Cytonn Annual Markets Review - 2024

By Research Team, Jan 5, 2025

Executive Summary

Global Markets Review

According to the World Bank's June 2024 Global Economic Prospects report, the global economy is projected to grow at 2.6% in 2024, matching the growth rate recorded in 2023. This forecast marks a slight downward revision from earlier projections, reflecting continued economic headwinds, particularly in the emerging markets. The World Bank’s growth projection is 0.6 percentage points lower than the IMF’s 2024 forecast of 3.2%. The lower growth is attributable to global inflationary pressures and continued tightening by central banks for much of 2024. However, recent developments indicate that some central banks, such as those in the United States and England, have cut interest rates in response to easing inflation, which could stimulate economic activity going forward. Notably, advanced economies are expected to record a 1.5% growth in 2024, remaining unchanged from the 1.5% expansion recorded in 2023. However, emerging markets and developing economies are projected to expand by 4.0% in 2024, lower than 4.2% growth in 2023;

Sub-Saharan Africa Regional Review

According to the World Bank, the Sub-Saharan economy is projected to grow at a moderate rate of 3.0% in 2024, which is 0.6% higher than the 2.4% growth recorded in 2023. The expected recovery is primarily driven by private consumption growth as declining inflation boosts the purchasing power of household incomes. Nevertheless, the risk of debt distress remains high with more than half of countries facing unsustainable debt burdens as the region’s public debt to GDP ratio is expected to remain high at 57.0% in 2024, albeit a decline from 60.0% in 2023. The public debt is expected to remain high due to increased debt servicing costs as a result of continued currency depreciation for most countries in the region and high interest rates. Additionally, many countries are providing subsidies in order to mitigate inflationary pressures, which could worsen public finance, increase public debt, and weigh down on debt sustainability;

In 2024, most of the select Sub-Saharan currencies depreciated against the US Dollar, mainly attributable to the elevated inflationary pressures in the region, high debt servicing costs that continue to dwindle foreign exchange reserves, and monetary policy tightening by advanced economies. The high interest rates in developed countries have led to massive capital outflows from the region as investors, both institutional and individual seek to take advantage of the higher returns offered in developed economies. Further, the elevated inflationary pressures in most economies in the region puts pressure on the value of local currencies due to expensive importation;

Kenya Macro Economic Review

According to the Kenya National Bureau of Statistics (KNBS) Q2’2024 Quarterly Gross Domestic Product Report, the Kenyan economy recorded a 4.6% growth in Q2’2024, slower than the 5.6% growth recorded in Q2’2023. For the sectoral performance, Agriculture, Fishing and Forestry sector grew by 4.8% in Q2’2024, lower than the 7.8% expansion recorded in Q2’2023. All sectors in Q2’2024, except Mining and Quarrying and Construction recorded positive growths, with varying magnitudes across activities. Most sectors recorded declining growth rates compared to Q2’2023 with Accommodation and Food Services, Financial & Insurance, and Construction Sectors recording the highest declines of 16.2%, 8.1%, and 5.6% points, respectively. The slowed growth in the economy could be attributed to the high fuel prices which made production more expensive and negatively impacted the business environment and the unrest caused by the anti-finance bill protests in June;

In 2024, the Kenyan economy is projected to grow at an average of 5.3%, down from 5.6% in 2023. The slower growth is primarily driven by reduced private sector activity and ongoing fiscal consolidation efforts by the government, which have limited public spending. Additionally, political instability during the year, fueled by anti-finance bill protests and opposition against the current regime, has undermined investor confidence and disrupted economic activities. This instability is expected to further weigh on economic growth;

Fixed Income

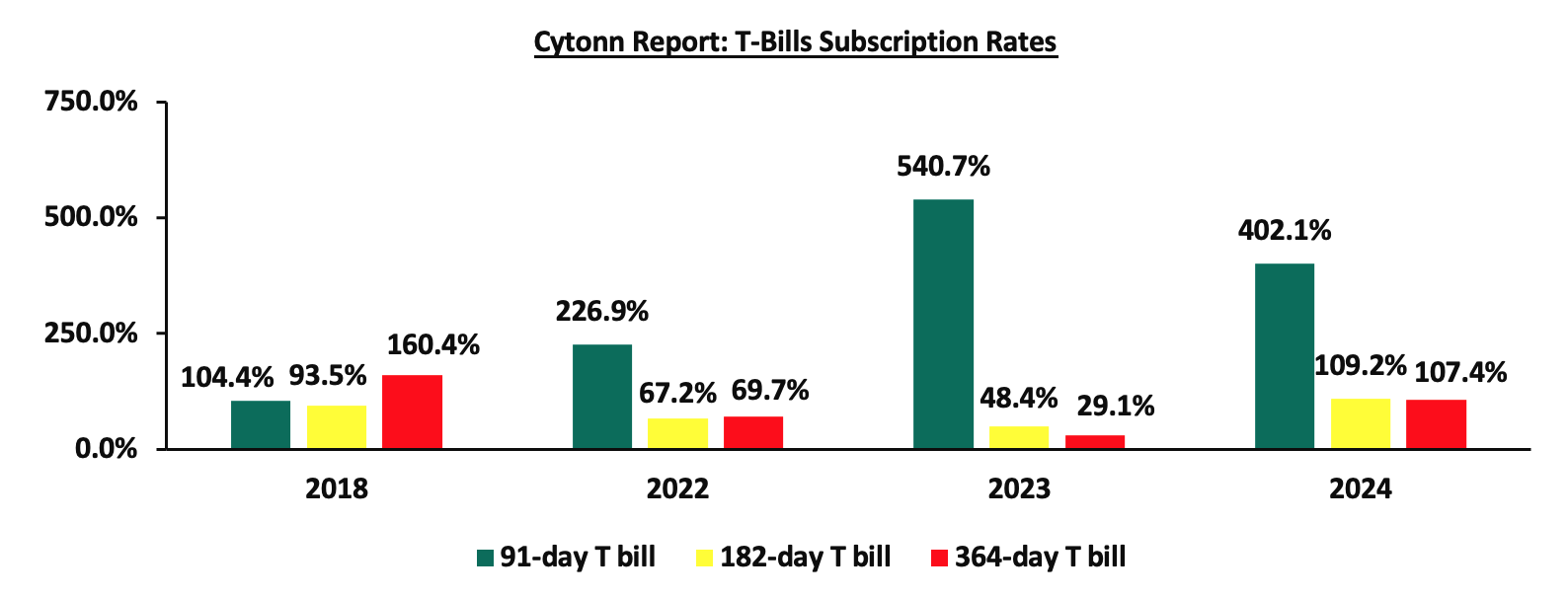

During the year, T-bills were oversubscribed, with the overall subscription rate coming in at 153.3%, up from 120.0% in FY’2023. Investors’ preference for the 91-day paper persisted as they sought to avoid duration risk, with the paper receiving bids worth Kshs 847.4 bn against the offered Kshs 212.0 bn, translating to an oversubscription rate of 399.7%, albeit lower than the oversubscription rate of 529.1% recorded in FY’2023. Overall subscription rates for the 364-day and 182-day papers came in at 103.0% and 104.9%, higher than the 29.0% and 48.5%, respectively, recorded in FY’2023. The average yields on the 364-day, 182-day, and 91-day papers were on an upward trajectory with the 182-day yields increasing the most by 330.6 bps to 15.7%, from 12.4% in 2023, while the 364-day and 91-day increased by 327.1 bps and 300.6 bps to 16.0% and 15.2% in 2024, from 12.8% and 12.2% in 2023, respectively. However, on y/y basis, the yields on the government papers registered significant decline in 2024 with the 91-day paper decreasing the most by 6.0% to close the year at 9.9% from the 15.9% recorded at the close of FY’2023, while the yields on the 182-day and 364-day decreased by 5.9% and 4.5% to close the year at 10.0% and 11.4%, from the 16.0% and 15.9%, respectively, recorded at the end of FY’2023. The year-on-year decline in yields is primarily driven by investors perceiving lower risks due to eased inflation, currency appreciation, and improved liquidity positions. As a result, there is less demand for higher returns to compensate for potential losses. The average acceptance rate during the period came in at 77.3%, albeit lower than the 92.5% recorded in FY’2023, with the government accepting a total of Kshs 1,507.3 bn out of the Kshs 1,949.4 bn worth of bids received. Notably, the decline in the government papers yields accelerated in December 2024 compared to November 2024, with the yields on the 91-day paper decreasing by 274.3 bps, compared to 190.8 bps decline that was recorded in November 2024, as the government manages the borrowing costs amid budgetary pressures;

Primary T-bond auctions in 2024 were generally oversubscribed, with bonds receiving bids worth Kshs 1,137.9 bn against the offered Kshs 665.0 bn, translating to an oversubscription rate of 171.1%, higher than the oversubscription rate of 128.5% recorded in 2023. The government accepted Kshs 867.8 bn of the Kshs 1,137.9 bn worth of bids received, translating to an acceptance rate of 76.3%. Additionally, in the primary bond market, the government is looking to raise Kshs 30.0 bn through the reopened fifteen year and twenty-five-year fixed coupon bonds; FXD1/2018/15 and FXD1/2022/25 with tenors to maturity of 8.3 years and 22.8 years respectively. The bonds will be offered at fixed coupon rates of 12.7% and 14.2% respectively. Our bidding range for the reopened bonds are 13.45%-13.85% and 15.65%-16.00% for the FXD1/2018/15 and FXD1/2022/25 respectively;

During the week, T-bills were undersubscribed for the fourth consecutive week, with the overall undersubscription rate coming in at 65.4%, higher than the undersubscription rate of 20.3% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 8.0 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 199.7%, significantly higher than the undersubscription rate of 56.1% recorded the previous week. The subscription rates for the 182-day paper increased to 60.8% from the 4.4% recorded the previous week, while the subscription rate for the 364-day paper decreased to 16.3% from 21.9% recorded the previous week. The government accepted a total of Kshs 15.7 bn worth of bids out of Kshs 15.7 bn bids received, translating to an acceptance rate of 100.0%. The yields on the government papers recorded a mixed performance, with the yields on the 182-day paper increasing marginally by 0.4 bps to 10.03% from 10.02% recorded the previous week, while the yields on the 364-day and 91-day papers declined by 3.8 bps and 6.9 bps respectively to 11.37% and 9.83% from the 11.41% and 9.89% respectively recorded the previous week.

During the week, KNBS released the y/y inflation for December 2024 highlighting that inflation increased slightly by 0.2% points to 3.0%, from the 2.8% recorded in November 2024. This was however in contrary with our projection to a range of 2.4% to 2.7%, where our projection was mainly driven by expectations of reduced fuel prices in December, coupled with the stability of the Kenyan Shilling. The headline inflation in December 2024 was majorly driven by increase in prices of commodities in the following categories; Food & Non-Alcoholic Beverages, and Transport sector by 4.8% and 0.2% respectively. However, the commodity prices in Housing, Water, Electricity, Gas & other fuels declined by 0.2%;

Equities

During the year, the Kenyan equities market was on an upward trajectory, with NSE 10 gaining the most by 42.9%, while NSE 25, NASI and NSE 20 gained by 42.5%,34.3% and 33.3%, respectively. The equities market performance was driven by gains recorded by large-cap stocks such as KCB Group, SCBK, Absa Bank, Diamond Trust Bank Kenya, Bamburi, and EABL of 89.5%, 74.6%, 56.3%, 54.2%, 52.8%, and 51.0% respectively. The performance was, however, weighed down by losses by large-cap stocks such BAT of 11.5%.

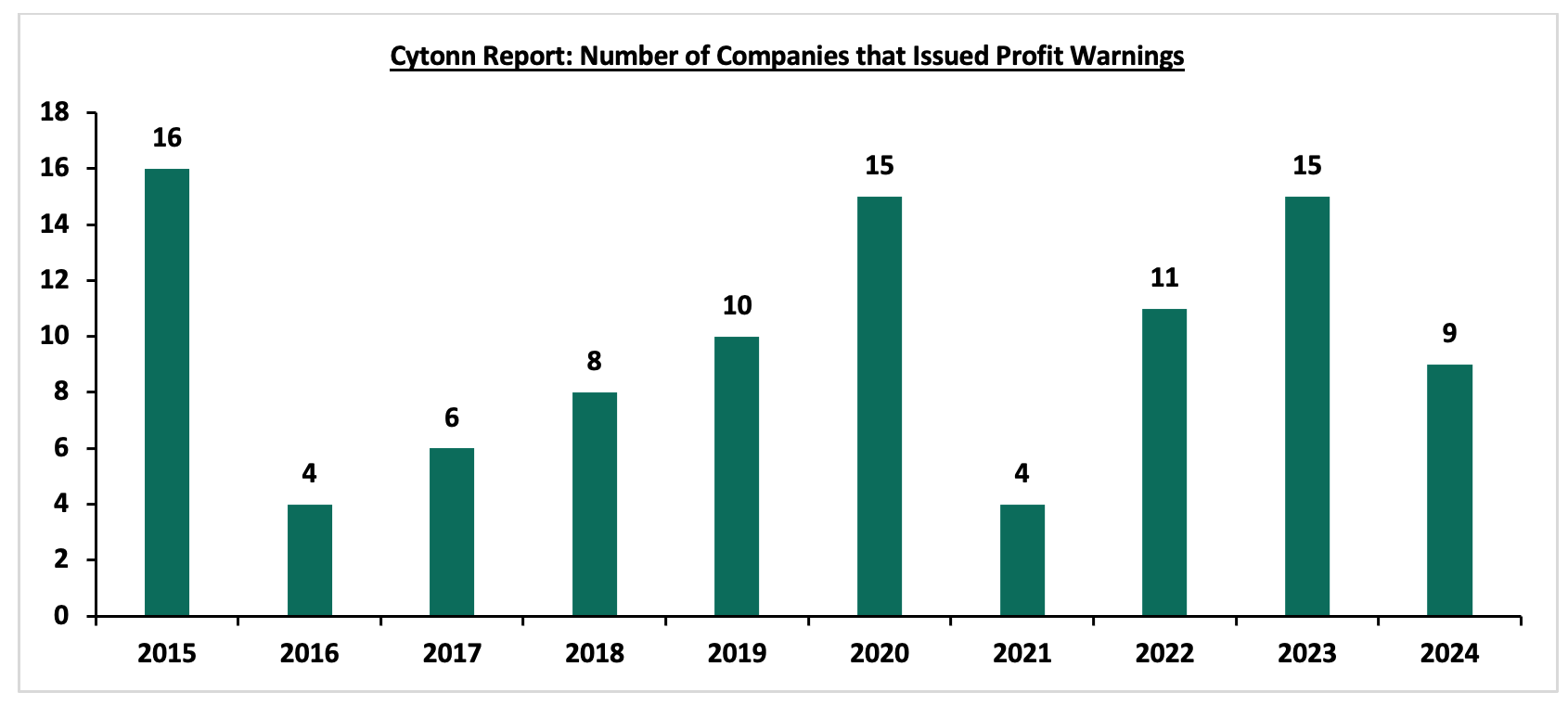

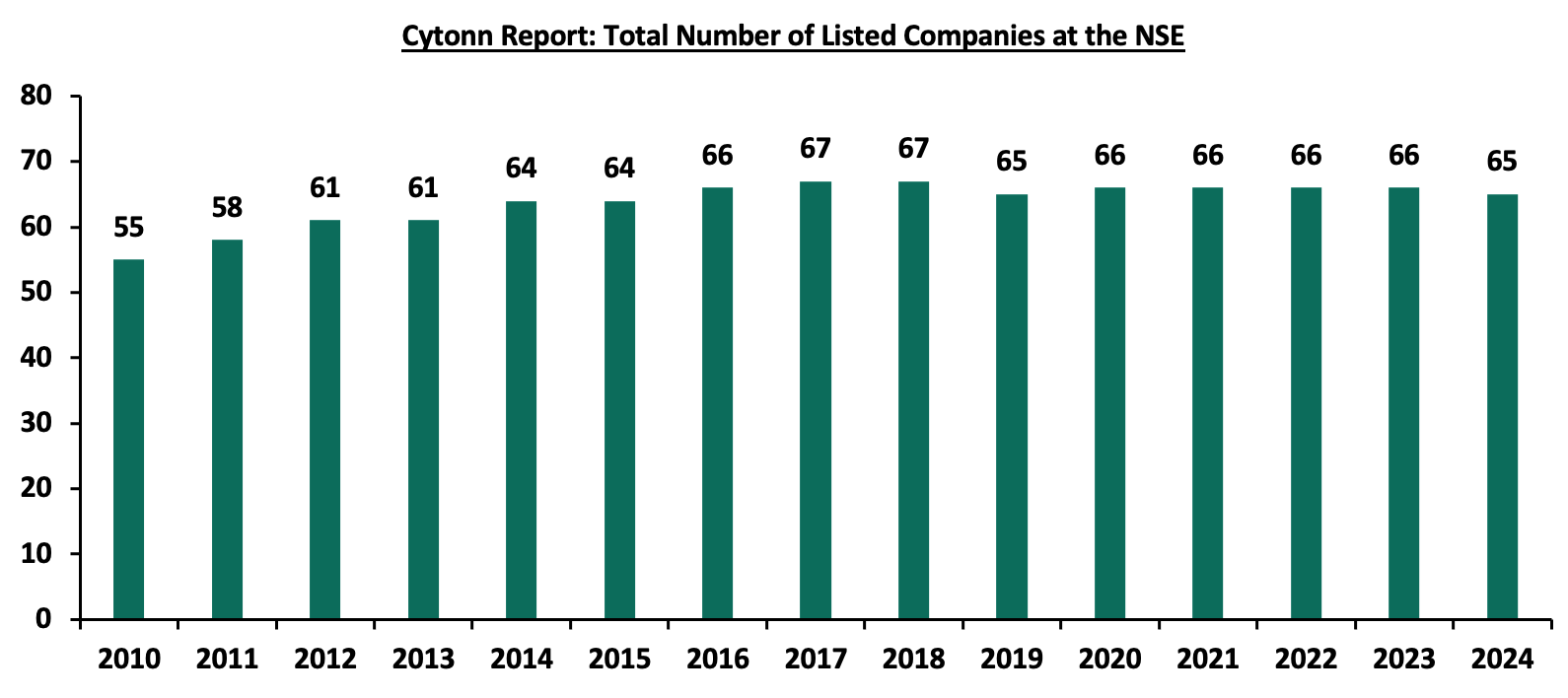

In the banking sector, the Kenya listed banks recorded a weighted average increase in the core earnings per share of 24.6% in Q3’2023, compared to a weighted average increase of 11.2% in Q3’2023, while in the Insurance sector, the listed insurers recorded a weighted average increase in core earnings per share of 39.6% in H1’2024, significantly higher compared to the weighted decline of 235.5%, in H1’2023. During the year, 9 companies issued profit warnings, as compared to 15 companies in 2023, and 11 companies in 2022 an indication that the operating environment became slightly better in 2024 compared to the previous years. Some of the companies that issued profit warnings include Express Kenya and Kakuzi Plc. Additionally, during the year, the Nairobi Securities Exchange admitted the Linzi Sukuk on the NSE Unquoted Securities Platform (USP) making the product the first Shari’ah compliant product to be admitted on the platform. The NSE also delisted Acorn Green Bond and ILAM FAHARI-I REIT from the Nairobi Securities Exchange. Four companies remained suspended at the Nairobi Securities Exchange, namely, Deacons (East Africa) PLC, ARM Cement PLC, Mumias Sugar Co. Ltd. and Kenya Airways.

