Extended Credit Facility (ECF) financing. Notably, Bilateral debt decreased by 2.9% points to 24.4% in June 2023, from 27.3% in June 2022,

- Commercial debt as a percentage of external debt reduced by 2.6% points to 24.9% of total external debt in June 2023 from 27.5% in June 2022, mainly attributable to Kenya’s government shunning away from the more expensive debt due to the prevailing market conditions. Notably, Kenya secured a medium-term commercial loan amounting to USD 500.0 mn (Kshs 69.6 bn) in July 2023 from a syndicate of global banks consisting of American Citibank, British Standard Chartered Bank, Stanbic Bank, and South Africa’s RMB Holdings Ltd, and,

- According to the CBK Quarterly Economic Review as at June 2023, 67.1% of the external debt was US Dollar denominated contributing to the increasing debt servicing cost given the shilling’s continuous depreciation having lost against the USD by 21.4% since the year began. The table below shows currency composition of the external debt stock:

Cytonn Report: Currency composition of the External Debt Stock (%)

Currency

June-2022

June-2023

USD

67.9%

67.1%

EUR

18.6%

21.3%

Yen

5.7%

3.9%

Yuan

5.3%

5.1%

GBP

2.3%

2.3%

Other Currencies

0.2%

0.2%

Source: Central Bank of Kenya

- Domestic Debt Composition by Holders

Banking institutions make up for the highest percentage of domestic debt, accounting for 45.2% of government securities holdings as at 13th October 2023, albeit 2.5% points lower than the 47.7% share recoded over a similar period in 2022, with the reduction mainly attributed heightened credit risk in the market due to the upcoming Eurobond maturity in 2024. On the other hand, government securities holding by other domestic investors registered a 3.3%-points increase to 9.6% as at 13th October 2023, from the 6.3% recorded over a similar period in 2022. Notably, pension funds accounted for the second largest portion with 31.9% of holdings in government securities as at 13th October 2023, albeit 0.7% points lower than the 32.6% registered the previous year. Below is a table of the composition of government domestic debt by holders:

|

Cytonn Report: Composition of Government Domestic Debt by Holder |

|||||||||||

|

Domestic debt |

Dec-13 |

Dec-14 |

Dec-15 |

Dec-16 |

Dec-17 |

Dec-18 |

Dec-19 |

Dec-20 |

Dec-21 |

Dec-22 |

Oct-23 |

|

Banking institutions |

49.2% |

54.3% |

55.4% |

52.2% |

54.6% |

54.5% |

54.3% |

53.3% |

50.2% |

46.8% |

45.2% |

|

Insurance Companies |

10.2% |

9.9% |

8.4% |

7.3% |

6.4% |

6.1% |

6.4% |

6.4% |

6.8% |

7.4% |

7.3% |

|

Parastatals |

3.5% |

2.8% |

4.6% |

5.8% |

6.9% |

7.3% |

6.5% |

5.7% |

5.6% |

6.1% |

6.0% |

|

Pension Funds |

26.1% |

23.9% |

25.4% |

28.2% |

27.5% |

27.6% |

28.6% |

30.3% |

31.3% |

33.3% |

31.9% |

|

Other domestic investors |

11.0% |

9.0% |

6.2% |

6.5% |

4.6% |

4.6% |

4.2% |

4.3% |

6.1% |

6.4% |

9.6% |

|

TOTAL |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

Source: Central Bank of Kenya

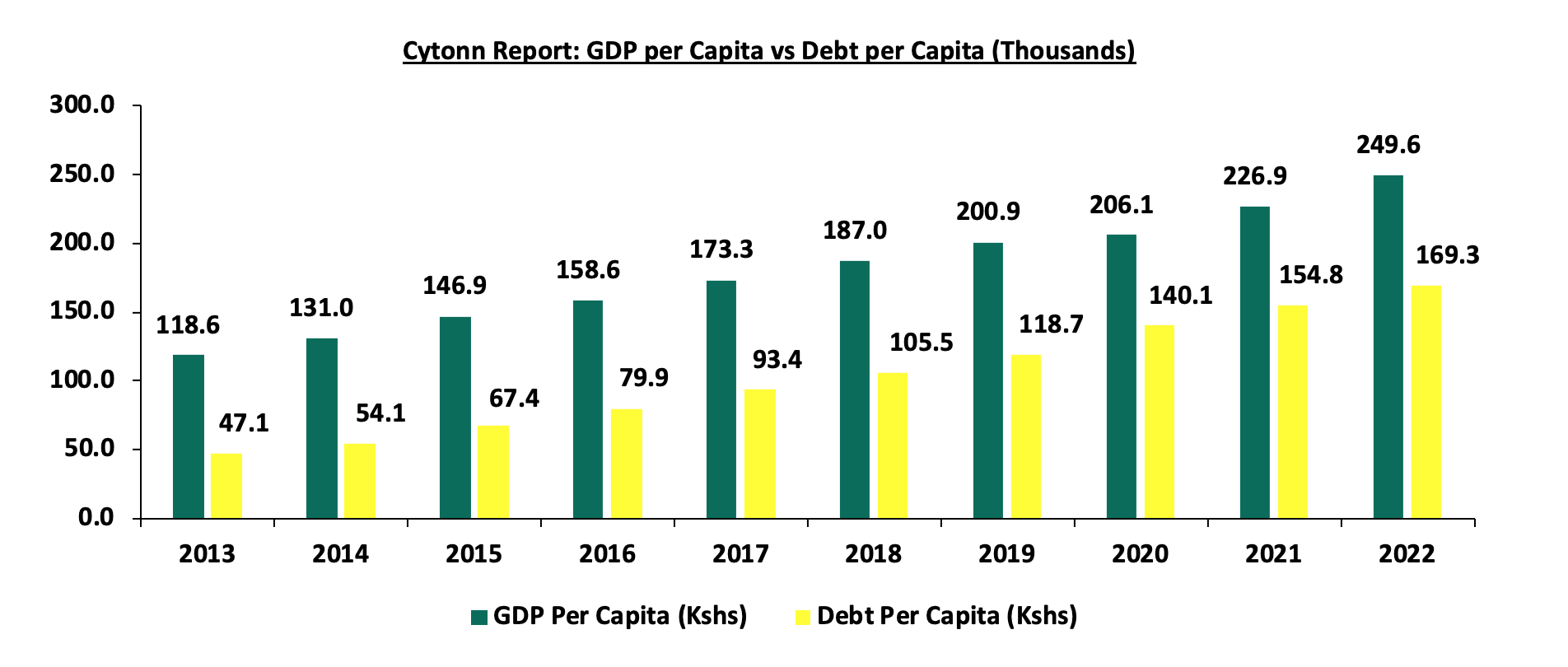

- GDP per Capita vs Debt per Capita

According to Central Bank data, Kenya’s Public Debt per Capita has increased at a 10-year CAGR of 15.2% to Kshs 169,283.9 in 2022, from Kshs 41,011.0 in 2012. On the other hand, GDP per Capita has grown at a slower 10-year CAGR of 8.6% to Kshs 249,558.2 in 2022, from Kshs 109,024.7 in 2012, implying that the increase in debt being incurred is not directly translating into economic growth. The chart below compares Kenya’s GDP per capita to the debt per capita over the last 10 years:

Source: World Bank, CBK

Factors that have accelerated the growth in Kenya’s Public debt;

- Fiscal Deficit – Kenya has witnessed a persistent fiscal deficit averaging at 7.6% of the GDP for the last 9 financial years and is projected to ease to 4.4% of the GDP at the end of FY’2023/24, from the 5.7% recorded in FY 2022/23. According to Budget Policy Statement FY'2023/24 released by the controller of budget, the approved budget for the FY’2023/24 is projected to be Kshs 3.7 tn against a targeted revenue collection of Kshs 2.9 tn, hence the need to borrow an additional Kshs 0.3 tn domestically and Kshs 0.5 tn of externally,