Additionally, during the year, HF Group released the results of its earlier approved rights issue, announcing that the rights were oversubscribed, with the oversubscription rate coming in at 138.3% having received offers worth Ksh 6.4 bn against the offered Ksh 4.6 bn. Notably, the Group accepted 474.2 million shares under the entitlement option against the offered 769.2 million, translating to an acceptance rate of 61.7%.

Additionally, during the year, Amsons Industries (K) Limited and Savannah Clinker made offers to acquire Bamburi Cement PLC. Later, the Capital Markets Authority (CMA) notified the shareholders of Bamburi Cement PLC and the public that Savannah clinker limited had withdrawn its competing offer on 4th December 2024 and that it had declined to extend the offer period by 60 days to enable the competing offer to respond to any inquiries. The sale of Bamburi Cement Plc shares to Amsons Industries (K) Limited, was approved by CMA without modifications;

Real Estate

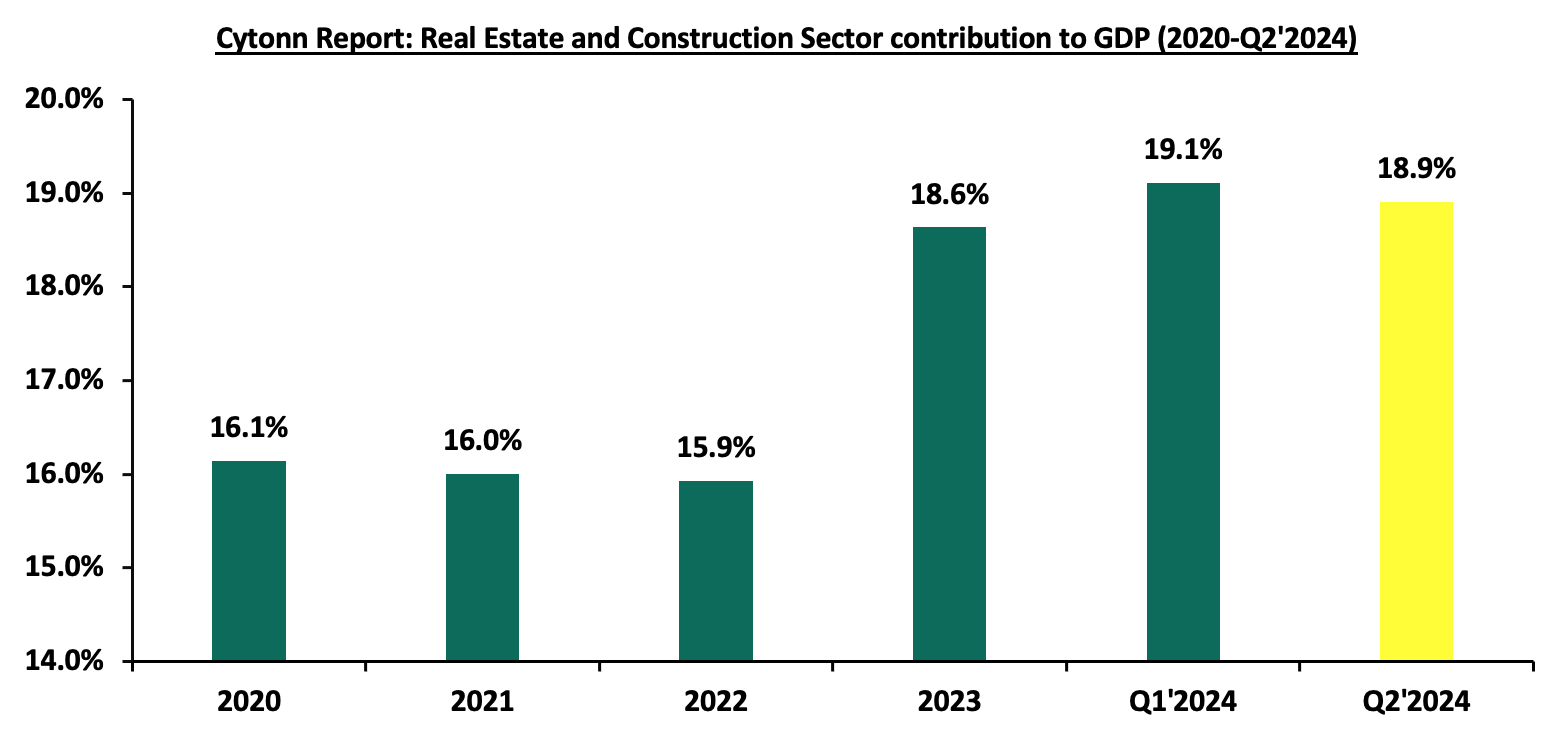

In 2024, the general Real Estate sector continued to witness considerable growth in activity in terms of property transactions and development activities. Consequently, the sector’s activity contribution to Gross Domestic Product (GDP) grew by 6.0 % to Kshs 281.6 bn in Q2’2024, from Kshs 265.8 bn recorded during the same period in 2023. In addition, the sector contributed 10.3% to the country’s GDP, 0.2% points decrease from 10.5% recorded in Q2’2023. Cumulatively, the Real Estate and construction sectors contributed 18.9% to GDP, a 2.3% points improvement from 16.6% in Q2’2023. The Nairobi Metropolitan Area (NMA) residential sector recorded a slight downtrend in performance, with the average total returns to investors coming in at 5.8%, a 0.3%-point decline from 6.1% recorded in FY’2023. The performance was attributed to a decrease in the residential average y/y price appreciation which came in at 0.3% in FY’2024, 0.3%-points lower than the 0.6% appreciation recorded in FY’2023, driven by a tough economic environment during the year. On the other hand, the average rental yield came in at 5.4% in FY’2024, recording a 0.1%-points decline from the 5.5% rental yield recorded in FY’2023;

In statutory reviews, during the week, Nairobi's City Hall announced revised land rates effective January 1, 2025, aiming to align charges with current property values and enhance revenue collection transparency. Under the new structure, annual rates will be determined by land size and value. Plots under 0.1 ha will incur a fee of Kshs 2,560, those between 0.1 and 0.2 ha Kshs 3,200, plots ranging from 0.2 to 0.4 ha Kshs 4,000, and those exceeding 0.4 ha Kshs 4,800. Additionally, residential, commercial, and agricultural properties will be taxed at 0.1% of their land value annually;

In the Real Estate Investments Trusts, Centum Investment Company is set to introduce Kenya's first dollar-denominated Income Real Estate Investment Trust (I-REIT) at its Two Rivers development in Nairobi. This strategic move aims to attract international investors seeking exposure to Kenya's real estate market while mitigating currency risk. The proposed I-REIT will focus on income-generating properties within the Two Rivers precinct, including office spaces, retail outlets, and residential units. By denominating the fund in U.S. dollars, Centum seeks to provide a hedge against the volatility of the Kenyan shilling, offering more stable returns for foreign investors;

On the Unquoted Securities Platform, Acorn D-REIT and I-REIT traded at Kshs 25.4 and Kshs 22.2 per unit, respectively, as per the last updated data on 31st October 2024. The performance represented a 27.0% and 11.0% gain for the D-REIT and I-REIT, respectively, from the Kshs s 20.0 inception price. Additionally, ILAM Fahari I-REIT traded at Kshs 11.0 per share as of 31st October 2024, representing a 45.0% loss from the Kshs 20.0 inception price. The volume traded to date came in at 138,600 shares for the I-REIT, with a turnover of Kshs 1.5 mn since inception in November 2015;

Investment Updates:

- Weekly Rates: Cytonn Money Market Fund closed the week at a yield of 16.84% p.a. To invest, dial *809# or download the Cytonn App from Google Play store here or from the Appstore here;

- We continue to offer Wealth Management Training every Monday, from 10:00 am to 12:00 pm. The training aims to grow financial literacy among the general public. To register for any of our Wealth Management Trainings, click here;

- If interested in our Private Wealth Management Training for your employees or investment group, please get in touch with us through wmt@cytonn.com;

- Cytonn Insurance Agency acts as an intermediary for those looking to secure their assets and loved ones’ future through insurance namely; Motor, Medical, Life, Property, WIBA, Credit and Fire and Burglary insurance covers. For assistance, get in touch with us through insuranceagency@cytonn.com;

- Cytonn Asset Managers Limited (CAML) continues to offer pension products to meet the needs of both individual clients who want to save for their retirement during their working years and Institutional clients that want to contribute on behalf of their employees to help them build their retirement pot. To more about our pension schemes, kindly get in touch with us through pensions@cytonn.com;

Hospitality Updates:

- We currently have promotions for Staycations. Visit cysuites.com/offers for details or email us at sales@cysuites.com;

Global Economic Growth:

According to the World Bank's June 2024 Global Economic Prospects report, the global economy is projected to grow at 2.6% in 2024, matching the growth rate recorded in 2023. This forecast marks a slight downward revision from earlier projections, reflecting continued economic headwinds, particularly in the emerging markets. The World Bank’s growth projection is 0.6 percentage points lower than the IMF’s 2024 forecast of 3.2%. The lower growth is attributable to global inflationary pressures and continued tightening by central banks for much of 2024. However, recent developments indicate that some central banks, such as those in the United States and England, have cut interest rates in response to easing inflation, which could stimulate economic activity going forward. Notably, advanced economies are expected to record a 1.5% growth in 2024, remaining unchanged from the 1.5% expansion recorded in 2023. However, emerging markets and developing economies are projected to expand by 4.0% in 2024, lower than 4.2% growth in 2023. The expected slowed down in global economic growth in 2024 as compared to 2023 is majorly attributable to;

- The elevated global inflationary pressures which have necessitated the hiking of interest rates by some central banks around the world with the aim of anchoring inflation. The global inflation is forecasted to ease slightly to 6.9% in 2024, from 8.7% in 2023,

- Tight global financial conditions occasioned by high cost of borrowing which have increased risks of debt distress in emerging economies. Although some central banks, including the U.S. Federal Reserve and Bank of England, have begun easing monetary policies, global financial conditions remain tight due to the lagging impact of past rate hikes, which continue to raise borrowing costs and heighten debt distress risks, especially in emerging economies, and,

- Persistent supply chain constraints worsened by the ongoing Russia-Ukraine conflict which has impacted global fuel and food prices. Consequently, the high energy prices have increased inflationary pressures as well as contributed to currency depreciation as dollar demand increases especially in Emerging Markets and Developing Economies.

The global economy is expected to remain subdued in the short term mainly as a result of persistent inflationary pressures as well as tightening of monetary policies which are expected to weigh down on economic activity. Furthermore, the global economy’s future performance is majorly dependent on how soon the inflationary pressures will ease, which will see central banks ease their monetary policies hence boosting economic activity.

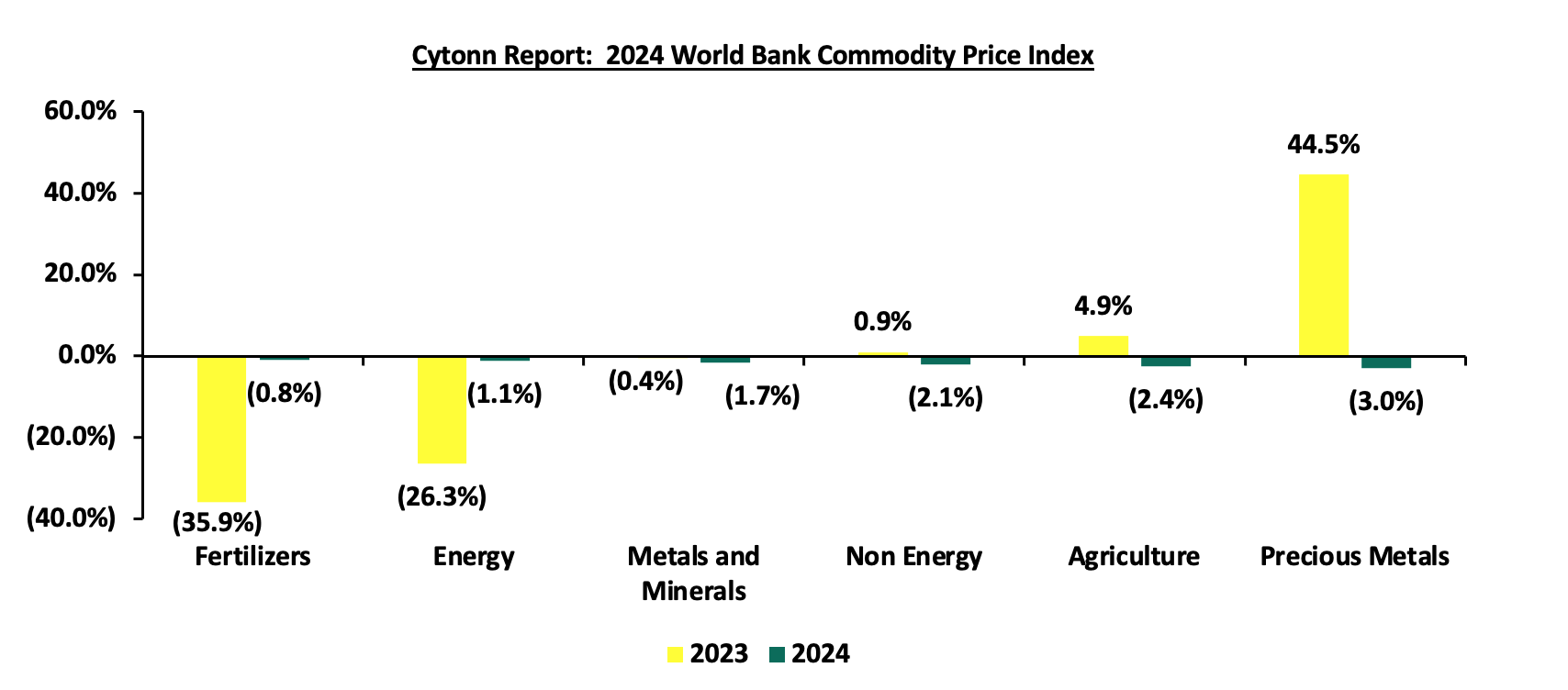

Global Commodities Market Performance:

Global commodity prices were on a downward trajectory in 2024, with prices of precious metals decreasing the most by 3.0% compared to the 44.5% increase recorded in 2023, mainly as a result of reduced demand from key markets, particularly China, and increased global production. Similarly, prices of agricultural commodities decreased by 2.4% in 2024, compared to a 4.9% increase in the same period last year, while prices of Non-Energy commodities, Metals & Minerals, Energy, and Fertilizers declined by 2.1%, 1.7%, 1.1%, and 0.8% respectively, on the back of ample supply due to strong harvests and increased production, coupled with subdued global demand. The chart below shows a summary of the performance of various commodities.

Global Equities Market Performance:

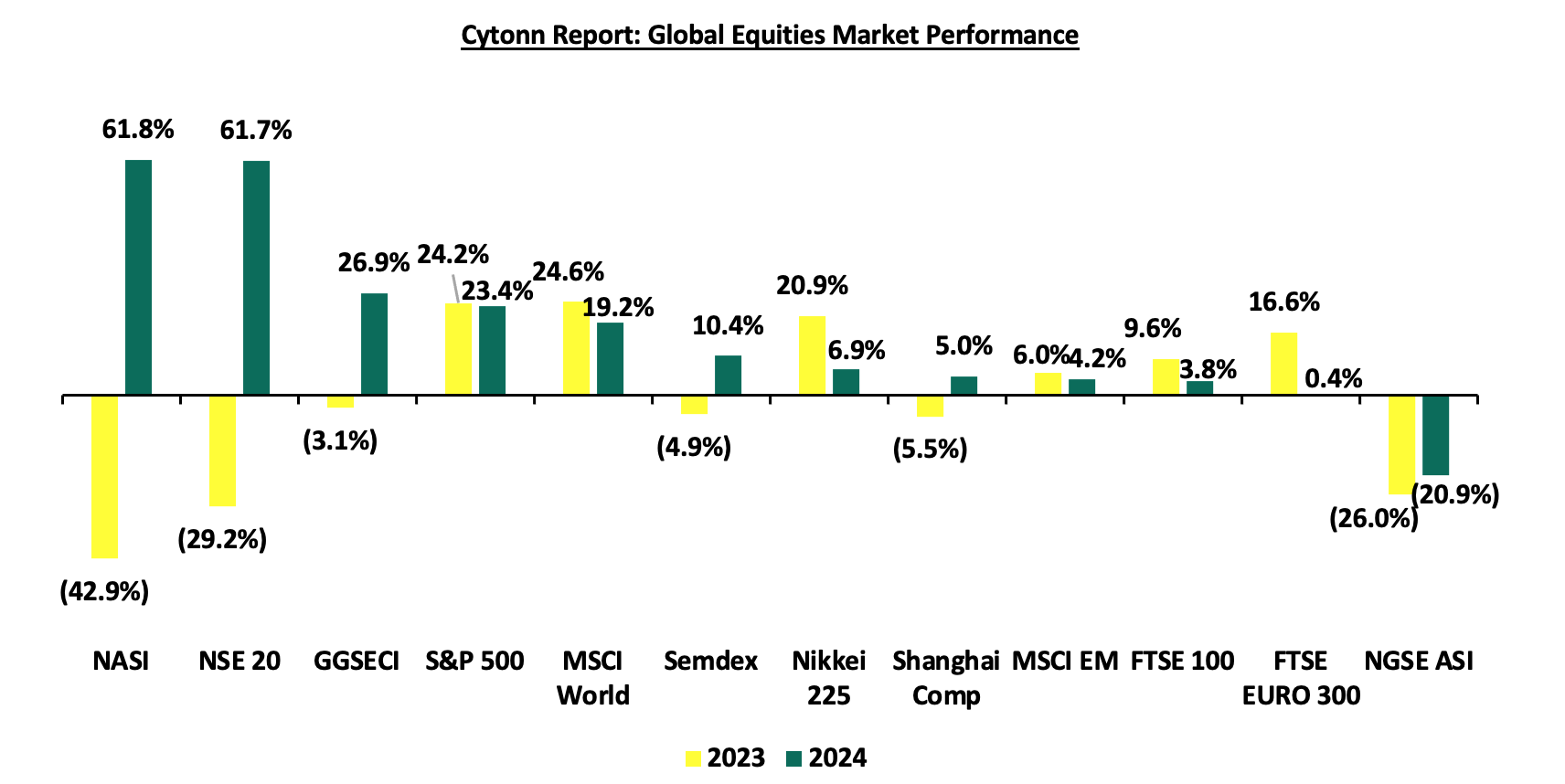

The global stock market recorded mixed performance in 2024, with most indices in the developed countries recording gains during the period, largely attributable to increased investor sentiments as a result of continued economic recovery following the full reopening of the economies coupled with investor preference for the stock markets in the developed countries. Notably, NASI was the best performer during the period, recording a gain at 61.8% in 2024 largely driven by gains in the large-cap stocks in the financial sector and a much stronger Shilling. NGSE ASI was the largest decliner, recording losses of 20.9% with the performance being skewed by the weakening of the Nigerian Naira following a recent decision by the Central Bank of Nigeria to adopt a floating exchange rate regime. Below is a summary of the performance of key indices as at the end of 2024;

*The index values are dollarized for ease of comparison

According to the World Bank, the Sub-Saharan African economy is projected to grow at a rate of 3.0% in 2024, 0.6% points higher than the 2.4% recorded in 2023. Notably, the projection was revised downwards from the earlier forecast of 3.4%. The downward revision of the regional growth by the IMF is mainly due to the destruction of Sudan's economy in a civil war, weak external demand, tight global financial conditions and high inflationary pressures in most countries. Additionally, public debt is expected to remain high due to increased debt serving costs as a result of continued currency depreciation in the region and high interest rates in developed economies. The decline in the region’s economic growth is attributable to;

- The heightened inflationary pressures following the Russia-Ukraine conflict which has prompted higher interest rates worldwide leading to slowing international demand, elevated spreads, and ongoing exchange rate pressures,

- Rising risk of debt distress in the region is expected to weigh down on the region’s growth due to increased debt-serving costs as a result of continued currency depreciation and high interest rates in developed economies, and,

- High interest rates in developed economies have led to a decline in foreign capital in the region further fueling the economic decline in the SSA.