- Debt Servicing Costs – Debt servicing cost has been on the rise, with the debt service to revenue ratio averaging 41.2% over the last 10 financial years and standing at 64.3% as of September 2023. The rising debt servicing cost is attributed to the continuous accumulation of external debt and the depreciation of the currency,

- Short falls of Revenue collections – Despite the significant growth in tax revenues, the Kenya Revenue Authority (KRA) has consistently fallen short on its tax revenue targets, with the tax collections for FY'2022/23 increasing by 6.6% to Kshs 2.2 tn from Kshs 2.0 tn in FY’2021/22, albeit short of the Kshs 2.3 tn target. To plug the budget deficits, the government has had to borrow externally and also from the domestic market thereby increasing the country’s debt profile over time, and,

- Guaranteed loans by the Government of Kenya – The national government incurred Kshs 12.3 bn guaranteed debt payment on behalf of Kenya Airways (KQ) during FY’2022/23. As a consequence, guaranteed loans on state corporations put pressure on the need for excessive spending, the despite poor performances by the said state corporations.

Section 2: Kenya’s Debt Servicing Cost

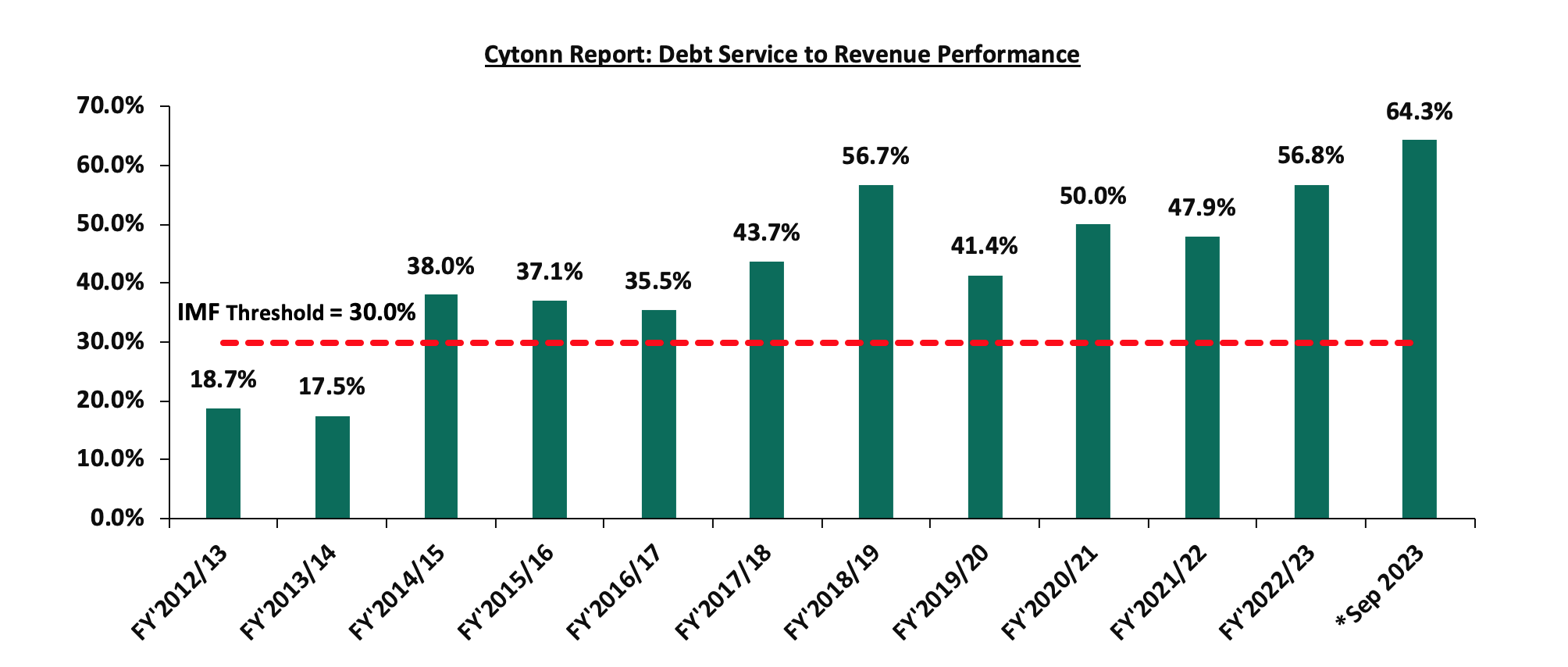

According to the Revenue and Net Expenditures Report for the FY’2022/23 by the National Treasury, the cumulative public debt servicing cost amounted to Kshs 1,161.6 bn which was 83.9% of the revised estimates of Kshs 1,385.1 bn, and 83.4% of the original estimates of Kshs 1,393.1 bn. Notably, the Kshs 1,161.6 bn debt servicing cost was equivalent to 56.8% of the actual revenues collected as at the end of FY’2022/23, which was 26.8% points above IMF’s recommended threshold of 30.0%. Similarly, according to the National Treasury’s Annual Public Debt Management Report 2022, the debt service to revenue ratio was estimated at 47.9% for the FY’2022/23 which was 2.1% points lower than 50.0% debt service to revenue ratio recorded in FY’2020/21. The sustained high debt service to revenue ratio above the recommended threshold is a worrying sign. A ratio approaching 50.0% means that nearly half of the government's revenue is being allocated to servicing debt which may leave limited fiscal space for public investments, social programs, and other critical government functions, which are essential for the long-term well-being of country. Notably, the debt servicing cost has continued to rise with the latest revenue and net expenditures for the three months of FY’2023/2024 ending 30th September 2023, highlighting that debt servicing to total revenue stood at 64.3%. Below is a chart showing the debt service to revenue ratio for the last ten fiscal years:

Source: National Treasury

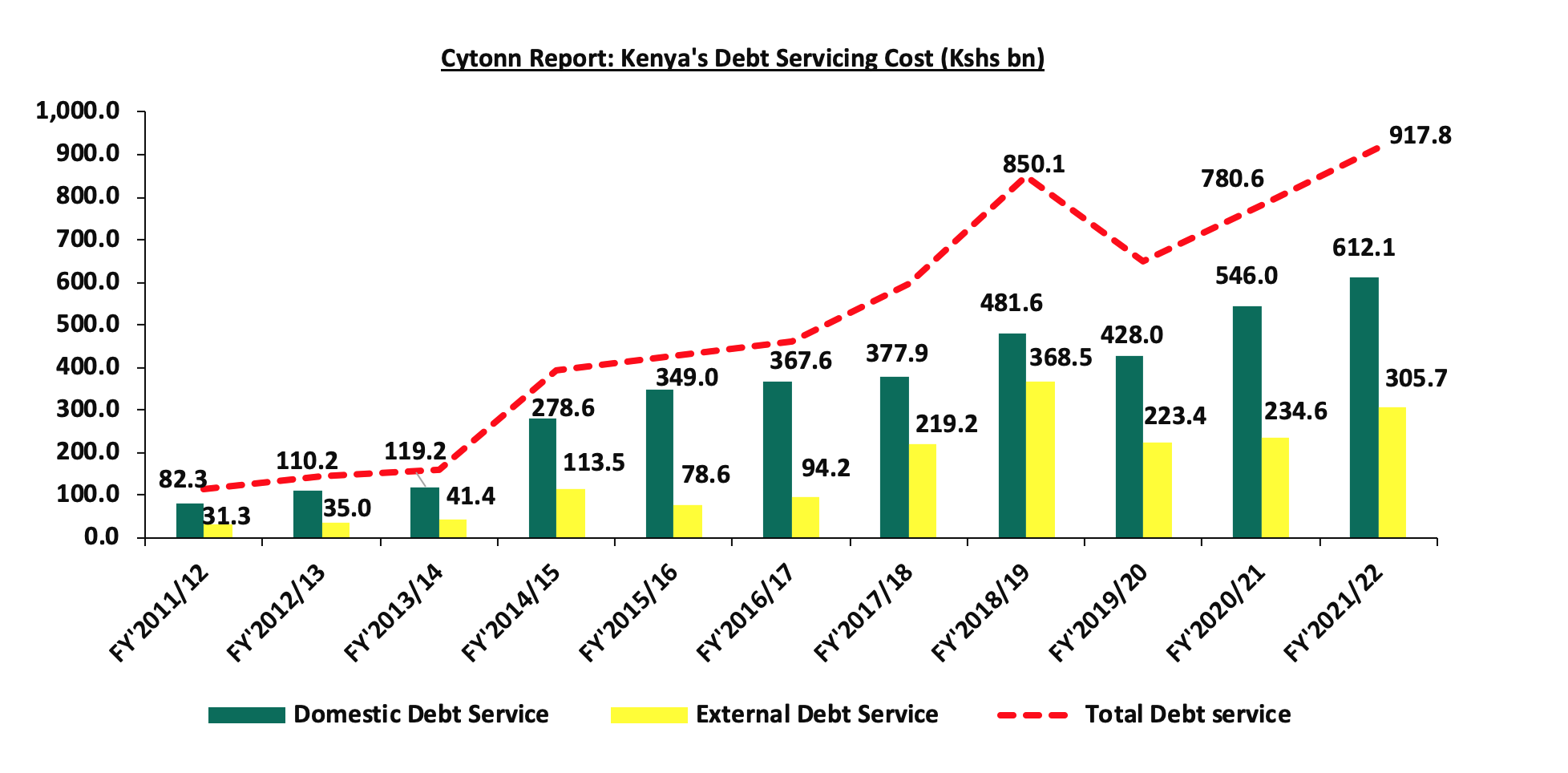

Kenya’s debt servicing costs have continued to increase over time growing at a 10-year CAGR of 23.2% to Kshs 917.8 bn in FY’2021/2022, from Kshs 113.6 bn in FY’2011/2012. The graph below compares the domestic debt servicing cost to the external debt servicing cost over the last ten fiscal years:

Source: National Treasury

The key take-outs from the chart include:

- Total debt service for the FY’2021/22 stood at Kshs 917.8 bn, a 17.6% increase from Kshs 780.6 bn recorded in FY’2020/21. Domestic debt service took the largest share, accounting for 66.7% of the total debt service while external debt service represented 33.3% in FY’2021/22, and,

- Interest payments made up the bulk of Kenya’s debt servicing costs coming in at 63.0% in FY’2021/2022. Notably, the domestic interest payments came in at Kshs 612.1 bn, while the external interest payment was Kshs 305.7 bn.

Section 3: Economic Consequences of High Debt Levels

The COVID-19 pandemic left many countries in sub-Saharan Africa struggling with a weak global economy, rising prices, expensive loans, and a high cost of living. Many of them still face challenges such as high inflation, high interest rates, currency fluctuations, and political unrest. As such, many developing countries including Kenya have had to borrow more in order to cushion their economies against the additional economic shocks resulting from internal geopolitical tensions and supply chain constraints amid arising global conflicts. However, this continuous borrowing has resulted in high levels of accumulated debt, with several implications for the Kenyan economy;

- Increased Debt Servicing Costs – High debt levels have led to increased costs of debt servicing given that a significant portion of the debt is in foreign currencies and the local currency has been weakening. The government has had to increase taxes and cut spending in other areas to meet its debt obligations and the conditions set by Multilateral lenders such as the IMF,