Currency Performance

In 2024, most of the select Sub-Saharan currencies depreciated against the US Dollar, mainly attributable to the elevated inflationary pressures in the region, high debt servicing costs that continue to dwindle foreign exchange reserves, and monetary policy tightening by advanced economies. The high interest rates in developed countries have led to massive capital outflows from the region as investors, both institutional and individual seek to take advantage of the higher returns offered in developed economies. Further, the elevated inflationary pressures in most economies in the region puts pressure on the value of local currencies due to expensive importation. The table below shows the performance of select African currencies against the USD;

|

Cytonn Report: Select Sub-Saharan Africa Currency Performance vs USD |

|||||

|

Currency |

Dec-22 |

Dec-23 |

Dec-24 |

2023 y/y change (%) |

2024 y/y change (%) |

|

Kenyan Shilling |

123.4 |

156.5 |

129.3 |

(26.8%) |

17.4% |

|

Tanzanian Shilling |

2334.0 |

2540.0 |

2394.8 |

(8.8%) |

5.7% |

|

Ugandan Shilling |

3683.0 |

3815.0 |

3670.3 |

(3.6%) |

3.8% |

|

South African Rand |

17.4 |

18.3 |

18.7 |

(5.1%) |

(2.3%) |

|

Malawian kwacha |

1026.6 |

1683.4 |

1734.0 |

(64.0%) |

(3.0%) |

|

Botswana Pula |

12.8 |

13.4 |

13.9 |

(5.1%) |

(3.9%) |

|

Senegal CFA Franc |

601.3 |

602.8 |

638.9 |

(0.2%) |

(6.0%) |

|

Mauritius Rupee |

44.4 |

44.5 |

47.5 |

(0.2%) |

(6.7%) |

|

Zambian Kwacha |

19.0 |

25.7 |

27.9 |

(35.2%) |

(8.4%) |

|

Ghanaian Cedi |

8.6 |

11.9 |

14.7 |

(38.5%) |

(23.7%) |

|

Nigerian Naira |

448.1 |

899.4 |

1535.3 |

(100.7%) |

(70.7%) |

Key take outs from the table include:

- The Kenya Shilling appreciated the most by 17.4% in 2024 to close at Kshs 129.3 against the US Dollar, compared to Kshs 156.5 recorded at the beginning of the year, driven by improved forex reserves currently at USD 9.0 bn (equivalent to 4.6-months of import cover), which is above the statutory requirement of maintaining at least 4.0-months of import cover and the EAC region’s convergence criteria of 4.5-months of import cover coupled with the successful issuance of a USD 1.5 billion Eurobond in February 2024 to refinance the maturing June 2024 Eurobond which reduced Kenya's immediate repayment risks, and,

- The Nigerian Naira was the worst performer during the year, depreciating by 29.1% against the dollar, attributable to the deteriorated macroeconomic environment, evidenced by its elevated inflation, with the December 2024 inflation rate coming in at a record of 34.6% compared to 28.9% recorded in December 2023. Further, the recent decision by the Central Bank of Nigeria to adopt floating exchange rate regime, where the currency value of the Naira is allowed to vary according to the foreign exchange market hence making the overvalued naira to undergo a massive devaluation, broadly aligning the currency with its black-market rate.

African Eurobonds:

Africa’s appetite for foreign-denominated debt has increased in recent times with the latest issuers during year being Ivory Coast, Benin, Kenya, Senegal and Cameroon raising a total of USD 2.6 bn, USD 0.8 bn, USD 1.5 bn, USD 0.8 bn and USD 0.6 bn respectively. Notably, all the bonds were oversubscribed with the high support being driven by the yield hungry investors and also the outlook of positive recovery in the regional economies. It is good to note that there was a general decline in the yields of the various bonds from different countries due to general improvement in investor sentiment as the economy recovers and the easing inflationary pressures in the region. The yields of the Benin’s 13-year Eurobond maturing in 2032 decreased marginally by 0.9% points to 7.2% as at the end of December 2024 from 8.0% recorded at the beginning of the year. Similarly, the yields of the Kenya’s 10-year Eurobond maturing in 2028 decreased by 1.4% points to 9.0% as at the end of December 2024 from 10.4% at the beginning of the year, partly attributable to improved investor confidence following the successful buy-back of the 2024 Eurobond maturity, increased IMF Credit funding and the strengthening of the Kenyan shilling against the dollar. Below is a graph showing the Eurobond secondary market performance of select Eurobonds issued by the respective countries.

Equities Market Performance:

Sub-Saharan Africa (SSA) stock markets recorded mixed performance in 2024, with the Nairobi All Share Index (NASI) being best performing market gaining by 61.8% in 2024 largely driven by gains in the large-cap stocks in the financial sector following improved earnings during the period, well supported by easing inflation and a stronger Shilling. In addition, the improved macroeconomic environment supported by the IMF financial assistance has continued to accelerate investor confidence in the country. Notably, Nigeria all share index declined by 20.9% in 2024, due to the aggressive depreciation of the Nigerian Naira against the dollar having depreciated by 29.1% in 2024 which has resulted to increased capital outflows in the country. Additionally, the reduction in oil production in Nigeria has led to the contraction of many key sectors of the economy considering that the country’s economy is highly dependent on crude oil exports. Below is a summary of the performance of the key SSA indices;

|

Cytonn Report: Equities Market Performance |

||||||

|

Country |

Index |

Dec-22 |

Dec-23 |

Dec-24 |

2023 y/y change (%) |

2024 y/y change (%) |

|

Kenya |

NASI |

1.0 |

0.6 |

1.0 |

(42.9%) |

61.8% |

|

Uganda |

USEASI |

0.3 |

0.2 |

0.3 |

(32.0%) |

45.4% |

|

Zambia |

LASILZ |

389.5 |

420.6 |

577.1 |

8.0% |

37.2% |

|

Ghana |

GSECI |

195.5 |

254.5 |

330.7 |

30.2% |

29.9% |

|

Tanzania |

DARSDEI |

0.8 |

0.7 |

0.9 |

(15.6%) |

25.3% |

|

South Africa |

JALSH |

4,317.1 |

4,137.9 |

4,494.3 |

(4.2%) |

8.6% |

|

Rwanda |

RSEASI |

0.1 |

0.1 |

0.1 |

(15.7%) |

(7.1%) |

|

Nigeria |

NGEASI |

114.6 |

84.9 |

67.1 |

(26.0%) |

(20.9%) |

|

*The index values are dollarized for ease of comparison |

||||||

The tough macroeconomic environment experienced in the region is expected to slow down economic growth. As such, subdued GDP growth rate in Sub-Saharan Africa is expected to continue in 2024, in line with the rest of the global economy. Elevated inflation rates, debt sustainability concerns, and supply chain constraints in the region are expected to persist in 2024, and this will continue to weigh down its economic growth. Additionally, the continued weakening of local currencies will even make debt servicing costlier, and this will lead to increased perceived risks in the region, resulting in reduced investor confidence in the region.

Economic Growth:

According to the Kenya National Bureau of Statistics (KNBS) Q2’2024 Quarterly Gross Domestic Product Report, the Kenyan economy recorded a 4.6% growth in Q2’2024, slower than the 5.6% growth recorded in Q2’2023. The main contributor to Kenyan GDP remains to be the Agriculture, Fishing and Forestry sector which grew by 4.8% in Q2’2024, lower than the 7.8% expansion recorded in Q2’2023. Most sectors recorded lower growth rates compared to Q2’2023 with Accommodation and Food Services and Financial & Insurance recording growth of 26.6%, 5.1%, compared to, 42.8%, 13.2% growth in Q2”2023 respectively. The slowed growth in the economy could be attributed to the still elevated fuel prices which made production more expensive and negatively impacted the business environment and the unrest caused by the anti-finance bill protests in June. The Kenyan Economy is projected to grow at an average of 5.3% in 2024 according to various organizations as shown below:

|

Cytonn Report: Kenya 2024 Growth Projections |

||

|

No. |

Organization |

2024 GDP Projections |

|

1 |

International Monetary Fund |

5.3% |

|

2 |

National Treasury |

5.5% |

|

3 |

World Bank |

5.2% |

|

4 |

Fitch Solutions |

5.2% |

|

5 |

Cytonn Investments Management PLC |

5.4% |

|

Average |

5.3% |

|

Source: Cytonn Research

In 2024, the Kenyan economy is projected to grow at an average of 5.3%, lower than the growth of 5.6% observed in 2023. The slower growth is primarily attributable to reduced private sector activity and ongoing fiscal consolidation efforts by the government, which have limited public spending. Additionally, political instability during the year, fueled by anti-finance bill protests and opposition against the current regime, has undermined investor confidence and disrupted economic activities. This instability is expected to further weigh on economic growth.

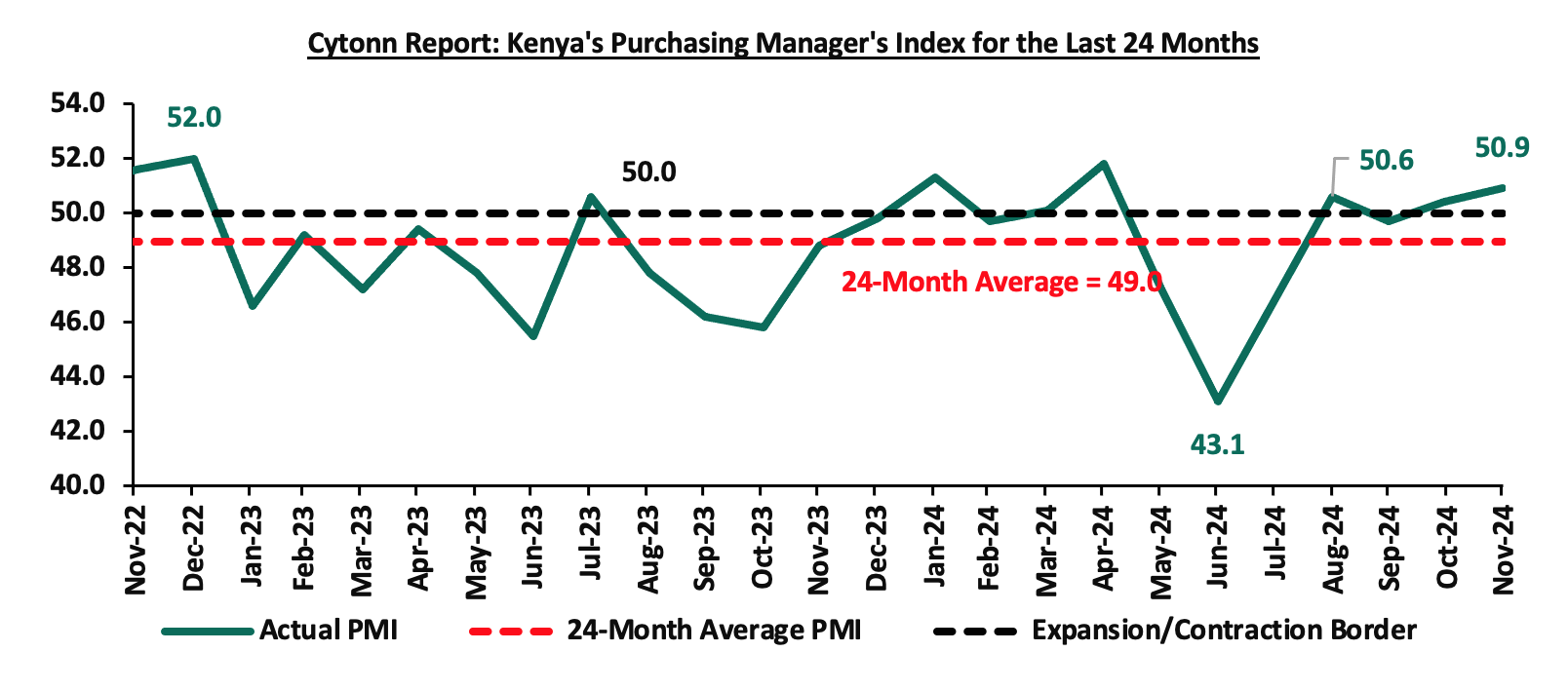

Business conditions in the Kenyan private sector recorded an improvement during the year, with the average Stanbic Bank Monthly Purchasing Managers’ Index (PMI) for the first eleven months averaging at 49.5, 1.5 points higher than the average of 48.0 recorded during a similar period in 2023. Similarly, PMI for the month of November 2024 came in at 50.9, up from 50.4 in October 2024 signaling an uptick of the business environment for the second consecutive month. This was majorly attributable to stable fuel prices and a decrease in borrowing costs, which resulted to the increase sales to its strongest performance in six months. The chart below shows the trend of Kenya’s Purchasing Managers index for the last 24 months;

Source: Stanbic PMI

Kenyan Shilling:

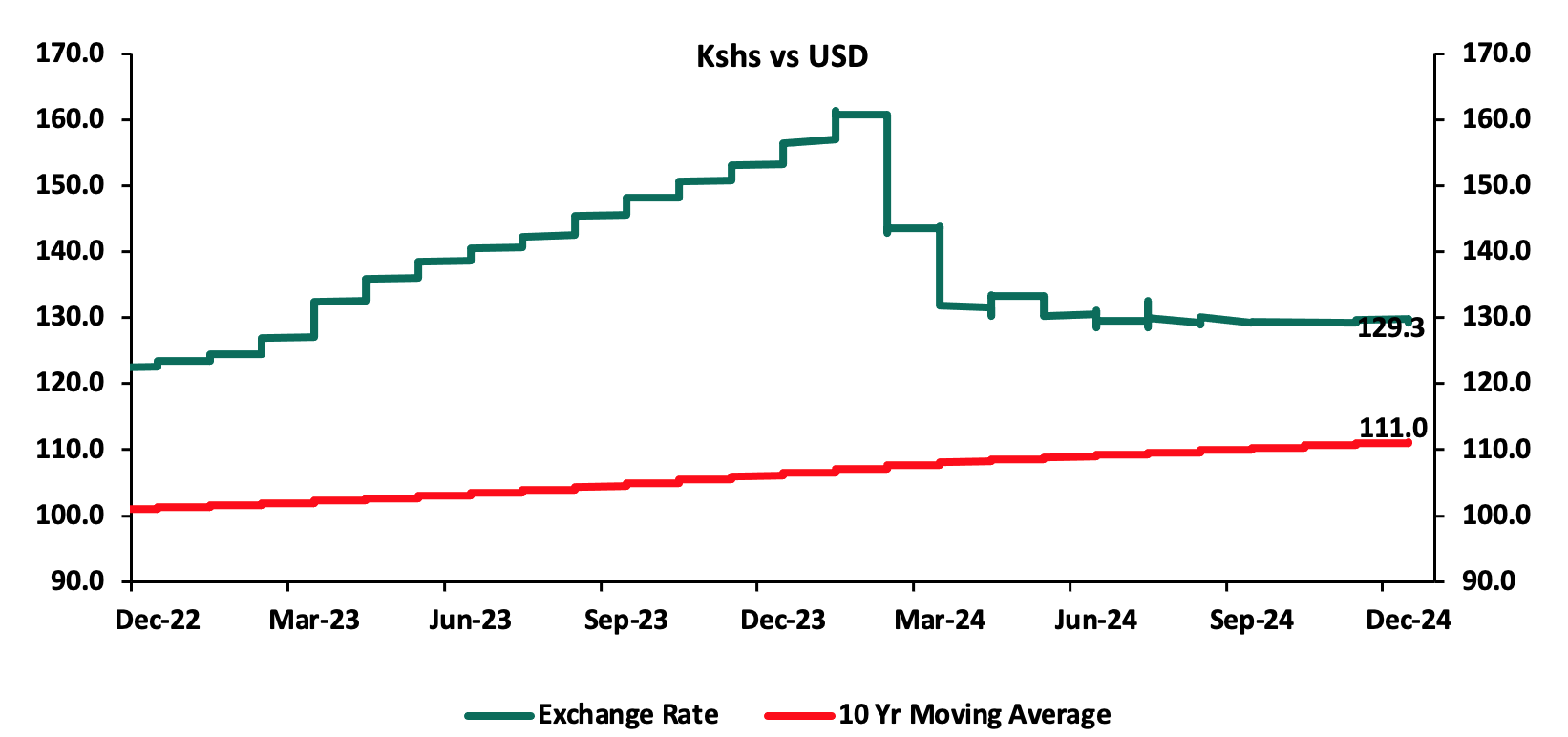

The Kenya Shilling appreciated by 17.4% against the US Dollar to close at Kshs 129.3 in 2024, compared to Kshs 156.5 at the end of 2023, a contrast to the 26.8% depreciation recorded in 2023. The chart below highlights the performance of the Kenyan Shilling against the US Dollar in 2024;