- Higher Borrowing Costs on New Loans – Given the country’s high levels of debt, lenders perceive Kenya’s credit environment to be riskier, therefore demanding higher interest rates for new borrowing. This makes it more expensive for the government to finance its operations and investments,

- Reduced Fiscal Space – High debt levels tend to limit a government’s fiscal space, or its ability to respond to economic shocks with fiscal policy. This is because a large portion of the government’s budget gets tied up in debt servicing, leaving less money for other expenditures and development,

- Crowding Out of the Private Sector – Because of the increased domestic borrowing, the government crowds out the private sector by driving up interest rates in the economy thus making it difficult for both businesses and individuals to borrow, and,

- Risk of Default – High levels of debt can lead to default, where a country is unable to meet its debt obligations. For Kenya’s situation, credit rating agencies such as Fitch and Moody’s have downgraded the country’s credit outlook from stable to negative resulting in increased borrowing costs and loss of investor confidence.

Section 4: Kenya’s Debt sustainability analysis and outlook

As discussed in above sections, the country’s risk of debt distress remains elevated as evidenced by the high debt service to revenue ratio of 64.3%. Additionally, Kenya’s debt to GDP ratio stood at 70.2% in June 2023, 20.2% points above IMF’s recommended threshold of 50.0% for developing countries. Notably, Kenya’s public debt recorded 10-year CAGR of 18.0% to Kshs 10.5 tn in August 2023, outpacing the economic growth’s 10 year average of 4.5%, with the International Monetary Fund (IMF) projecting Kenya’s 2023 GDP growth to come in at 5.0% as of July 2023, a downward revision from its projection of 5.3% made in April 2023 as a result of elevated inflation and high interest rates. The persistent fiscal deficits resulting from the revenue-expenditure mismatch continue to hamper fiscal consolidation efforts as revenue continues to lag behind expenditure.

Kenya’s debt levels have been of concern, with the recent ratings by S&P Global, Fitch and Moody’s credit agencies downgrading the country’s credit outlook from stable to negative. The downgrades of Kenya’s credit score have dimmed the country’s ability to access cheaper loans in the international financial markets, with the yields on the 10-year 2014 Eurobond Issue reaching a high of 20.3% on 3rd October 2023. Below is a summary of the credit rating on Kenya by various rating agencies:

|

Cytonn Report: Kenya Credit Rating Agencies Ratings |

|||||

|

Rating Agency |

Previous Rating |

Current Outlook |

Current Rating |

Current Outlook |

Date Released |

|

Moody’s Ratings |

B3 |

Stable |

B3 |

Negative |

28th July 2023 |

|

Fitch Ratings |

B |

Stable |

B |

Negative |

20th July 2023 |

|

S&P Global |

B |

Stable |

B |

Negative |

24th February 2023 |

Source: Fitch Ratings, S&P Global

With the tough macro-economic environment currently being witnessed in the country, the government’s projection of increased revenues especially through tax collection may fall short of its target, thus leading to continuous need for borrowing. The table below gives the trend of both expenditure and revenue growths in the last five financial years and projections in the medium term;