Source: Central Bank of Kenya

The appreciation of the Kenyan shilling in 2024 was driven by;

- Improved diaspora remittances standing at a cumulative USD 4,872.0 mn in the 12 months to November 2024, 16.7% higher than the USD 4,175.0 mn recorded over the same period in 2023. In the November 2024 diaspora remittances figures, North America remained the largest source of remittances to Kenya accounting for 53.4% in the period,

- CBK’s supportive activities in the money market, such as repurchase agreements and selling of dollars,

- Foreign loan disbursements, with the government receiving a total USD 3.1 bn out of the committed USD 3.6 bn from International Monetary Fund (IMF) as of November 2024 under the 38-month Extended Fund Facility (EFF) and Extended Credit Facility (ECF), as well as USD 180.4 mn out of the committed USD 541.3 mn from the Resilience Sustainability Facility (RSF) following the completion of the second review in November 2024, and,

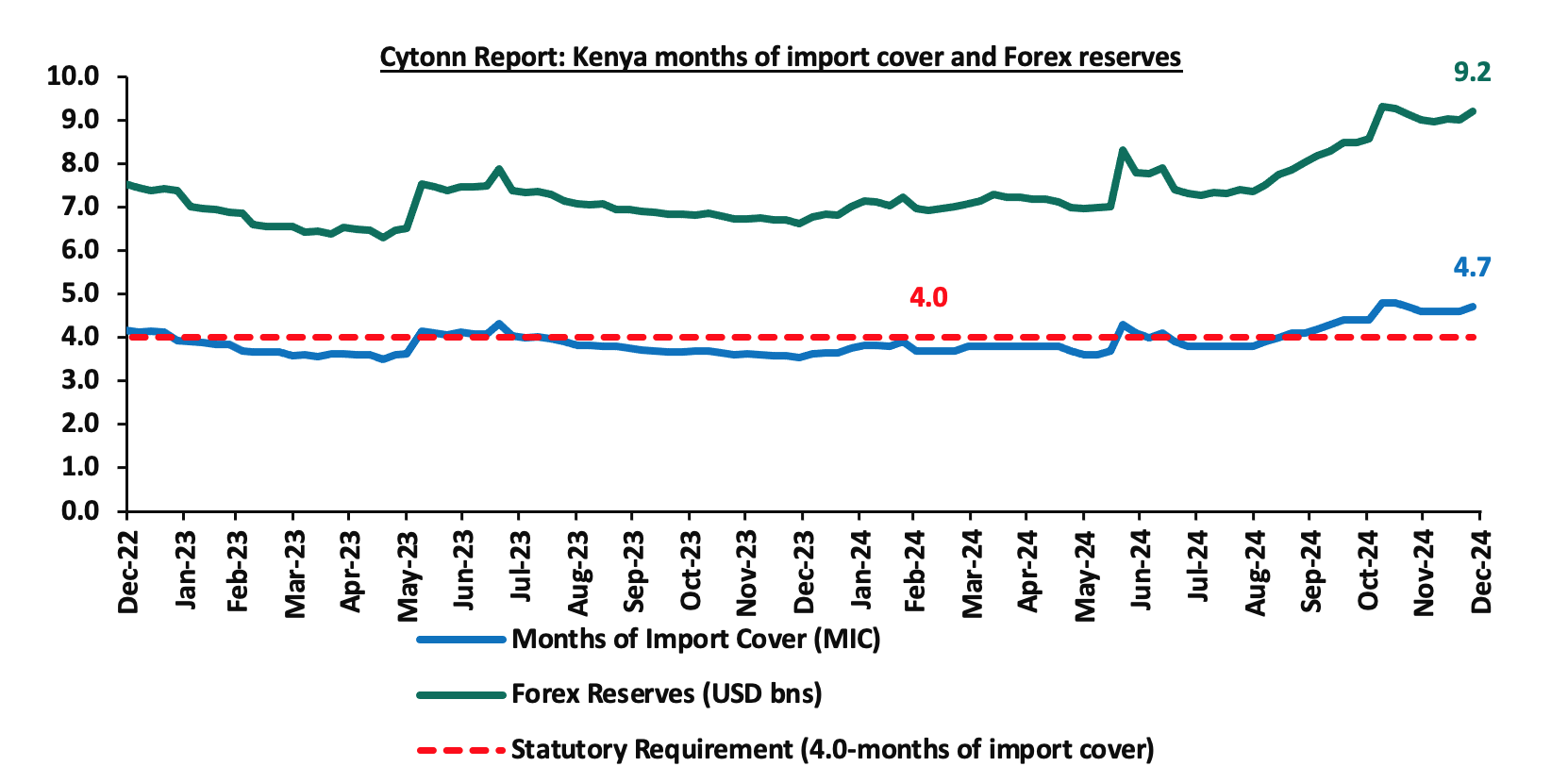

- Improved forex reserves currently at USD 9.2 bn (equivalent to 4.7-months of import cover), which is above the statutory requirement of maintaining at least 4.0-months of import cover and the EAC region’s convergence criteria of 4.5-months of import cover. The following is a graph showing Kenya months of import cover and forex reserves for the last 10 years;

Source: Central Bank of Kenya

The shilling was however weighed down by:

- An ever-present current account deficit which came at 3.8% of GDP in Q2’2024 from 3.7% recorded in a similar period last year. Key to note, the current account deficit narrowed by 34.5% to Kshs 104.1 bn from Kshs 159.0 bn in Q2’2023. The y/y narrowing of the current account was brought about by the 3.7% narrowing in Merchandise trade deficit to Kshs 341.2 bn in Q2’2024, from Kshs 354.3 bn in Q2’2023 driven by the 10.9% growth in merchandise exports to Kshs 276.2 bn, from Kshs 249.1 bn in Q2’2023 which outpaced the 2.3% increase in merchandise imports to Kshs 617.5 bn from Kshs 603.4 bn recorded in a similar period in 2023, and,

- The need for government debt servicing, continues to put pressure on forex reserves given that 67.2% of Kenya’s external debt is US Dollar-denominated as of June 2024.

The Kenyan shilling gained by 17.4% in 2024 to close the year at Kshs 129.3. We expected the shilling to remain within a range of Kshs 183.2 and Kshs 189.6 against the USD by the end of 2024 with a bias towards a 16.4% depreciation by the end of the year. The shilling’s appreciation against the USD dollar overshot our projection due to the aggressive mechanism by the CBK to allow the currency exchange rate reach an equilibrium hence hitting its true value as well the USD 1.5 bn Eurobond buyback in February. Read on our outlook on Performance of Kenya Currency. Looking ahead, we expect the currency to continue to remain steady in the short term with CBK's interventions and favorable foreign exchange inflows likely to play a crucial role in mitigating excessive volatility.

Inflation:

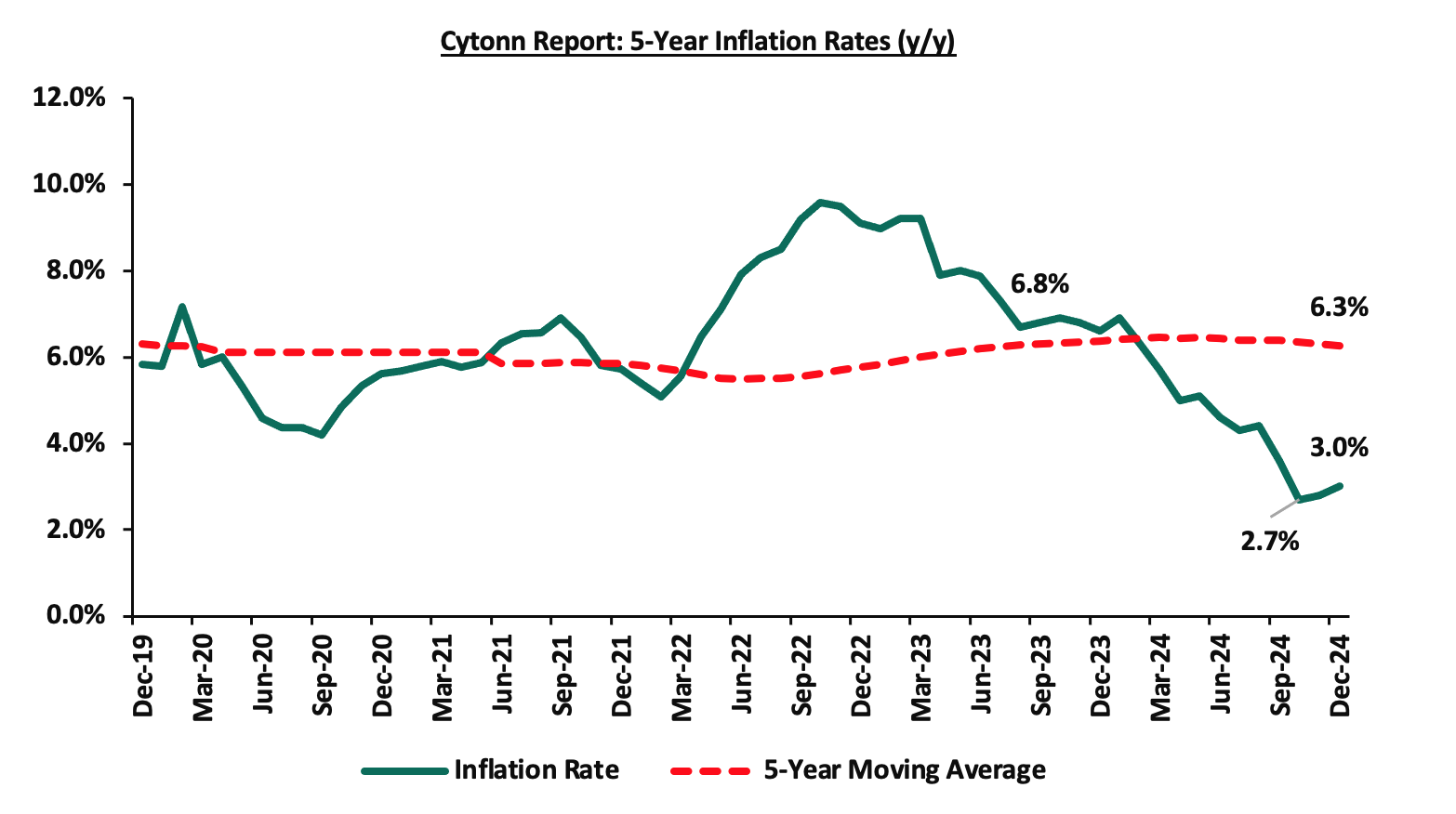

The inflation rate for the year 2024 averaged at 4.5%, compared to 7.7% recorded in 2023. Notably, the y/y inflation in December 2024 increased slightly by 0.2% points to 3.0%, from the 2.8% recorded in November 2024. The headline inflation in December 2024 was majorly driven by increases in prices of commodities in the following categories; Food & Non-Alcoholic Beverages, and Transport sector by 4.8% and 0.2% respectively. However, the commodity prices in Housing, Water, Electricity, Gas & other fuels declined by 0.2%.

Going forward, we expect inflation to remain within the CBK’s preferred range of 2.5%-7.5%, mainly on the back of a stronger currency and stable fuel prices. Additionally, favourable weather conditions will also contribute to stabilizing of food prices, further supporting lower inflation rates. The risk, however, lies in the fuel prices which despite their decline over the last months, still remain elevated compared to historical levels. Key to note is that the Monetary Policy Committee cut the Central Bank Rate by 75.0 bps to 11.25% from 12.00% in its December 2024 meeting. This cut in the Central Bank Rate is likely to elevate inflationary pressures as consumer spending rises leading to demand- pull inflation. The committee is expected to lower rates further , though gradually, to provide further support for the economy.

Monetary Policy:

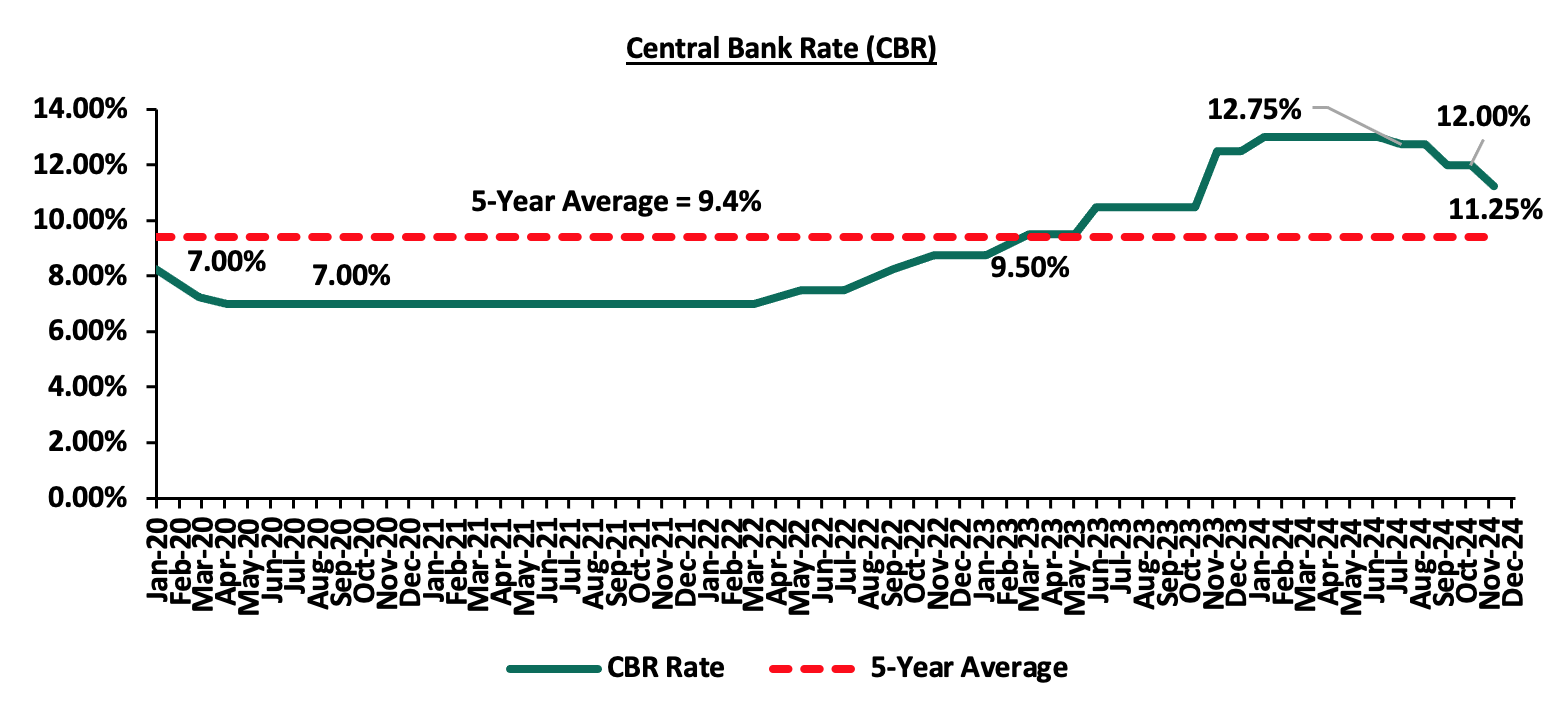

During the year the Monetary Policy Committee (MPC) met 6 times where it raised the Central Bank Rate (CBR) to 13.00% from 12.50% in the first meeting held in February. The MPC then retained the rate in its April and June sittings, in a bid to stabilize the currency and anchor inflation. In August, the MPC initiated a series of rate cuts, lowering the CBR by 25.0 bps to 12.75%, followed by a further reduction of 75.0 bps to 12.00% in October on the back of a strengthened and stable currency, easing inflation which fell below the mid-point of the CBK’s target of a range 0f 2.5% - 7.5%. In its latest meeting held in December, the MPC lowered the CBR rate by 75.0 bps to 11.25%, from 12.00% which was in line with our expectation for the MPC to lower the CBR rate. Our expectation to cut the rate was mainly on the back of rate cuts by some major economies, a stable exchange rate, anchored inflationary pressures, with inflation coming in at 2.8% in November 2024, marginally up from 2.7% in October 2024, as well as the need to support the economy by adopting an accommodative policy that will ease financing activities. In total, MPC lowered the rates in 2024 by 1.75%, from 13.00% in February to 11.25% in December. We expect the MPC to continue lowering the rates in the short to medium term therefore lowering borrowing costs, leading to increased spending and an uptick in the business environment as well as reduced debt servicing costs for the government, and anchoring private sector credit growth, noting that its previous measures have successfully reduced overall inflation to below the mid-point of the target range of 2.5% - 7.5%, stabilized the exchange rate, and anchored inflationary expectations. The following is a graph highlighting the Central Bank Rate for the last 5 years;

Source: Central Bank of Kenya

2024 Key Highlights:

- FY’2024/2025 Budget Policy Statement

- On 13 June 2024, the National Treasury presented Kenya’s FY’2024/2025 National Budget to the National Assembly highlighting that the total budget estimates for FY’2024/25 increased by 3.1% to Kshs 4.0 tn from the Kshs 3.9 tn in FY’2023/2024 while the total revenue inclusive of grants increased by 15.2% to Kshs 3.4 tn from the Kshs 2.9 tn in FY’2023/2024. The increase is mainly due to an 18.5% increase in ordinary revenue to Kshs 2.9 tn for FY’2024/2025, from the Kshs 2.5 tn in FY’2023/24. For more information, please read our Budget Review Note.

- On July 12, 2024, the National Treasury presented the Supplementary Estimates I for the Fiscal Year 2024/25 to the National Assembly. This presentation outlined plans to adjust the FY’2024/25 Budget Estimates to align with the Revised Fiscal Framework and implement expenditure cuts, following the withdrawal of Finance Bill 2024 which sought to raise Kshs 344.3 bn. The recurrent expenditure (Costs incurred to cover regular government expenses such as salaries, operational costs and maintenance costs) decreased by 2.1% to Kshs 1,598.0 bn in the Supplementary Estimates I from Kshs 1,632.1 bn in the original estimates, an indication of the government's initiative to cut expenditure cuts while still boosting public services, responding to economic growth and ensuring the well-being of its citizens. For more information please see our Supplementary Budget Estimates I Note

- Credit Facilities extended to Kenya

- The Executive Board of the International Monetary Fund (IMF) concluded the 2023 Article IV consultation with Kenya together with the sixth reviews and augmentations of access of USD 941.2 mn (Kshs 151.3 bn) under the Extended Fund Facility (EFF) and the Extended Credit Facility (ECF) arrangements, and the first review under the 20-month Resilience and Sustainability Facility (RSF) arrangement, approved in July 2023. Please see our Cytonn Weekly 03/2024,

- The International Monetary Fund (IMF) team and Kenyan authorities reached a staff-level agreement for the seventh reviews of Kenya’s economic program supported by the IMF’s Extended Fund Facility (EFF) and Extended Credit Facility (ECF), and the second Review under the Resilience Sustainability Facility (RSF). Notably, the discussions considered Kenya’s request for an augmentation under the EFF/ECF arrangement and the RSF, which if approved by the IMF executive board, will lead to a potential total commitment of more than USD 3.6 bn during the program's duration. Furthermore, the IMF team and Kenyan authorities agreed on a set of comprehensive policies and reforms needed to complete the seventh review, entailing corrective measures to safeguard debt sustainability, and fiscal discipline following a slip in FY’2023/24 budget, where the government in expected to miss out on its revenue targets. Please see our Cytonn Weekly 24/2024, and,

- The International Monetary Fund (IMF) Executive Board completedthe seventh and eighth reviews under the Extended Fund Facility (EFF) and Extended Credit Facility (ECF), alongside a review under the Resilience Sustainability Facility (RSF). This decision enables the immediate disbursement of approximately USD 606.1 mn to support Kenya’s efforts to stabilize its economy, address fiscal challenges, and enhance resilience to climate-related shocks. The IMF’s approval allows Kenya to receive USD 485.8 mn under the EFF/ECF arrangements, aimed at reducing Kenya’s debt vulnerabilities, safeguarding funds for social and developmental priorities, and supporting broader economic reforms and USD 120.3 mn under the RSF, which focuses on reinforcing Kenya's climate-related initiatives and catalysing additional private sector climate finance. Please see our Cytonn Monthly October 2024 for more information.

- FY’2023/2024 KRA Revenue Performance

In July 2024, the Kenya Revenue Authority (KRA) released the annual revenue performance for FY’2023/24, highlighting that revenue mobilization for the period grew by a notable 11.1% up from 6.4% growth in the previous financial year, after KRA collected Kshs 2.4 tn compared to Kshs 2.2 tn in the previous financial year. This translates to a performance rate of 95.5% against the target. Please see our Cytonn Weekly 28/2024,

- Balance of Payments

Kenya National Bureau of Statistics released the Q2’2024 Balance of Payment Report, noting that Kenya’s balance of payments position deteriorated by 45.0% in Q2’2024 with a reduction of the surplus to Kshs 84.1 bn, from a surplus of Kshs 152.9 bn in Q2’2023 but was a significant improvement from the Kshs 36.0 bn deficit recorded in Q1’2024. Please see our Cytonn Weekly 37/2024,

- Current account

Kenya’s current account deficit narrowed by 34.5% to Kshs 104.1 bn in Q2’2024 from the Kshs 159.0 bn deficit recorded in Q2’2023. The y/y contraction registered was driven by the narrowing of the merchandise trade account deficit (the value of import goods exceeds the value of export goods, resulting in a negative net foreign investment) by 3.7% to Kshs 341.2 bn in Q2’2024, from Kshs 354.3 bn recorded in Q2’2023, a 59.1% improvement in the secondary trade balance to a surplus of Kshs 43.6 bn from a surplus of Kshs 27.4 bn in Q2’2023, and, the narrowing of the primary income deficit (the earnings that residents of a country receive from their investments abroad and the compensation they receive for providing labour to foreign entities) by 34.6% to Kshs 45.6 bn in Q2’2024, from Kshs 69.8 bn recorded in Q2’2023.

- Credit Ratings

- On July 8th 2024, the global ratings agency, Moody’s announced its revision of Kenya’s credit score, downgrading it to Caa1 from a credit rating of B3 while maintaining a negative outlook, on the back of on the back of of the government's decision to forgo proposed tax increases through the Finance Bill 2024 and rely on expenditure cuts, significantly impacting Kenya's fiscal trajectory and financing needs. The downgrade of Kenya's rating indicates a greatly reduced ability to implement fiscal consolidation measures focused on revenue, which are necessary to improve debt affordability and reduce overall debt. Please see our Cytonn Weekly 30/2024.

- On 2nd August 2024 the global ratings agency, Fitch Ratings announced its revision of Kenya’s credit score, downgrading it to B- from a credit rating of B while also revising the outlook to stable, from a negative outlook affirmed on 16th February 2024. Their decision comes on the back of the government's decision to forgo proposed tax increases through the Finance Bill 2024 and rely on expenditure cuts, significantly impacting Kenya's fiscal trajectory and financing needs. The downgrade follows Moody’s downgrading Kenya’s IDR to Caa1 from a credit rating of B3 while maintaining a negative outlook on July 8th Please see our Cytonn Weekly 32/2024, and,

- On 23rd August 2024 S&P Global Ratings announced its revision of Kenya’s long-term sovereign credit rating, downgrading it to B-, and a stable outlook from a credit rating of B and a negative outlook, on the back of the government's decision to forgo proposed tax increases through the Finance Bill 2024 and rely on expenditure cuts, significantly impacting Kenya's fiscal trajectory and financing needs. Please see our Cytonn Weekly 34/2024. For more information, see our, Cytonn Q3'2024 Markets Review. Below is a summary of the credit rating on Kenya by various rating agencies;

|

Cytonn Report: Kenya’s Credit Ratings |

||||||

|

Rating Agency |

Previous Rating |

Previous Outlook |

Current Rating |

Current Outlook |

Meaning |

Date Released |

|

Moody's Rating |

B3 |

Negative |

Caa1 |

Negative |

Substantial credit risks |

8th July, 2024 |

|

Fitch Ratings |

B |

Negative |

B- |

Stable |

Highly Speculative |

2nd August 2024 |

|

S&P Global |

B |

Negative |

B- |

Stable |

Extremely high risk, very vulnerable to default |

23rd August 2024 |

Source: Fitch Ratings, S&P Global, Moody’s

2024 Returns by Various Asset Classes:

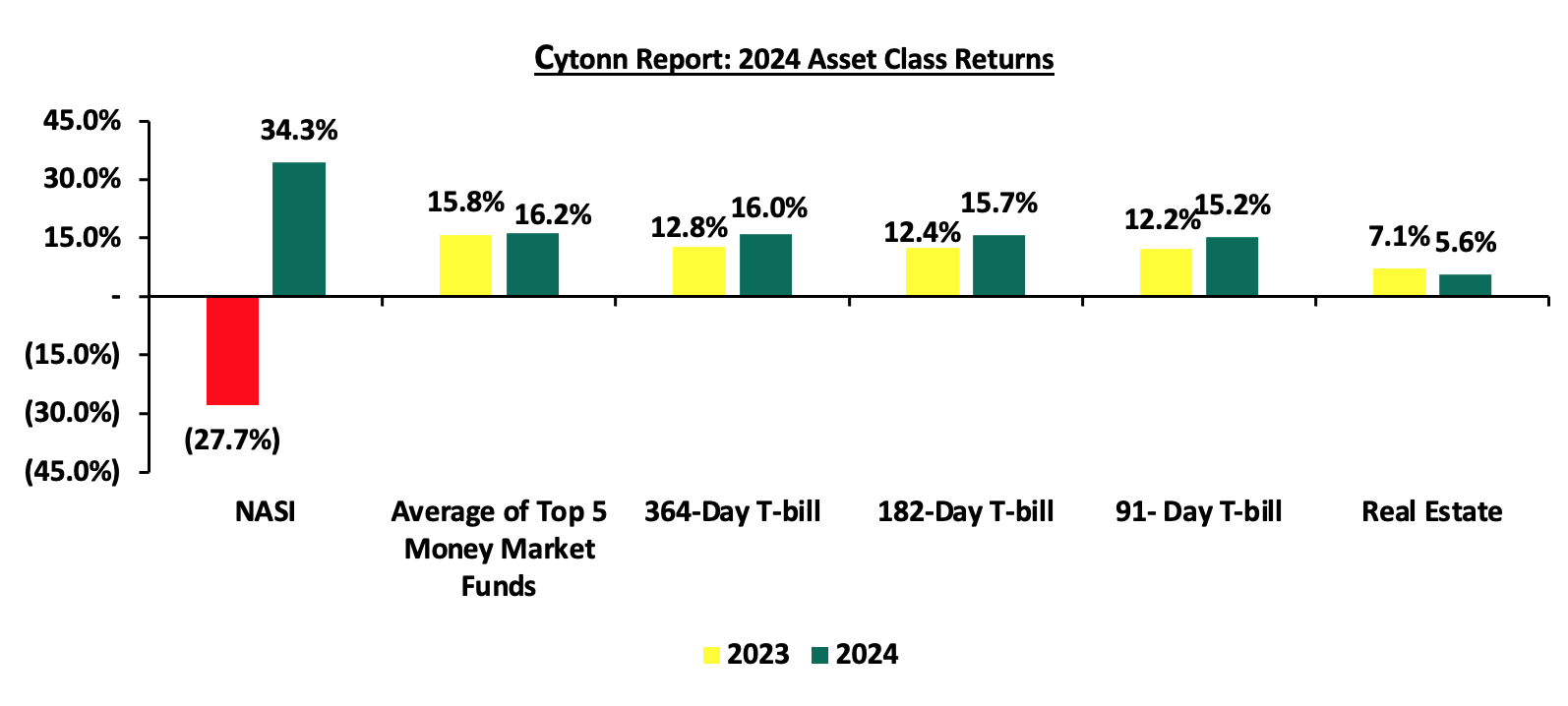

The returns by the various asset classes recorded mixed performances in 2024, in comparison to a similar period last year, with the NASI and the average of the top five money market funds (MMFs), being on upward trajectories. For the equities class, NASI registered a 34.3% gain in 2024, a significant improvement from the 27.7% loss recorded in 2023, as the average of top 5 MMFs recorded a yield of 16.2%, 0.5% points higher than the 15.8% average recorded in 2023. Additionally, the 364-day, 182-day and 91-day Government papers recorded average yields of 16.0%, 15.7% and 15.2%, respectively, higher than the average yields of 12.8%, 12.4% and 12.2%, respectively recorded in 2023, while the average Real Estate yield also decreased by 1.5% points to 5.6% in 2024, from 7.1% recorded in 2023. The graph below shows the summary of returns by various asset classes (Average top 5 MMF, Fixed Income, Real Estate and Equities).

The table below shows the macro-economic indicators that we track, indicating our expectations for each variable at the beginning of 2024 versus the experience;

|

Cytonn Report: Macro-Economic & Business Environment Outlook |

||||

|

Macro-Economic Indicators |

2025 Outlook |

Effect |

2024 Experience |

Effect |

|

Government Borrowing |

|

Negative |

· The government’s domestic debt stood at Kshs 5.6 tn as of September 2024, 8.0% higher than external debt that came in at Kshs 5.2 tn in the same period. Notably, domestic debt recorded an 10.9% increase from the year’s opening position of Kshs 5.0 tn relative to a 14.1% decline in external debt from the year’s opening position of Kshs 6.1 tn. The higher growth in domestic debt indicates the government’s preference for domestic borrowing in line with our expectation of aggressive borrowing in the domestic front during the year, · The government is 161.6% ahead its prorated borrowing target of Kshs 212.1 bn having borrowed Kshs 554.8 bn of the Kshs 408.4 bn borrowing target for the FY’2023/24, · Kenya’s debt to GDP ratio came in at an estimated 71.8% as of June 2024, 21.8% points above the IMF recommended threshold of 50.0% for developing nations, and 1.8% points increase on a Year on year basis from 70.8% recorded in June 2023, · The government tapped into the international markets for debt, to raise cash and buy back the 10-year Eurobond of USD 2.0 bn through the issuance of a new USD 1.5 bn Eurobond successfully redeeming the 10-year Eurobond due in June 2024. · Total revenue collected as at the end of November 2024 amounted to Kshs 940.9 bn, equivalent to 35.8% of the revised estimates of Kshs 2,631.4 bn for FY’2024/2025 and is 85.8% of the prorated estimates of Kshs 1,096.4 bn, indicating an underperformance in revenue collection, · We foresee that the collected revenue will fall short of covering the government’s deficit. Consequently, we predict that the government will intensify its domestic borrowing to compensate for the fiscal deficit, projected to be 4.1% of GDP for the FY’2024/25 budget. |

Negative |

|

Exchange Rate |

|

Negative |

· The Kenya Shilling appreciated by 17.4% against the US Dollar to close at Kshs at Kshs 129.3 in 2024, compared to Kshs 156.5 at the end of 2023. We note that the continuous appreciation of the shilling during the year was caused by CBK’s aggressive efforts to support the shilling, improved diaspora remittances standing at a cumulative USD 4,872.0 mn in the 12 months to November 2024 and improved forex reserves. · The forex reserves increased by 35.8% to USD 9.2 bn from USD 6.8 bn at year opening, with the former translating to 4.7 months of import cover, meeting the CBK’s statutory requirement to endeavor to maintain at least 4.0 months of import cover

|

Positive |

|

Interest Rates |

|

Neutral |

· In the first half of 2024, yields on government securities were on an upward trajectory primarily due to the government’s amplified borrowing needs and investors’ pursuit of higher returns to mitigate the impact of the inflation rates observed in the first half of the year. The second half of the year saw a decline in yields as a result of lower interest rates. · During the year, the MPC lowered the central bank rate by a cumulative 1.7% points to 11.25% from 13.00%, with the Kenya Shilling having gained and stabilized against the USD and inflation eased closing the year at 3.0% · Notably, the government's ability to meet coupon payments and successfully redeem the 10-year Eurobond in June 2024 provided much-needed confidence in Kenya's fiscal management. |

Positive |

|

Inflation |

|

Neutral |

· Having averaged at 4.5% in 2024, the inflation rate was within the government’s target range of 2.5% - 7.5%. Notably, on a monthly basis, the inflation rate came in at 3.0% in December 2024, marking the eighteenth consecutive month that the inflation rate remained within the government’s target range, · Going forward, we expect inflation to remain within the CBK’s preferred range of 2.5%-7.5%, mainly on the back of a strengthened currency and stable fuel prices. Additionally, favourable weather conditions will also contribute to stabilizing food prices, further supporting lower inflation rates. The risk, however, lies in the fuel prices which despite their decline over the last months, still remain elevated compared to historical levels. Key to note is that the Monetary Policy Committee cut the Central Bank Rate by 75.0 bps to 11.25% from 12.00% in its December 2024 meeting, with the aim of easing the monetary policy, while maintaining exchange rate stability, and will meet again in February 2025. This cut in the Central Bank Rate is likely to elevate inflationary pressures as consumer spending rises leading to demand- pull inflation. |

Positive |

|

GDP |

|

Neutral |

· With the economy having grown at average of 4.8% in the first two quarters of 2024. Given the growth momentum observed during the year, Kenya’s GDP growth is currently below the projected growth of 5.3%. The slower growth is primarily driven by reduced private sector activity and ongoing fiscal consolidation efforts by the government, which have limited public spending. Additionally, political instability during the year, fueled by anti-finance bill protests and opposition against the current regime, has undermined investor confidence and disrupted economic activities. This instability is expected to further weigh on economic growth |

Neutral |

|

Investor Sentiment |

|

Neutral |

· With the appreciation of the Kenyan shilling and reducing debt sustainability concerns, companies trading in the Nairobi Securities Exchange (NSE) have recorded relatively high trade volumes throughout the year, · The NSE has experienced capital inflows and repatriation with the NSE equity turnover increasing by 22.0% to close the year at USD 0.8 bn in 2024 from USD 0.6 bn recorded in 2023, · Further, the government's ability to meet coupon payments and successfully redeem the 10-year Eurobond in June 2024 provided much-needed confidence in Kenya's fiscal management, boosting investor confidence · Majority of companies are trading at higher prices relative to the year opening prices, signaling overvaluation |

Positive |

|

Security |

|

Positive |

· The country witnessed heightened political tensions in June and July following the mass demonstrations against the Finance Bill 2024 resulting in business disruption in several parts of the country. However, the government withdrew the Bill, restoring peace in the country in the second half of 2024. Despite this, the current regime still faces opposition fueling political instability in the country. |

Negative |

Since the beginning of the year, the notable changes we have seen out of the seven metrics that we track, fall under three metrics, namely; the GDP, investor sentiment, and Security. Key to note, economic growth remained neutral, while investor sentiments and security changed from neutral and positive respectively to positive and negative respectively. In conclusion, macroeconomic fundamentals showed mixed performance during the year with most metrics on upward trajectories. We expect a slight recovery in 2024 supported by the improving economic conditions in the country evidenced by momentum in GDP growth and declining inflation with the rate remaining within target range of 2.5% to 7.5% for the eighteenth consecutive month, driven by the improvement of the business conditions and stabilization of the Kenyan currency.