|

Cytonn Report: Public Debt (Kshs tn) |

|||||||

|

FY'2018/19 |

FY'2019/20 |

FY'2020/21 |

FY'2021/22 |

FY2022/23 |

FY2023/24 |

FY2024/25 |

|

|

Cumulative Domestic Debt |

2.8 |

3.2 |

3.7 |

4.3 |

4.7 |

5.1 |

5.5 |

|

Cumulative External Debt |

3.0 |

3.5 |

4.0 |

4.3 |

5.5 |

5.9 |

6.1 |

|

Total |

5.8 |

6.7 |

7.7 |

8.6 |

10.3 |

10.9 |

11.6 |

|

Expenditure |

2.4 |

2.6 |

2.8 |

3.0 |

3.1 |

3.7 |

4.0 |

|

Revenue Collected |

1.5 |

1.6 |

1.6 |

1.9 |

2.4 |

2.6 |

2.9 |

|

Budget Deficit |

0.9 |

1.0 |

1.2 |

1.1 |

0.7 |

1.2 |

1.1 |

|

Domestic Borrowings |

0.3 |

0.5 |

0.6 |

0.6 |

0.6 |

0.3 |

0.4 |

|

External Borrowings |

0.4 |

0.3 |

0.3 |

0.1 |

0.1 |

0.3 |

0.3 |

|

Total |

0.7 |

0.8 |

1.0 |

0.7 |

0.7 |

0.6 |

0.7 |

|

Domestic debt service |

0.5 |

0.4 |

0.5 |

0.6 |

1.0 |

0.8 |

0.9 |

|

External debt Service |

0.4 |

0.2 |

0.2 |

0.3 |

0.4 |

0.6 |

0.4 |

|

Total Debt Service |

0.9 |

0.7 |

0.8 |

0.9 |

1.4 |

1.5 |

1.4 |

|

Debt service to Revenue |

56.7% |

41.4% |

50.0% |

47.9% |

56.8% |

57.2% |

47.5% |

Source: National Treasury (Annual Public Debt Management Report and Budget Policy Statement)

Key take outs;

- Debt servicing costs is expected to remain high in the FY’2023/24 due to the need for more borrowings. The high borrowings are expected to be channelled to debt repayment, financing the increasing fiscal deficit as KRA lags behind target and the depreciating shilling continues to increase debt repayment costs,Our View: Debt service projected to grow in FY’2022/23 with debt servicing cost remaining high due to upcoming Eurobond maturity worth USD 2.0 bn and continued local debt maturities,

- Revenue is expected to grow at a 5-year CAGR of 12.8% to Kshs 2.9 tn by the end of FY’2024/25, from Kshs 1.6 tn in FY’2019/20, attributable to the governments focus to increased tax revenues. Due to the unfavourable business climate, combined with high inflation and limited liquidity in the country, it is anticipated that revenue collections will not meet the target. Consequently, the success of revenue collection is heavily reliant on the country’s economic performance and how quickly the business environment improves,

- Compared to revenue, expenditure is expected to grow at a relatively slower 5-year CAGR of 9.2% to Kshs 4.0 tn by the end of FY’2024/25, from 2.6 tn recorded in FY’2019/20, on the back of increased recurrent expenditure, sustained currency depreciation and persistent current account deficit, and,

- The budget deficit is expected to widen in the projected years due to a mismatch in revenue against expenditure growths despite revenue projected to increase at a faster rate compared to expenditure. The persistent budget deficit in the projected financial years, is an indication of the need for further borrowing, impeding the government’s in managing the current debt level.

It is clear that the government faces challenges on how they shall finance their operations in the next couple of months as the debt servicing is high and the economic activity is much slower. The KRA collections for the FY’2022/23 amounted to Kshs 2.2 tn, falling short of the tax revenue target of Kshs 2.3 tn, mainly attributed the tough macroeconomic situation in the country. The situation is exacerbated by the tightened liquidity that currently stands at 12.6% in the local market as of 19th October 2023 amidst the deteriorated business environment. Further, the weakening of the Kenyan shilling has increased the cost of servicing and repaying loans denominated in foreign currencies. As a result, the government’s capability to repay its upcoming maturities and meet its debt obligations is still a major concern.