T-Bills & T-Bonds Primary Auction:

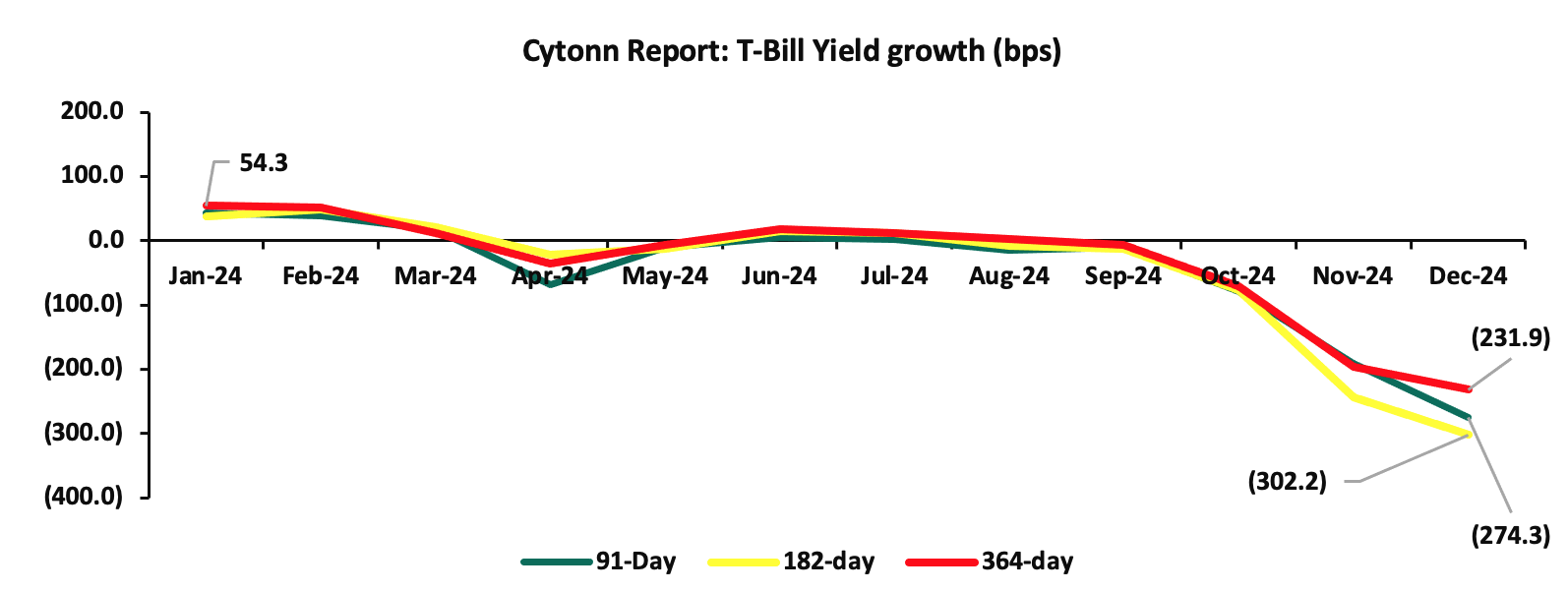

During the year, T-bills were oversubscribed, with the overall subscription rate coming in at 153.3%, up from 120.0% in FY’2023. Investors’ preference for the 91-day paper persisted as they sought to avoid duration risk, with the paper receiving bids worth Kshs 847.4 bn against the offered Kshs 212.0 bn, translating to an oversubscription rate of 399.7%, albeit lower than the oversubscription rate of 529.1% recorded in FY’2023. Overall subscription rates for the 364-day and 182-day papers came in at 103.0% and 104.9%, higher than the 29.0% and 48.5%, respectively, recorded in FY’2023. The average yields on the 364-day, 182-day, and 91-day papers were on an upward trajectory with the 182-day yields increasing the most by 330.6 bps to 15.7%, from 12.4% in 2023, while the 364-day and 91-day increased by 327.1 bps and 300.6 bps to 16.0% and 15.2% in 2024, from 12.8% and 12.2% in 2023, respectively. However, on y/y basis, the yields on the government papers registered significant decline in 2024 with the 91-day paper decreasing the most by 6.0% to close the year at 9.9% from the 15.9% recorded at the close of FY’2023, while the yields on the 182-day and 364-day decreased by 5.9% and 4.5% to close the year at 10.0% and 11.4%, from the 16.0% and 15.9%, respectively, recorded at the end of FY’2023. The year-on-year decline in yields is primarily driven by investors perceiving lower risks due to eased inflation, currency appreciation, and improved liquidity positions. As a result, there is less demand for higher returns to compensate for potential losses. The average acceptance rate during the period came in at 77.3%, albeit lower than the 92.5% recorded in FY’2023, with the government accepting a total of Kshs 1,507.3 bn out of the Kshs 1,949.4 bn worth of bids received. Notably, the decline in the government papers yields accelerated in December 2024 compared to November 2024, with the yields on the 91-day paper decreasing by 274.3 bps, compared to 190.8 bps decline that was recorded in November 2024, as the government manages the borrowing costs amid budgetary pressures. The chart below shows the yields growth rate for the 91-day, 182-day and 365-day papers during the year;

During the week, T-bills were undersubscribed for the fourth consecutive week, with the overall undersubscription rate coming in at 65.4%, higher than the undersubscription rate of 20.3% recorded the previous week. Investors’ preference for the shorter 91-day paper persisted, with the paper receiving bids worth Kshs 8.0 bn against the offered Kshs 4.0 bn, translating to an oversubscription rate of 199.7%, significantly higher than the undersubscription rate of 56.1% recorded the previous week. The subscription rates for the 182-day paper increased to 60.8% from the 4.4% recorded the previous week, while the subscription rate for the 364-day paper decreased to 16.3% from 21.9% recorded the previous week. The government accepted a total of Kshs 15.7 bn worth of bids out of Kshs 15.7 bn bids received, translating to an acceptance rate of 100.0%. The yields on the government papers recorded a mixed performance, with the yields on the 182-day paper increasing marginally by 0.4 bps to 10.03% from 10.02% recorded the previous week, while the yields on the 364-day and 91-day papers declined by 3.8 bps and 6.9 bps respectively to 11.37% and 9.83% from the 11.41% and 9.89% respectively recorded the previous week.

The chart below compares the overall average T- bills subscription rates obtained in 2018, 2022, 2023 and FY’2024;

Primary T-Bond Auctions in FY’2024

Primary T-bond auctions in 2024 were generally oversubscribed, with bonds receiving bids worth Kshs 1,137.9 bn against the offered Kshs 665.0 bn, translating to an oversubscription rate of 171.1%, higher than the oversubscription rate of 128.5% recorded in 2023. The government accepted Kshs 867.8 bn of the Kshs 1,137.9 bn worth of bids received, translating to an acceptance rate of 76.3%.

Additionally, in the primary bond market, the government is looking to raise Kshs 30.0 bn through the reopened fifteen year and twenty-five-year fixed coupon bonds; FXD1/2018/15 and FXD1/2022/25 with tenors to maturity of 8.3 years and 22.8 years respectively. The bonds will be offered at fixed coupon rates of 12.7% and 14.2% respectively. Our bidding range for the reopened bonds are 13.45%-13.85% and 15.65%-16.00% for the FXD1/2018/15 and FXD1/2022/25 respectively

Secondary Bond Market Activity:

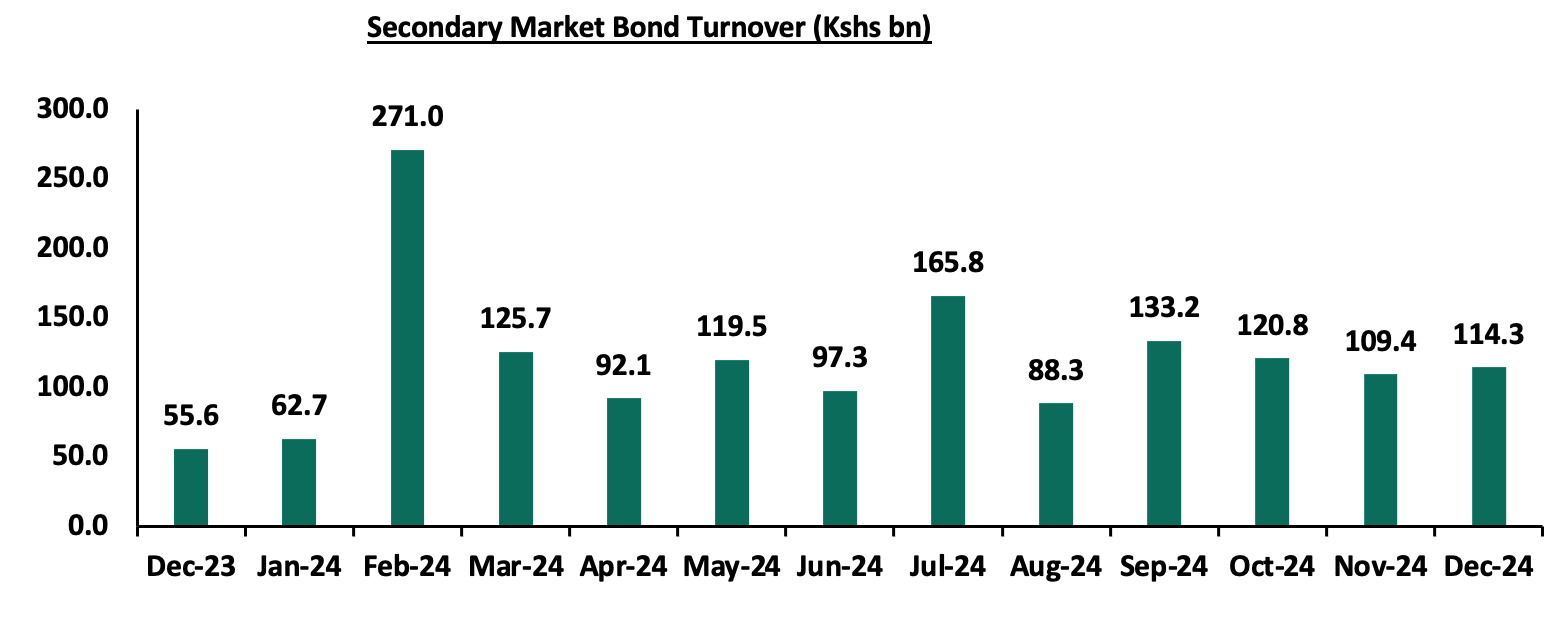

The secondary bond turnover increased by 4.5% to Kshs 114.3 bn in December 2024, from Kshs 109.4 bn recorded in November 2024, pointing towards increased activities by commercial banks in the secondary bonds market for the month of December. Similarly, on a year-on-year basis, the bond turnover increased by 105.5% from Kshs 55.6 bn worth of treasury bonds transacted over a similar period last year. The chart below shows the bond turnover over the past 12 months to December 2024;

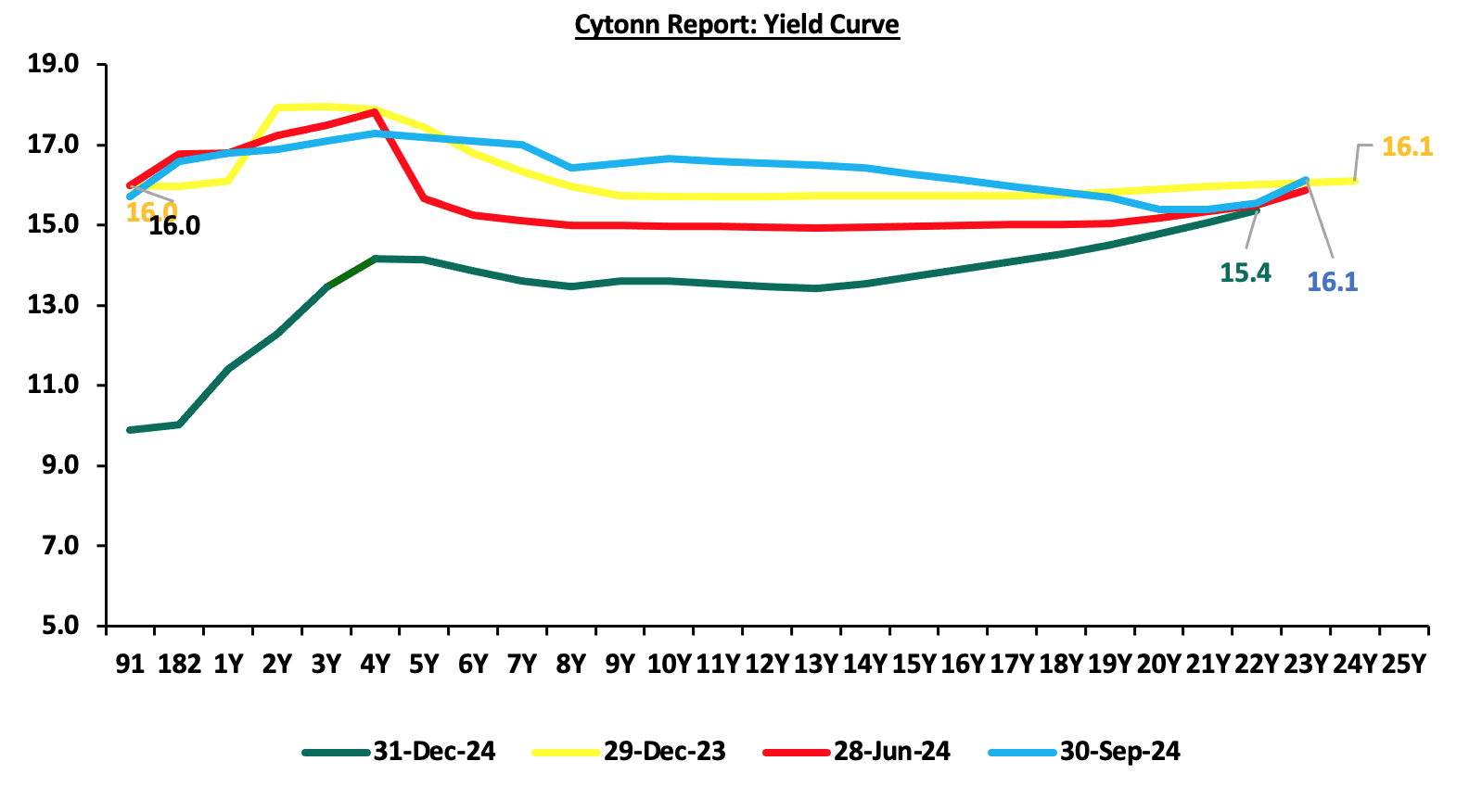

In 2024, the yield curve experienced a downward adjustment compared to 2023, primarily driven by decreased government borrowing, local currency appreciation, and eased inflation. These factors reduced the need for investors to demand higher yields as compensation for inflation and currency depreciation risks, resulting in an overall decline across the yield curve. Notably, the yield curve is adjusting from a humped yield curve observed at close of 2023 towards a normal upward sloping curve, with long-term bonds registering highest yields. The chart below is the yield curve movement during the period;

Money Market Performance:

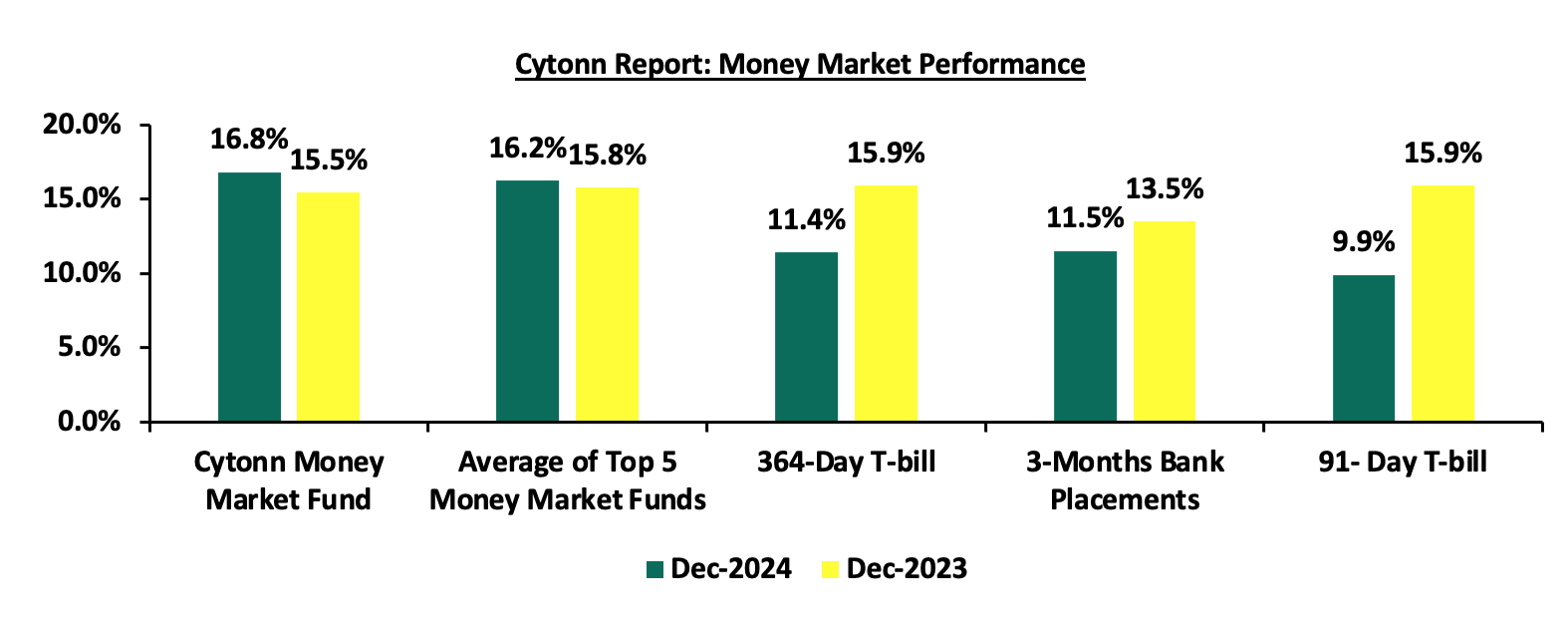

The 3-month bank placements recorded 11.5% at the end of FY’2024, 2.0% points lower than the 13.5%recorded at the end of FY’2023 (based on what we have been offered by various banks). The 91-day and 364-day papers decreased by 6.0% points and 4.5% to 9.9% and 11.4% at the end of 2024, from 15.9% and 15.9% at the end of FY’2023 respectively, while the average Top 5 Money Market Funds increased by 0.5% points to 16.2%, from 15.8% at the end of FY’2023. The yield on the Cytonn Money Market (CMMF) increased by 1.4% points to 16.8% at the end of FY’2024, from 15.5% recorded at the end of FY’2023.

During the week, 3-month bank placements ended the week at 11.5% (based on what we have been offered by various banks), and yields on the government papers decreased, with the yields on the 364-day and 91-day papers decreased by 3.8 bps and 6.9 bps to 11.4% and 9.8% respectively from 11.4% and 9.9% respectively recorded the previous week. The yield on the Cytonn Money Market Fund remained unchanged at the 16.8% recorded the previous week, while the average yields on the Top 5 Money Market Funds decreased by 6.0 bps to close the week at 16.2%, from 16.3% recorded the previous week. The table below shows the Money Market Fund Yields for Kenyan Fund Managers as published on 3rd January 2025:

|

Cytonn Report: Money Market Fund Yield for Fund Managers as published on 3rd January 2025 |

||

|

Rank |

Fund Manager |

Effective Annual Rate |

|

1 |

Cytonn Money Market Fund (Dial *809# or download the Cytonn App) |

16.8% |

|

2 |

Lofty-Corban Money Market Fund |

16.5% |

|

3 |

Gulfcap Money Market Fund |

16.3% |

|

4 |

Etica Money Market Fund |

16.1% |

|

5 |

Kuza Money Market fund |

15.9% |

|

6 |

Ndovu Money Market Fund |

15.5% |

|

7 |

Orient Kasha Money Market Fund |

15.5% |

|

8 |

Arvocap Money Market Fund |

15.4% |

|

9 |

Mali Money Market Fund |

15.2% |

|

10 |

Faulu Money Market Fund |

14.5% |

|

11 |

Sanlam Money Market Fund |

14.1% |

|

12 |

Madison Money Market Fund |

14.0% |

|

13 |

Dry Associates Money Market Fund |

13.9% |

|

14 |

Genghis Money Market Fund |

13.9% |

|

15 |

Jubilee Money Market Fund |

13.8% |

|

16 |

Enwealth Money Market Fund |

13.6% |

|

17 |

GenAfrica Money Market Fund |

13.5% |

|

18 |

Co-op Money Market Fund |

13.3% |

|

19 |

KCB Money Market Fund |

13.3% |

|

20 |

Nabo Africa Money Market Fund |

13.3% |

|

21 |

Apollo Money Market Fund |

13.1% |

|

22 |

British-American Money Market Fund |

13.0% |

|

23 |

Old Mutual Money Market Fund |

13.0% |

|

24 |

ICEA Lion Money Market Fund |

12.9% |

|

25 |

CIC Money Market Fund |

12.7% |

|

26 |

Absa Shilling Money Market Fund |

12.7% |

|

27 |

Ziidi Money Market Fund |

12.4% |

|

28 |

Mayfair Money Market Fund |

12.3% |

|

29 |

AA Kenya Shillings Fund |

11.7% |

|

30 |

Stanbic Money Market Fund |

11.2% |

|

31 |

Equity Money Market Fund |

8.7% |

Source: Business Daily

Liquidity:

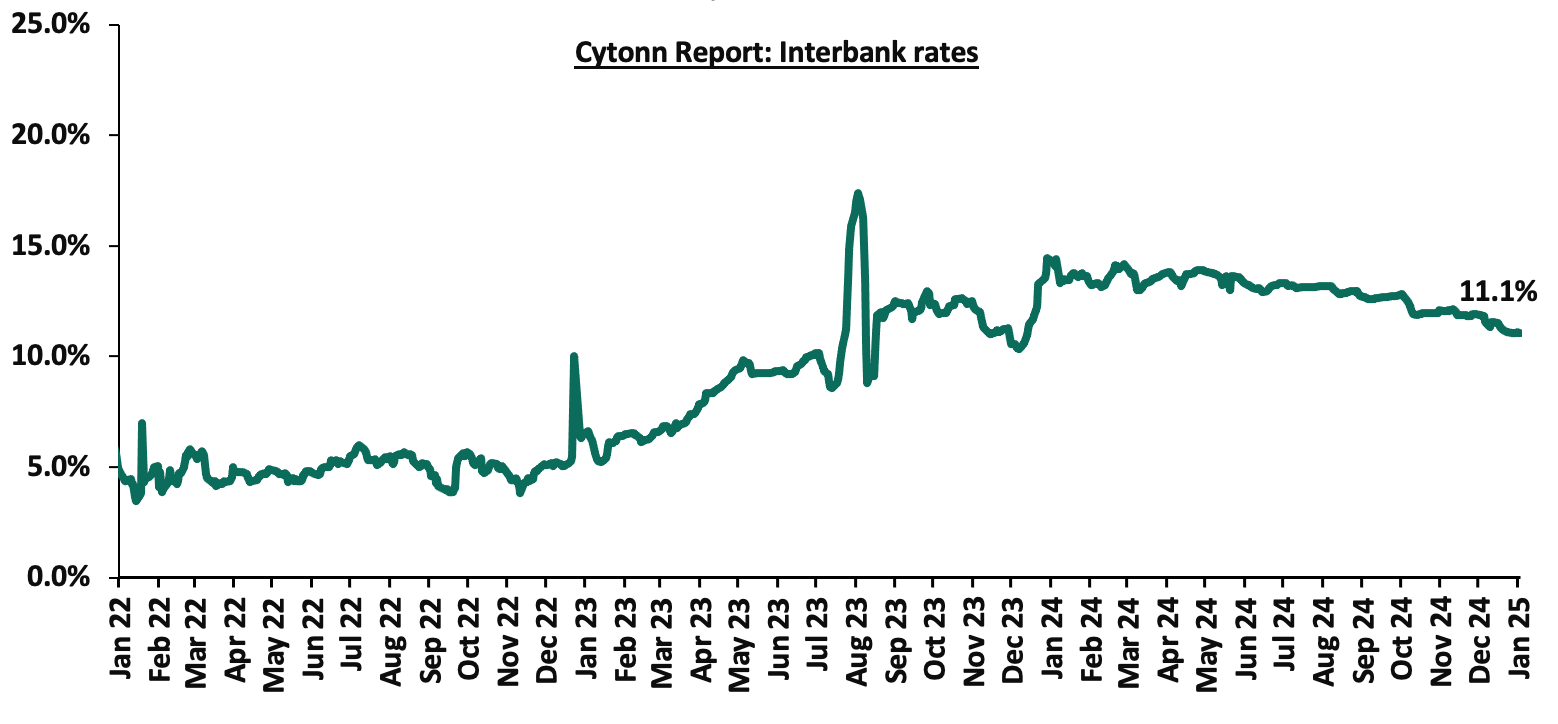

During the year, liquidity levels tightened as evidenced by the increase in the average interbank rate by 3.2% points to 13.0%, from 9.8% in 2023. The tightened liquidity is partly due to tax remittances which offset government payments. However, the average volumes traded in the interbank market increased by 19.1% to Kshs 26.7 bn in 2024, from Kshs 21.6 bn recorded in 2023.

During the week, liquidity in the money markets eased, with the average interbank rate decreasing marginally by 2.0 bps, to remain relatively unchanged at 11.1% recorded the previous week, partly attributable to government payments that offset tax remittances. The average interbank volumes traded decreased by 35.2% to Kshs 22.3 bn from Kshs 34.4 bn recorded the previous week. The chart below shows the interbank rates in the market over the years:

Kenya Eurobonds:

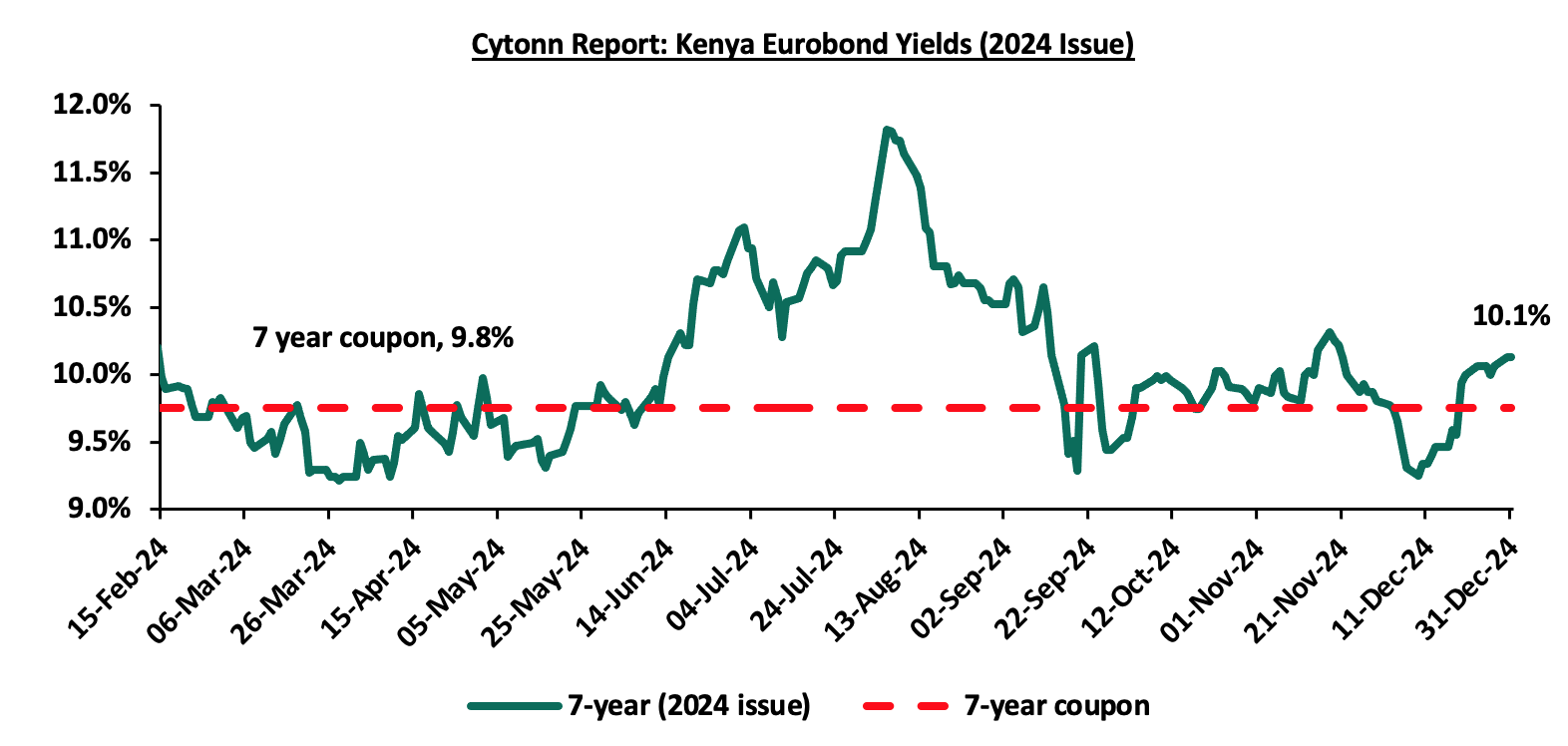

Yields on the 7-Year Eurobond issued in 2024, set to mature in 2031, decreased by 0.1% points to close the year at 10.1%, from 10.2% recorded in February 2024 when it was issued.

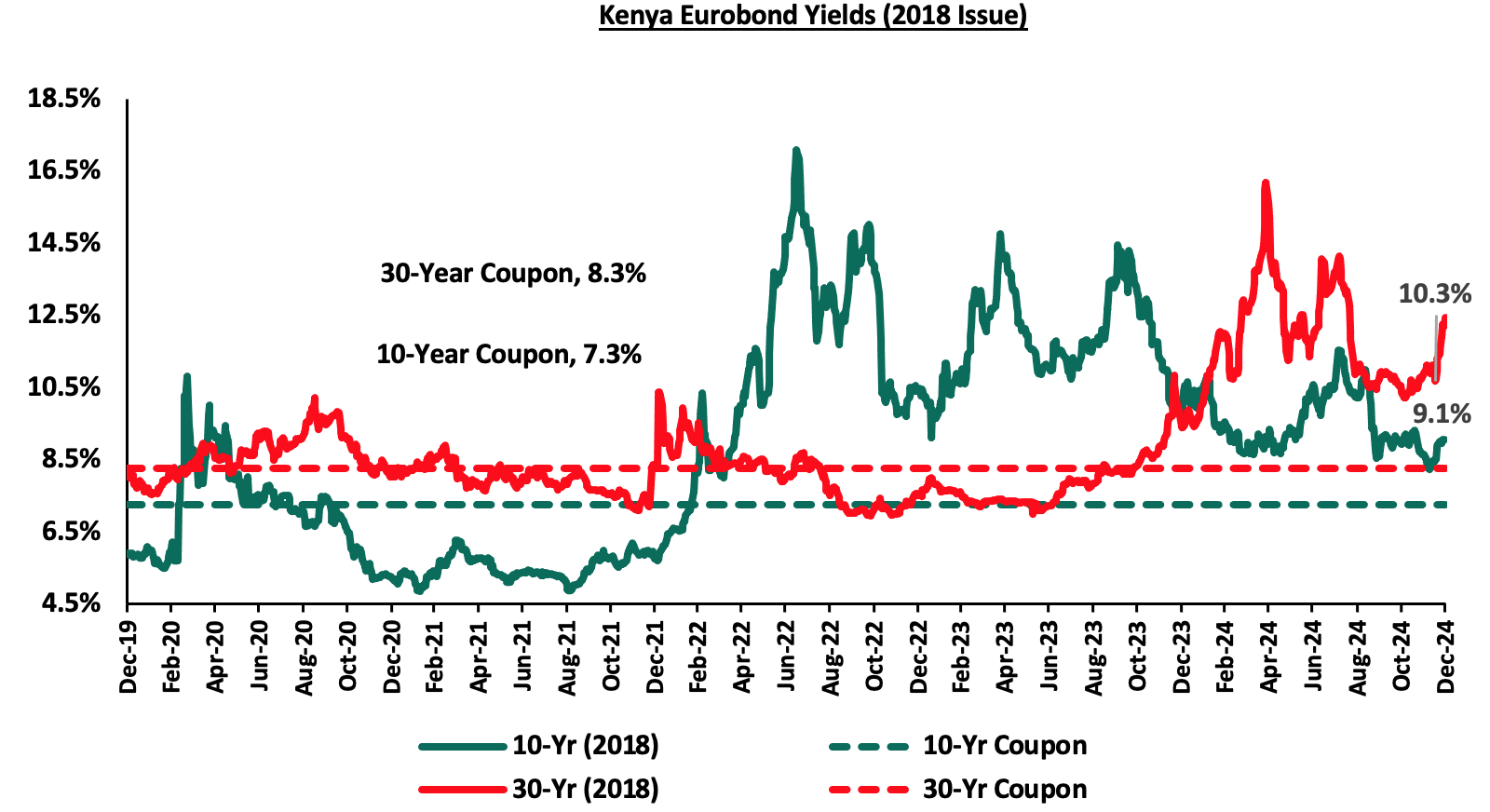

For the 2018 Eurobond issue, the yields on the 10-year Eurobond decreased by 0.8% points to close the year at 9.1% from 9.8% recorded at the start of 2024, while the yields on the 30-year Eurobond increased by 0.1% points to close the year at 10.3% from 10.2% recorded at the beginning of the year.

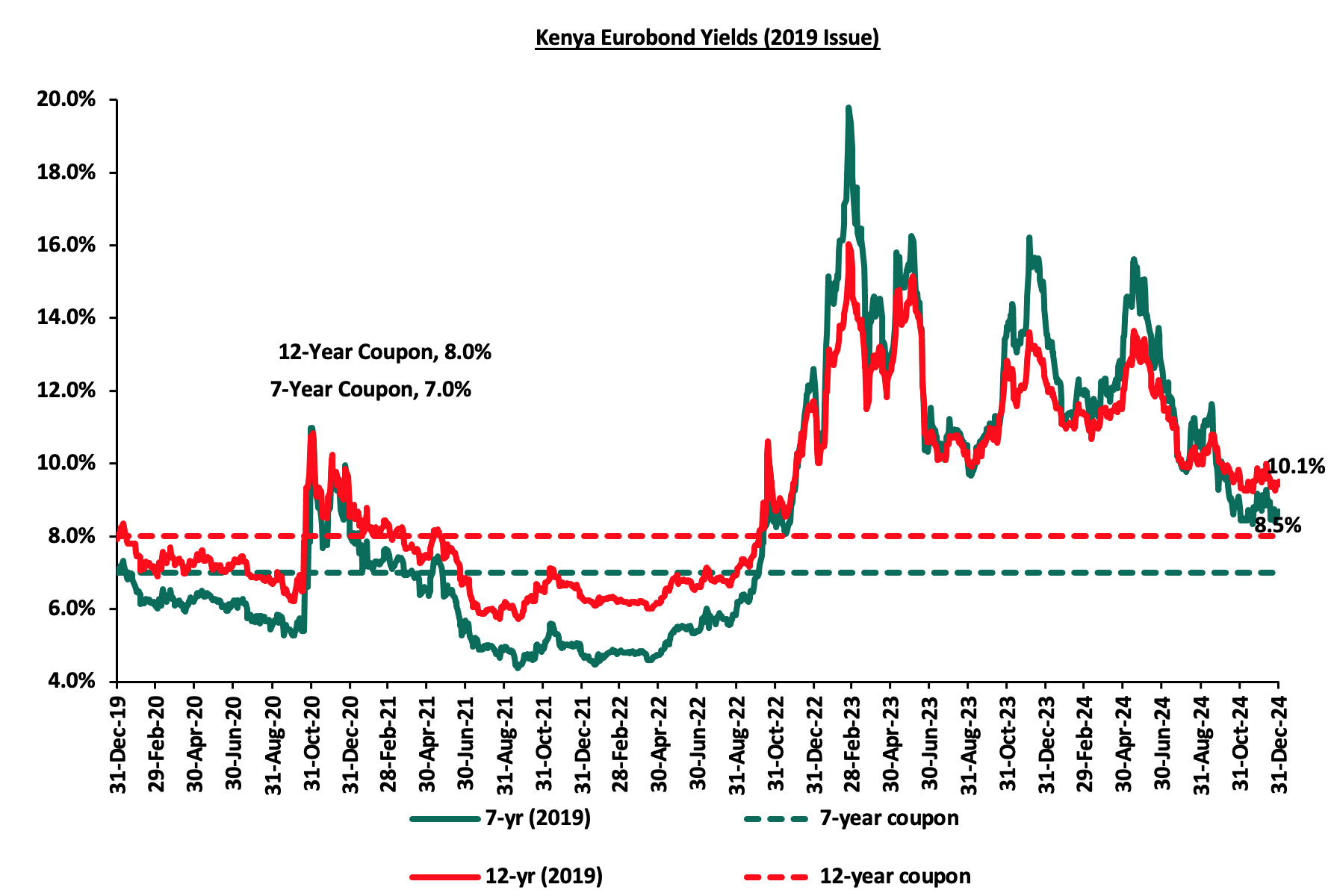

For the 2019 Dual-tranche Eurobond issue, the yields on the 7-year Eurobond decreased by 1.6% points to close the year at 8.5%, from 10.1% recorded at the start of 2024, while the yields on the 12-year Eurobond increased by 0.2% points, to close the year at 10.1% from 9.9% at the beginning of 2024.

The yields on the 12-Year Eurobond issued in 2021, set to mature in 2033, increased by 0.6% points to close the year at 10.1% from 9.5% recorded at the start of the year;

During the year, the yields on Eurobonds recorded mixed performance, with the yields on the 13-year Eurobond issued in 2021 increasing the most by 60.3 bps to 10.1% from 9.5% recorded at the start of the year, while the with the yields on the 7-year Eurobond issued in 2019 decreased the most by 162.4 bps to 8.5% from 10.1% recorded at the start of the year.