Section 5: Conclusions and Recommendations

Kenya's public debt situation underscores the need for prudent fiscal management and strategic planning to ensure that the debt remains sustainable and does not compromise the country's economic prospects. It is essential to strike a balance between funding the government's development projects and maintaining debt at manageable levels. To address the challenges posed by the high public debt in Kenya, here are some actionable steps that the Kenyan government can consider:

- Enhanced Debt Management – Implement a comprehensive debt management strategy that encompasses short, medium, and long-term objectives which regularly assess the cost and risk profile of the debt portfolio as well as Prioritizing refinancing high-cost debt with lower-cost alternatives to reduce debt service obligations,

- Capital Markets Reform – The government should strengthen the regulatory and supervisory framework for capital markets and improve the efficiency, stability, and inclusiveness of the financial sector, especially the markets for stocks, bonds, and other securities to improve capital formation and foreign direct investments (FDIs) flowing into the country,

- Improve Ease of Doing Business – The government should improve the competitiveness and attractiveness of the country for investors and entrepreneurs. This can be achieved by simplifying and streamlining the procedures and requirements for starting, operating, and closing a business. This also includes promoting a conducive and competitive business environment that fosters innovation, productivity, and growth. These measures will spur business growth and improve the country’s production thus allowing the government to collect more revenue inform of taxes,

- Economic Diversification – The government should put more efforts on diversifying the economy by encouraging the growth of non-traditional sectors such as technology, agribusiness, manufacturing, and renewable energy as well as Implement structural reforms to improve the ease of doing business and attract foreign direct investment (FDI) which would in turn increase the country’s revenue collection,

- Fiscal Consolidation – High fiscal deficit is attributable to higher growth in expenditure volumes relative to revenue collections, creating the need for excessive borrowing levels. The government needs to implement robust fiscal consolidation through expenditure reduction by introducing austerity measures and limit capital expenditure to projects with either high social impact or have a high Economic Rate of Return (ERR), and high economic benefits outweighing costs,

- Investment in Productive Sectors – Direct investments toward sectors that have the potential for high economic growth and job creation, such as infrastructure, agriculture, and manufacturing as well as developing targeted incentive programs to attract both domestic and foreign investments in these sectors,

- Public-Private Partnerships (PPPs) – The government should identify infrastructure projects suitable for PPP arrangements and incentivize the private sector to participate in such projects, thus sharing the financial burden and transferring project risk to the private sector,

- Improving the Country’s Exports – The government should formulate export and manufacturing favourable policies to improve the current account. This would stabilize the exchange rate and stop our foreign denominated debt from increasing as the shilling depreciates,

- Efficient Tax Collection – The government should strengthen tax collection and administration to improve revenue collection without increasing tax rates significantly. This can be done through broadening the tax base while ensuring tax policies are equitable and do not disproportionately burden the lower-income segments of the population,

- Transparency and Accountability: Maintain transparency in the utilization of borrowed funds and ensure that loans are allocated to projects with measurable returns. Better governance will help to reduce wastage and corruption levels that had impeded proper allocation of funds towards designated projects, resulting in misappropriation of funds, and,

- Monitoring and Reporting: Establish mechanisms for continuous monitoring of debt levels and fiscal health, with regular reporting to stakeholders and the public.

Addressing the public debt issue is a collective effort that requires cooperation among policymakers, stakeholders, and the general public, all working together to secure the country’s financial future and prosperity.

Disclaimer: The views expressed in this publication are those of the writers where particulars are not warranted. This publication, which is in compliance with Section 2 of the Capital Markets Authority Act Cap 485A, is meant for general information only and is not a warranty, representation, advice or solicitation of any nature. Readers are advised in all circumstances to seek the advice of a registered investment advisor.

- Talk to us

- Kenya

- P.O Box 20695 - 00200, Nairobi, Kenya

- Cell +254709101200

- Tel +254709101200

- WhatsApp +254741676635

- United States

- +254709101200

- DOWNLOAD OUR APP

-

- Kenya

- 8th Floor, Pinetree Plaza, Kaburu Drive, Ngong Road, Nairobi, Kenya

- USA

- Suite 1150, 1775 Eye Street NW, USA, Washington DC 20006, USA

- Investments

- High Yield

- Private Equity

- Real Estate

- Real Estate

- RiverRun Estates

- Cytonn Towers

- The Ridge

- Taraji Heights

- The Alma