However, during the week, the yields on Eurobonds were on an upward trajectory, with the yields on the 7-year Eurobond issued in 2019 increasing the most by 21.6 bps, to 8.5% from 8.3% recorded the previous week. The table below shows the summary of the performance of the Kenyan Eurobonds as of 2nd January 2025:

|

Cytonn Report: Kenya Eurobonds Performance |

||||||

|

|

2018 |

2019 |

2021 |

2024 |

||

|

Tenor |

10-year issue |

30-year issue |

7-year issue |

12-year issue |

13-year issue |

7-year issue |

|

Amount Issued (USD) |

1.0 bn |

1.0 bn |

0.9 bn |

1.2 bn |

1.0 bn |

1.5 bn |

|

Years to Maturity |

3.2 |

23.2 |

2.4 |

7.4 |

9.5 |

6.1 |

|

Yields at Issue |

7.3% |

8.3% |

7.0% |

7.9% |

6.2% |

10.4% |

|

01-Jan-24 |

9.8% |

10.2% |

10.1% |

9.9% |

9.5% |

|

|

29-Nov-24 |

8.6% |

10.1% |

8.0% |

9.7% |

10.1% |

9.8% |

|

26-Dec-24 |

9.0% |

10.2% |

8.3% |

9.9% |

10.0% |

10.0% |

|

27-Dec-24 |

9.1% |

10.3% |

8.5% |

10.1% |

10.1% |

10.1% |

|

30-Dec-24 |

9.1% |

10.3% |

8.5% |

10.1% |

10.1% |

10.1% |

|

31-Dec-24 |

9.1% |

10.3% |

8.5% |

10.1% |

10.1% |

10.1% |

|

01-Jan-25 |

9.1% |

10.3% |

8.5% |

10.1% |

10.1% |

10.1% |

|

02-Jan-25 |

9.1% |

10.3% |

8.5% |

10.1% |

10.1% |

10.1% |

|

Weekly Change |

0.1% |

0.0% |

0.2% |

0.1% |

0.1% |

0.1% |

|

MoM Change |

0.4% |

0.2% |

0.5% |

0.4% |

0.0% |

0.3% |

|

YoY Change |

(0.8%) |

0.1% |

(1.6%) |

0.2% |

0.6% |

- |

Source: Central Bank of Kenya (CBK)

Weekly Highlights

- Inflation Highlight December 2024

The y/y inflation in December 2024 increased slightly by 0.2% points to 3.0%, from the 2.8% recorded in November 2024. This was however in contrary with our projection to a range of 2.4% to 2.7%, where our decision was mainly driven by reduced fuel prices in December, with maximum allowed price for Super Petrol, Diesel and Kerosene decreasing by Kshs 4.4, Kshs 3.0 and Kshs 3.0 respectively, coupled with the stability of the Kenyan Shilling having recorded a 0.3% month-to-date appreciation as of 27th December 2024 to Kshs 129.3 from Kshs 129.6. The headline inflation in December 2024 was majorly driven by increase in prices of commodities in the following categories; Food & Non-Alcoholic Beverages, and Transport sector by 4.8% and 0.2% respectively. However, the commodity prices in Housing, Water, Electricity, Gas & other fuels declined by 0.2%. The table below shows a summary of both the year-on-year and month-on-month commodity indices performance:

|

Cytonn Report: Major Inflation Changes – December 2024 |

|||

|

Broad Commodity Group |

Price change m/m (December-2024/ November -2024) |

Price change y/y (December-2024/December-2023) |

Reason |

|

Food and non-alcoholic beverages |

0.7% |

4.8% |

The m/m increase was mainly driven by the increase in prices of commodities such as maize flour sifted, Fortified maize flour and tomatoes by 7.0%, 5.8% and 1.8% respectively. However, the increase was weighed down by decrease in prices of Mangoes, Potatoes and Cabbages by 6.2%, 5.0%, and 2.8%, respectively |

|

Transport |

1.8% |

0.2% |

The slight m/m increase recorded in the transport index came despite prices of Super Petrol and Diesel decreasing by 2.4% and 1.8% to sell at Kshs 176.3 and Kshs 165.1 respectively, from Kshs 180.7 and 168.1 respectively |

|

Housing, water, electricity, gas and other fuels |

0.2% |

(0.2%) |

The slight m/m increase was mainly driven by an increase in prices of 50 kWh of electricity and 200 kWh of electricity by 0.6% and 0.5% respectively. The increase was however weighed down by decrease in prices of Kerosene by 2.0% to sell at Kshs 148.4, from Kshs 145.4 |

|

Overall Inflation |

0.6% |

3.0% |

The m/m increase was mainly attributable to the 0.7% increase in Food and non-alcoholic beverages. |

Notably, December’s overall headline inflation increased slightly for the second consecutive month, remaining within the CBK’s preferred range of 2.5%-7.5% for the eighteenth consecutive month. The increase in headline inflation in December 2024 comes despite the decrease in maximum allowed price for Super Petrol, Diesel and Kerosene by Kshs 4.4, Kshs 3.0 and Kshs 3.0 per litre respectively to retail at Kshs 176.3, Kshs. 165.1 and Kshs 148.4 per litre respectively, from Kshs 180.7, Kshs. 165.1 and Kshs. 145.4 per litre respectively the last month. Key to note, the Kenya Shilling also recorded a 0.3% month on month gain as of 31st December 2024 to Kshs 129.3 from Kshs 129.7 recorded as of the end of November 2024, and a 17.4% year-on-year gain from the Kshs 156.5 recorded at the end of 2023. The chart below shows the inflation rates for the past 5 years:

Going forward, we expect inflation to remain within the CBK’s preferred range of 2.5%-7.5%, mainly on the back of a strengthened currency and stable fuel prices. Additionally, favourable weather conditions will also contribute to stabilizing food prices, further supporting lower inflation rates. The risk, however, lies in the fuel prices which despite their decline over the last months, still remain elevated compared to historical levels. Key to note is that the Monetary Policy Committee cut the Central Bank Rate by 75.0 bps to 11.25% from 12.00% in its December 2024 meeting, with the aim of easing the monetary policy, while maintaining exchange rate stability, and will meet again in February 2025. This cut in the Central Bank Rate is likely to elevate inflationary pressures as consumer spending rises leading to demand- pull inflation.

Rates in the Fixed Income market have been on a downward trend given the continued low demand for cash by the government and the improved liquidity in the money market. The government is 161.6% ahead of its prorated net domestic borrowing target of Kshs 212.2 bn, and 35.8% ahead of the total FY’2024/25 net domestic borrowing target of Kshs 408.4 bn, having a net borrowing position of Kshs 554.8 bn. However, we expect a continued downward readjustment of the yield curve in the short and medium term, with the government looking to increase its external borrowing to maintain the fiscal surplus, hence alleviating pressure in the domestic market. As such, we expect the yield curve to normalize in the medium-term and hence investors are expected to shift towards the long-term papers to lock in the high returns.

Market Performance

In 2024, the Kenyan equities market was on an upward trajectory with NSE 10 gaining the most by 42.9%, while NSE 25, NASI and NSE 20 gained by 42.5%,34.3% and 33.3%, respectively. Below is a summary of the 2024 annual performance of some of the large-cap stocks in the Kenyan stock market:

|

Cytonn Report: Kenya Equities Performance - Large Cap Gainers and Losers 2024 |

||

|

No |

Company |

Share Price Performance 2024 |

|

1 |

KCB Group |

89.5% |

|

2 |

Standard Chartered Bank |

74.6% |

|

3 |

Absa Bank |

56.3% |

|

4 |

Diamond Trust Bank |

54.2% |

|

5 |

Bamburi |

52.8% |

|

6 |

East Africa Breweries |

51.0% |

|

7 |

Co-operative Bank |

44.9% |

|

8 |

Equity Group |

41.2% |

|

9 |

Stanbic |

29.2% |

|

10 |

NCBA |

24.1% |

|

11 |

Safaricom |

24.0% |

|

12 |

BAT |

(11.5%) |

During the week, the equities market was on an upward trajectory, with NSE 20 gaining the most by 5.4% while NSE 10, NSE 25 and NASI gained by 4.7%,4.0% and 3.2%, respectively. The equities market performance was mainly driven by gains recorded by large-cap stocks such as Co-operative Bank, ABSA Bank, and KCB Group of 11.0%, 9.2% and 7.1%, respectively. The performance was however weighed down by losses recorded by large-cap stocks such as Diamond Trust Bank Kenya, BAT and EABL of 1.8%, 1.2%, and 0.6% respectively.

During the year, equities turnover gained by 22.0% to close the year at USD 0.8 bn, from USD 0.6 bn recorded in 2023. Foreign investors remained net sellers, with a net outflow of USD 16.9 mn, compared to net outflows of USD 92.0 mn recorded in 2023. The foreign-investor outflows during the year can be largely attributed to investors fleeing emerging markets such as Kenya, to advanced economies such as United States and United Kingdom following interest rate hikes as well as increased concerns about macroeconomic deterioration in emerging markets.

During the week, equities turnover increased significantly by 97.3% to USD 4.2 mn from USD 2.1 mn recorded the previous week, taking the YTD turnover to USD 2.5 mn. Additionally, foreign investors remained net sellers for the third week, with a net selling position of USD 0.6 mn, from a net selling position of USD 0.9 mn recorded the previous week, taking the YTD net selling position to USD 0.1 mn.

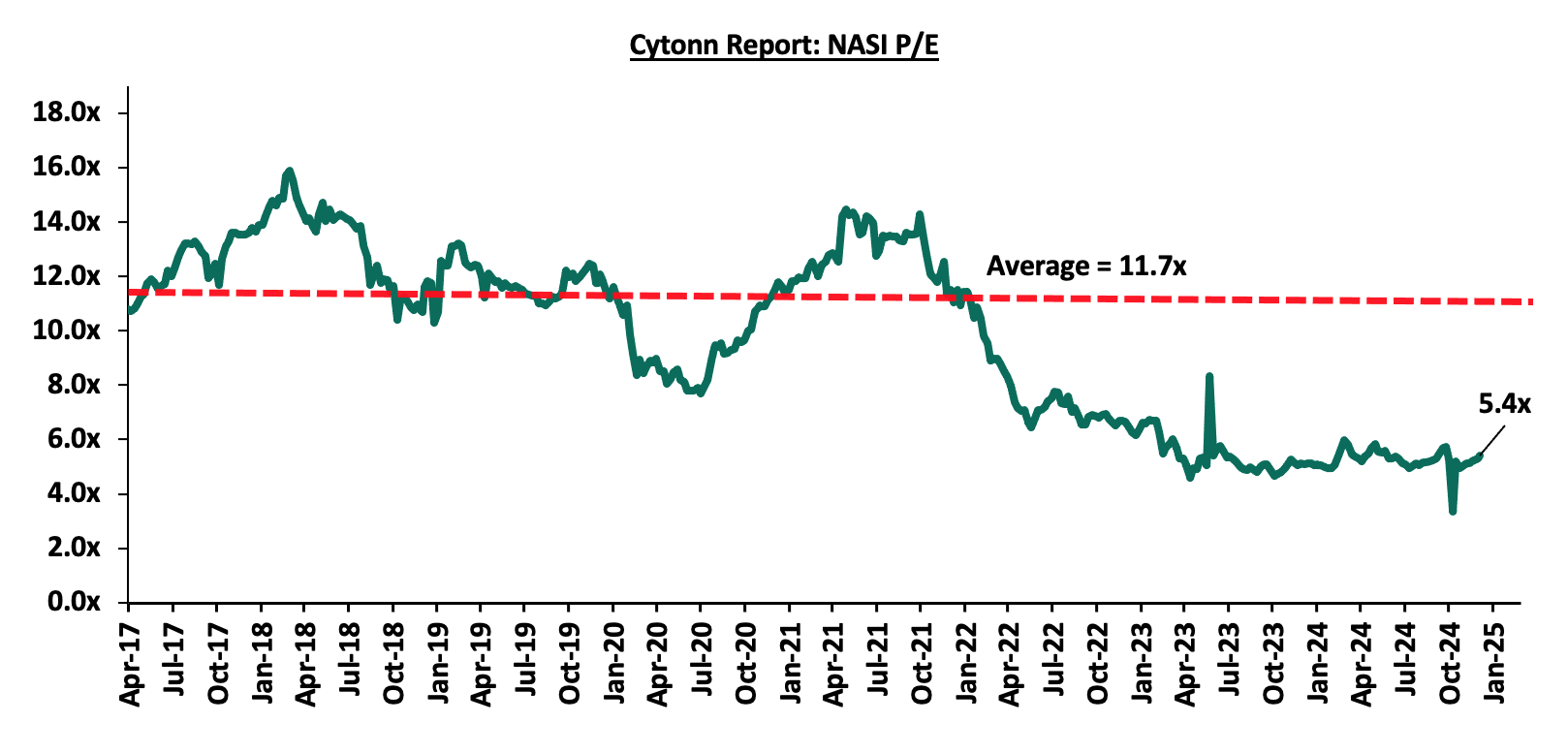

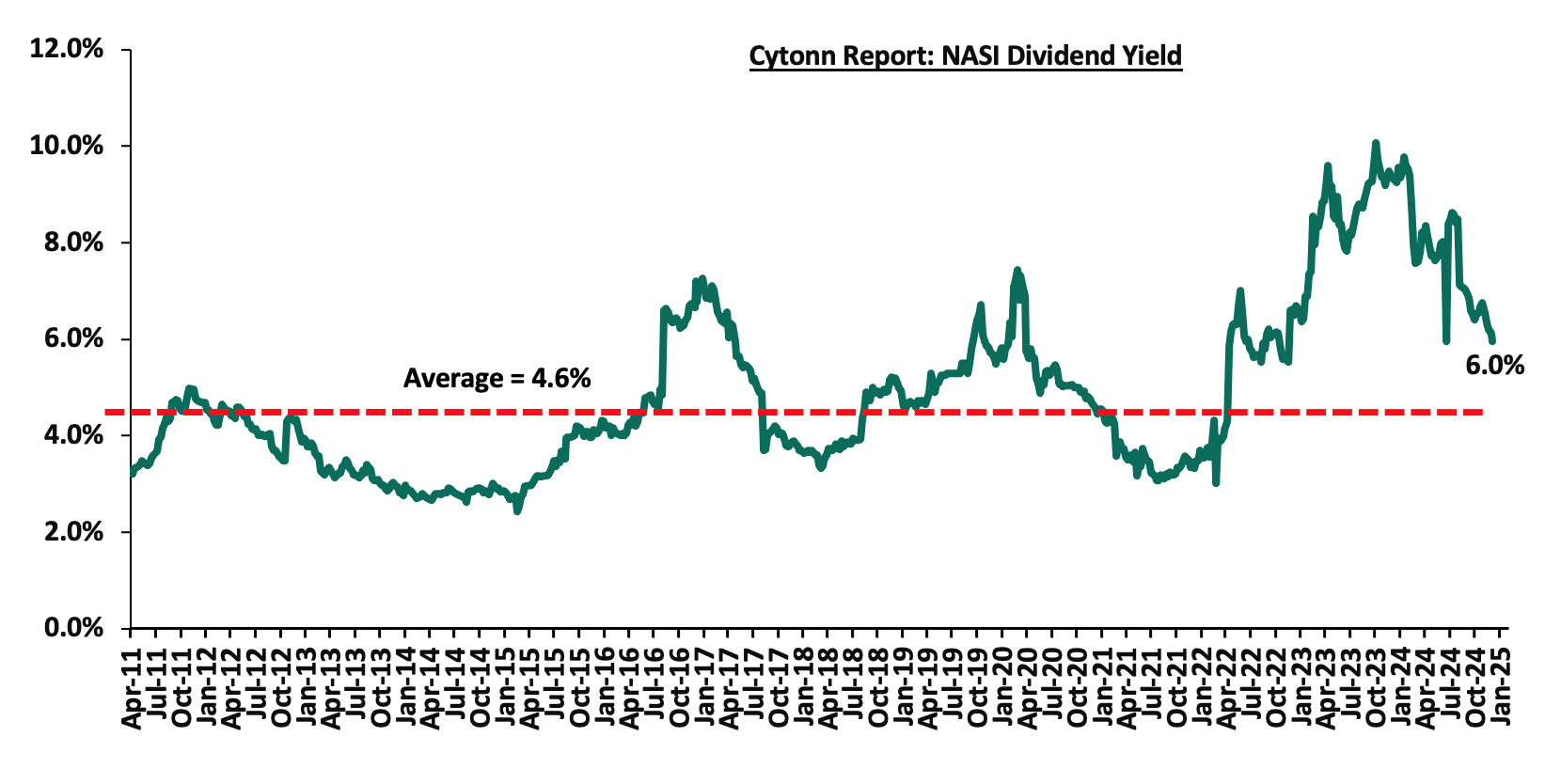

The market is currently trading at a price-to-earnings ratio (P/E) of 5.4x higher than 5.1x recorded at the end of 2023, and is 53.7% below the 15-year historical average of 11.7x. NASI’s P/E ratio remained boosted for the majority of the year, mainly attributable to a rise in price of large-cap stocks such as Safaricom whose price rose by 24.0% during the year. Safaricom continues to be a key part of Kenyan equities portfolios, accounting for 39.0% of Nairobi Stock Exchange (NSE’s) market capitalization, and has dominated both the market turnover and determines the direction of the market given its weight and liquidity in the Nairobi Securities Exchange. On the other hand, the dividend yield is currently at 6.0%, 1.3% points above the historical average of 4.6%.

Key to note, NASI’s PEG ratio currently stands at 0.7 an indication that the market is undervalued relative to its future earnings growth. The charts below indicate the market’s historical P/E and dividend yield:

2024 Key Highlights

- Banking Sector Earnings

According to the Q3’2024 banking results core earnings per share (EPS) for the listed banks recorded a weighted growth of 24.6% in Q3’2024, compared to a weighted growth of 11.2% recorded in Q3’2023, an indication of sustained performance supported by improved operating environment experienced in Q3’2024 on the back of easing inflationary pressures and a strengthening Shilling. The table below highlights the performance of the banking sector, showing the performance using several metrics, and the key take-outs of the performance.

|

Cytonn Report: Kenyan Listed Banks Performance Q3’2024 |

|||||||||||||||

|

Bank |

Core EPS Growth |

Interest Income Growth |

Interest Expense Growth |

Net Interest Income Growth |

Net Interest Margin |

Non-Funded Income Growth |

NFI to Total Operating Income |